Gold: It Is What It Is

If there ever was a year when the unforeseeable can happen, this is the year. Covid-19 plunged economies into a recession, but the turbulent markets reached all-time record highs as interest rates collapsed to near zero levels as part of the extraordinary moves by central banks to rescue their economies. Gold also reached an all time high of $2,064 an ounce, up from $1,700 in May, in the expectation that the flood of trillions of newly minted dollars of stimulus, on a scale never seen before would ignite long dormant inflation. And US money supply surged to double digit levels as the US debases its currency seeking a competitive edge for its exports. Worrisome too, with everything in the US becoming politicized, is that the deeply divisive presidential election might not be settled in November due to constitutional challenges or a disputed election result, which could derail the dollar and market for the ensuing weeks or months. We can recall George Bush’s election results took a month for a winner to be declared after disputes over “chads”.

Against the backdrop of polarising disinformation, there is a national crisis over trust and democracy itself as the US political divide widens from voting rights to racial injustice to police brutality. Armed civilians have become fixtures at marches for racial equality and the taking up of arms to enforce political will is a disturbing escalation of the peace marches and a sign of the deterioration of democracy’s fabric. And still the pandemic rages as the most powerful economy in the world slides into the worst slump since the Great Depression.

Yet, the stock market reached record highs.

Debt Dead End is at an End

For the past forty years, central banks’ main tool was to lower interest rates to lessen the cost of borrowing and to stimulate economic activity. Lower interest rates did avert a fiscal catastrophe in the pandemic-ridden economies, but borrowing their way out of trouble resulted in more debt creation. In March, Washington chose to nationalize its economy by subsidising businesses and wages with another round of deficit spending, delivered not by helicopters but electronically. None of this is pretty. The problem is that the stimulus programmes simply froze the pandemic-hit economy and months later, the thawing has exposed a wider problem. The debt solution of simply more debt is unsustainable as countries cannot borrow forever.

And in the past decade, central banks led by the Fed undertook Quantitative Easing (QE), buying up government bonds and lately, corporate paper to pull rates down. However, to accomplish this, the Fed increased its balance sheet to $7.3 trillion, up from $4 trillion in March, which is the highest ever representing a third of America’s gross domestic product. The expansion is unprecedented and this time even base money supply has expanded relative to GDP. The latest official projection from US Congressional Budget Office (CBO) estimates that the federal budgetary deficit will quadruple to $3.8 trillion or 19% of US economic output, which is more than the combined deficits since 1945. As a percentage of GDP, the US deficit is worse than Spain’s, Greece’s and Italy’s. The March turbulence expanded the Fed’s balance sheet further with a program of unlimited asset purchases including corporate bonds like the now bankrupt Hertz. The Fed’s new mandate seems to keep stock prices higher and intervene whenever they fail.

Free Money

And, by opening the spigots of liquidity, the Fed provided the rocket fuel for the stock market’s run. The more the Fed drives real yields down and valuation in stock prices up, the more the Fed must keep buying debt just to keep them there. And, by pushing on the string, the more glaring problem and unanswered is the mountain of debt left as a consequence of a decade of QE, and the trillions of dollars from the largest government bailout in history.

And for most of the past four decades, central banks conducted monetary policy with the goal of price stability. However, after repeatedly failing to meet their 2% inflation target, the Fed jettisoned its long standing policy and adopted a more dovish monetary framework, promising near zero rates for a very long time, maybe years. Although, with rates near zero, the Fed removes one of its conventional tools, leaving them fewer options in the next crisis, particularly since the virus seems likely to outlast the latest round of stimulus.

Now, with the Fed’s U-turn and promise of low interest rates forever, the future will see more financial booms and busts. So far the flood of monetary and fiscal stimuli has created winners and losers, steering investments into unproductive debt or bubble-like markets, destroying the returns of traditional saving institutions, elderly savings and productive investments. The promise of easy money makes it easy to own real estate when 30 year mortgages are below 3%, making home builders, owners and lumber producers the big winners, with the losers, the financial institutions and those with savings. But cheaper borrowing costs have not helped the solvency of the leisure, travel and energy companies hit hard by Covid-19.

The Seeds of Hyperinflation Have Been Sown

Consequently investors have lost their fear of debt and reinforced by the Fed’s new monetary mandate, believe that ultralow rates are forever. Since 2010, the 10 year Treasury forward has fallen from 5% to just 1.6%, an indication that investors expect rates to be below inflation for the next decade. But the calculus of public debt has changed. If the Fed keeps rates at less than 1% but manages to achieve its target inflation rate of 2%, how is an investor to win? That said, if government paper promises yields of little or nothing, it becomes less of a traditional safe haven.

Only six months into this year, US debt soared in the second quarter, standing at $27 trillion or 126% of GDP, the largest indebtedness ever. For now, nobody is worried because the cost of this debt is minimal. But this time, money supply has grown by double digits at a pace not seen for more than a decade or two. Ironically, in using the printing press to make debts go away and with the double-digit explosion in money supply, the Fed an inflation denier has chosen to use the age-old politically expedient solution of inflation and currency debasement to deal with the growing debt burden. However, history shows that when central banks ignore inflation and focus on unemployment, inflation eventually rears its ugly head. Just look at Venezuela to see how this works. And this time the trade wars and pandemic have caused supply shocks which will boost inflation. It has happened before. The last time debt was more than 120% of GDP, was after World War II and it took two decades of growth and inflation to erase that debt. We might not be so lucky this time. The Fed should be careful for what they wish for because when inflation raises its head, under the new guidance they won’t be able to rein in inflation with higher interest rates.

The Economic Recovery That Isn’t

But, the market is telling a different story. While the old adage goes, “the market discounts ahead”, record breaking market highs suggest a super strong economic recovery is in the offing. However, the International Monetary Fund (IMF) noted that global output will actually fall 5% this year, despite the largest bailouts in history. Consequently, rather than a “V-shaped” recovery, a square root shaped “”recovery is more likely as the other side of the valley is not so visible. Of note is that it took 23 years and World War II for the US economy to recover from the Great Depression. After 2008, it took almost 8 years for the economy to recover.

Why are the markets so disconnected from America’s economic reality?

Simply, the trillions of support packages only “froze” the global economy, With the economies only now thawing out, the impact of the coronavirus and deep recession is only being felt as the lockdowns alters consumer behavior, imperiling the business models of everything from retail to travel to oil. The “never normal” will see households facing massive job losses and with declines in consumer spending, once the mainstay of the US economy sharply lower, corporate profits will plunge with consumption replaced by evictions. Already, JC Penny, the iconic retailer has closed as has nutritionist GNC, J Crew, Ann Taylor, and California Pizza. American Airlines will cut 19,000 workers. Disney is to eliminate 28,000 jobs. In the United States about 20% or nearly 10 million workers are receiving benefits.

Dethroning the Greenback

The US dollar is the world’s reserve currency. The low interest environment enables the government to borrow at 1% or lower, keeping borrowing costs down as well as providing a return to the Federal Reserve, which has become a buyer of last resort replacing foreigners who have sought alternatives to the dollar.

Nonetheless, the greenback has fallen more than 6% because of the crisis-induced spike in March. But still in the grips of the pandemic, the dollar has wobbled on fears of a long awaited meltdown. The dollar isn’t so mighty anymore weighed down by the twin deficits caused by the record expansion of the federal budget deficit and a widening current account deficit caused by the need to replace domestic saving and attract outside capital. China has become the world’s leading exporter and financier as net creditor to the rest of the world. For all the talk about America’s big market, the EU is the world’s largest single market area. And today, more euros, renminbis, rubles and yen are traded daily overshadowing the dollar, with the dollar’s share falling below 50%.

Between March 1985 and 1987, the greenback dropped 50% against the yen and the deutschmark, forcing the US to sign the Plaza Accord as its liabilities and deficits piled up. And today, America’s willingness to weaponize its financial hegemony, not only erodes the dollar’s supremacy, but is eerily similar to the Great Depression. America’s economic nationalism is a repeat of the protectionist policies that exacerbated the Great Depression. Then, international cooperation broke down as governments of uncompetitive economies put up tariffs erecting capital controls. And today, as America weaponizes its currency and financial system together with a fiscal imbalance, dysfunctional politics, and a collapsing US economy, alternatives to the greenback are being sought, like the US-controlled SWIFT payment system. America’s currency debasement and debt accumulation has sown the seeds of a burst in inflation eroding of the dollar’s role as the world’s currency. What is exceptional here is how easy America has lost its privileged mantle, ironically to be one of Mr. Trump’s lasting legacies. It would be tragic if history was forgotten and all had to be relearnt all over again.

Decoupling the Digital Divide with China

Yet, as the coronavirus crushes the US economy threatening Trump’s re-election hopes, the president has raised the stakes and made China an ideological scapegoat and part of his election platform by demonizing everything that is Chinese. By ratcheting up already acrimonious tensions on everything from trade to 5G to pharmaceutical elements, he has altered Americans’ views on the economic and social issues with China. It is a gloomy moment.

The US-China geopolitical relationship is at its lowest ebb in half a century, entering a new dark age that has spread beyond trade to technological competition, finance and geopolitical influences. After decades of developing economic ties, the geopolitical battle over data, the lifeblood of modern economies has forced America to escalate the battle dangerously by imposing new regulations and sanctions. American rules and standards once shaped global use of technology and they have always been protective of copyrights. However this has since widened to include pharmaceuticals, tech and even the marketing of hardware. Information and data is the new 21st century proprietary issue and both countries are pushing back on all fronts. America’s big tech giants like Amazon, Google, and Facebook have thrived on the trade and control of data. Similarly China’s tech giants Huawei, Alibaba and Tencent too have prospered, supported by a population which is four times bigger than America’s. In fact, many of America’s companies are loosely integrated with their Chinese counterparts as they try to expand into the East.

Nevertheless, American tech companies are in a bind, reluctant to join the “Made in USA” tech war because of globalization and like Facebook’s messaging app WhatsApp are heavily dependent on the Chinese market. China is American tech companies’ biggest consumer market and they do not want to provoke China’s ire nor suffer from local boycotts. Consequently, Trump in invoking bans on WeChat and TikTok which is popular among teenagers, citing sweeping claims of national security and even forcing the sale of TikTok’s business, should realize that the technology race will be won by China if he keeps intervening in the World Wide Web. Also Apple, the world’s richest tech company, depends on China for its manufacturing base and is heavily reliant on the Chinese market.

America’s Unilateralism has its Costs

Despite the trade wars and a revamped NAFTA with Canada and Mexico, the US trade deficit surged in July to the highest level in 12 years. For all the talk about “winning” the trade war with China and a “Phase One” agreement to buy more than $200 billion in goods and services, the trade deal appears to be a deal in name only. The US trade deficit in 2016 stood at $347 billion. Last year despite the hawkish rhetoric, the deficit stood at $345 billion. During this period, America’s farmers saw their markets disappear as America’s exports collapsed to $48.5 billion, falling well short of the $100 billion target. US-China investment flows fell to their lowest levels in a decade to a paltry $10.9 billion in the first six months of this year. US soybean exports to China collapsed despite China’s higher global soybean imports. Tens of thousands of students started the school year without laptops, because many were made in the East and bottle-necked supply chains and the trade war limited supplies. America’s economic nationalism has its costs.

The pandemic exposed many other weaknesses. For example, the critical pharmaceutical ingredients, which American companies use to make drugs, are made in China and the desire for self-sufficiency drove the Trump administration to throw almost three quarters of a billion dollars into Eastman Kodak, a former American icon, to produce drug ingredients, despite never having manufactured a molecule. At one time America was the dominant producer of pharmaceuticals, but environmentalists and ever stricter rules in the US made manufacturing pharmaceuticals too expensive and so China and India became the alternate suppliers. Today China provides more than 90 % of the raw material metrics for vitamins and antibiotics.

Ironically, in a tit-for-tat retaliation, China could easily weaponize its drug exports, and the self-sufficiency moves by America would be difficult to repatriate, let alone duplicate. After Covid-19, most nations will strengthen their health systems and the sharing of vaccines and medicines is likely. China already is distributing a “Made in China” vaccine. Despite having one of the worst infection rates in the world, the vaccine-less Trump administration not only withdrew from the World Health Organization (WHO), but opted not to join a consortium of more than 150 countries aiming to develop a vaccine.

One thing is clear. Over the past two decades, China has grown into a superpower with a large industrial base, global reach and a population four times larger than the United States. China has built its own ecosystem, rivaling the United States with its own homegrown technology, financial and consumer giants. China’s huge economy is becoming integrated with the world as America severs its deep network of alliances, discarding agreements and antagonizing allies, China’s embassies and consulates around the world outnumber those of the United States. China has stepped into the power vacuum, poised to trade places with the United States. Huawei, a regular US target, appears to be losing access to the western 5G market after US pressure on the “Five Eyes” partnership, which forced Britain to ban Huawei’s 5G equipment. However, Huawei reported its biggest growth in profits due to growth in their home markets.

Falling Into the Thucydides Trap

China also reformed its capital markets, opening a second technology-focused Shenzhen’s ChiNext Exchange to compete with Shanghai’s STAR, a NASDAQ look-a-like market. Congress’ recent threat to delist Chinese companies is alarming to American investors, who would suffer because many of China’s stocks are incorporated in the global indices like the MSCI broad index of which they are big investors in index-tracking funds. Still, Washington lawmakers are pushing to blackball Chinese companies. China, however has major stock exchanges with more than 3,900 companies listed of which many Americans hold shares like Alibaba and Tencent. The value of Chinese listings on Wall Street rose this year with more than 200 Chinese companies listed in the US with a value of almost $2 trillion. Many might quit US bourses anyway as they are already listed on Hong Kong or China’s exchanges.

Bypassing Wall Street, China’s Ant Group will soon go public in a dual Hong Kong-Shanghai listing in the biggest IPO in history. Beijing, Shanghai, and Hong Kong have become major financial centres where the world’s largest index players participate on a daily basis, making the threat of delisting a non-event in a globalised financial world. BlackRock, the world’s biggest asset manager and JP Morgan Chase are setting up shop in China in a bid to gain access to the world’s most populous country. Ironically, the US government’s protective actions are driving investment away from their home borders to other countries. Within today’s global inter-relationships of finance, any decoupling would be messy, hurting both economies and investors.

Indeed, the rivalry between China and the United States is reminiscent of the 500 years of historical great power competitions studied by Professor G.T. Allison of Harvard, who cited in the Thucydides Trap that when a rising power threatened to replace an established power, in 12 of the 16 cases, the end result was war. Only in four of those cases was there no war. While markets are largely complacent about the past, the notion of a war between the two superpowers seems remote, yet history and the steady escalation of tensions and the new Cold War makes the prospects too real.

Nuclear Option

All this points to the dilemma of the United States, the world’s largest debtor with debt at $27 trillion or 126% of their GDP, thinking that increasing this debt will solve their indebtedness problem. However almost a third of US government debt is owed to foreigners like the Chinese. China in turn has become the world’s largest creditor. Despite the rounds and rounds of US sanctions targeting everything from technology, to companies, to officials and Chinese goods, China has adopted a strategic “wait-and-see policy” reflecting their stance to play the long game.

However, in their arsenal is the $3.1 trillion of foreign exchange reserves of which one third is invested in US Treasury bills. While China has recently slowed down their US debt purchases, preferring gold (which is denominated in dollars) and alternative assets, China has yet to dump their holdings en masse in part because that “nuclear” option would send the US dollar and markets into a “tailspin”, ending the dollar’s role as the world’s reserve currency. Instead, China’s absence from Treasury sales forced the Fed to take up the slack as a buyer of last resort, piling up of more debt on top of more debt as they resort to the printing press. America’s financing needs have become its Achilles heel as its debt load keeps on getting heavier. Economic nationalism has its costs.

Gold Is a Barometer of Investor Anxiety

History shows that gold is money, it is under-owned. Its allure as a store of value is that it can’t be printed into existence. Unlike fiat currencies, gold is finite and the only way to increase the gold supply is to dig up more and it is this scarcity that is its attractiveness and the reason that gold is held in central banks’ reserves. Central banks know it is an asset, not represented by another’s debt or liquidity. The Bank for International Settlements (BIS), the bankers’ bank recognizes gold as a monetary asset with gold part of its monetary unit of exchange.

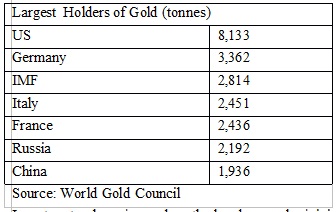

Central banks for the last decade have become the world’s largest buyers of gold and the US is the largest holder of the precious metal at 8,133 tonnes accounting for 78% of its reserves. China is the world’s largest consumer and producer of gold but their output is declining because of a crackdown in illegal mining. In addition, many of China’s mines have short reserve lives because their open pits are running out of reserves as the pits get deeper. In the meantime, Russia liquidated its entire US Treasury holdings, purchasing gold such that Russia’s gold holdings today is valued at $100 billion. We believe China has followed as a part of a strategic effort to hedge risk to the dollar.

China’s Golden Appetite

Russia has accumulated 2,192 tonnes of gold, followed by China at 1,936 tonnes, the sixth largest holder. Other major central banks too have added to their reserves purchasing almost 400 tonnes in the first half of the year. Although Russia has almost 20% of their foreign exchange reserves in gold, China has less than 3% and thus we believe China’s strategy is to increase their gold holdings. As the world looks for alternatives to the dollar as a reserve currency, however, there is not enough gold to satisfy China’s demands. We believe more likely is a renminbi currency basket tied to gold, which would replace China’s usage of the dollar.

Investors too have jumped on the bandwagon by joining the central banks in buying gold. In the Chinese investment world, retail buying has taken off with two new gold funds listed in China, collectively adding 3 tonnes of buying. Over the last eight months, global gold ETFs increased by 38% making up almost 35% of global demand. Year to date, gold ETF net inflows was almost 1,000 tonnes and gold ETFs now hold 3,824 tonnes making the ETFs the second largest holders in the world, after the United States and ahead of Germany. Also, following on the heels of legendary investor Warren Buffett’s Berkshire Hathaway purchase of $500 million of Barrick recently, the $16 billion Ohio Police and Fire Pension Fund invest up to 5% into gold as a portfolio hedge. Still, gold is under-owned.

The Shanghai Exchange (SGE) has become the world’s largest physical gold trader and has even purchased storage vaults becoming one of the world’s major vault holders. With other countries holding the bulk of their foreign exchange reserves in gold, we believe China is desirous of significantly increasing their holding. The trouble is that there is not enough gold to satisfy China’s ambitions, either internally or externally. Therefore China has to buy reserves in the ground and thus we believe Western gold miners are the likely next targets. After all, the world’s second largest economy has the largest foreign exchange reserves in the world at $3.1 trillion, of which one third is held in US debt. America has become the biggest debtor in the world, so China’s superior financing power could dictate terms because America’s debt and deficits keep climbing in the misguided belief that they can “grow” their way out of debt.

Recommendation

America’s 2020 election in our view is one of the stock market’s biggest risks. Equally worrying is a potential Supreme Court fight which intensifies the partisanship on Capitol Hill that would be catastrophic as investors find themselves in the midst of an election result to be decided by a Court that is equally divided. President Trump has already called the election “rigged” and “one of the great embarrassments”, while state and local officials admit it might take a while to certify the election results and there is the post office which can deliver mail “rain or shine”, but might not deliver the ballots in this election on time.

Gold usually rises in times of fiscal uncertainty and, many times is a barometer of investor anxiety. We believe the uncertain election outcome and potential for a protracted result will introduce an unusual amount of market volatility and anxiety. We believe gold will continue to outperform stock markets as it has this year. The financial markets are going to be in serious difficulties. Gold is a defense against the unknown.

While we have long maintained a $2,200 an ounce target for years, we do not believe that this is the top. After reaching a closing high of $2,064 an ounce, gold corrected to $1,850 challenged by a recovery of the US dollar. A pullback and the ensuing need for a consolidation is not surprising since gold was at $1,700 in May. We believe that the pullback is a buying opportunity, with limited downside risk at $1,725 an ounce.

How high? How low the US dollar. A lower dollar would boost inflation and since the Fed will not defend the dollar by raising rates (under Powell’s new policy), the dollar could soon be in freefall. We also believe Mr. Trump’s retreat from the global stage in the face of rising global disorder is a repudiation of all things that made America great. We believe no matter the election outcome in the United States, major changes are ahead. Gold is a hedge against this uncertainty. Since gold was $32 an ounce, we have observed that the barbaric metal always makes successive record highs. Since the coronavirus hit, gold has outperformed all assets. It is not so different this time.

In the latest quarter, M&A activity was quiet despite miners generating billions of free cash flow. Reserve replacement remains the key problem for the industry and it is cheaper to buy ounces on Bay Street than spending money with the drill bit. Consequently we continue to expect heightened levels of M&A over the next year or two. Further, there are a host of development prospects needing financing and most likely to find the capital needed in the current gold cycle. Canadian producers particularly benefited from the surge in gold as they received more than $2,700 per ounce for their production.

We believe M&A activity will be driven by the need for reserves, unlike the last peak in 2011 when companies acquired others for growth and for growth sakes, but the return on capital was lower than the cost of capital, which left a legacy of over $80 billon of writedowns when gold prices crashed. A decade later, a chastened industry is looking for value-added acquisitions such as Kirkland Lake’s $4.9 billion acquisition of Detour to boost its reserve profile or Teranga’s acquisition of high-grade Massawa from Barrick. The industry has returned to fundamentals and dividends are part of the new mantra. Among the seniors, we like Barrick Gold, Agnico Eagle and B2Gold. We also favour Lundin Gold and view Centamin, Centerra and Eldorado as potential M&A targets in the next gold run. Developers are well-placed like Osisko Mining, Sabina Gold & Silver or McEwen Mining with projects that can be brought into production in the current gold cycle. Further, we view the exploration players as the next beneficiaries of the coming cash flow bonanza of higher gold prices. Drill baby, drill.

Agnico Eagle Mines Ltd.

Agnico produced 330,000 ounces in the second quarter enabling it to meet guidance at 1.68 million to 1.73 million ounces. In Nunavut, Meliadine’s mill throughput increased to 4,300 tpd and should top 4,600 tpd after a filter press is installed. At Kittila in Finland, the receipt of a permit allowed an expansion of the processing facility to 2 million tonnes per year as reserves and resource gets bigger. At the Canadian Malartic joint venture, Agnico has 10 drills turning at the East Gouldie deposit. Results are expected shortly which will allow an update of the resource. Agnico and Newmont have formed a 50/50 joint venture to explore a 200 km2 in Northern Colombia. We like Agnico here for its organic growth from mines in Canada, Finland and Mexico. Buy

B2Gold Corp.

B2Gold’s Fekola mill expansion will increase production by 1.5 million tonnes per annum. Fekola in Mali produced 147,000 ounces in the second quarter at a cash cost of only $300 an ounce, which is a large part of B2Gold’s total production of 257,000 ounces. B2Gold is a low cost operator, with cash flow of $238 million in the quarter enabling it to finance Gramalote, a 50/50 joint venture with AngloGold Ashanti in Colombia. A feasibility study is expected in the first quarter next year, building on a PEA that outlined 400,000 ounces a year from an open-pit at AISC of $648 an ounce. B2Gold shares weakened recently because of a military coup in Mali, but the mine was unaffected. We would take advantage of the pullback and buy.

Barrick Gold Corp.

Barrick met its targeted $1.5 billion non-core asset disposal program, boosting free cash flow and with efficiencies at core asset Nevada Gold Mine Joint Venture, cash costs shrunk to $716 an ounce. At refreshed Hemlo, Barrick transitioned to an underground contracting model and the gold district is having a sorely needed second look. After sorting out problems with a new agreement with the Tanzanian government, Barrick and joint venture partner Zijin is teeing off with the Papua New Guinea government by placing Porgera on care and maintenance while negotiations take place. Hopefully this too should pass. The world’s second largest gold producer has become a cash machine, producing 5 million ounces or so at AISC under $1,000 an ounce. Barrick is one of the most profitable around with an enviable array of core assets and excellent management. Buy.

Centerra Inc.

Centerra produced 220,000 ounces of gold in the quarter, generating $169 million of positive free cash flow with Kumtor producing 170,000 ounces at a cost of $692 an ounce. Recently commissioned Oksut in Turkey produced 12,000 ounces at $393 an ounce, which was a stub quarter. Centerra has cash of $212 million with total liquidity of $712 million sufficient to handle $415 million of spending this year. Centerra is an intermediate producer with a flat production profile from its mines in Kyrgyzstan, Canada and Turkey. However, the company has a flat production profile, which is in harvest mode and thus we prefer more growth oriented B2Gold here.

Eldorado Gold Corp.

Eldorado produced 138,000 ounces in the quarter at AISC of $859 per ounce. Guidance was maintained at 520,000 to 550,000 ounces with AISC between $850 and $950 per ounce. Eldorado produced free cash flow of $63 million finishing the quarter with $440 million in cash and equivalents. At Kisladag in Turkey, output was 20% higher than the first quarter due to better weather. An update at Lamaque in Quebec is expected by year-end which will include upgrades of the Sigma mill and details of the nearby Triangle deposit. Close-by is the Ormaque discovery which could help the assessment. At Olympias in Greece, output increased slightly and development continues at Skouries. Eldorado’s dilemma is that their mines do not generate enough cash flow to finance the $900 million required to bring Skouries and Perama Hill into production. Consequently, Eldorado would be a nice tidbit for a major looking to boost output. Eldorado is a hold for future M&A action.

IAMGold Corp.

Mid-tier IAMGold produced 155,000 ounces due to contributions from Essakane and Rosebel, however AISC was over $1,100 an ounce. IAMGold also surprised the Street by lowering guidance to 645,000 to 700,000 ounces because of expected shortfalls from Rosebel with a boost in all-in-costs to over $1,200 an ounces. Rosebel in Suriname produced 52,000 ounces with first ore material from Saramacca in the quarter. The shortfall was attributable to Covid-19 and a strike. Production at trouble-prone Westwood was a paltry 20,000 ounces and reserves were slashed 48%. IAMGold now plans a slower ramp-up to 100,000 to 125,000 ounces but they will have to develop more reserves. Meantime, IAMGold is betting the farm on joint venture Côté, which has a $900 million price tag. We believe there is little on the horizon and thus this high cost producer could stub its toes again, since Côté is a big bet. Sell.

Kinross Gold Corp.

Kinross had a decent second quarter generating $220 million free cash flow and producing 572,000 ounces. At Tasiast in Mauritania, mill throughput was 16,700 tpd, which is expected to increase to 21,000 tpd by the end of 2021. However Tasiast production near term was affected by Covid-19 and a 17 day strike. Longer term the mine plan is being reviewed but the schedule remains. At Kupol in Russia, exploration continues with a reserve update expected at year-end which will extend Kupol’s mine life as it switches to narrow vein mining. Kinross plans to spend $900 billion or most of their cash flow this year at Kupol and Tasiast, which is manageable because of their balance sheet. In the interim however, Kinross has a flat to declining production profile because the Kupol expansion and recently acquired Chulbatkan won’t be in production until 2023. Kinross’ shares trade at a discount to its peers due to its Russian exposure. We thus prefer B2Gold for its growth and geographic profile.

Lundin Gold Inc.

Lundin Gold’s Fruta del Norte (FDN) is back up and running with the mill processing stockpiled ore. Production guidance for the last half of the year is expected at 165,000 ounces at AISC of $800 per ounce. Fruta del Norte’s is one of the world’s richest gold mines and should produce 300,000 ounces or so next year with free cash flow of $300 million plus. The company will spend $5 million on exploring their highly prospective land package of 29 mining concessions, covering some 70,000 hectares of land, beginning with Barbasco and hopes to spend double that that next year. We like the shares here, particularly for their exploration upside, which we recall from Dr. Keith Barron, discoverer of FDN, as highly prospective. Buy.

Newmont Corp.

Newmont produced 1.3 million ounces at AISC of $1,097 per ounce. The largest gold producer in the world, with a portfolio of 12 operating mines and two joint ventures with Barrick is capable of producing 6 million ounces a year for most of this decade, generating free cash flow of a billion dollars plus a year for the next five years. In the last quarter, Newmont restarted three sites, focusing on turning around Goldcorp’s Eleonore in Quebec and Penasquito in Mexico. In South America, Newmont focused on developing Yanacocha’s sulphides to extend their flagship’s life. Newmont has a strong balance sheet with $6.7 billion of liquidity. While Newmont is considered a core stock, we prefer more potential growth-oriented and lower cost Barrick.

Yamana Gold Inc.

Yamana produced 164,000 ounces in the quarter with a solid contribution from Jacobina (46,000 ounces) and joint venture Canadian Malartic. An update to expand Jacobina was tabled which will cost $57 million to boost output 30%. Yamana plans to list on the London Stock Exchange to broaden shareholder reach but we note that London Exchange players support mostly African plays. Earlier, many mines left London and switched to North American exchanges because of a broader market and prohibitive listing costs. We think the move is more arm-waving than substantive since Yamana’s problem is not shareholder recognition, but too high debt and high cost mines. Sell.

John R. Ing

Please refer to the Legal Section of our website (maisonplacements.com) for our Research Disclosures for an explanation of our rating structure at https://maisonplacements.com/research-reports.

********