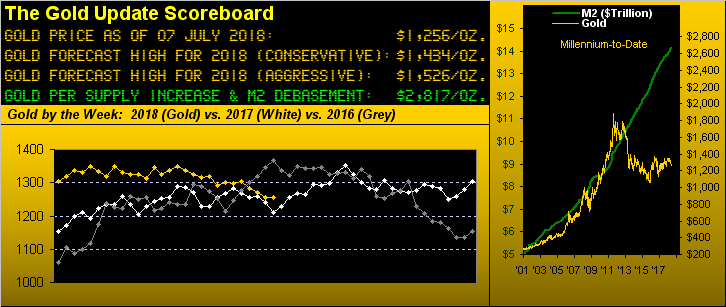

Gold Firms Off The Bottom Of The Box

In a week fraught with TradeTalk, TariffTiffs, better EconData, worse EconData, and an exchange halt StateSide for Independence Day, trading volume thinned across the BEGOS Markets (Bond Euro Gold Oil S&P) with one exception: Gold! Its contract volume for the week (1.57MM) not only exceeded that of the prior week (1.14MM), but was the most since the week ending 25 May (1.72MM). Moreover, in going all the way back to that week and looking at the trading volume day-by-day since then from 18:00-21:00 PT (01:00-04:00 GMT), gold this past Monday evening (02 July) traded its largest contract volume specific to that time slot.

Why?

Because: At 18:43 PT (01:43 CET) Gold hit the bottom of The Box (1280-1240) for the first time since 12 December -- on which day the low was 1238.3 -- and for which this past Monday evening was a nearly identical low at 1238.8 -- and anybody and everybody with an ounce of gold sense said "no! No!! NO!!!" and raced to gold's rescue. 'Twas a beautiful thing to behold, and yours truly even teared up a bit upon the world's recognition that gold's being at The Box's bottom meant "buy! Buy!! BUY!!!" Whether or not our blessedly having 1,000s of readers had anything to with the placing of buy limits at 1240, to wit, here is the price of gold as did the week unfold by the hour, price spritely leaping up and away from Monday's moment of truth, to then firm and close it all out yesterday (Friday) at 1256:

But does such supportive event declare gold as having put in its low for this year? Perhaps. We don't view ourselves as predicting gold's annual lows; rather a silly exercise for the BEGOS Market having the most overdue upside potential. Instead, with gold having closed out the week above the bottom of The Box, our forecast high for this year of 1434 remains intact. Still, the trend -- in this case an unwelcome friend -- remains down, the parabolic Short dots now extending their reach through 10 weeks as shown here in the weekly bars from a year ago-to-date, (the sigh of relief at 1240 notwithstanding):

As for gold's 300-day moving average -- a once stalwart friend turned foe turned neither do we know -- today we find price (1256) some 36 points below said average (1292), a distance basically not seen since July a year ago, and from which come that September gold then found itself nearly 150 points higher. Repeat that performance from here and we'll find gold finally to have broken above Base Camp 1377 with the drive to 1434 in the balance. First things first however: do not bust below The Box, and better yet, break out above it. Here's the whole picture by the day since gold's highest settle nearly seven years ago:

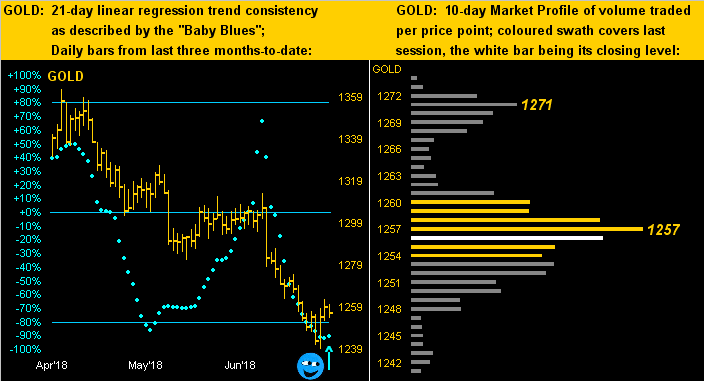

As for the present, let's turn to the two-panel chart of gold's daily bars from three months ago-to-date on the left and the 10-day Market Profile on the right. Note gold's rightmost baby blue dot of linear regression trend consistency: 'tis up (from below the -80% axis), which oft heralds the early days of a new uptrend, (thank you Monday evening's "bottom of The Box" buyers). And in the Profile, clearly the near-term trading line in the sand is 1257:

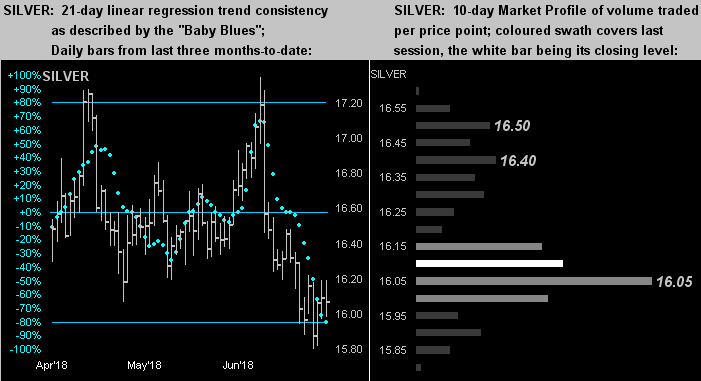

However for Sister Silver, her "Baby Blues" (left) continue their decline, albeit price firmed this past week. Still, by her Profile (right), 'tis all about staying out of the 15s:

Fundamentally, despite such disparate pricing vs. proper valuation, the market is never wrong, (that courtesy of the "'Tis What 'Tis Dept."). Gold is presently at 1256, whereas its proper valuation by currency debasement (per our opening Gold Scoreboard) is 2817. The S&P 500 is presently at 2760, whereas by any stretch of proper valuation vis-à-vis earnings it ought be 'round 2000. Recall our "correction" call to 2154 also incorporates a guesstimated price/earnings ratio (thanks to the reduced corporate tax rate) at that level of 16.4x, a vast improvement from Bob Shiller's present CAPE of 32.8x and our median "trailing twelve months" reading of 24.2x. And in due course, the "regression to the mean" will out: it always does.

Further, as is also always the case, the Fed will again be found "behind the curve". Whilst the minutes from the Federal Open Market Committee's 12/13 June meeting duly note concern over TradeTalk and TariffTiffs, the group remains headstrong toward keepin' rates-a-risin'. But neither a-risin' nor a-fallin' of late is our Economic Barometer. This past week it received better reports for Factory Orders, the Trade Deficit, the Institute for Supply Management's manufacturing and services readings, and Vehicle Sales; yet slowing reports were realized for Payrolls creation (with a 2-pip up-tick in unemployment for the first time since June 2016), Hourly Earnings, and Construction Spending. "But we'll gradually raise rates anyway" say they. Too far up with rates and down with the economy, down with the stock market, the FOMC switches back to "QE" ... and up with gold. 'Tis so easy:

In closing, you'll recall we'd cryptically thought we'd seen it all several weeks back whilst trundling along Monaco's Boulevard d'Italie past the rather vacant-looking offices of the Monoeci. (Indeed we see its price dropped some 22% just yesterday alone in closing out the week at 20¢, overall -98% from its all-time high of $10.32). But now Switzerland? Really?

Mountainous protection, privacy, security, wealth, discipline, common sense, the home of the Amsteg depository, the ever-enduing strength of the Swiss Franc: all of that is Switzerland. Except that now the Zürich-based SIX Swiss Exchange is taking a European lead on becoming a venue for the trading of crypto-assets -- over which Helvetia herself has to have her knickers in a braided twist. "Say it ain't so!" And in all likelihood, we'll be trundling past that Pfingstweidstrasse venue as well come this fall. "Fall?" Yikes! Mind your Gold!

www.deMeadville.com

www.TheGoldUpdate.com

********

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.