Gold's Bid Is The Real Deal

I know, I know, Goldman Sachs Smart Alecks are now on record as of this past Tuesday (16 February) for Gold to return back down to 1100 within three months time, and then to further tumble to 1000 by a year from now. To be sure, as we again update straightaway the following criteria and graphic as to "how we'll know when the bottom is in" -- specific to these metrics -- we don't yet know:

■ The weekly parabolic trend ought be Long ('tis)

■ Price ought be above the 300-day moving average ('tis)

■ The 300-day moving average itself ought be rising ('tis)

■ Price ought trade at least one full week clear above 1280 (hasn't)

But Gold's extraordinary resilience that characterized the "expected" down week just past -- settling yesterday (Friday) at 1227 -- suggests 'tis BS from GS and that Gold's bid this time 'round is the Real Deal. For as we've oft put forth in these missives, just as "the market is never wrong" to the downside, the same now applies to the upside. Don't miss the ride. Here are the weekly bars in stride:

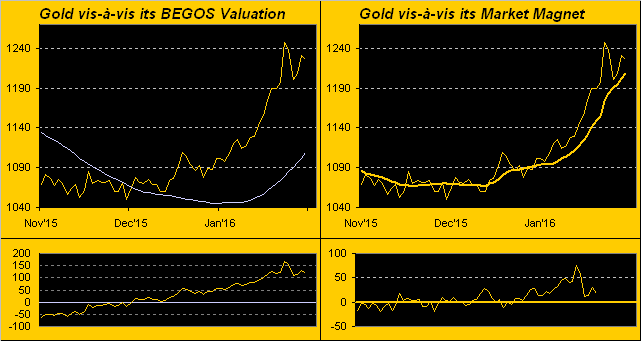

Next, let's reinforce the strength of the Gold bid. We just used the word "expected" with respect to Gold's having put in a down week, our repeatedly citing of late that price had become stretched to extreme upside levels vis-à-vis regressing its movements to those of the primary BEGOS Markets (Bond / Euro / Gold / Oil / S&P 500), as well as relative to Gold's Market Magnet (the 10-day moving average as weighted by the amount of contract volume per price point). Not that we're complaining about Gold having gone up too fast ... 'tis a beautiful thing! But relative to the two measures as below shown with Gold's daily closes for the past three months-to-date, look on the left at the robust upswing of the smooth pearly BEGOS valuation line: a week ago, Gold was (per the oscillator at the panel's foot of price less valuation) better than +150 points "high", indeed the highest distance ever since the 2011 All-Time High. Today, that difference is "still too high" at +118: but by the smooth line's rising at the rate 'tis, Gold doesn't have to go back over the cliff before again encountering the smooth line. Moreover, as we look to the right, Gold has essentially already unwound the extreme distance from its Market Magnet: from being in the extreme to simply back in the upstream:

As for putting to bed GS, they of course don't see Gold by said measures, (or don't so wish), nor can we blame them. Theirs is a fee-driven world. To board the Gold Bus could deter stock market thrust, reducing activity and thus fees that they trust. Heaven forbid having to shut down their "How Can We Fool 'Em Today Dept." Best to champion stocks for clientele whilst shoveling the commodity relic of Gold next to the worthless piles of tungsten and molybdenum. (

Speaking of stocks, there's now squawking that they're no longer on the rocks, the S&P having risen into this past week with three 30+ daily gains in a row. To wit, in Tuesday's wee hours on Bloomy Radio, we heard out of London the ever-respectable Stephen Mitchell (Jupiter Asset Management) acknowledge that asset levels had gotten a bit ahead of themselves, but with the [price earnings ratio of the S&P 500] coming into year's year at around 17.5x, there's value to be had; (they've an apt name for that firm's location given our year-end p/e for the S&P instead being 45.1x). But then in contrast during Wednesday's wee hours, again from London, came the dulcet tones of David Buik (Panmure Gordon) who upon looking into his crystal ball said he saw nothing, whilst underscoring the downside severity for stocks in starting the year such that caution ought be had. That's what makes a market. Here's the S&P (red line) from a year ago-to-date, featuring, of course, our Economic Barometer (blue line):

"Hey, it's starting to get better, mmb..."

And rightly so, Squire, as there've been a bevy of Baro boosting reports since its most recent low some two weeks ago: the StateSide rate of unemployment in January "officially" improved from 5.0% to 4.9%, whilst both hourly earnings and hours worked increased. Consumer credit also grew, as did retail sales, industrial production, capacity utilization, and inflation gauges. Why even the "Philly Phed" Index became "less negative". Ready for that March interest rate raise by the Federal Reserve Bank? (Not...)

In fact, there's much ado these days about more central banks crossing the line to negative depository rates, an option which even Federal Open Market Committee Chair Janet Yellen is nursing, and of which some are saying is simply a matter of time for the Fed to implement. "Make loans, else we'll eat away at your deposits!" Well, what if the loans made are not properly serviced nor repaid? "That's an irrelevancy! Make the damn loans!" See the problem? Got Gold?

Meanwhile as exports from Japan are falling to seven-year lows, (the Bank of Japan itself on Tuesday having begun assessing -0.1% for deposits), China isn't waiting around: purportedly, the banks there in January funded some $385 billion (¥2.5 trillion) in new loans, a lovely injection of faux dough into global currency coffers. Gold loves faux dough, and provably so even astride "Dollar strength" you know.

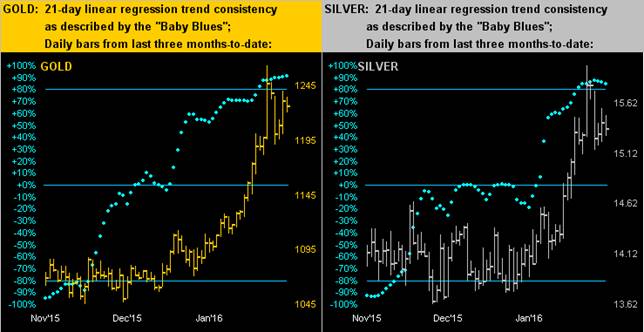

So in moving along "The Golden Road"--(The Grateful Dead, '67), below as shown we've the tracks of Gold (left) and Silver (right) via their daily bars over the last three-months to date, along with the baby blue dots which from day-to-day denote the consistency of the respective 21-day linear regression trends. 'Tis hard to top what is near perfection, so let's enjoy it:

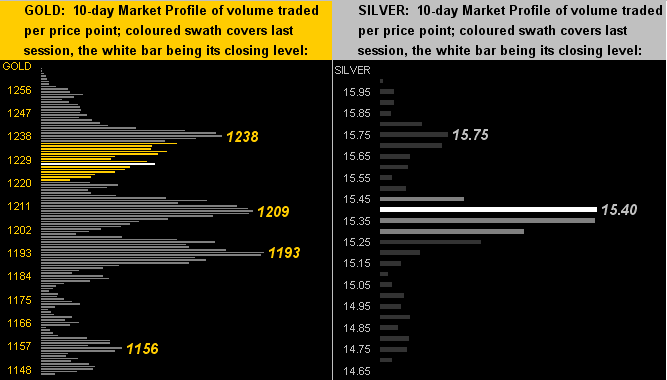

And in updating their 10-day Market Profiles, here again we've King Gold (left) and Sister Silver (right), the more material support/resistance apices as labeled...

...and as well incorporated into:

The Gold Stack

Gold's Value per Dollar Debasement, (from our opening "Scoreboard"): 2528

Gold’s All-Time High: 1923 (06 September 2011)

The Gateway to 2000: 1900+

Gold’s All-Time Closing High: 1900 (22 August 2011)

The Final Frontier: 1800-1900

The Northern Front: 1750-1800

On Maneuvers: 1579-1750

The Floor: 1466-1579

Le Sous-sol: Sub-1466

Base Camp: 1377

Neverland: The Whiny 1290s

Year-to-Date High: 1264

10-Session directional range: up to 1264 (from 1146) = +118 points or +10%

Resistance Band: 1240-1280

Trading Resistance: 1238

Gold Currently: 1227, (weighted-average trading range per day: 25 points)

Trading Support: 1209 / 1193 / 1156

10-Session “volume-weighted” average price magnet: 1208

The 300-Day Moving Average: 1158

The Weekly Parabolic Price to flip Short: 1088

Year-to-Date Low: 1061

Finally, this friendly reminder on the proper use (and not for the first time) of markets jargon. Let's preface our remark with the usual percentage tracks graphic of Gold vs. the S&P for the last 21 trading days (one month)-to-date:

The above chart fairly highlights Gold's robust upside move of late, and yet month-over month, the S&P is actually up some 3%. To be sure, since the S&P's all-time closing high of 2131 last 21 May, the index presently at 1918 is -10%, en route having been down as much as -14%. Here's the point, and not to specifically pick on The Telegraph's Mehreen Khan, (for quite a number of journalists have essentially said same), but she nonetheless posted a piece this past week citing "Global markets have crashed into bear market territory". A 14% correction in the S&P over these past nine months is not a "crash". Indeed, given how overdue 'tis been, we deem it as "normal". The closest event we've had to a "crash" in the past seven-to-eight years, (save for the 15-minute whirl-around of 06 May 2010), was during The Black Swan (2008/2009). Indeed should the S&P saunter down to our 2016 target of the low 1400s, we'd still refer to it as a "correction". That said, should we encounter a lock limit down day for the S&P futures, (5% overnight, else 7% during stock market hours), then we can consider use of the word "crash". Given the S&P's current level, that'd be a same day drop of some 95-134 points, (or for those of you who still watch the average at which our parents look, some 812 to 1,145 "Dow" points) ... just in case you're scoring at home, such that you'll know when it next occurs. In the interim, 30-point set backs here and there in the S&P ought best be considered as "noise". End of markets jargon lesson.

As to what's imminently occurring is a bountiful platter of incoming Econ Data to pour into the Econ Baro next week. Gold itself may pour a bit lower still, but well within its renewed context of boring back higher, for per this missive's title, we see of late Gold's bid as the Real Deal!

Now yer seein' the light!

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.