Fed Can't Completely Stop The Kress Cycle

Try as it may, the Federal Reserve can’t seem to patch all the holes in the leaky inner tube that is the U.S. economy. While Fed chief Bernanke is credited for pumping up the deflated tire since 2009, each time he succeeds in patching one hole another leak takes its place.

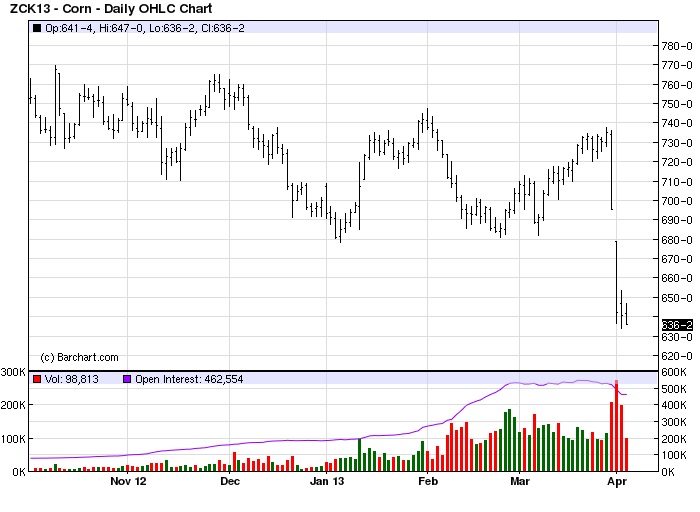

While all eyes are on the soaring U.S. stock market and rebounding housing market, few commentators have drawn attention to the remarkable weakness in the commodities market. Consider that in the last 1-2 years bear markets of varying magnitudes have overtaken the markets for “softs” including coffee, sugar and cocoa. More recently grains prices have taken a tumble. Corn prices are in free-fall and wheat prices are also in steep decline. The price of corn crashed recently when a USDA report revealed much higher corn supplies than the market anticipated.

To make matters worse, deflation has again reared its ugly head in Europe as Cyprus became the latest victim of the European sovereign-debt crisis. The revival of the deflationary scare in Cyprus has had a spillover effect on several countries and has resulted in falling stock prices across the euro zone. Greece’s stock market has retraced more than half its gains since August while Spain and Italy’s equity markets have also recently stumbled. The declining value of the euro currency meanwhile suggests that Europe’s troubles are far from over.

Adding to the difficulties in containing the global deflation problem is the threat of an economic contraction in China. The governor of China’s central bank issued a warning over the country’s high inflation rate of 3.2 percent (as of February). The People’s Bank of China also released a survey saying that 68 percent of the Chinese households believe that housing prices are “too high.” The government is widely expected to tighten money supply in an attempt at curbing the housing market again. This will have an adverse impact on the Chinese economy with possible spillover repercussions for the global economy.

What’s making it difficult for central bankers to completely contain the deflationary threat is that the fiscal policy of several major nations is at odds with what Bernanke and Draghi are trying to do. While the Fed and the ECB are committed to ultra-loose money policies, the governments of leading nations in North America and Europe have embraced austerity and/or fiscal tightening. Such fiscal policies will only serve to counteract much of what the central banks of the U.S. and Europe are trying to accomplish in the way of re-inflating the global economy. It’s like trying to mix oil and water – it simply won’t work.

Since lawmakers are stumbling over their own feet in this matter we can expect that at some point – probably later this year – the momentum from the 2009-2013 financial and economic recovery will wane. When it does, it’s only a matter of time before the downside pressure from the bottoming long-wave deflationary cycle takes over and reverses much of the gains of recent years.

Governments, it seems, never can learn from the mistakes of the past and are indeed doomed to repeat them.

The Rich Are Leveraging Up

There’s a saying about high-net-worth individuals: they’re always the first to snap their wallets shut in a recession and the last to start spending in a recovery. But when the rich finally start spending again they spare no expense!

Witness the rebound in consumer spending in the U.S. since the 2009 rebound. While earnings and discretionary spending among the middle class has shown only modest gains, spending among the “upper crust” has been nothing short of robust. According to Mark Jordahl, president of U.S. Bank Wealth Management, high-net-worth individuals are not only spending fast and furiously, their also taking on leverage. Jordahl told Barron’s that his lending business is up 66% on a year-over-year basis.

The increased borrowing among the wealthy is not a function of need, but of perceived opportunity. The rich are taking on leverage because they see investment return opportunities at historically low rates of interest. They’re feeling more risk averse than they were just a couple of years ago and more money is coming out of safe haven investments (like bonds and gold) and flowing into risk assets (like stocks).

Spending patterns by upper-income earners remain buoyant thanks to strong stock prices and rising home prices, as well as dividends and bonuses distributed in late 2012 (rather than in 2013 to avoid higher taxes). Kipplinger Finance points out that consumers at the upper end of the wealth spectrum pack an outsize punch in the economy, with those in the top 20% of income accounting for roughly 40% of spending.

So what does it mean when the rich come out to play? While it’s still too early to worry about the implication of increased leveraged among upper-income investors, the trend toward increased debt is certainly troubling and will eventually lead to increased volatility down the line. For now, let’s enjoy the economy’s strong showing courtesy of the upper 20%!

Gold

Gold continues to face selling pressure in the face of declining investment demand. According to Bloomberg, the SPDR Gold Trust (GLD) – the largest bullion-backed ETF – saw its holdings fall 4.21 tons on Monday to put the total known stock in exchange-traded funds at the lowest since August 2012. The general trend toward higher equity prices is primarily responsible for the investors’ increasing demand for risk assets, causing them to shed save haven investments like gold and silver.

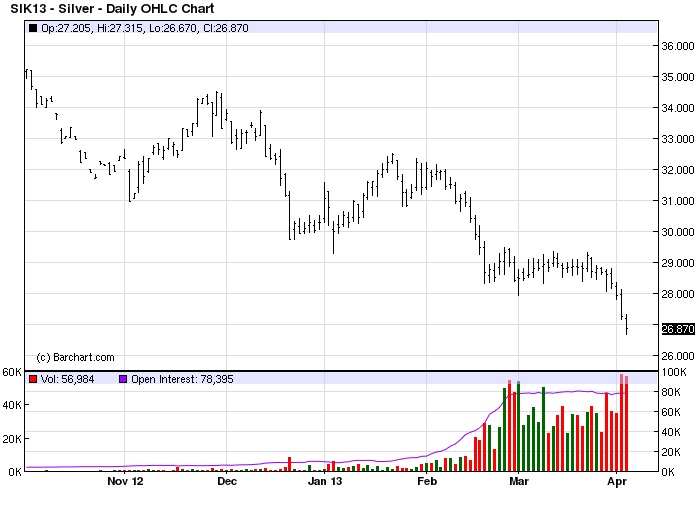

Silver, meanwhile, showed relative weakness last week when it broke under its recent trading floor at the 28.50 level and continues to decline. This negative leadership has had a spillover effect on gold with the yellow metal showing weakness in recent days. The white metal has often served as a leading indicator for the yellow metal and silver’s recent breakdown could be warning of a similar decline for gold.

Moreover, more than one economist is expecting the economic numbers to weaken in the second quarter. One bank analyst reports: “There is no consensus among economists as to whether the recent growth numbers are sustainable, but there are some who are warning that another “spring swoon” in Q2 is not only possible but likely. They tend to cite three factors. The first is that exports are way down—growing by only 2% when in the past they were growing by as much as 15%. The weakness in Europe is really hurting an economy that sells a lot to these states. The second factor is that the sequester pain is only starting to be felt. The layoffs begin in April and so do the furloughs and budget cuts. There could be as much as $10 billion coming out of the economy in just a few weeks. There is also a feeling that the stock market is in for a big correction that will take the investment community by surprise. There is just not much to justify the performance of the market and when that realization comes the collapse will be swift.”

Momentum Strategies Report

The stock market recovery is nearly four years old, and investors wonder if it will continue. While many experts have made forecasts for the coming year, few have been as impressive as the Kress cycles in projecting the market’s year-ahead performance since the recovery began.

Each year I publish a forecast for the coming year based on a series of historical rhythms known within Kress cycle theory. Last year’s forecast was remarkably accurate in predicting the pivotal market turns, including the June 1 bottom in the S&P.

Here’s a sampling from last year’s forecast:

“The first five months of 2012 will likely be characterized by greater than average volatility....This will create a level of choppiness to coincide, if not exacerbate, the market’s underlying predisposition to volatility owing to the euro zone debt crisis…the May-June 2006 stock market slide could be repeated in May-June 2012. Our short-term trading discipline should allow us to navigate this volatility and there should be at least two worthwhile trading opportunities between [January] and the scheduled major weekly cycle around the start of June 2012. From there, the stock market should experience what amounts to the final bull market leg of the current 120-year cycle, which is scheduled to bottom in October 2014.

“Keeping in mind that like snowflakes, no two markets are exactly alike, the Kress cycle echo analysis for 2012 tells us to expect a final upswing for stocks in the second half of the year with the first half of 2012 likely to be more favorably to the bears, especially if events in Europe are allowed to get out of hand.”

This is your opportunity to find out what the Kress cycles are telling us to expect for 2013. Subscribe to the Momentum Strategies Report now and receive as my compliments to you the 2013 Forecast issue.

In addition to that you’ll also receive the MSR newsletter emailed to you each Monday, Wednesday and Friday. MSR provides reliable forecasts and analysis of U.S. and global markets based on internal momentum, cyclical and technical factors. Low-risk stock and ETF recommendations are also made based on my proprietary system of selection. Specific entry and exit instructions are also given for each recommendation.

********

[For the complete 2013 Kress cycle forecast for the U.S. stock market and the latest newsletters, subscribe to the Momentum Strategies Report at the link below.]

http://www.clifdroke.com/subscribe_msr.mgi

Clif Droke is the editor of the three times weekly Momentum Strategies Report newsletter, published since 1997, which covers U.S. equity markets and various stock sectors, natural resources, money supply and bank credit trends, the dollar and the U.S. economy. The forecasts are made using a unique proprietary blend of analytical methods involving cycles, internal momentum and moving average systems, as well as investor sentiment. He is also the author of numerous books, including most recently “2014: America’s Date With Destiny.” For more information visit www.clifdroke.com

More from Gold-Eagle