Gold Forecast: Wars Don’t Always Mean Increased Gold Prices

Buy the rumor, sell the news. Gold remains bearish in the medium-term, as Russia may end up selling its gold to remain afloat and the USD is poised to benefit.

Buy the rumor, sell the news. Gold remains bearish in the medium-term, as Russia may end up selling its gold to remain afloat and the USD is poised to benefit.

As the Russia-Ukraine conflict continues to escalate (despite ongoing talks), responses from NATO allies intensified over the weekend. For example, select Russian commercial banks were sanctioned and cut off from the Society for Worldwide Interbank Financial Telecommunication (SWIFT). In addition, the Russian central bank has been isolated from the global monetary system.

Thus, while volatility may be the name of the game this week as investors struggle to digest the implications, the geopolitical risk premium that often supports gold may prove counterintuitive this time around.

For example, gold rallied hard as the Russia-Ukraine conflict escalated. However, after a ‘buy the rumor, sell the news’ event unfolded on Feb. 25, gold declined by 2.01%. Moreover, even if the recent escalation uplifts gold in the short term, the fundamental implications of Russia’s financial plight don’t support higher gold prices over the medium term. And there are strong technical and other forces (rising long-term rates, rising USD Index) that support gold price’s decline over the medium term.

Please see below:

To explain, with Russia essentially blacklisted from many influential FX counterparties, the Russian ruble relative to the U.S. dollar was exchanged for a roughly 50% discount on Feb. 27. As a result, Russia's purchasing power is nearly half of what it was before Sunday's developments.

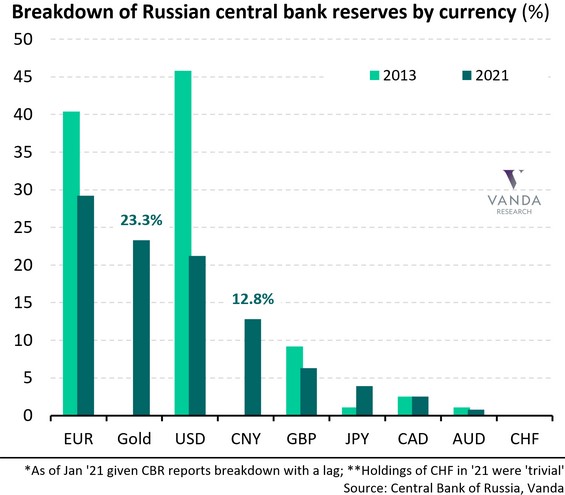

Furthermore, if you analyze the chart above, you can see that euros and U.S. dollars made up a large portion of Russia's monetary base in 2013 (the green bars on the left). Conversely, those holdings dropped dramatically in 2021 (the blue bars on the left).

In addition, if you focus your attention on the column labeled "Gold," you can see that FX has been swapped for gold, and the yellow metal accounts for roughly 23% of Russia's monetary base. Now, with the impaired state of the ruble offering little financial reprieve, Russia may have to sell its gold reserves to alleviate the pressure from NATO's economic sanctions.

As a result, while war is often bullish for gold, the fundamental implications of currency devaluation mean that gold is Russia's only worthwhile asset outside of oil. Thus, with bank runs already unfolding in the region, the yellow metal could be collateral damage.

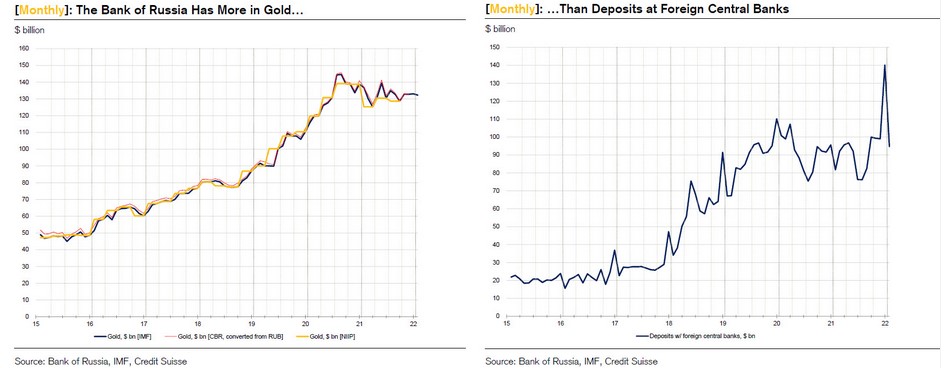

As further evidence, it's important to remember that Russia has plenty of gold stored at foreign central banks. In fact, the aggregate amounts outstrip its foreign FX deposits.

Please see below:

To explain, the chart on the left tracks Russian gold stored at foreign central banks, while the chart on the right tracks deposits other than the yellow metal. If you analyze the trends, the former has remained uplifted, while the latter has declined recently.

However, if NATO countries’ central banks seize these holdings as part of their financial crackdown, it could put more pressure on Russia to liquidate its domestic bullion. As a result, while volatility will likely lead to sharp moves in both directions this week, the often-bullish impact of geopolitical tensions has less fundamental merit this time around.

If that wasn’t enough, you know that I’ve been bearish on the EUR/USD for many months. And since the currency pair accounts for nearly 58% of the USD Index’s movement, its impact is material. To that point, since Eurozone banks have more exposure to Russian debt than their U.S. counterparts, the recent developments are fundamentally bearish for the EUR/USD.

Please see below:

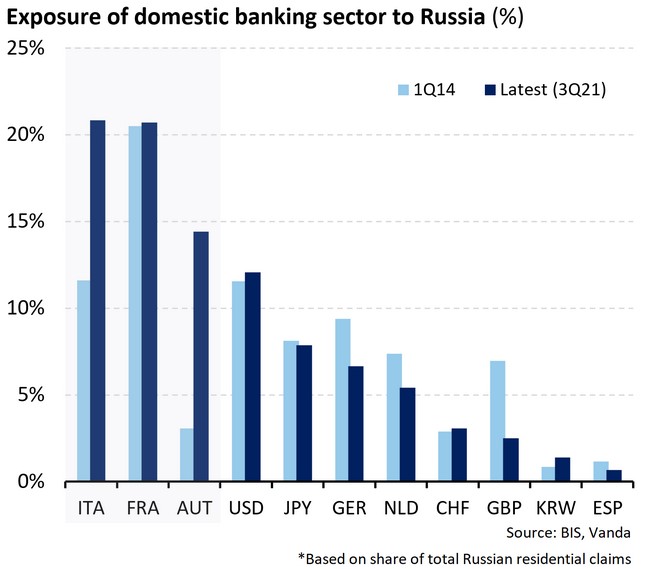

To explain, the light blue bars above depict various countries’ domestic bank exposure to Russian debt in Q1 2014 and the dark blue bars above depict the situation as of Q3 2021. If you analyze the left side of the chart, you can see that Italy, France and Austria are the most exposed to a Russian financial crisis. Moreover, Italy and Austria are much more levered to Russia than in 2014 (compare the light and dark blue bars).

Conversely, while U.S. exposure to Russian debt is material, the share is still lower than its Eurozone counterparts. Furthermore, with Italy’s fiscal health already quite precarious, the impact of potential defaults is much worse than in the U.S. As a result, more pain should confront the euro, which should help uplift the USD Index.

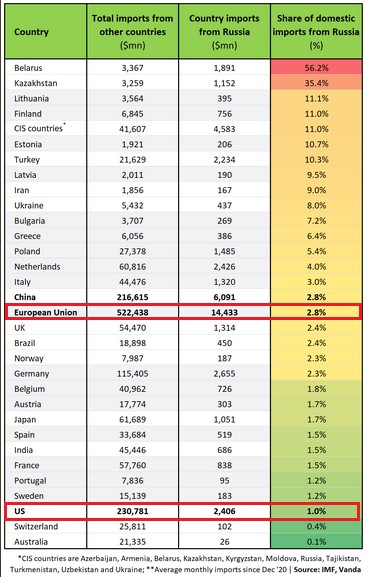

To that point, potential Russian delinquencies aren’t the only problem confronting the Eurozone. For example, Russian imports accounted for 2.8% of the Eurozone’s consolidated average monthly total since December 2020. In contrast, Russian imports only accounted for 1% of the U.S.’ consolidated average monthly total since December 2020.

Thus, while the percentages may seem immaterial, it’s important to remember that it’s all relative. And with the Eurozone under more relative pressure than the U.S., the FX implications support a stronger greenback.

Please see below:

To explain, if you analyze the second column from the right, you can see that Eurozone average monthly imports of Russian goods and services since December 2020 are $14.433 billion. Conversely, the U.S. monthly average stands at $2.406 billion. As a result, the Eurozone economy faces much steeper conflict risks, and the U.S. dollar is a relative beneficiary from the Russia-Ukraine upheaval.

The bottom line? While concerns over World War 3 and anxiety over Russian President Vladimir Putin's nuclear arsenal may elicit a short-term bid for gold, the prospect of a global crisis remains remote at this point. Moreover, with the U.S. dollar a winner, the euro a loser, and Russian isolation likely to result in the selling of its gold reserves, the fundamental implications support lower precious metals prices over the next few months.

To that point, the Fed's stance also remains unchanged, and the Russia-Ukraine drama is unlikely to derail a rate hike in March. Moreover, if the conflict unfolds like 2014, the market impact of each new headline will likely diminish over time. As a result, plenty of bearish fundamental developments should confront the PMs in the coming months.

What if we see these events develop into World War 3? Then gold in the insurance part of one’s portfolio would likely soar, more than making up for any profits not realized in case of short-term trades. That’s unlikely though. What is likely is that we’re already past the peak concern and that gold can now decline along with its medium-term trend. And that junior mining stocks would be affected to the highest degree.

In conclusion, the PMs were mixed on Feb. 25, as the general stock market's risk-on, risk-off behavior continues to pull them in competing directions. However, while the news flow, and investors' reaction to it, remain extremely uncertain in the short term, the bearish medium-term thesis remains intact: technicals, fundamentals and often misguided war premiums support sharp reversals for gold, silver, and mining stocks in the coming months. As a result, while it may be a wild ride this week, ignoring the noise and remaining level-headed is the most prudent course of action.[PR1]

Summary

To summarize, despite the ongoing Russian invasion of Ukraine, and despite gold being the traditional safe haven in times of turmoil, the overall outlook for the precious metals sector still remains bearish for the next few months.

Prices will likely remain volatile this week. The question on many analysts’ minds is whether today’s talks between the Russian and Ukrainian delegations in Belarus will be fruitful. The parties have returned to their respective countries and, as the Ukrainian Presidential Press Service reports, will resume a second round of talks after further consultations in Moscow and Kyiv. Positive news from negotiations will be bad news for gold.

Russia’s economic prospects don’t look good either, even if the country has turned itself into a fortress. The dollar only stands to gain from a Russian bullion crisis or EUR/USD troubles. The medium-term outlook for the yellow metal still remains pessimistic.

Since it seems that the PMs are starting another short-term move lower more than it seems that they are continuing their bigger decline, I think that junior miners would be likely to (at least initially) decline more than silver.

From the medium-term point of view, the key two long-term factors remain the analogy to 2013 in gold and the broad head and shoulders pattern in the HUI Index. They both suggest much lower prices ahead.

As silver often moves in close relation to the yellow metal, when gold falls, silver is likely to decline as well – it has probably already started its slide. The times when gold is continuously trading well above the 2011 highs will come, but they are unlikely to be seen without being preceded by a sharp drop first.

Thank you for reading our free analysis today. Please note that it is just a small fraction of today’s all-encompassing Gold & Silver Trading Alert. The latter includes multiple premium details such as the outline of our trading strategy as gold moves lower.

If you’d like to read those premium details, we have good news for you. As soon as you sign up for our free gold newsletter, you’ll get a free 7-day no-obligation trial access to our premium Gold & Silver Trading Alerts. It’s really free – sign up today.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Sunshine Profits - Effective Investments through Diligence and Care

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses are based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are deemed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

********

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com. You can reach Przemyslaw at: http://www.sunshineprofits.com/help/contact-us/.

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com. You can reach Przemyslaw at: http://www.sunshineprofits.com/help/contact-us/.