The Dow Jones at 116,000? Good Grief!

At market tops, bullish enthusiasm alters society’s brain chemistry to the point where what should be ridiculed becomes widely acceptable to the cattle rushing towards a terrible day of reckoning. Case in point is the following video, where 116,000 is taken as a serious possibility for the Dow Jones Industrials.

Now the basis for this seems rational; an average increase of 7% per year will raise the Dow Jones to 116K sometime in the next few decades. But never asked is where the 7% per year on average is coming from; it’s coming from the Federal Reserve’s Open Market Committee’s (FOMC) open market operations. The 116,000 Dow Jones will be valued in dollars that will be greatly depreciated from the dollars that prices today’s 15,000 Dow Jones.

The FOMC isn’t doing anything today it hasn’t done for decades; purchasing debt with dollars that it creates but shouldn’t exist. Over the decades, the FOMC has changed the financial landscape by facilitating the expansion of un-payable debt at all levels of society that it is responsible for. Paul Volcker in the late 1970s and early 80s could and did raised the Federal Reserve’s Fed Funds Rate above 20%, taking long term US Treasury’s yields to 15%. Three decades ago this was immensely painful, but not fatal to the global economy.

This is not possible today. With the creation of the OTC derivatives market, promoted by Alan Greenspan and Robert Rubin in their 1999 Congressional Testimony, a return of the Fed Funds rate of 5%, and 7% for the 10Yr T-Bond, would bring into the money tens, if not hundreds of trillions in interest rate derivatives that the global banking system is liable for, but can’t possibly honor. These potential obligations of the banking system are so immense that when they come into the money, and they will, the ability of the US Government to come to the aid of their banking system will be overwhelmed.

To accept the possibility of the Dow Jones at 116K in the decades to come, one must accept that what is now considered business as usual in Washington and Wall Street (out of control spending financed by ever expanding Treasury debt, with the Federal Reserve monetizing much of Congress’s un-payable bills) can continue for many years to come.

But believing our leveraged to the hilt financial system can continue pushing ever increasing levels of debt on governments, commerce and private citizens for decades to come isn’t a reasonable assumption, as the banks’ customers are having problems servicing their current levels of debt. And if I’m wrong and the world’s economy is willing and able to absorb, say an additional $150 trillion in US Treasury debt in the next two decades, with the Federal Reserve monetizing half of it, why should anyone expect that the value of the Dow Jones would rise as fast, or faster than the increase in the supply of dollars? The Dow Jones has failed to do so in the past.

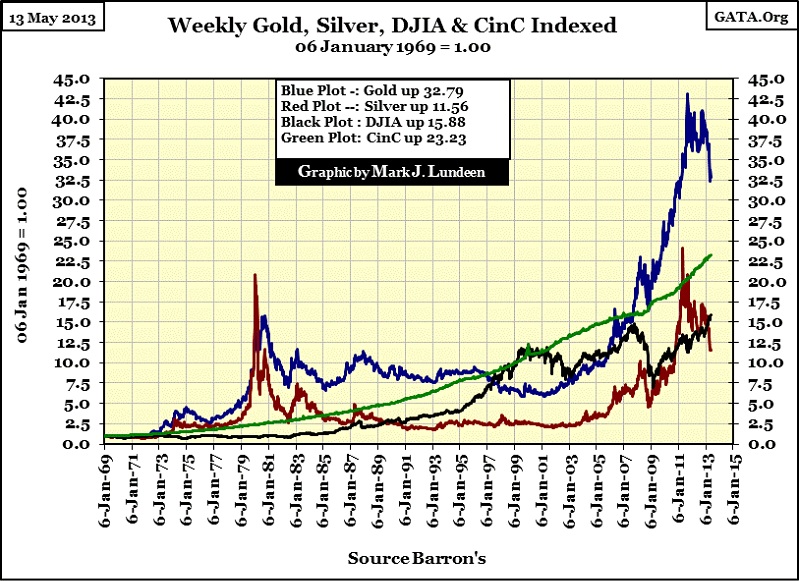

To make my point, here is a chart plotting the indexed values of the Dow Jones (Black Plot), US Currency in Circulation (CinC; Green Plot) and the old monetary metals from 1969. Except for the Dow Jones market top from 1997-2000, since 1969 the Dow Jones has failed to keep up with the growth in monetary inflation, though you can be sure that the increase in the Dow Jones from 950 in January 1969 to now over 15,000 in May 2013 was an inflationary consequence of the FOMC. Note that holding gold (Blue Plot) since 1969 has actually benefitted investors from inflationary increases in CinC, unlike the Dow Jones. But does today’s $15,000 in income, wages or the Dow Jones purchase more than $950 did in 1969? After debt service and taxes, I’d say no! Why would having the Dow Jones “grow” to 116K in 2050 benefit future investors any more than has the increase from 950 in 1969 to 15,000 today?

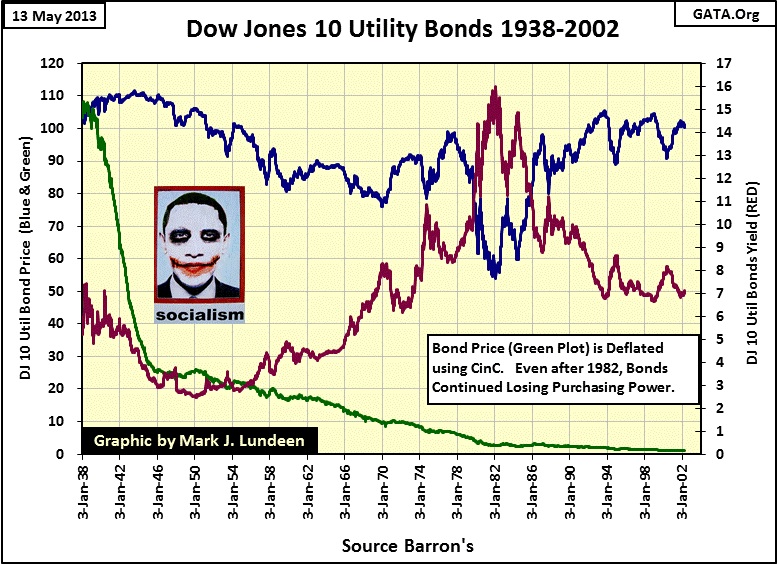

But at least the price of dividend yielding blue-chip stocks has increased with inflation in past decades, as did their cash-dividend payouts, if not on a 1 for 1 basis. It’s a totally different story for fixed income investments like bonds, as can be seen with the now discontinued Dow Jones 10 Utility Bond Average (DJ 10 Util Bd) published from 1938 to 2002. The DJ 10 Util Bond Average’s published price is plotted in blue. The Green plot shows the DJ 10 Util Bond Average’s valuation deflated with CinC, and shows how seriously economists at the Federal Reserve take their “dismal science” when it comes to the bond market.

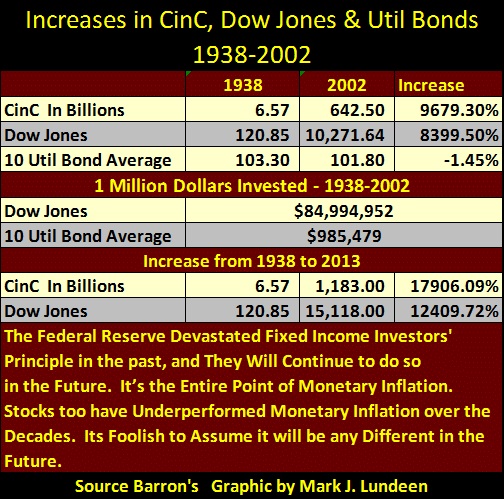

Note that over time the relationship between bond prices and yields are not fixed as the bonds used in constructing this Average in 1938 were replaced with bonds with higher coupons over time. But still when Dow Jones Inc. discontinued publishing this data in April 2002, the DJ 10 Util Average’s price and yield were about the same as they were in 1938, but after six decades of monetary inflation that’s horrible. Look at the table below for the specifics. From January 1938 to April 2002, both CinC and the Dow Jones increased by two orders of magnitude, though CinC inflation is up more than the Dow Jones. But from its first to its last published price (sixty four years between the two), the DJ 10 Util Bond Average lost $1.50. But In 1938 $1.50 was a good hourly wage for skilled labor. In 2002 a $1.50 didn’t buy a large cup of coffee at Starbucks, thanks to the FOMC.

Note that over time the relationship between bond prices and yields are not fixed as the bonds used in constructing this Average in 1938 were replaced with bonds with higher coupons over time. But still when Dow Jones Inc. discontinued publishing this data in April 2002, the DJ 10 Util Average’s price and yield were about the same as they were in 1938, but after six decades of monetary inflation that’s horrible. Look at the table below for the specifics. From January 1938 to April 2002, both CinC and the Dow Jones increased by two orders of magnitude, though CinC inflation is up more than the Dow Jones. But from its first to its last published price (sixty four years between the two), the DJ 10 Util Bond Average lost $1.50. But In 1938 $1.50 was a good hourly wage for skilled labor. In 2002 a $1.50 didn’t buy a large cup of coffee at Starbucks, thanks to the FOMC.

The true scope of this bond market investment disaster can be seen by noting what happened to $1 million dollars invested in the Dow Jones Industrial and high grade utility bonds from January 1938 to April 2002. The Dow Jones increased by a factor of 85 as the DJ 10 Util Bond Average actually lost a $1.50 in nominal dollar terms. Sure, no one in 1938 purchased bonds for capital gains. Bonds were, and are still typically purchased for income. But the monetary inflation our current financial system is based on, consumed most of the purchasing power of each 1938 dollar invested in the bond market over time. The stock market too has failed to protect investors from the predation of the Federal Reserve. As seen in the last section of the table above, since 2002 CinC has increased from 642 billion to 1.183 trillion dollars; almost a double. But the Dow Jones is far behind this increase in CinC inflation.

But we can’t blame Doctor Bernanke for any performance short-fall in the stock market. He and his banking system are trying as best they can to drive stock valuations upward. In fact the good doctor has for the third time since 1982 succeeded in inflating an inflationary bubble in the stock market.

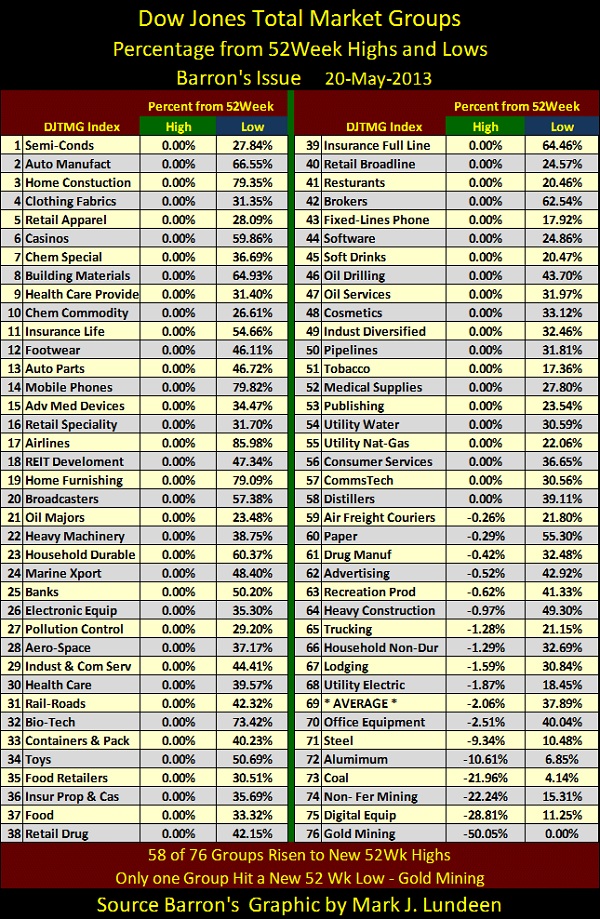

The table below lists how far the 76 DJTMG indexes I follow (weekly closing price basis) are from their 52 Wk highs and lows. A 0.00% marks a new 52Wk high (Green Column) or 52Wk low (Blue Column). At Friday’s close, a fantastic 58 of the 76 indexes made new 52Wk highs, with only one making a new 52Wk lows – gold mining. I’m not surprised as Doc B and his banking system really hate the gold miners, and after all this bull market is their show. That said, look at how far down the list we have to go to see one of these indexed more than 1% from a new 52Wk high: down to #65, and not until #72 do we see an index more than 10% from a new 52Wk high. What we are seeing below is a real valuation stampede in the stock market, courtesy of the Federal Reserve and its QE to Infinity! But like Alan Greenspan’s stock market bubbles, this too shall end in tears for most retail investors. I just can’t say exactly when the party is going to end.

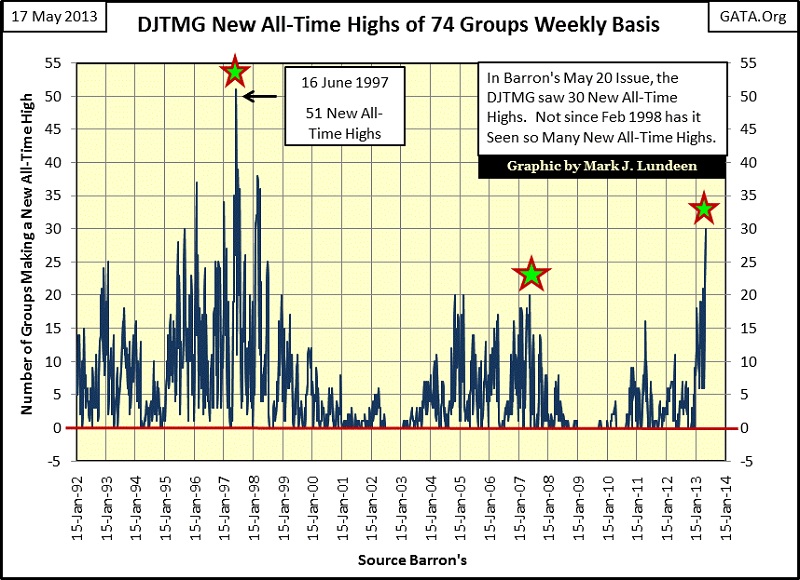

Seeing all these stock market groups making new 52Wk highs during a time when nothing is working right in Washington, Wall Street or down the street from where you live is crazy; but not as crazy as looking at the DJTMG’s new ALL-TIME HIGHS. Why do I say this? Well look at the chart below displaying new all-time highs for the Dow Jones Total Market Groups for the past 21 years. The last time the DJTMG saw 30 groups making new all-time highs was in February 1998, when the economy was described as a “Goldie-Locks Economy” as everything economically speaking was “just right” (not to hot and not to cold). Also, most people were actually happy back then, thinking of how they were going to spend their retirement years in luxury after selling their high tech stocks.

Seeing all these stock market groups making new 52Wk highs during a time when nothing is working right in Washington, Wall Street or down the street from where you live is crazy; but not as crazy as looking at the DJTMG’s new ALL-TIME HIGHS. Why do I say this? Well look at the chart below displaying new all-time highs for the Dow Jones Total Market Groups for the past 21 years. The last time the DJTMG saw 30 groups making new all-time highs was in February 1998, when the economy was described as a “Goldie-Locks Economy” as everything economically speaking was “just right” (not to hot and not to cold). Also, most people were actually happy back then, thinking of how they were going to spend their retirement years in luxury after selling their high tech stocks.

But that was fifteen years ago; today the markets and the economy begin to slip into withdrawal symptoms without a daily “injection” of “liquidity” from Doctor Bernanke. For many people, especially union construction workers, these are not good times. Unlike 1998, if people lose their jobs today, they just may stay unemployed. And then there is the pending Obama Health Care program – that’s a real economic wrecking ball coming our way. So why are 30 DJTMG indexes at new ALL-TIME HIGHS? The FOMC is actively inflating financial asset valuation so that politicians can say that all is right with the world, and your retirement accounts.

But that was fifteen years ago; today the markets and the economy begin to slip into withdrawal symptoms without a daily “injection” of “liquidity” from Doctor Bernanke. For many people, especially union construction workers, these are not good times. Unlike 1998, if people lose their jobs today, they just may stay unemployed. And then there is the pending Obama Health Care program – that’s a real economic wrecking ball coming our way. So why are 30 DJTMG indexes at new ALL-TIME HIGHS? The FOMC is actively inflating financial asset valuation so that politicians can say that all is right with the world, and your retirement accounts.

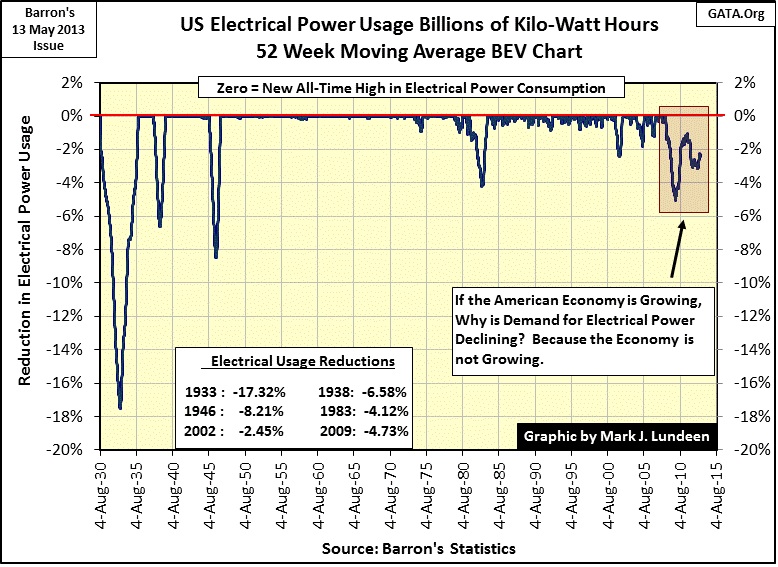

I don’t care what the government says about “economic growth”, business conditions and employment prospects in the United States have been awful for the past five years. The next chart plots electrical power consumption (EP) for the United States since 1930, and it shows the economic reality that Washington’s statisticians are paid to cover up, the United States’ economy is at risk of slipping into another depression because of the housing blunder Washington and Wall Street inflicted on the economy from 2002-07. Not a single new all-time high in US EP since August 2008, the month before the beginning of the credit crisis to today.

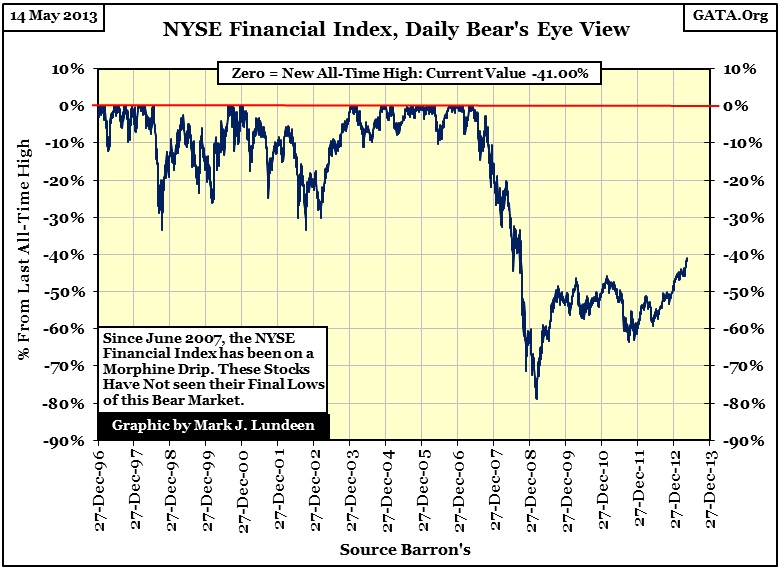

There is another fly in the ointment; the NYSE Financial index contained the companies that were at ground zero in the housing bubble, as well as the stock market’s current bubble. These companies were investor favorites during the housing bubble, but collapsed 79% in its aftermath. Since March 2009, their valuations have improved, but are far from the lofty valuations they enjoyed during the housing bubble, and for good reason! Had the US Treasury and Federal Reserve not bailed them out in 2008 with trillions of dollars, and new accounting rules that tolerated them to book their garbage reserves of abandoned mortgages at face value, many of these companies would have gone down to ruin with Lehman Brothers. Today, how many of these companies are alive only because of Doctor Bernanke’s unending quantitative easings?

There is another fly in the ointment; the NYSE Financial index contained the companies that were at ground zero in the housing bubble, as well as the stock market’s current bubble. These companies were investor favorites during the housing bubble, but collapsed 79% in its aftermath. Since March 2009, their valuations have improved, but are far from the lofty valuations they enjoyed during the housing bubble, and for good reason! Had the US Treasury and Federal Reserve not bailed them out in 2008 with trillions of dollars, and new accounting rules that tolerated them to book their garbage reserves of abandoned mortgages at face value, many of these companies would have gone down to ruin with Lehman Brothers. Today, how many of these companies are alive only because of Doctor Bernanke’s unending quantitative easings?

When we realize the failure of these companies to behave in a responsible manner, resulting in the Dow Jones seeing its second deepest bear market bottom since 1885 in March 2009, and understand their current vulnerability to rising interest rates, due to their fraudulent selling of hundreds of trillions of dollars in interest rate derivative to pension funds and insurance companies, it hard to believe that the current stock market “bull market” is anything more than a contrived dead-cat bounce off its lows of 2009.

When we realize the failure of these companies to behave in a responsible manner, resulting in the Dow Jones seeing its second deepest bear market bottom since 1885 in March 2009, and understand their current vulnerability to rising interest rates, due to their fraudulent selling of hundreds of trillions of dollars in interest rate derivative to pension funds and insurance companies, it hard to believe that the current stock market “bull market” is anything more than a contrived dead-cat bounce off its lows of 2009.

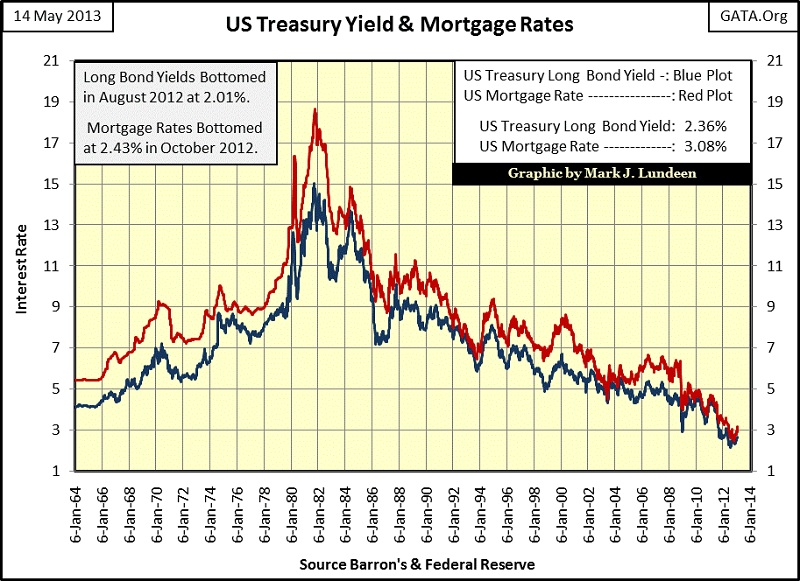

It’s not a quirk of history that the bull market in bond and stocks began in 1981-2. It was in the early 1980s (chart below) when interest rates peaked, and began a decline that has continued for the past three decades, taking financial assets (bonds and stocks) up as rates went down. For this reason, the key for when the current stock market bubble will end is found in the debt and interest rate markets.

When interest rates and bond yields once again begin to rise, there will be no more talk of the Dow Jones at 116K.

When interest rates and bond yields once again begin to rise, there will be no more talk of the Dow Jones at 116K.

Mark J. Lundeen

More from Gold-Eagle