Gold: A Rising Tide Lifts All Boats

The greatest blackout in US history saw millions of Texans without heat as a polar vortex knocked out half of the United State’s energy grid, shutting down more than 4 million barrels a day of output or 40 percent of US production. Meantime for almost a year, the Western world’s economy has been in a deep freeze despite trillions of subsidies and programmes to revive their economies from the pandemic. During this year’s devasting hurricanes, droughts in the Southwest, Californian fires, to Texas’ power outages, there is an obvious need for boosting America’s outdated infrastructure and regulations. The pandemic and climate change demonstrate the challenges ahead and the need to spread scarce resources as the First World faces repeated Third World problems. It seems that America’s new economic binary is that of a Third World country, politically and socially, with the highest Covid death rates and one of the deepest recessions in the world.

US Credit Binge

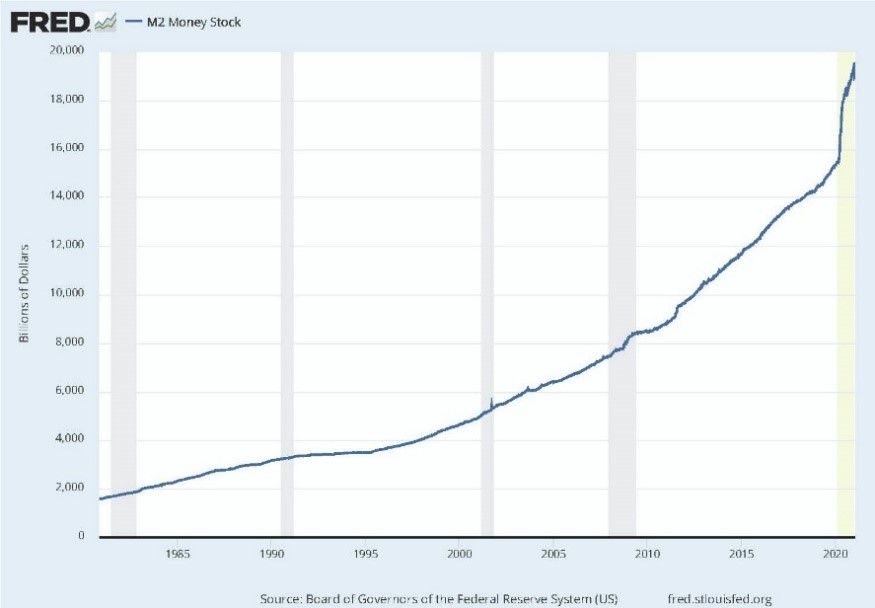

Despite the blowout in US fiscal policy and an explosion in government spending of historic proportions, the price tag to combat the pandemic and resuscitate the economy rises as Congress approved its sixth bailout. In America, complacent investors have failed to spot a pivotal shift in financial markets, preferring to celebrate the market’s daily highs as the avalanche of cheap money inflates assets. Up, up and away! The Fed flooded the system with liquidity by increasing the broader money supply M2 28 percent, the fastest pace ever. The mood is euphoric. America itself is a bubble that must go deeper into debt just to keep everything going. The Fed has handed out trillions, that even exceeded lost revenues but, rather than provide the framework to revive the economy, the Fed has lost control of the markets as monetary policy fuels speculation and a stock market boom.

The danger is that policymakers and investors believe that the monetary and fiscal stimulus is the perfect antidote to the once in a century pandemic. This time money was deposited directly into household accounts as stimulus checks, unlike previous government stimulus programmes, when after the 2009 financial crash, money found its way into Wall Street accounts and bond traders’ positions. With stimuli at 15 percent of GDP and budget deficits already exceeding World War II levels, there is little concern that at $28 trillion, that the record US debt levels will restrict options to stimulate growth. Public debt to GDP is more than 100% of GDP, that spells trouble, inflation trouble.

Signs of bubbles are everywhere and negative yields have made borrowing money never cheaper, which benefits the big borrowers such as governments, allowing them to rack up huge debts at little cost or consequences. The absence of inflation made their massive debt loads manageable, aided in part by their own central bank purchases of most of that debt, reinforcing the market’s erroneous logic that low rates are a permanent state of affairs. However, as the economy surges, so will inflationary pressures. Other central banks like the ECB, Australia and Korea have even upped their bond buying to keep rates low because they believe more bond buying means more liquidity to help the faltering economy. Although market sentiment has shifted with inflation expectations and real rates rising sharply, central banks are willing to let inflation expectations overshoot and are reluctant to take the punch bowl away.

Thus, we expect a booming “Twenties” type of economy, aided in part by Mr. Biden’s gargantuan $1.9 trillion-dollar American Rescue Plan package which is twice Mr. Obama’s stimulus package in a leftward shift that gives the White House a bigger role and widens America’s social safety net. And, there is yet another spending package, a $2 trillion Green New Deal to be paid by more borrowed money (MMT). The Fed’s willingness to accommodate even higher inflation rates and the American dream is reflected in the record federal spending, deficits and level of debt already reached in February. However, unless America is to be an eternal debtor, it has to raise taxes, something it has not done for almost 30 years.

YOLO Meets FOMO

Today excess liquidity has added fuel to powerful markets everywhere, which are recording daily record highs. Rising markets seem to lift all boats including the art market boat. Once the venue of the old rich and baby boomers, markets have attracted a new generation of investors who have flocked to tech-related stocks like Tesla and Amazon, aided by the boom in online trading of the zero free commission platforms of Robinhood and TD Ameritrade. Strategies like short squeezes took on new forms as millions of newbie investors piled into GameStop, a once dominant digital retailer, eschewing valuations or trading algorithms of the old money crowd. A new generation of investors joined Wall Street’s exclusive party with the “you only live once” (YOLO) crowd, meeting the “fear of missing out” (FOMO) crowd, as social media replaces the old time “boiler rooms”.

All things digital have become the new meme, replacing the brick and mortars of the old generation. After the 2009 crash, Wall Street was forced to dismantle proprietary trading desks and abandon market making which resulted in the loss of market liquidity. But a decade later, Wall Street has created new and improved trading vehicles such as exchange traded funds (ETFs) and special purpose acquisition companies (SPACs), which quickly grew in popularity. Paving the way were WFH supercharged traders who added to the liquidity aided by stimulus checks and the digital platforms of the algo and high frequency players like Citadel and Virtu, who prospered because their black boxes were even faster. Liquidity begat liquidity.

Just Another Ponzi Scheme

The simplest stock fraud is a “Ponzi scheme” that generates returns to the earliest investors from later investors. As the scheme attracts more and more investors, the fraudsters pay out to the early players but some end up keeping most for themselves. Of course, with the need to bring in more money, this “house of cards” eventually collapses. “Ponzi” schemes were named after Charles Ponzi who duped investors in the 1920s.

Today, financial populism has blurred the boundaries between real and faux reality as well as a challenge for lawmakers and regulators. Markets today appear to be a gigantic Ponzi scheme with the earlier investors (Wall Street) making money off the online retail investors who trade on platforms like Robinhood with these latecomers, the losers. Timing is everything.

As for the much talked about GameStop, there are a number of lessons. First like a “Ponzi” scheme, people who got in early, were the big winners. In GameStop, those hedge funds that were “short” early, were actually the big losers but eventually those who were short later, made big money. The biggest losers were those Reddit players, who discovered the run up last and thinking they could duplicate results, lost big. Finally, we knew how this would end. Nothing changed, just the players. Ironically despite the short squeeze that saw $2.2 billion of GameStop shares covered, GameStop remains one of the markets’ most heavily shorted situations, according to the Institutional Investor.

The digital platforms have even created a new type of cryptocurrency, non-fungible tokens (NFT), a special crypto-token digitizing unique pieces of art, trading cards or any other collectible, but not interchangeable or fungible like bitcoin. Art as a digital clip all of a sudden has value and unrelated to their artistic value have become vehicles for speculation with some increasing 300% last year. Art has become like their bearers, tradeable snowflakes.

Inflation Is Dead, The Obituaries Are Premature

Since the nineties, inflation has been non-existent but three decades later, rising inflation warnings are being ignored as in the fable of the “Boy Who Cried Wolf”, who repeatedly cried wolf because he was bored, but when a wolf actually showed up, the villagers ignored him and the sheep were lost. Today the warnings of inflation, because of massive deficits and levels of debt are being ignored, just as markets believed in the 60s that a surge in inflation was impossible. The conditions are ripe for a comeback. They were wrong then, and today. History teaches us otherwise. In the late sixties, the Fed accommodated deficit spending to fight the Vietnam War and finance President Lyndon Johnson’s “Great Society”. Within two years, the direct consequence of the ‘guns and butter” decision led to higher government spending, deficits and inflation. Gold went from $32 to a peak of $875 an ounce in 1980 or a 2,634 percent gain.

Inflation is already here and the warning signs are everywhere, in booming markets, art prices collectibles and currencies. In stealth-like fashion, inflation has moved closer to the targeted 2 percent, fuelled largely by the massive stimulus packages which represented a whopping 15 percent of America’s GDP. Markets too are dynamic, recording successive highs. Add in a new round of $1,400 stimulus checks and rising import costs due to a weaker dollar, you have the toxic combination of the cost-push inflation of the late 60s and early 70s, when double digit inflation required double digit interest rates and a recession to stop near hyperinflation.

Yet, despite the threat of higher rates, the Fed is reluctant to end the cheap money stance because of the 2013 market collapse when a hawkish Ben Bernanke tightened in a” taper tantrum”, that erased 30% of the gains in a month. Not wanting to repeat Bernanke’s taper tantrum, the Fed has downplayed the concerns and will tolerate an overshoot of the targeted 2%, notwithstanding that the combination of ultra-low rates and overheated markets elevates systemic risk and quashes the price discovery of other assets. The problem is that we declared the patient dead from the symptoms, not the causes. Inflation is very much alive.

If the supply of Kobe beef were as plentiful as bushels of wheat, the price of Kobe beef would be lower given the relationship to supply and demand. Likewise, if the supply of money increases too fast, goods will cost more as money buys less. For much of the 20th century and part of this century, the quantity of money was fixed to gold. That changed in two stages with the latest in 1971 when President Nixon severed the link to gold, flooding the world with dollars. The money gates were opened. Since then, not surprisingly the purchasing power of the dollar has declined 90 percent while gold peaked at $2,000 an ounce. The money explosion isn’t over.

Commodities are a lead indicator of inflation. In addition, hopes for a vaccine-driven global economic recovery juiced by the record amounts of fiscal stimulus have, in our opinion, laid the foundations for the first leg of a supercycle similar to 2000s or seventies. Hopes for a structural bull market in commodities were boosted by China’s early recovery from the pandemic and unprecedented spending by global governments. Looking beyond the memes and mania, the other signs of a Fed-enabled frothy market is the herds’ switch from GamesStop to bigger game, commodities. Silver was the first choice when over one billion ounces of silver traded in one day. However, commodities were already in an upswing fueled by pent-up consumer, supply bottlenecks and industrial demand for raw materials and China’s voracious appetite.

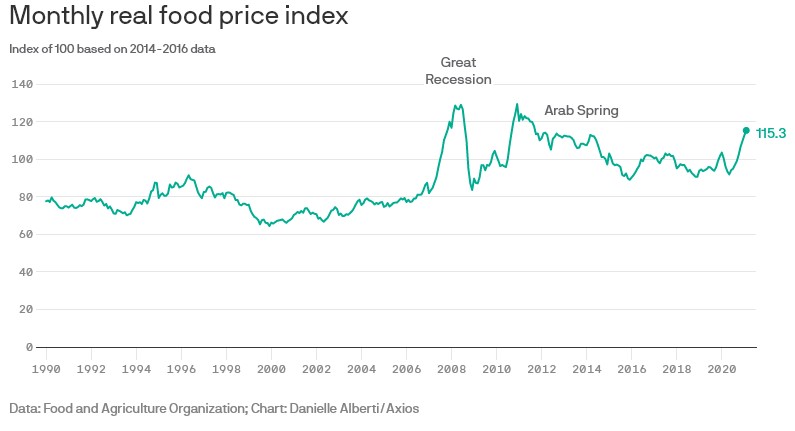

Steel prices are at the highest level in more than a decade on the back of a rebound in Chinese demand. Copper has risen 40 percent as the shift to the green economy accelerates. Trump’s trade war with China forced commodities like soybeans higher, doubling in price in the last year. Crude oil has jumped 75 percent since November due to OPEC production cuts. Food prices have increased every month since May. It would appear that trees can grow to the sky. We believe there is a secular change happening. The longer the Fed resists putting its foot on the monetary brakes, the closer we get to an out-of-control inflation or even hyperinflation.

Bubbles Aren’t a Problem, Until They Pop

Resurgent nationalism and Donald Trump’s assault on the rules-based global order played a major part in unleashing a new era of protectionism and tariffs, which shutdown significant international trading capacity. The pandemic itself disrupted supply chains such that bottlenecks at key ports show no signs of disappearing. New projects need lead times of anywhere from four years to a decade and supply constraints have already pushed up inflation, making new projects more expensive. A semi-conductor chip shortage that shutdown carmakers’ production line caused a political crisis in Washington. Yet bubbles aren’t a problem, until they pop.

With investors chasing returns wherever they can find them and at a time of maximum bullishness, current uber “Big Tech” valuations are vulnerable to corrections because the companies are “priced for perfection”. At the same time governments are looking for ways to finance their deficits and tax the behemoths or even break up the powerful web companies. The “pay for content” is only the beginning as government seek new revenues from the golden geese. Change and higher taxes are coming.

As the tide drifts out, the world will look for alternatives.

Then there is the geopolitical uncertainty. As a result of the distrust of Western hegemony and tug-of-war between America and China, we believe there is a movement towards economic blocs around the US, China and a revigorated Europe. Vaccine nationalism already has taken its toll with deep divisions as countries hoard domestic supplies or block critical raw material exports, putting political and commercial interests ahead of humanitarian interests in a vaccine cold war. No longer is there a dependence on US hegemony and, the “America First” stance has resulted in a diversification from the dollar ecosystem as well as multilateral relationships. In the New Year of the OX, China’s renminbi is slowly climbing in importance with a rumoured backing by gold, raising Western eyebrows. In a year in which geopolitics has been extremely volatile, currency nationalism has also surfaced and the world desirous of an alternative financial order, rather than American-led debt-ridden world order is looking to China as a healthy offset to US financial hegemony, particularly since America has become the world’s largest debtor, whilst China is the world’s largest creditor.

Geopolitics and deficits do matter. Markets are complacent in the view that despite record debts, the cost of borrowing is minimal. America’s decade of money printing not only fueled a bull market of historic proportions but papered over systemic long-term economic problems and inequities. America’s response to the pandemic has been massive monetary financing (MMT) and large-scale asset purchases, racking up record amounts of debt. Foreign investors own a third of that debt and were among the biggest buyers of Treasuries but lately have shown less appetite for money losing debt. And, despite the hardening of relations between China and the US, China remains the largest holder of that debt. Today, there is no certainty that they would want more dollars, since they already own more than $1 trillion of America’s debt. We believe America’s fiscal profligacy is its Achilles heel.

To be sure, the past few years of American politics have taken a toll in the world’s trust in America and its leadership role. The Trumpian rollback in free trade, and blowout in deficit spending has led to diminished trust, eroding faith in the US dollar as the world’s global reserve currency.. The dollar’s vulnerability is exacerbated by the scale of the Fed’s efforts to keep rates low through bond buying and an extremely loose monetary policy, which has lowered the return of safe assets and increased demand for risky ones.

The Swamp Drains

At a time of maximum bullishness, markets are vulnerable to a correction and with the correction, overlooked abuses, overvalued shares and over overachievers have been exposed. The swamp is draining with echoes of 2008. Late February, credit default swaps (CDS) were triggered on Greensill capital notes following Credit Suisse’s suspension of $10 billon of funding to Greensill, which specialized in supply chain financing, using derivatives in a Ponzi-type structure. And last month, there was the bankruptcy of Texas’ largest cooperative power generator, as the financial fallout from the ice storm saw Brazos Electric Power Corporation face more then $2.1 billion in bills when electricity soared to $50 billion overnight. Or, there is the “payment for order flow” which allowed trading platform Robinhood to offer zero commission because, they received the bulk of their revenues from hedge funds who pay for their order flow, allowing the “market makers” to front run Robinhood’s orders in a predatory fashion. To no surprise, the SEC is investigating their business model, which is banned in most other jurisdictions because their clients often get “second best” execution.

Then, on a broader scale there is the disruption of the $21 trillion US government debt market which saw 10-year Treasury yields skyrocket from 0.90% to over 1.60%, triggering a massive market sell-off and drying up liquidity in what is considered the largest and most liquid market in the world. And, after a sale of the seven-year Treasury auction nearly flopped, markets froze temporarily on concerns reminiscent of the near failure in the repo market last year which forced the Fed to intervene to restore order. The massive auctions are necessary as the government must finance Mr. Biden’s $1.9 trillion stimulus package worth some 8 percent of US GDP. Then there are bonds, of which many are yielding negative returns, that guarantee losses if held to maturity. The fixed income sector is particularly vulnerable to an upswing in interest rates, which threatens to end their 40-year bull run. The tide is moving out. As in the past, the massive Biden stimulus could invite a return of the bond market vigilantes. Cracks are appearing, heightening concern in this so-called risk-free market, which could be the trigger for a financially disruptive bursting of the bubble.

The internet, then social media and now digital currencies have reflected a technological revolution that has swept the markets, lifting all boats. While stocks are backed by the faith and expectations of future earnings, today bitcoin is considered money, yet possesses no sovereign imprimatur and therefore not subject to government control. Running on peer-to-peer networks whose value is backed by the faith of the “eye of the beholder” or a sort of financial Wikipedia, prices have skyrocketed, rising from $5,000 to $55,000 this year.

That is the rub. The bull market has lifted all boats. In the race to capitalize on new opportunities, investors have succumbed to the age-old disease that affects our markets. Greed. Greed is not good. Faith becomes scarce when bubbles bursts. If governments continue to pile up debt and keep printing money, fear of currency debasement and the consequential inflation will create a bullish condition for gold. Since fiat money has no backing or limit of supplies like gold, investors would be wiser to wait for the tide to go out. This new era is only beginning.

Recommendations

Commodities are lead indicators of inflation. Most are priced in dollars and the recent slide in the dollar has made them cheaper in other currencies, further boosting demand. Meantime, years of lower prices have forced the shutdown of capacity and curbs in spending, holding back supplies. The oil industry is a good example where low shale oil prices curbed production and capex spending.

In essence the avalanche of central bank and fiscal stimuli have created a series of bubbles, overflowing into other markets like commodities where agricultural, industrial, and energy bubbles have reached their highest levels since 2013. Although the boom-like conditions raises hopes of the biggest economic boom in a generation, America’s economy is on a slippery slope and self-destructive path. The stimulus package and war on Covid was not paid by higher taxes or bond sales to the public but by debt that has tripled in 12 years and, there is more to come. Money supply has skyrocketed and the profligate spending only widened the wealth gap, undermining the US dollar role as the world’s reserve currency.

Gold is a casualty of the tug-a-war between the Fed and the markets. The sharp spike in rates have firmed the greenback, causing a correction in gold, which has fallen almost 18 percent from the record high at $2,000. Also, the rallying markets and the vaccine rollout has deflated some of gold’s “safe-haven” characteristics. However, seasonal demand from large consuming countries like China and India will put a floor under the price as China continues to buy more gold than it produces. Also supporting higher prices are real yields, which remain negative despite the uptick in rates. We believe gold’s bull market remains intact on expectations that the US dollar is a suspect currency because of the size of US deficits and escalating debt load. We continue to expect $2,200 an ounce as gold’s next target. Gold remains a barometer of investor anxiety of which there is much ahead.

The next generation of gold mines will have to cope with lower grades, more hostile jurisdictions and tougher environmental restrictions such that the long lead times between “pick to pour” will mean supplies won’t be available until the end of the decade. The industry did not replace reserves last year. Meantime, the industry is awash in cash so M&A activity is one of the cheaper ways to boost depleting reserves since it is cheaper to buy ounces on Bay Street than to go out exploring. We believe M&A activity will gather momentum with miners needing to replace declining reserves, particularly since the average market cap per ounce at in-situ reserves is less than $500 an ounce. IAMGold’s acquisition of Monarch, Agnico’s buyout of Hope Bay, Evolution’s bid for Battle North, Red Lake Mining, Kinross’ purchase of Peak Gold and Newmont’s $400 million bid for GT Gold, suggest that the game of musical chairs has only just begun as the industry gobbles up cheap reserves on Bay Street. Gold companies will attract even the value players because of their low P/E multiples and above average dividend payments.

We thus continue to favour the senior producers like Barrick and Agnico Eagle. We also like growth oriented B2Gold and Lundin Gold. We believe Eldorado and Kirkland Lake, Centerra and Centamin will be among the likely participants in M&A game of musical chairs. Developers like McEwen Gold and Osisko are cashed up, poised to bring on new production. New players like Victoria Gold and Equinox Gold should be looked at now that the teething problems are behind them.

Agnico Eagle Mines Ltd.

Agnico's latest results were ahead of expectations, producing 500,000 ounces in the quarter generating $1.2 billion of cash flow for the year. Agnico will produce 2 million ounces this year, an 18 percent improvement over last year. However, the next few years out, Canadian Malartic’s Odyssey, and Amaruq in Nunavut will boost output by 300,000 ounces which some found lower than projected. Agnico’s reserves were boosted by 12 percent to 24 million ounces due to 3.3 million ounces from Hammond Reef. As for Hope Bay, they are starting anew because Hope Bay was a sinkhole for money due to a poorly developed processing plant and plans. A new mine plan is required. Reserves are there but Hope Bay has become another one of Agnico’s development projects.

Meantime, Agnico will spend $160 million on exploration and $800 million on capex. At Kittila in Finland, the expansion will boost average tonnage to 2 million tonnes per year despite a delay with shaft sinking. At the Canadian Malartic joint venture, about $30 million will be spent on drilling, largely at East Gouldie as that mine switches from an open pit to the largest underground operation in Canada. Agnico has abundant free cash flow, great execution capabilities and an array of development projects. The pullback in the shares presents an attractive buy opportunity.

B2Gold Corp.

B2gold reported net income of $672 million for the year, benefitting from a trio of low-cost operations. B2Gold had a record year producing one million ounces from Fekola (623,000 ounces), Masbate (205,000 ounces) and Otjikoto (168,000 ounces) in Namibia at an AISC of $926 an ounce. B2Gold’s next producer will be the Columbian Gramalote joint venture, which could produce 400,000 ounces with half attributable to B2Gold. Construction could begin this year and a feasibility study is expected in April. After expanding Fekola to 7.5 Mtpa from 6 Mtpa and adding to the fleet, the company is looking to mine nearby satellite deposits, Cardinal and Anaconda which is only 20 kilometres away. B2Gold has almost half a billion of cash and is net debt free. AISC is an industry low of $900 at ounce and the company plans to spend $66 million on exploration. We like the shares here.

Barrick Gold Corp.

The world’s second largest producer has become a cash machine and upped its shareholder payouts by declaring a return of capital of $750 million, from the sale of $1.5 billion of noncore assets. Barrick reaffirmed guidance at 4.7 million ounces at an AISC of $1,000 per ounce. Barrick also sold Lagunas Norte in Peru for $81 million, removing closure liabilities as part of its sale of non-core assets. Left out of this guidance is PNG’s Porgera mine, which is locked in a dispute with the government over the renewal of its mining lease. History shows that the government’s desire to kill the golden goose always ends in a give and take, but mines do not stay idle for too long. With $3.4 billion of free cash flow, Barrick’s cash hoard is about $5.2 billion and net debt position is zero, a far cry from the $13 billon of debt in 2013. This year, Barrick should generate another $4 billion of cash with a healthy contribution from Bully in Tanzania. We like the shares down here.

Centerra Gold Inc.

Centerra will produce between 700,000 – 800,000 ounces this year but lower grades from flagship Kumtor in the Kyrgyz Republic will boost AISC to $1,000 an ounce (due to sequencing). Newly commissioned Oksut in Turkey will produce 100,000 ounces. Mount Milligan in BC should produce between 180,000 – 200,000 ounces and 70 million pounds of copper, with the water problems behind them. Cash flow is expected between $750 and $800 million with Oksut generating $100 million of free cash flow. Centerra’s new life of mine (LOM) plan for Kumtor increases reserves from 3 million ounces to 6 million ounces, extending that mine’s life from 5 years to 11 years. Centerra has a debt-free balance sheet with $545 million of cash so share buybacks or dividend hikes are possible. Hold.

Eldorado Gold Corp.

Mid-tier Eldorado maintained its guidance this year between 430,000 – 460,000 ounces at AISC of $1,000 an ounce. Eldorado boosted reserves at Lamaque in Quebec adding 800,000 ounces of gold at 9.5 g/t from Ormaque, which could be mined in the latter part of this year. Eldorado acquired QMX in Quebec, a tuck-in acquisition. After protracted negotiations, Eldorado entered into an agreement with the Greek government for development of Skouries, Olympias and Stratoni, which could finally surface hidden value after two decades of talks. The deal needs to be ratified by the Greek Parliament but allows resumption of Skouries development. We like the shares for the hidden Greek value.

IAMGold Corp.

IAMGold had a disappointing quarter producing 653,000 ounces last year but AISC jumped to $1,300 an ounce. This year, IAMGold’s production will be flat with reserves slipping to 14 million ounces since the miner did not replace reserves last year. Essakane was a bright light producing 364,000 ounces. However, the company must spend a good part of $1 billion to fund the joint venture Côté Gold over the next two years with $355 million to be spent this year. Also, IAMGold’s total sustaining capital will top $120 million while non-sustaining capital totals $590 million. We thus believe IAMGold’s shares are dead money, particularly given the potential downside risk if Côté is not be the project as advertised. Sell.

Kinross Gold Corporation

Kinross had a flat year producing 2.4 million gold equivalent ounces from flagship Paracatu in Brazil, Kupol in Russia and Tasiast in Mauritania. Cash flow was almost one billion and Kinross ended the year with over $1.2 billion in cash and equivalents versus total debt of $1.9 billon. Kinross should produce 2.4 million ounces this year but Tasiast will produce fewer ounces pushing AISC to $1,025 an ounce. Kinross is expected to spend $900 million this year and $120 million on exploration. Reserves were boosted at Lobo Marte where a feasibility study is set to be released before yearend. Unfortunately, Kinross’ big capex plans will drain cash over the next few years so the shares are dead money for a while. We prefer B2Gold here.

Kirkland Lake Gold Ltd.

Kirkland reported a solid quarter producing 370,000 ounces in the quarter for record full year production of 1.4 million ounces at AISC of $800 an ounce. Free cash flow was $733 million with Detour contributing 40 percent. Kirkland’s balance sheet is strong with cash piling up to $850 million and no debt. As a result, the miner bought back almost 19 million shares and paid $115 million in dividends. Guidance for this year was unchanged. Fosterville in Australia reserve grade slipped largely due to depletion and the high-grade mine has a short life. Overall, Kinross’ resources are pegged at 20 million ounces reflecting the rationale for acquiring Detour Lake mine which has a long reserve life. Sustaining capex at Detour was $270 million. At Macassa, shaft sinking is at 4,240 feet with a targeted depth at 6,400 feet to be reached late 2022, a year ahead of schedule. Kirkland shares have done well and we expect them to be on the acquisition trail again, using their richly valued paper.

Lundin Gold Inc.

High grade miner, Lundin had a good quarter producing 97,000 ounces and 242,000 ounces in its first year of production at Fruta del Norte (FDN) in Ecuador. Generating positive cash flow, FDN is expected to produce about 400,000 ounces at a low AISC of $800 an ounce, generating free cash flow of $300 million. We expect Lundin to aggressively pay down debt incurred to build FDN and the Company has begun an aggressive exploration programme on its extensive Ecuadorian land position. We like the shares here for potential exploration surprises. Buy.

New Gold Inc.

New Gold produced almost 67,000 ounces in the latest quarter due to higher grades at Rainy River and New Afton. However, AISC increased to $1,491 per equivalent ounce. Cash on hand improved to $185 million allowing them to redeem $200 million of notes. Renaud Adams has turned around operations and Rainy River’s mill ran at 150,000 tpd which should result in a pick-up in production and lower costs. However, a new mine plan at New Afton following the mud-slide has become now a four-year project. On a brighter note, the Company surfaced hidden value by selling Blackwater for $190 million of cash and an 8 percent gold stream. Although Blackwater has reserves of 8 million ounces of gold and 61 million ounces of silver, the capital cost was too high for New Gold. While New Gold may be a turnaround situation, over the near term, there are better buys like B2Gold or Eldorado.

Newmont Mining Corp

Newmont reserves were flat last year joining other miners who encountered difficulties replacing reserves with the drill bit. Newmont’s reserves fell to 94 million ounces of which 35 percent are in North America. Newmont plans to spend $215 million on exploration and purchased GT gold for $400 million whose Tatogga copper-gold Saddle North project is in the Golden Triangle. While Newmont produced 1.6 million ounces in the fourth quarter, meeting guidance of 5.9 million ounces, production slipped 11 percent from a year earlier as they pruned the Goldcorp portfolio. Newmont generated a whopping $3.6 billion of free cash flow and holds $5.5 billion in cash allowing them to buy back shares (last year share buyback $1 billion) as well maintain a liberal dividend policy tied to the gold price. At Tanami, Newmont produced 600,000 ounces at AISC of $745 an ounce. Tanami’s expansion will involve a 1.6-kilometre deep production shaft to boost output by 150,000 or 200,000 ounces per year. Nonetheless, we prefer Barrick shares for its upside superior potential.

Yamana Gold Inc.

Yamana provided 901,000 ounces of (geQ), meeting guidance. Jacobina produced 44,000 ounces in the quarter and almost 180,000 ounces for the year. El Penon in Chile, continues producing 43,000 ounces and 930,000 ounces of silver but the mine is mature. Yamana’s profile for the next few years is flat with AISC around $1,000 an ounce. Resources are almost 14 million ounces of gold with newly acquired Wasamac in Quebec adding 1.8 million ounces and an updated feasibility study is planned for this year. Nonetheless, Yamana has too much debt for our liking. Sell.

John R. Ing

Please refer to the Legal Section of our website (maisonplacements.com) for our Research Disclosures for an explanation of our rating structure at https://maisonplacements.com/research-reports.

********