Dollar Competitiveness (Part I)

The US Dollar has been “strong” on foreign exchange markets for the past six months, with the USD Index having risen from 79 to 88, a gain of almost 11½%. That’s an increase in the value of the Dollars in your pocket (or bank account) compared to the currencies of our major trading partners around the world. If the value of your money could grow at a 23% annual rate year after year, you’d be rich in no time flat.

The US Dollar has been “strong” on foreign exchange markets for the past six months, with the USD Index having risen from 79 to 88, a gain of almost 11½%. That’s an increase in the value of the Dollars in your pocket (or bank account) compared to the currencies of our major trading partners around the world. If the value of your money could grow at a 23% annual rate year after year, you’d be rich in no time flat.

Alas, this is not the way the world works. The Dollar got down to 79

after it fell from 88 in June 2010. And, in March 2002, the Dollar index stood at 120! That’s a loss in the value of the Dollar versus other currencies at almost a 3% per year rate.

The value of a country’s currency is affected by a number of factors, mostly controlled by the government. One of these is the Interest Rate compared to rates in other countries. If all else were equal (it never is, but let’s assume), then people would tend to send their money wherever rates were highest. If you could get a 10% rate in country A vs only a 1% rate in country B, you would tend to send your money to country A.

The US FED has kept interest rates very low for several years, but recently the Eurozone Central Bank and the Japanese Central Bank have made local interest rates even lower. So, money will tend to leave Japan and the Eurozone and go toward the US, pushing up the Dollar.

Investors look not only for a high Return on Investment but also want to assure the Return of their Investment. They look at the credit-worthiness of the borrower. Since most foreign money goes into a country’s Treasury debt, the more of this debt a country has compared to GDP, the less likely the debt will be repaid. (In the PIIGS countries – Portugal, Ireland, Iceland, Greece, and Spain – interest rates frequently have gotten to be 5% or more compared to US rates.) So, a country’s ability to repay the debt affects the foreign exchange rate.

The ability to repay also depends on whether the tax base (the GDP) is growing or declining. A growing Economy can generate higher tax revenues, so it is deemed more credit-worthy. Regulation and Bureaucracy loom large in determining if an Economy can grow or not. As stifling as these are in the US, they are worse in Europe.

When a country has a large National Debt – too large to repay – the country likely will default. A formal default – “We ain’t gonna pay you!” – is only one way. Most times a country will choose to repay in a debased currency, and they do this by printing more and more paper money. Today, most countries are complaining that Inflation is too low. They’re telling all who hear that they want to cheat their creditors of the capital they have invested.

A government may manipulate the data that they report on the Economy. They may adjust the way they calculate price increases – in the US the official CPI is rising 2% today, but using the 1980s methodology, the CPI would be closer to 10% annual increases. This makes real, after inflation, GDP look larger, making the country appear more credit worthy.

Even though

- The US FED has been manipulating interest rates lower than the Free Market rate

- The US Government has run Budget Deficits since Eisenhower was President (Treasury debt actually grew every year under Clinton, so the surplus wasn’t real)

- The US National Debt, currently around $18 Trillion is not repayable in constant Dollars (a default MUST happen)

- US CPI is rising at an almost 10% annual rate (base on the 1980 methodology)

- The US Fed has ramped up money printing (the FED’s Balance Sheet has grown about 5 times in 6 years)

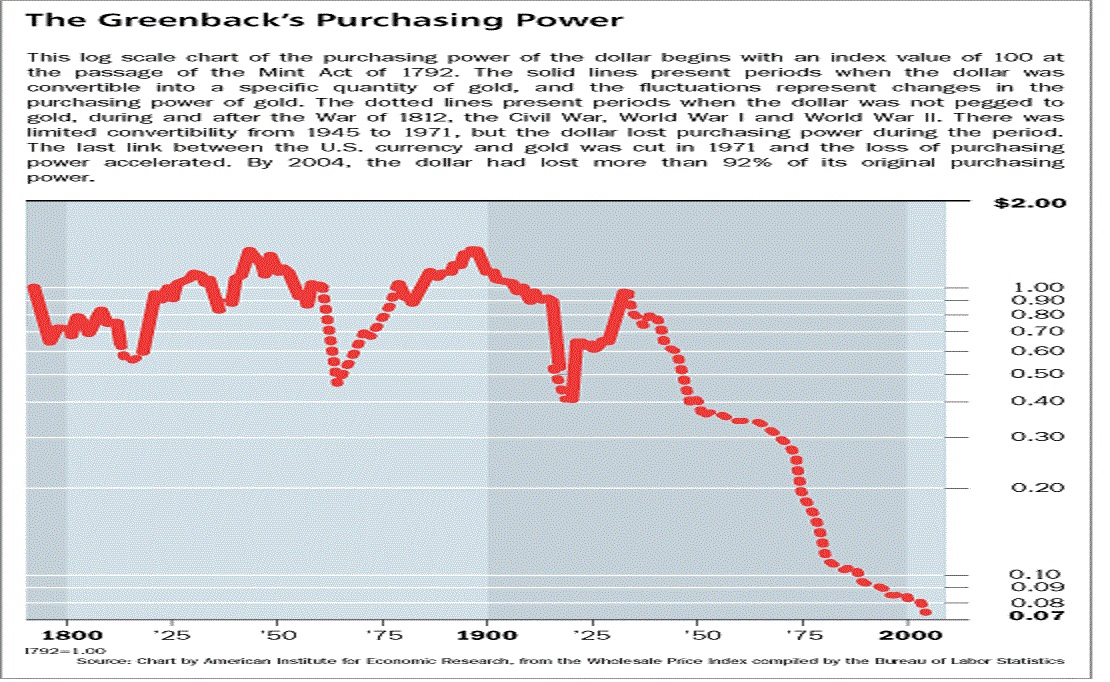

the Dollar has been up over the last 6 months because other countries have worse records. Long term (60 years) the Dollar has tanked against most of our trading partners. Long term, all Americans have lost a massive amount of purchasing power due to government policies which have cheapened the Dollar for generations.

If we hope to remedy this disease, we need to see who wins and who loses from these policies. As “Deep Throat” said, “Follow the money!”

In Part II tomorrow, we’ll look at the winners and losers.

Robert (Bob) Shapiro is self-taught in Austrian Economics and has consulted briefly for the governments of Mexico, Greece, Portugal and Spain. He has traded Gold & Silver and their stocks since 1970. Bob Shapiro’s blog is http://us-issues.com

Robert (Bob) Shapiro is self-taught in Austrian Economics and has consulted briefly for the governments of Mexico, Greece, Portugal and Spain. He has traded Gold & Silver and their stocks since 1970. Bob Shapiro’s blog is http://us-issues.com