Fed Guidance: The Oxymoronic Illusion

During the past week, we had to endure yet another Fed Open Market Committee (“FOMC”) meeting during which we were spoon fed ample dollops of hopium sprinkled with equal portions of hubris and deception. As the “prepared remarks” were being delivered in grandfatherly grace and academic aplomb, the markets cheered and jeered as houses in various parts of North America emerged as the focus of multiple bidding wars at prices several hundred thousand dollars above originally asking price while copper screamed to multi-year highs with stocks at bubblicious altitudes.

The definition of the word “oxymoron” is “a contradiction in terms” with such commonplace examples being “military intelligence” or “friendly fire” but the greatest example of an oxymoron is the one delivered by the current ex-Goldman stock peddler, Jerome Powell in using the term “Fed Guidance”. I submit that word “guidance” is a misnomer; there are other words infinitely more accurate that describe the style and tone of the spin-slop that oozes from the mouths of Fed officials with the primary one being “obfuscation” and the ending one “prevarication”.

How dare a Chairman of the Federal Reserve Board actually stand in front of an elected body, looking straight into the eyes of the American people through the tinted cable TV cameras and teleprompter memory and use the term “transitory inflation”. As the chart of “U.S. Dollar Purchasing Power” reveals, nothing about the impact of the Fed since 1913 has been “transitory”.

It seems like only yesterday that we had to watch Treasury Secretary Hank Paulson get down on his knees and beg Congress for a bailout of “the financial system” after the collateral underpinning the loan portfolios of all of the Member Banks got blown to smithereens by fraud and avarice and really shady lending practices. Then Chairman Ben Bernanke issued another famous contradiction in terms with his description of the 2007-2008 housing conflagration as a “contained crisis”. It took about fifteen days for the markets to recognize the flaw in the argument before entering serious “Crash Mode”.

When a former Chairwoman of the Fed moves into the role of Secretary of the Treasury in the form of Janet Yellen, you no longer need to turn a blind eye to the dividing line between “Fed Independence” and the “Government Sponsored Entity”. To say that the Fed is not political because Powell wears purple ties and Yellen wore a purple shawl is an insult to the intelligence of the average American citizen. (To students of the art world, when you blend blue (Democrat) and red (Republican) together on a painter’s palette, the resultant colour is purple; hence the donning of purple by Fed officials.) The Fed is a totally political animal because in Washington (or London or Ottawa or Tokyo), to be “apolitical” is to be a sacrificial gesture and since there is a reason that lambs are led to slaughter, an apolitical Fed will NEVER allow itself to EVER be put in that position.

The Bank of Canada acts in a far less theatrical manner because unlike the U.S., Canadian politicians (and citizens) take enormous pride in the (over-glorified) reputation of the Canadian banking cartel – er – system. There has never been a case where a business that has been granted a Canadian banking charter has EVER had to worry about competition because the Bank of Canada, under the direction and edicts of the British North America Act of 1867, gave to the Big Five Canadian Banks full “right of plunder” of the financial landscape in the second largest continental land mass on the planet. In fact, many of the longstanding followers (to my inane ramblings) will recall the chart I provided in 2010, mere weeks after the Canadian financial press were trumpeting out the “conservative values” and “superior corporate governance” of the Canadian banks that demonstrated that Canada’s TD Bank was listed in the “Top Ten Derivatives Holders” before the sub-prime meltdown cratered literally EVERYONE in the lending business but magically and wondrously and testimonial to the apolitical status of the Canadian banking system, those derivatives never became “systemic” and they barely scratched the TD balance sheet or income statement. Oh, to have been a “Fly on the wall” in those meetings thirteen short years ago.

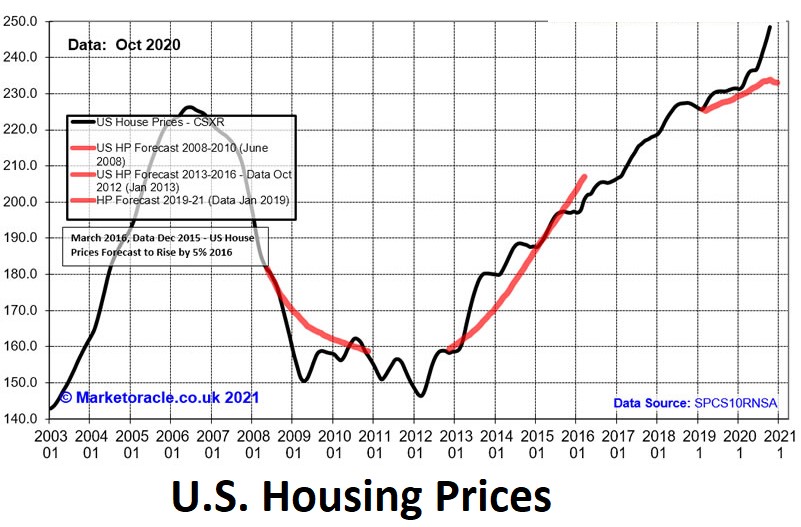

What readers of this publication must accept is that the only thing that matters to any central banker or political associate is the integrity of the collateral of the Member Banks. If TD Bank were to have been forced to vapourize shareholder equity in order to comply with the British North America Act, pension fund assets around the world (and especially in Canada) would have been placed in jeopardy because the collateral behind which loan portfolios were firewalled would have been impaired to the point of insolvency and forced liquidation. That is what happened to U.S. housing prices in 2007 and it took twelve agonizingly long years of monetary inflation (money printing) before the median home price finally reached 2007 levels.

I will refrain from throwing up a battery of charts which proves this thesis but a causal glance at the Fed balance sheet or U.S. Treasury debt levels allows the drawing of a straight line between member bank loan collateral and the new Fed Mandate. Gone forever is the dual mandate of “price stability” and “maximum full employment” replaced with red-faced admission by “member bank protection”. The sad truth is that this has been the camouflaged function of the

Fed since December 23, 1913 when they waited until the majority of the voting Congress was absent for the Christmas break before introducing and passing the Federal Reserve Act of 1913.

The lesson learned by the Fed from the Stagflation Seventies by Paul Volcker was that “We failed to control the gold price”. The lesson learned by Alan Greenspan from the Crash of 1987 resulted in the creation of the Working Group on Capital Markets from which there arose an army of Fed traders charged with “market price maintenance” who are commonly known as “The Plunge Protection Team” (or “PPT”). However, the most obvious and at once insidious lesson learned from the two major crises of the past two decades – the Great Financial Crisis of 2007-2008 and the Global COVID-19 Pandemic of 2020-2021 – was that the Fed must move to protect member bank collateral at all costs and since the two largest forms of vulnerability comes in the form of mortgages (housing) and corporate debt (buyback bond issues) and they are both in very wobbly orbits around the level of real interest rates.

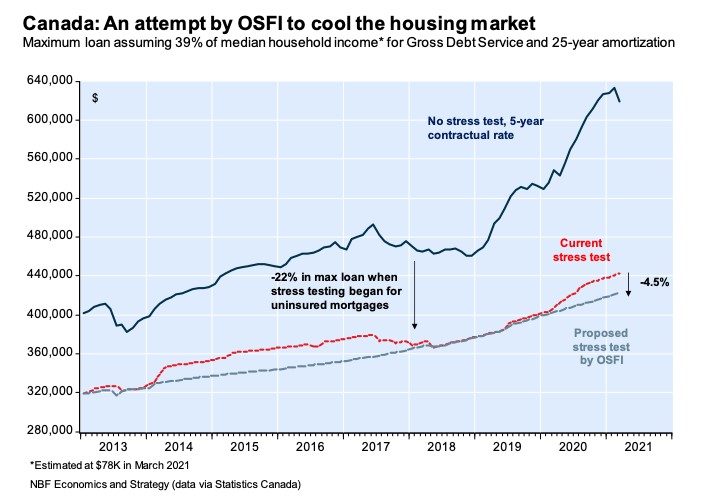

Central bank officials around the globe all trumpet the same line of propaganda because they all have the same mandate. Officials of the Bank of Canada and the Royal Bank of Australia care not a wit about the inability of younger citizens to afford a home because to raise mortgage rates would seriously impair the collateral held by the banks, so it is far preferable to have these youngsters enslaved for thirty-five or forty years to a gargantuan monthly payment to their local bank than to have prices become more manageable. (Whose “back” do you think they have now?)

So, in circling back to the theme of this missive, I would ask that the next time a Fed (or Bank of Canada or Bank of Japan or ECB) official stands in front of you and tells you that he “has your back” and will provide you with “transparency” when central bank mandates are discussed, I urge all of you to recall the immortal words of Abraham Lincoln that cut through this narrative like a Brazilian machete:

********