The Dow In 1937 vs Today…Warnings From The Past

Much has been discussed, about has happened to the world since 2008, and many investors today are anchoring to the most recent crash in 2008-09. A new crop of investors never even experienced a true crash. But the next crash is never the same as the last crash. The solutions to end the last crash, are typically the fuel and causes for the next crash. Even in the 1930s, after the 1929 crash, investors were waiting for a next similar type of crash. Ray Dalio and the team at Bridgewater have stated, that we are currently going through a 1937 type of environment in relation to the economic and political cycles. The next questions remain: “What happened to the Dow Jones Industrial Average during 1937-1938? What happened to the US Economy in 1937-1938? Did the US enter a recession? Did the Central Banks save the world?

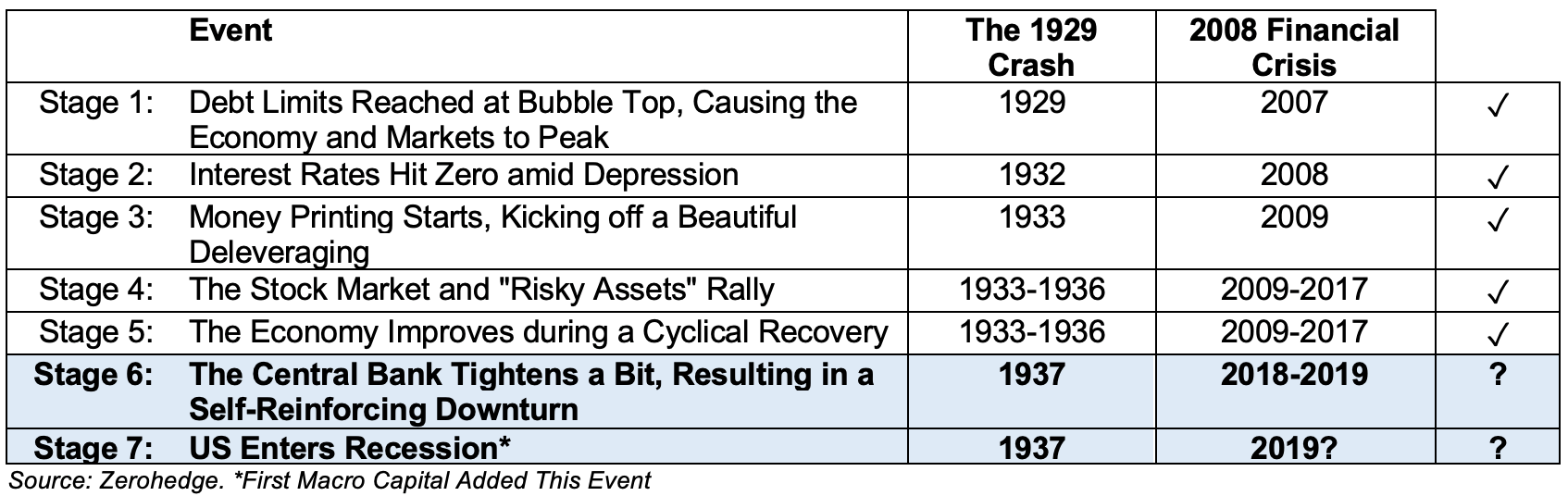

The 1929 Crash vs 2008 Financial Crisis

When we look at the stages from the peak of 1929 to the crash, the Great Depression, then followed by the next business cycle, which then ended in 1937. We can see the similarities of today’s current business cycle to 1929. And where are we today? Stage 6: “Central Bank Tightens a bit, resulting in a self-enforcing downturn.”

Stages of the Cycle as Per Ray Dalio from 1929 Crash vs 2008 Crash

What was the Federal Reserve Policy Mistake That Caused the 1937 Crash?

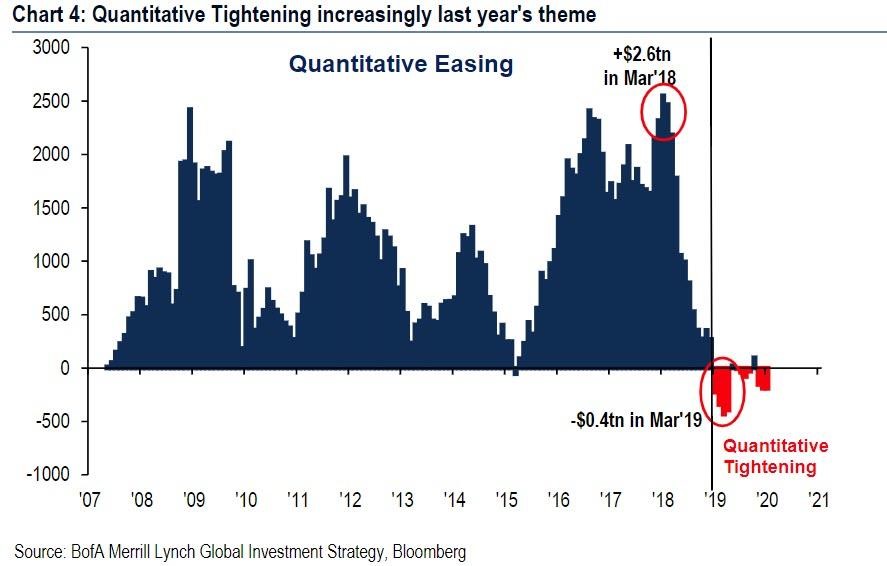

When we talk about the massive amount of liquidity being withdrawn by Central today, not unlike the halt in monetary expansion in 1936, which is very similar to the policy decision to reduce central bank balance sheets. We can see in the following chart, the Federal Reserve monetary expansion growth stopped.

“There is a natural tendency for policymakers to pull back on accommodation too early before the real rate of interest has fallen to low enough levels. Such errors happened in 1937 when the Fed prematurely withdrew accommodation.” - Chicago Fed President Charles (2012), Federal Reserve History

“The Fed’s contractionary policy was complemented by the Treasury’s decision, in late June 1936, to sterilize gold inflows in order to reduce excess reserves. The sterilization policy severed the link between gold inflows and monetary expansion. By preventing gold inflows from becoming part of the monetary base, this policy abruptly halted what had been a strong monetary expansion.” Federal Reserve History.

US money supply (M2), 1934-39

Source: https://voxeu.org/

THE FED IS CAUGHT IN THE SAME TRAP TODAY LIKE 1937

While the future never exactly repeats, it sure does rhyme? As Central Banks around the world are unwinding their Mount Everest size balance sheets, even if they pause rising interest rates. The massive withdrawal of liquidity will be pulling the oxygen out of the financial markets, “the Fed’s balance sheet rose from $900bn in 2008 to $4300bn in 2018. It is likely to drop only as far as $2900bn by the end of 2020” (FT). This is a 33% drop in the size of the Fed’s balance sheet and if you look to history, there is no guarantee it will drop by that much if we head into a recession in 2019 because the Fed may have to inject more liquidity back into the system by then. We will wait and see.

THE GHOSTS OF THE DOW IN 1937

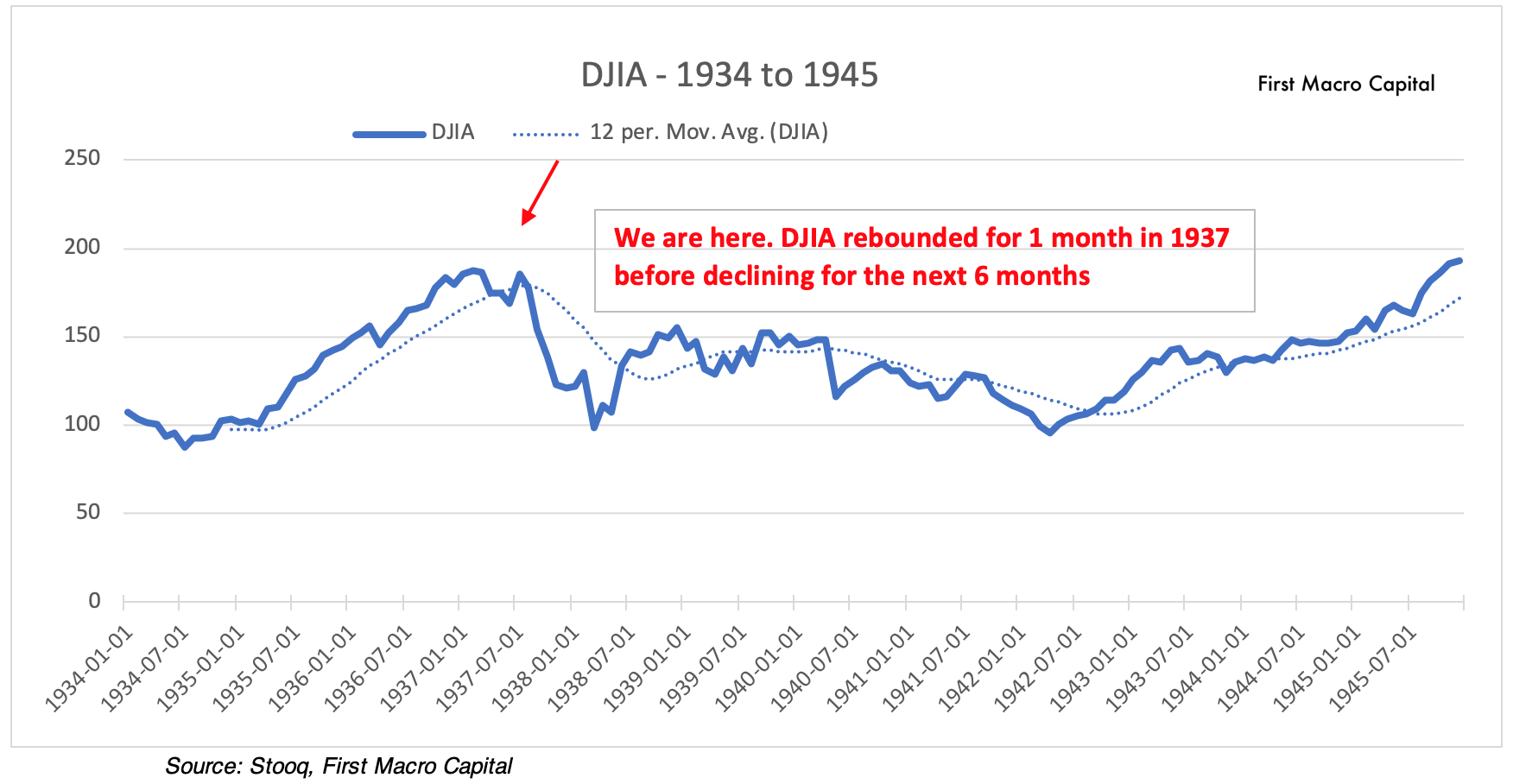

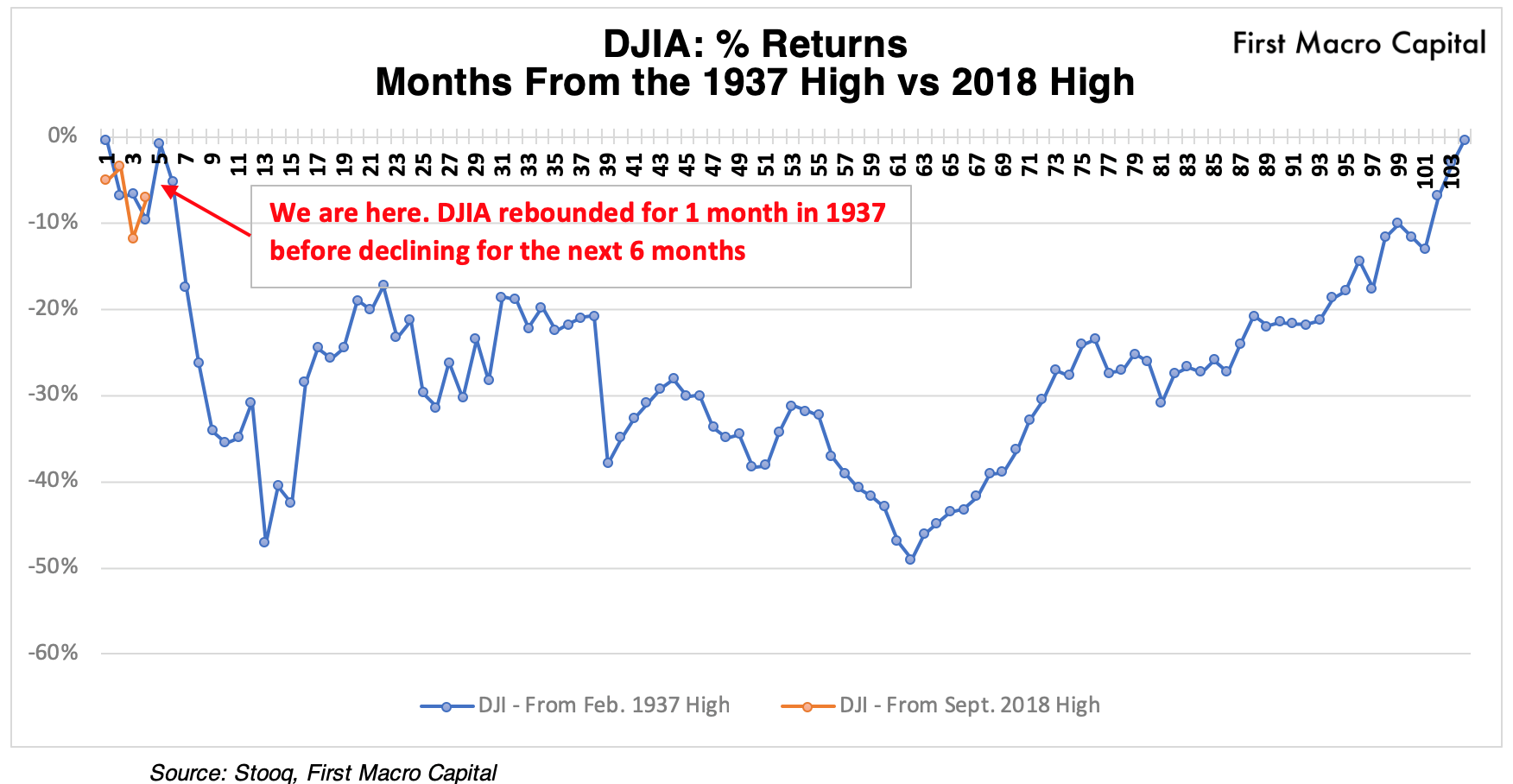

The Dow peaked in February 1937 and then fell by ~10% over a four-month period. It then recovered for a month, then went down by almost 10% from its high and recovered for a month before crashing by almost 50% for the next 8 months. The Dow Stayed range bound for the next 103 months. The US entered a recession three months later in May 1937, and it lasted for 13 months. US GDP declined by 18.2%, making it one of the deepest recessions over the 20th and 21st centuries. The recession of 2008 lasted for 19 months and GDP decreased by 5.2% [bea.gov].

SO WHERE ARE WE TODAY?

If we assume the high is in for the Dow Jones Industrial Average in September 2018, which then decreased by more than 10% over the next three months, before rallying higher this past month. So far the Dow is repeating the path of 1937, and this recent rally may be only a bear market trap for investors. It is a reminder to be cautious as 1937 shows just how quickly things can deteriorate as the Dow Jones Industrial average dropped by almost 50% in 8 months because of the Fed policy being caught. Consumer Discretionary and technology underperform more than other sectors late in the cycle, and technology continues to underperform during the recession stage. Apple demand has dropped off, which we previously have written about. If industrials underperform going forward than this would highlight a slowdown is in the cards.

If industrial order books outlook slows over the next six months, then industrial stocks will underperform more than most sectors, confirming we are at the recessionary stage of the cycle because of demand falling over.

RECESSION IN THE CARDS FOR 2019

If we look back at past market tops, historically recessions start within 1-13 months from the market top. This would put a recession in the cards for the US between October 2018 to October 2019. When looking at the J.P. Morgan Global Composite PMI has now hit 27-month lows, and we would expect to further deteriorate in 2019 as the US shutdown continues, sentiment surveys (Consumer, Business, CEO) deteriorate, and both US manufacturing and non-manufacturing PMIs decelerate. We also expect jobless claims to accelerate in the weeks ahead as we have seen manufacturing companies increase layoffs over the past two months, from GM, Ford, and has only increased in January 2019.

2019 has started off with a boom, but there is still more than 90% to go to end 2019, and there is still a lot that can happen until the end of the year. If 1937 is to repeat, further economic deceleration is in the cards for 2019 that many investors should be prepared for. A Fed policy mistake from Central because of the liquidity withdrawal looks increasingly probable, and the consequences to the markets are high. Here is to 2019, keep your eyes open and be flexible.

Paul Farrugia, BCom. Paul is the President & CEO of First Macro Capital. He helps his readers identify mining stocks to hold for the long-term. He provides a checklist to find winning gold and silver mining producer stocks, including battery metals.

Disclaimer

The information contained herein is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your financial situation – we are not investment advisors, nor do we give personalized investment advice. The opinions expressed herein are those of the publisher and are subject to change without notice. It may become outdated, and there is no obligation to update any such information.

Investments recommended in our publications, blog posts, emails, online communications, or any online contents published by any party of First Macro Capital and its affiliated companies should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company in question. You should not make any decision based solely on what you read here.

First Macro Capital writers and publications do not take compensation in any form for covering those securities or commodities. First Macro Capital employees and agents of First Macro Capital and its affiliated companies own some of the stocks mentioned in this article, prior to the writing of this article.

*********