Gold: Wars, Wars and More Wars

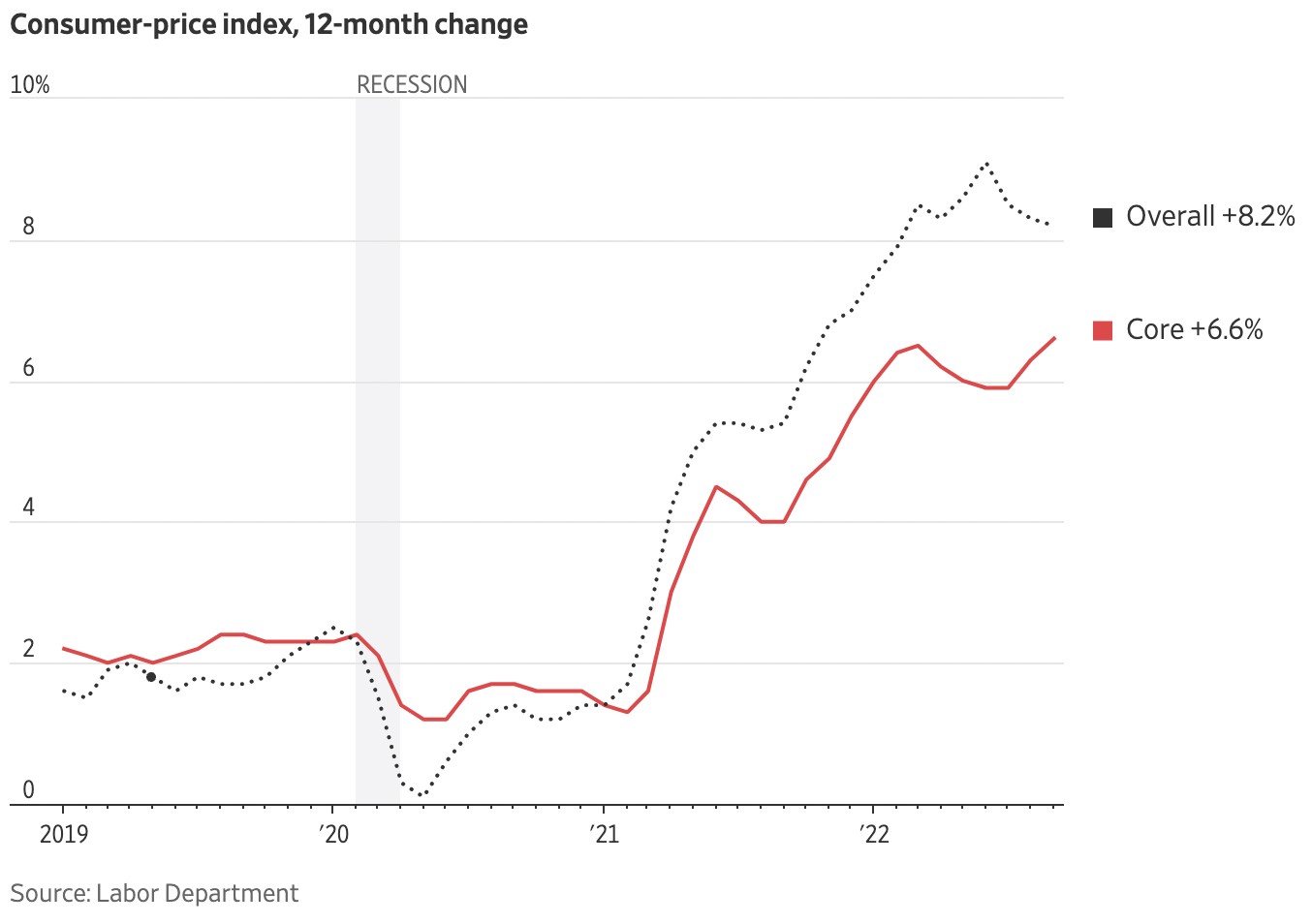

This month a cooling CPI number sparked a mammoth rally on Wall Street on hopes that the Federal Reserve may be ready for a pivot (aka capitulation) in its battle against inflation. The gains are premature and won’t change the trajectory of the economy. Global inflation soared to 40-year highs from the monetary excesses of the past as governments unleashed trillions of dollars of additional spending, stoking the inflationary fires. Yet, despite the concern over rate increases, the global economy remains resilient. US households and companies are flush with cash from pandemic support packages. US capacity utilization are at 14-year highs. Q3 GDP grew 2.6%. Unemployment is back to pre-pandemic lows. Wages are up 8.2% fueling demand. Consequently with inflation so broadly based, investors’ hopes of a reprieve from rate increases will probably prove unfounded and yet another head fake or false dawn.

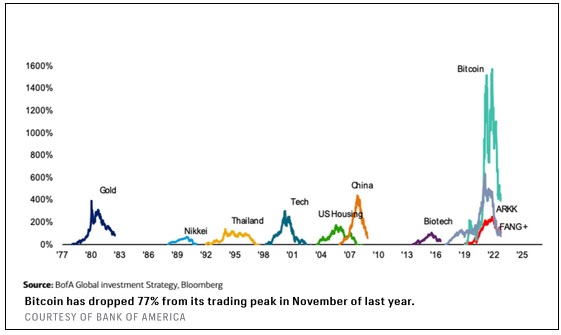

Also feeding inflation are wars. Wars cost money. They have substantial costs and have bankrupted nations. The US war efforts in Afghanistan, Iraq and Vietnam were debt financed, and those war debts and free spending governments produced more inflation, made worse by the pandemic stimulus. The decades of unfunded deficits, quantitative easing, and trillions of public spending created a faux sense of prosperity made possible by artificially low interest rates and cheap credit. At the same time central banks led by the Fed kept rates near zero using experimental techniques to revive inflation. It worked. But the corresponding boost to debt and consumption also created the biggest stock market bubble in history. The Fed’s free money sent a behavioral incentive to markets that not only money was free, but risk too was free. The FTX crypto pyramid implosion could put a $10-50 billion hole in the market. However, the mirage vanished when Biden’s colossal spending, the war and state intervention let inflation get out of hand forcing the Fed to crank up interest rates to tame inflation. And now investors must deal with both a raging war, soaring prices and skyrocketing interest rates deepening the financial hole between government expenditures and revenues. However deficits financed by new borrowings cannot go on forever as the UK discovered when they announced tax cuts, triggering a near collapse of their pension funds.

The problem is that consecutive budget deficits of 10% plus of GDP financed when money was cheap allowed governments to spend without repercussions. And governments kept on spending, funded by the central banks’ purchases of government debt leading to the inflation of today. First, the pandemic and now the Ukraine war. Tomorrow might be the need for more spending to boost an economic recovery to offset the soaring cost of scarce energy, food and credit.

The End of Cheap Money

Money is now expensive and dear. The important point though is amid this feast to famine, little was done to boost supplies and less to control out-of-control spending to stop fueling inflation. And today’s inflation is more than the cost of energy or food.

Inflation is simply too much money chasing too few goods. Inflation is high because spending has remained high and monetary policy too loose. History shows that money is the clear root of inflation, aided by spendthrift governments and complicit central banks. Economist Milton Friedman once observed that inflation, “is always and everywhere a monetary phenomenon”, as part of the centuries-old quantity theory of money that holds prices are linked to the growth in money. Once believing that inflation was a transitory phenomenon, central banks now face problems putting the inflation genie back in the bottle. Most investors blame the adverse effect on Russia. Others fear rising rates will trigger a debt avalanche and the end of the long boom. The main culprit was the generous government spending on the pandemic, war, climate change and handouts aided by their central banks’ toolbox of experimental quantitative easing and outright purchases of $15 trillion of their own debt. Now that inflation is surging, central banks who earlier believed it was transitory have turned the screws on the global economy to tame an inflation that has become deeply entrenched and persistent.

Having misread inflation, policymakers are now misreading its causes. And as runaway inflation sends rates higher, markets are straining at the seams as we face a liquidity crunch in financial markets that has already caused a change in the UK government and now a crypto implosion. The stock market is in trouble because the bond market has already crashed. This is just the latest in a string of liquidity problems and as the liquidity swamp drains, only the ugly frogs are left, a harbinger of what is to come.

You Can’t Suck and Blow at The Same Time

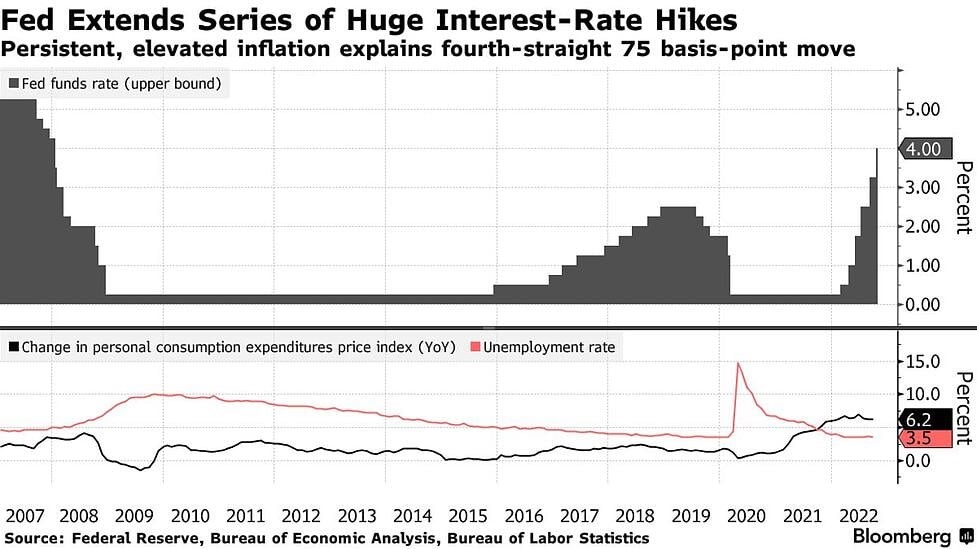

Fiscal and monetary policy are related. As inflation rages and a deepening recession looms, the market hopes that governments will again succumb or pivot back to their free spending ways to avoid a UK type crash. That was the path in the 70s when deficit financing to fight the Vietnam War and President Johnson's War on Poverty, unleashed double-digit inflation. Then the oil embargo hit. After hiking rates in the wake of serial commodity price shocks, policymakers prematurely declared victory over inflation when they saw the economy weaken and slashed rates. But those inflation embers grew to a fire, needing inflation-busting Fed Chair Paul Volcker to raise rates to double-digit levels which caused two recessions to bring inflation from 20% to 3.5%. Forty years on, the latest cycle is no different.

The out-of-sync conflict between fiscal and monetary policies is also being waged elsewhere. In Europe, pandemic support already cost half a trillion euros with the Italian government spending 11% of GDP and the French 10% of GDP. So far the politicians’ solution to rising prices is the introduction of massive subsidy support programs, windfall taxes, cheap loans and price caps costing some half a trillion dollars of public funds which stretches already tight sovereign balance sheets. The situation is dangerous.

With the US government debt topping $31 trillion and annual trillion-dollar deficits, the Treasury has to issue and refund debt at a whopping $5 trillion a year, forcing the central bank to print money to pay for America’s bills, contributing to solidly entrenched inflation as too many dollars again chases too little supplies. The Fed is in a box as fiscal policy pushes in the opposite direction of monetary policy, undermining the central bank’s effort to curb inflation. The yield on benchmark 10-year Treasuries jumped the most since the pandemic. Without both working together to squeeze inflation, history shows that you can’t suck and blow at the same time. In previous high inflation periods, the common denominator was this lack of both a monetary policy anchor and a sufficiently credible central bank response which resulted in the lack of monetary co-ordination.

Faced with the resultant spiral in decades-high inflation and sinking markets, some central banks have already pivoted, reversing course, relaxing monetary policy in a repeat of yesteryear. Canada has slowed its rate increases and European politicians, fearful of their jobs have stepped up spending in defiance of their central banks amid signs that investors are getting more nervous about the limits of fiscal deficits, particularly following the turmoil that engulfed the UK debt market. Volatility begats more volatility. The increased volatility is due to a series of events as countries discover that “exiting” or so-called quantitative tightening (QT) is not so easy. Governments haven’t got the message, particularly in America where the midterms were accompanied by extra rounds of spending. If the UK can so easily botch its “exit”, what is to happen with the United States?

Chickens Come Home to Roost

The first casualty is Japan, which spent $60 billion in FX markets for the first time since 1991 to defend a collapsing yen that fell to its lowest levels since the seventies, aggravated by the Bank of Japan’s refusal to move rates in line with the global community. In maintaining an ultra-loose monetary policy, they hope to postpone the day of reckoning. Not so lucky was UK’s Liz Truss who quit in reaction to her mini-Budget’s deficit-financed tax cuts which triggered a conflict between a lax fiscal policy and a tighter monetary policy. Her “tough” stance did not last long as both the Bank of England and government capitulated in a policy U-turn and re-instituted quantitative easing by buying $65 billion of government debt to save their pension funds that will drive inflation and interest rates higher. Truss served the shortest serving ever in office for a British prime minister, burying a queen, the pound and her government in only 45 days.

We recall in 2013, the Fed similarly tried to tighten but “pivoted” when global markets nosedived in a “taper-tantrum.” A looming source of trouble today is the Fed’s quantitative tightening (QT) to reduce the $9 trillion balance sheet which has quadrupled from a decade of bond purchases, increasing the supply of money and now playing an outsized role in the opaque $24 trillion Treasury market. However this time in removing $95 billion a month liquidity from the market, the Fed’s taper is made more difficult because of the book losses of $1 trillion against a paltry $42 billion of the Fed’s capital, requiring more accounting creativity. Normally, they could always print more, or can they? US broad money supply has shrunk from 30% to only 1% in the six months to July. In the UK, the government had to transfer $12.4 billion to cover the Bank of England’s red ink in its bond buying program. We believe that unlike the global financial crisis of 2007-2009 when over-extended financial institutions failed, this time it is sovereign governments’ turn as a game of chicken plays out between “independent” central bankers and their free spending elected officials.

Energy Geopolitics Boosts Inflation

Amid the energy crisis sparked by Russia’s invasion of Ukraine, prices skyrocketed as Putin squeezed supplies to force the EU to abandon Ukraine. The surging energy costs created the biggest shock to the global energy infrastructure since the oil embargoes of the seventies. The brutal invasion only accelerated secular inflation as soaring natural gas prices caused demand destruction and energy-saving ways. Governments reacted with handouts, windfall taxes and massive interventions with average energy bailouts at 5% of GDP, declaring an energy war in addition to that other war where checks and spare tanks were being shipped to Ukraine. Today there are no winners, only losers in a war without end.

Things could get worse before they get better. The EU previously relied on Russia for close to 40% of its gas and more than half its coal and as a result, industries from fertilizer producers to steel makers to glass makers had to shutdown, unable to pay increased fuel bills. The EU is set to ban crude oil imports from Russia. Although America is one of the world’s largest oil producers at 11.4 million barrels of oil, they are also the largest consumer of some 20 million barrels a day, leaving them exposed since they must import some 8 million barrels of oil and petroleum products. Price caps or windfall taxes will only drive energy investments to other lower taxed jurisdictions, while robbing OPEC Gulf countries of revenues. US wholesale natural gas is up 68% this year. Any cap or windfall tax on one market such as Europe would send energy to other markets like Asia, risking a “beggar-thy-neighbour” conflict. Similarly Norway’s blockage of electricity exports or Germany’s purchases of scarce LNG supplies underlines the need for EU unity. Part of the problem is that Europe’s energy market is not a unified bloc but consists of 27 energy “private” fiefdoms.

The world’s fourth biggest economy, Germany built its mighty industrial complex on cheap Russian gas and that reliance backfired, as surging energy costs curtailed consumer spending, forcing factories to curb production. As de-industrialization set in, Arcelor Mittal, one of the largest steel complexes in the world will shut down two important mills. Germany has scrapped its fiscal austerity and has had to borrow a gorilla-sized $200 billion energy support package or 5% of GDP to help their citizens survive the gas crisis, violating EU’s solidarity in a return of realpolitiks. Germany once relied on exports to provide growth, but the war, higher costs for energy and China’s lockdown has removed an important prop to Europe’s economy. Who will replace Germany?

The US is vulnerable as the oil industry could not replace shortages at a time when the oil taps were needed to be turned on. At the same time to push gasoline prices down ahead of the midterms, Biden dumped a couple hundred million barrels of oil from the Strategic Petroleum Reserve which is at 38-year lows. In defiance of Washington, Middle East players have accepted renminbi and OPEC (including Russia) cut back output by 2 million barrels a day to boost oil prices, moving away from long time Western allies with the setting up a Petro-bloc along with an Asian bloc, upending the world order. Consequently, energy has become a pawn with negative economic spillovers, further enhancing inflation.

Climate Change Compounds Uncertainty

The new reality is that decarbonization itself is inflationary. Borrowings to finance energy subsidies, fuel rebates and caps might soften the near-term impact from inflation, but the underlying debt is a primary cause of inflation. We are not yet predicting hyperinflation but like the seventies, the causes and effects are eerily underway. And amid fast-changing climate changes, the world has never been so imbalanced with poorly allocated credit and unintended consequences. Mr. Biden’s ramping up of climate change expenditures hurt him in the midterms and exacerbated inflation by shutting down fossil fuels which accounts for some 80% of America’s usage. And despite higher prices, US oil industry output has flattened due to overregulation and the lack of investment after the Biden administration’s war on fossil fuels stopped pipelines and canceled oil leases. History shows that the conflict between the central bank and government is a dangerous step that has often triggered hyperinflation spirals in the past.

In addition to energy, the Russian invasion exposed the globe’s vulnerability to the availability of agriculture and water in the face of a dangerous combination of war, drought and higher prices for food and fertilizers. Without co-operation there is that other war of climate change. The decoupling between China and the US has implications for climate change as both countries are responsible for over 40% of global emissions. A growing population in the developing world has caused a decline in arable farmland colliding with precarious water supplies, such that agriculture like energy has been weaponized. Plant-based proteins have gone to a premium. And a global drought has taken down hydropower from California to Chile, driving up prices. Ironically one of the unintended consequences of the lack of water is that coal consumption has increased 6% as utilities try to maintain electricity supplies. Moreover decarbonizing our power grid whilst boosting infrastructure to meet increased demand from the electrification of energy for cars to steel mills can no longer be kicked down the road, yet another boost to inflation.

Sanctions Too Increase Risks in Financial System

Chastened by a string of failed military interventions, the US resorted to sanctions as a low-cost alternative to warfare. Banning investors from purchasing Russian bonds, and the confiscation of half of Russia’s $600 billion of currency reserves was meant to increase the cost of credit and paralyze the Russian financial system. The waves of western sanctions were to cripple the Russian economy yet Russian oil revenues are more than when they invaded Ukraine. When Western companies pulled out of Russia, the ruble lost 25% of its value, but is higher today than when Russian tanks moved into Kiev and today, Russia has little external debt and despite the exclusion from the Western backed SWIFT financial payments system, Russia continues to pay their bills, bypassing the dollar and the western financial ecosystem. Yet the war continues, another inflationary input.

Still, when was the last time sanctions worked? Sanctions are not an effective deterrent because the world economy has become interrelated. Economic sanctions have a long history of being broken. Still Washington is intent on keeping the pressure on Moscow despite the blowback and its knock-on effects on domestic food and energy prices. Moreover not all countries have observed or enforced America’s sanctions. Iran, Venezuela, Cuba and other authoritarian states helped circumvent the sanctions, but others like Indonesia and Sri Lanka bought cheap Russian crude. Not surprisingly, China and India have also purchased cheap oil in yuan and rubles, offsetting their energy costs, circumventing the Western sanctions.

Above all, the United States continues deep commercial links with and is dependent on Russian uranium supplies - no price caps there. The EU and US continues to buy Russian nickel and aluminum from Russia’s Rusal as well as other critical metals needed for defense work. Noteworthy is that excluded from the sanctions, Russia’s state-owned Rosatom is one of the world’s largest nuclear plant builders, which accounts for 40% of the world’s uranium enrichment capacity. Nonetheless governments and companies worried about supply chain interruptions and the lack of domestic supplies of critical minerals, are attempting to subsidize and bring back production to North America, heaping costs on American taxpayers and yet another input to long-term inflationary pressures.

Derivatives of Mass Destruction

When the UK “mini” Budget forced the Bank of England to intervene to stop a collapse of the pension fund industry, derivatives played a major role since many were unable to meet cash collateral calls of their LDIs or liability driven risk derivatives. These Wall Street created derivatives were designed to hedge against inflation and interest rates. All this was symptomatic of the freewheeling debt-fueled era when “no cost” leverage credit default swaps (CDS) triggered the 2008 financial meltdown, contributing to the collapse of housing and Wall Street firms.

Today there are different players but derivatives continue to be used in the trading market when an estimated $1.5 trillion of derivative contracts or weapons of mass destruction almost sank the UK pension funds. And today with stretched balance sheets and soaring interest rates there are similar pressures on the banks and power utilities as new and improved toxic derivatives have surfaced with inflationary implications. Amid the plans to electrify economies, surging electricity costs are a fresh source of inflationary problems but worse are the industry’s usage of derivatives of mass destruction which has become part and parcel of today’s ecosystem. The consequences are equally inflationary as the recent saving of utilities from collapse, threatens to trigger another derivative implosion. As prices skyrocketed, so have the liabilities and the need for more collateral and for some, bailouts demonstrated by Germany’s Uniper, which had to be nationalized by the government after an initial $15 billion bailout. Overlooked energy is as a critical part of our infrastructure as our banking system. The derivative time bomb fuse has been lit. We about to pay the price for our complacency.

The Dollar Is King

Rising US rates and troubles around the globe have also translated into a soaring dollar trading at levels not seen since the start of the century, wreaking havoc everywhere but America. The greenback, the world’s reserve currency is used in trade and finance, and its strength has lifted borrowing costs, the price of imports and inflation elsewhere. A wave of dollar strength has sent currencies like the euro, Japanese yen and British pound to multi-decade lows, squeezing global credit which is a problem for America's allies because stronger dollar-priced imports and high dollar debts come at a time when domestic inflation is climbing. The dollar is king. A strong dollar translates into cheaper foreign made imports helping moderate US inflation.

Modern-day central bankers believe they have more power than the market and old time “bond vigilantes”. From Greenspan to Bernanke to Powell, a few cryptic utterances were often enough to settle markets. That won’t work today. Fundamentals do matter. Investors or the market reacts to economic forces to protect assets. Only a change in economic forces will get the results desired by the central banks, not their mandarin’s utterances. In the case of the collapsing pound, Britain’s gilt market turmoil sparked a rethink. The same truth holds for the yen. The market is sending a message. Debt matters. The free lunch of yesteryear is over. However it seems that Liz Truss, the Biden government and Japanese authorities did not get the message.

Currency Crisis

Now under pressure of rapid rate increases and soaring inflation, the global debt burden led by America raises the spectre of a debt contagion crisis. America’s interest cost alone will exceed $1 trillion which is more than they spend on defense spending. With a Republican controlled House, America faces gridlock. No party has a solution to inflation except maybe more spending which would be equally inflationary. Also, America’s faster growth has led to a widening of the current account deficit and a surge in imports, unmatched by the rise in exports exacerbating a serious payment situation. Current account imbalances affect currency values because they determine the degree to which a country has to attract external financings.

“Our currency, but your problem”, said John Connally, Treasury Secretary for Richard Nixon at a meeting in 1971. While a strong dollar helps moderate US inflation, the reverse is true for others. Most are dollar dependent, having to pay more for critical oil, natural gas and food, as well as higher interest costs. The Fed’s raising of rates is a key driver to a “global reverse currency war” in which countries have resorted to supporting their currencies through FX support, in a “beggar thy neighbour” reminiscent of the Great Depression, exacerbating a shock rise in the US dollar and domestic inflation. In treadmill fashion as currencies hit new lows, current account deficits soar, pushing rates even higher increasing risk of some kind of financial or economic blow-up.

The dollar has been strong before. In 1985 we can recall when the US dollar was similarly strong causing governments to intervene as the dollar was hurting their currencies and an escalation of trade tensions. Back then, Ronald Reagan’s supply-side revolution and stimulative low-tax fiscal policy clashed with the Fed trying to rein in inflation which resulted in US deficits reaching 5% of gross domestic production. Consequently Japan joined the US, Britain, France and West Germany at the Plaza Hotel to sign “The Plaza Accord”, an agreement to jointly intervene in the currency markets to drive down the dollar’s value. It worked. Over the next decade the dollar dropped. To counter the stronger yen, Japanese interest rates were slashed as part of a huge fiscal stimulus program which resulted in stock market and land bubbles. However, those bubbles eventually burst resulting in Japan’s lost decade, which turned into two lost decades.

Today the dollar similarly appears unstoppable. Using 1985 as a reference point, current fiscal policy remains expansionary while monetary policy has contracted with deficits again approaching 5% of GDP. Lacking in savings, the US has taken advantage of the dollar’s primacy as the world’s reserve currency, drawing heavily on foreign borrowings to finance consumption. Noteworthy is that while the market frets about Britain’s deteriorating finances, America is in worst shape with total debt to GDP at 130% versus Britain’s stoic 86%. And as before, the US has been running twin deficits (trade and budget) which is unsustainable. Politically the US midterms were marked by polarisation, political violence and denials at a time when the divided states of America’s relative power is under threat.

There is another war looming – for the soul of America. The most expensive midterms ever shows that the divided state of America is undermining the system of government and democracy itself. The violent uprising on January 6 was only the beginning. The Democrats believe that they lost the House because of Donald Trump’s interference. The Republicans, now emboldened are ready to sink the Biden’s presidency, paving the way for an ugly 2024. Expect outright war and while Mr. Biden voiced that democracy itself was at risk, it was pocketbook issues that sunk his party – it’s the economy stupid. Elected two years ago on a backlash against Trump, Biden steered his party’s agenda to the extreme left, spending trillions contributing to the runaway inflation, hurting voters. Today rather than feel their pain, he instead alienated their values. Voters are worried. Neither party has a solution. Of concern is that over the next two years America will be involved in internecine warfare and its finances and dollar will be ignored. That is about to change.

Wars, Wars and More Wars

History shows that money creation as a means of financing wars in every case, resulted in substantial inflation. The US government has racked up the world’s largest debt, financing their economy after the 2008 crash, multiple wars then and now, a pandemic and now a green revolution. In the aftermath, the United States is also waging an economic war with China, Russia, a climate change war and a war with “Big Oil”. Wars are inflationary and often triggered hyperinflation. The habit is hard to break as the US has already provided Ukraine $60 billion for the war effort. Initially the cost was negligible, but the protracted war and the need to replace munitions and equipment along with the new cold war with Russia, and China will help turbocharge an embedded inflation. No wonder that the average inflation rate of 10 percent over 10 years grows.

The US has become complacent, printing money to pay its bills. America’s debt is built on trust, the trust that they can pay their bills and repay that debt. That trust is fragile, as Britain’s novice Prime Minister Truss discovered that risks in the financial ecosystem can easily bubble up from nowhere, igniting massive sales of debt, triggering instability in the markets overnight. Deficits do matter.

A Chinese Reserve Currency?

The era where both China and America mutually prospered from globalization is past with both inflationary and financial implications. Not surprisingly decoupling has toughened both sides with long reaching implications as the US tries to thwart China’s rise with trade and technology sanctions. America’s fiscal recklessness has caused an increase in protectionist sentiment as America divides the world, polarizing allies with no shades of gray (except for Canada’s me- tooism). Business feels otherwise, at the Shanghai Import/Export Expo, over half of Fortune 500 companies were in attendance. The recent thawing in relations is welcome since the two leading powers are no longer competitors but adversaries, underlining the need to co-exist to prevent conflicts. While a clash with America has caused a deep rift among America's allies, a potential costly economic war where energy, food and finance become pawns would leave only losers, feeding inflation further.

China’s market, voracious consumers and trillions of financial reserves will be a formidable challenge to the American-led world order. Although China enjoys a huge lead in AI, chip-making and 5G, the United States has declared a tech war, targeting imports of critical semiconductors from China and even barring US citizens from working for Chinese tech companies. We believe the move is a serious setback in the technology race since Silicon Valley benefited from the relationship and access to China’s $16.3 trillion digital economy. Despite sentiments to the country, Americans rely on China for everything from Apple products to Teslas. Today even Israel spends more of its GDP on R&D. And significantly, the US relies on China for the critical materials such as rare earths, a key building block in the technology ecosystem, giving Mr. Xi a hold over America’s economy. Of concern is that China too could use the same argument by withholding rare metals, vital to America’s modern technology-dependant economy.

China has four times the population of the US and four times the potential economic growth after lifting 800 million people out of extreme poverty. The second largest economy remains the largest market in the world and importantly, the world’s banker. China’s national savings and investment are both about 40% of GDP. China was the global engine after the Great Recession and after two years of lockdowns, China’s reopening will have widespread impact on everything from commodities to luxury goods to energy as the dragon’s consumers begin to spend again.

To be sure America’s economic war with China increases global instability and isolates itself needlessly, risking blowbacks everywhere. Moreover, while America's debt grows, its massive unfunded liabilities like Social Security, Medicare and federal pensions also grow, deepening the financial hole. Another example of its profligacy is Mr. Biden's opportunistic massive student loan debt forgiveness plan that puts another $500 billion of financing on the inflationary fires. Filling America’s financing hole is impossible, particularly when capital has become scarce. Japan has been among the world’s largest buyers of US Treasuries for years, but they have reduced their holdings as part of an effort to support its ailing yen. China is also among the largest investors, holding some $1 trillion of American debt. Noteworthy is that China has not participated in six consecutive monthly auctions in the US, creating a potential financing problem in that any boycott would drive US yields even higher, at home and aboard. And, what would happen if they wanted their money back?

The Dollar Is Strong Until It Isn’t

But what of the dollar? What will be the catalyst that will sink the US dollar?

First, America’s profligate government spends more than it taxes, borrows more from the market, especially from foreigners to fill the fiscal hole. In the past decade to boost a sluggish economy, the government embraced unprecedented spending and the Fed accommodated with a mixture of easy money and low interest rates which resulted in America having the highest debt to GDP among the G7 countries at 130% of GDP up from 34.3% in 1982. US household debt grew at the fastest pace since 2008 topping $16.5 trillion. America’s deficit is more than 6% of GDP and the national debt remains the highest in the world, ensuring that with a GOP controlled House, those debt ceiling showdowns will return. Too much debt is America’s Achilles' heel.

Second, America’s debt to GDP rivals the all-time World War II peak and will worsen this year under the pandemic, support programs for Ukraine and rounds of social spending programs. As Germany’s dependence on cheap Russian energy led to its vulnerability, so does America’s dependence on others to bridge the gap between what it produces and what it consumes. Britain’s fiscal soap opera shows what it looks like to have fiscal policy in conflict with monetary policy, forcing the Bank of England to declare “chicken” on tightening, undermining its credibility as UK’s borrowing costs nears those of Italy.

Third, governments earlier misallocated revenues from the strongest global economy in decades and instead deployed climate change subsidies, generous pandemic stimulus and social plans that added to spending and debt, making the financing gap worse. Politicians had become complacent about finance, believing deficits didn’t matter because money was free. Deficits matter as the British government discovered when their “mini-Budget” of tax cuts and spending provoked a market fallout and a collapse of the government. America’s finances too have been left to depend upon the kindness of strangers. The more imminent risk is that with the Fed no longer buying government debt and China’s interest waning, who will buy America’s debt? The UK’s financial crisis serves as a warning that amassing debt without regard to paying it back is risky. A new era of financial and economic change is in place, yet the politicians just don’t get it.

Today America’s mountain of debt keeps growing and almost 25 percent of America's debt is held by outsiders, of which a large portion are Chinese and Japanese investors. We believe a pivot reckoning is in the offing. Gold has an inverse relationship with the dollar which has eased 7% on hopes of cooler inflation and a Powell pivot. We believe the tenuous hopes of a Powell pivot will prove to be the catalyst for the long-awaited collapse in the dollar. When the music stops, America’s monster debt and internal divisions will be laid bare.

As Good As Gold

Our view is that the era of the dollar’s “exorbitant privilege” is ending and its strength is unsustainable. China is the world’s second largest economy whose industrial capacity surpasses that of the US, Germany and Japan combined. China also has the largest financial reserves in the world. The US wrongly views China as the greatest test to its primacy. Wrong. It is itself.

The economic and political challenge is that a divided America in scapegoating others jeopardises its future. True, exorbitant privilege enables them to borrow in a currency it prints, however its self-destructive behaviour, massive debt and profligacy, based on “exceptionalism politics” ignores the laws of economies. Exceptionalism has to be earned, not taken for granted. And this is where the dollar comes into play. This time as rates head higher, there are more and more dollar claims and while this large overhang of borrowings from abroad finances America’s government and twin deficits, it also plants the seeds of the dollar’s downfall. A lower dollar will prove to the catalyst for lower markets and this time, Paul Volcker is not around.

Gold is an alternative to the dollar. It is an index of currency fears. We believe that today’s economic situation has eerie parallels with the 1930s, particularly since Washington gridlock now risks open civil war. A week after the midterm election, neither party clinched and the result is a stalemate in Congress, frustrating Mr. Biden’s ambitious agenda of healthcare, climate change and aid to Ukraine. Without confidence in the dollar, there is no reserve currency. If confidence is not restored, as we saw with the pound, anything can happen. Gold will be a good thing to have.

Which Way Is Up?

Despite a powerful rally on cooler inflation data, the S&P500 is down 16% while gold prices have fallen 4.5 percent from a year ago. Still gold has been a disappointing asset, surprisingly, given that gold is considered an inflation hedge, and a safe haven in times of turmoil. Russia's invasion of Ukraine should have seen the gold price soar but instead dropped like a stone. The war continues. Gold broke the $1,800 level, $1,700 level but successfully held $1,600/oz back to the pre-pandemic levels. The main reason for gold/dollar’s non-performance was the super strong dollar climbing 11% against a basket of six peers this year as investors were attracted by the Fed’s higher rates.

Importantly however, gold in yen is up 16 percent, gold in pounds up 8 percent and gold/euros up 5 percent. Gold has done what it should, protecting yen, euro and pound assets from falling currencies, and acting as a safe haven asset during financial stress. Only in dollars that gold has not done well. Co-incidentally central banks have also added to their gold reserves by almost 400 tonnes in the third quarter after boosting their reserves last year by 80%, according to the World Gold Council. China and Russia were among the biggest buyers. And since April, 527 tonnes of gold have moved from Western vaults to Asian vaults as Chinese gold imports hit all-time highs in August, according to the CME Group and the London Bullion Market Association. And we continue to expect gold to reach $2,200/oz in this current cycle with resistance at $1,800/oz.

Recommendations

Gold producers’ earnings were lower in the third quarter due to rising costs and lower bullion prices and in some cases, production shortfalls. Guidance edged down to the lower range. We believe gold producers’ valuations are nonetheless particularly attractive with most possessing abundant free cash flow and dividend increases. In situ reserves in the ground are low by historic standards, ensuring continued M&A activity since it is cheaper to buy reserves on Bay Street than to put money in the ground. In addition, there have been few discoveries reinforcing our view that we are still in a supercycle. In addition, exploration spending remains subdued as the low hanging fruit has been picked and mine grade has declined, making gold more expensive to mine. Moreover as the mining industry reduces carbon emissions, costs have increased, in particular the cost to build new discoveries which are in the billions, as IAMGOLD has discovered.

Despite gold trading above $1,700 per ounce, there are some gold companies that are not making money. In fact, junior Pure Gold filed bankruptcy because of cost overruns and operating problems at Madsen in Red Lake. Madsen operated for 40 years and was mined out, but new management optimistically believed that the mine could produce another million ounces. Wrong. Management’s optimism resulted in a rush to production and the lack of continuity plus cost overruns was a big reason for the failure. Not all gold miners are alike, and we would favour the seniors who are cash flow positive with an array of tier I assets end, and on the other end, avoid those that are barely making money and having to finance huge projects. Selectivity is paramount. We thus continue to recommend Barrick and Agnico Eagle among the seniors. We like developers B2Gold and McEwen Mining. We also like Lundin Gold, Centamin, Eldorado and Dundee as future players in the M&A game.

Agnico Eagle Mines Ltd.

Agnico produced a solid 817,000 ounces at an all-in cost near $1,100 per ounce. The results were in line with expectations with a record contribution from Amaruq. Costs have increased while the company looks for efficiencies, but operating margins remain healthy. Agnico Eagle repaid $100 million of debt in the quarter and maintains a healthy balance sheet. At high grade Macassa, the extension of the underground ramp and additional ventilation has been complete, allowing drills to operate from the ramp. At Detour Lake, the new life of mine was updated which extended Detour’s already long mine life. Next quarter there should be an improved contribution from high grade Fosterville in Australia and Meliadine which is being expanded to 6,000 tpd. Agnico paid a slight premium for full ownership of the Malartic mine allowing for operational and cash flow synergies, particularly since a yearend reserve update at Odyssey is expected with 14 drill rigs currently turning. Agnico Eagle maintained their guidance and the Malartic acquisition will boost production by 10% next year and credit Agnico with almost 8 million ounce resource. Buy.

Barrick Gold Corp.

Barrick, the second largest producer in the world, reported strong operating cash flow of $760 million on third-quarter production of about 1 million ounces at the low-end of its guidance (due to sequencing) but maintained annual guidance of 4.2 million to 4.6 million ounces at cash costs of $891/oz. Barrick is expected to boost production in the last quarter with higher grades from long-life Nevada Gold Mines Joint Venture, Veladero and Pueblo Viejo in the Dominican Republic. The copper contribution from Lumwana (mine life to 2042) and Zaldívar was also a major contributor and copper is now a significant part (25%) of Barrick's outlook. Construction at Pueblo Viejo is 70% complete with capex at $1.4 billion in line with earlier estimates. Barrick is also retiring a half billion of notes (2042). A ramped up Goldrush and Turquoise Ridge will also be contributors next year. The Reko Diq joint venture in Pakistan won’t be into production until 2028, however we continue to recommend the shares for their organic growth potential.

B2Gold Corp.

B2Gold produced 220,000 ounces in the quarter which was on the low side of their guidance at AISC of $1,154/oz, higher than expected. Production at flagship Fekola in Mali was affected by rainfall which prevented access to higher grade ore. Fekola produced 130,000 ounces in the quarter which was below estimates. The company expects an improvement in the fourth quarter, producing 77,000 ounces in October alone and B2Gold is expected to produce 1 million ounces this year at cash cost under $700/oz. At Otjikoto, the company only produced 35,000 ounces due to delays in the underground operations, following a change in contractors. Nonetheless the company expects production between 165,000 to 175,000 ounces. B2Gold is one of the lowest cost gold producers in the world with a strong balance sheet of $550 million cash and a $600 million undrawn line with a $200 million accordion. Debt is a paltry $63 million. To replace the JV Gramalote (AngloGold) which is to be sold because of not meeting thresholds, B2Gold is studying expanding Fekola’s phase 2 complex through an expansion of mine and processing facilities at Anaconda which could add a potential 800,000 ounces by 2026. We like the shares here for B2Gold’s growth profile.

Centerra Gold Inc.

Centerra gold will buy back about 7% of the shares taking advantage of the weakness in the company's share price following the nationalization of their major asset Kumtor in the Kyrgyz Republic. Centerra is hard pressed to maintain output at the Mount Milligan copper gold mine in BC and the Öksüt gold mine in Turkey which coincidentally shutdown because of mercury at its ADR plant. A new EIA has to be filed. Costs increased while Centerra released a new life of mine plan for Mount Milligan which extended the low-grade deposit life by 4 years to 2033. Nonetheless Centerra will only produce 250,000 or so ounces, about half last year’s guidance and is hard pressed to replace the loss of Kumtor. We think there are better situations elsewhere.

Eldorado Gold Corp.

Mid-tier Eldorado reported a third quarter loss of $51 million on production of 119,000 ounces at a cash cost of $803/oz due to higher costs and increased electricity prices in Greece and Turkey. Kışladağ in Turkey again had a bad quarter as the company's HPGR attempts to extract more gold from heap leaching pads is proving difficult. Eldorado will meet the lower end of their full year guidance of 460,000 to 490,000 ounces at best. Eldorado reported negative cash flow of $26 million due to increased development at Skouries. Eldorado has a mandate letter with Greek banks for €680 million project financing which is an initial step to get this big project off the ground. Olympias produced only 16,000 ounces in the quarter which was a disappointment. Eldorado is a hold here on expectations that they can extract value from their Greek operations, specifically Skouries. The good news is that the balance sheet has $300 million of unrestricted cash. Hold.

IAMGOLD Corp.

IAMGOLD sold Rosebel in Suriname to Zijin Mining of China for $360 million which was an attractive price. The proceeds will be applied to the Côté Gold project which still needs at least another $1.2 billion to complete. But, with the Rosebel sale goes needed production and the company's existing mines are not sufficient to finance Côté Gold. Côté Gold is overbudget and the project costs keep going up at over $2 billion and pouring its first gold bar is years away. We believe Côté Gold is a company breaker not a company builder. The miner lost money in the quarter and will be hard pressed to finance the shortfall. As such, we would sell IAMGOLD.

Lundin Gold Inc.

Lundin Gold reported completion of the South Ventilation Raise (SVR) at 100% owned Fruta del Norte (FDN) gold mine in Ecuador which allows efficiencies and a boost in tonnage. Lundin produced 122,000 ounces in the quarter due to higher grades and better recoveries. The completion of the SVR allows access also to higher grade ore resulting in Lundin raising its guidance from 390,000 to 430,000-460,000 ounces this year at AISC of $850/oz. Lundin also reported cash of $300 million as they pile up a cash against about $600 million of long-term debt incurred to build the world's highest-grade gold mine. We like the shares here for its long-term growth prospects and exploration potential of its largely unexplored lands.

McEwen Mining Inc.

The developer produced 35,700 (GEQ) ounces because of grade and bottleneck issues at Fox Complex. San José in Argentina was affected by Covid. Those issues were not new. The key is to find enough resource which to replace now depleted Froome at Fox. A crushing plant will be installed boosting efficiency. The company’s PEA suggests a potential 80,000 ounces over 8 years at IRR of 21%, thus the need to find more resources. At Gold Bar in Nevada, the systems are large but elusive. Gold Bar, a heap leaching operation, was plagued by poor waste to strip ratio and carbonaceous ore, so AISC was $2,000/oz. Gold Bar South is better grade and little carbonaceous ore which should bump up output (Gold Bar accounts for one quarter of production). Also there is upside from Rio Tinto’s Kennecott joint venture to invest $80 million to earn a 60% in McEwen’s Elder Creek also in Nevada. Surprisingly, MUX will restart El Gallo in Mexico with a refurbished 7,000 tonne per day processing plant to reprocess leach pads. All in all, the problems this year should be behind MUX. McEwen Copper’s $82 million financing was completed with a subsidiary of Rio Tinto. MUX will own 68% of McEwen Copper and thus the parts are worth more than the whole. Buy.

New Gold Inc.

New Gold’s Rainy River faced heavy rain and despite production from the Intrepid Zone produced 91,000 (GEO) up from the second quarter. Nonetheless New Gold reported a quarterly loss with AISC at $1,600/oz due to spending $73 million of which $42 million was spent on sustaining capital. The strip ratio was also high. While New Gold hopes to improve its life of mine (LOM) plan, Rainy River is a low-grade deposit and the company's difficulties are expected to continue. The underground Intrepid development continues with some revenues reported in the last quarter. Still, faced with top heavy debt at $305 million and underperforming assets, we would sell the shares.

Newmont Corp.

Newmont had an uncharacteristic poor quarter missing both revenue and earnings guidance whilst cash flow was negative. Newmont produced 1.5 million ounces at all in cost of $1,200/oz. Newmont generated about $466 million in operating cash flow but capex in the quarter was $529 million resulting in negative cash flow of $63 million. Nonetheless, Newmont retained guidance at 6 million ounces at an all-in cost of $1,150 per ounce. Boddington in Australia continues to be a drag impacted by heavy rain. Newmont’s near-term outlook depends on Ahafo North whose capital cost has increased and production won’t begin until mid-2025. Newmont has delayed the huge Yanachocha sulfides project as they rework the basic economics, given increased costs. After spending $300 million to buyout the remaining balance, it is surprising that they are having a second look – so much money and so little results. Newmont does have a stellar balance sheet with $6.7 billion in total liquidity, but its large capex and drop off in cash flow could yet impact dividend payments which is tied to operations. We prefer Barrick here because Newmont's production profile is flat for a few years.

John R. Ing

*********

More from Gold-Eagle