Have A Tipping Point Where Bond Interest And Inflation Both Matter A LOT

We have just entered those days of heady inflation that I have said will kill the stock market and bond funds. There is a tipping point at which inflation and the interest changes that respond to inflation matter, but it has never been a clearly defined point.

Inflation has now hit the level that is forcing the Fed to respond, as I’ve argued it would, and the Fed’s response will be a game changer, but it is a graduated response, so it has no clear tipping point. If the Fed simply ended its massive QE, the market would tip right away, but the Fed is tapering its response to inflation, as we all knew it would. The taper has begun and will continue because the Fed cannot back down due to inflation. The market, however, is still blind from years of believing the Fed always has its back to all that really means.

In my next Patron Post, I’ll be giving an overview of what is now the most precarious stock market in history. Let me start off by clarifying that, by “most precarious,” I’m not saying the market will crash right away. Inflation and the Fed tapering that inflation forces into place do their work over time, and the tapering show has only just begun.

Sentiment is still highly charged with mind-numbing testosterone and blind faith in the Fed. Being effectively braindead doesn’t mean investors won’t maintain their bullheaded stampede uphill awhile longer, but inflation will still relentlessly continue to pull like gravity on the market, and its gravity will keep increasing. No bull can run uphill against increasing gravity forever. Their run only means the market will have all the further to fall in order to catch down to reality. That time is not far off because of the main thing that I want to talk about in THIS article, which is the correlation between stocks and bond yields.

The Fed is in bondage

Now you are likely thinking, the Fed won’t let the market fall because it has arrested every fall for the last twenty years. You may believe the Fed will save the market, as so many investors due, because the Fed always has saved all markets from any disastrous landings for the last twenty years.

You must, however, keep in mind that this time is entirely different! This time the Fed is facing inflation that already matches the 70s (if measured as it was in the 70s), and in the 70s when inflation hit the same level where it is today, the Fed had to intentionally raise interest to extremely high levels for a few years to stop inflation.

That means it is now going to be really hard for the Fed to leap back into quantitative easing when stocks and bonds get into trouble because of its taper. The Fed has nowhere to go to lower interest rates if things get bad because its interest target is already on the floor. More importantly, the market is going to take interest higher on its own.

As the Fed tapers, bond interest will rise. I laid out in my last Patron Post why that is assured this time when it wasn’t always so evident during other periods tapering or tightening. That assurance is inflation, which will force the Fed to hold the new course it has set. I pointed out a critical blind spot that most investors and analysts and economists all have right now. Almost no one is talking about it; but, once it’s pointed out to you, it’s so simple it is almost undeniable and inevitable. It is a regime change, and you can read about it at that post. Even then you may miss it because it is such a simple and obvious fact that it is hard for people to grasp that it will be such a game changer.

When bond interest does take off for the reason that article gives, so the bond vigilantes are freed from their own bondage to finally price in inflation, yields have a lot of rapid catching up to do. We all know that a lot of the upward momentum in stocks and the choice to defy risk and ignore overvalued prices has been driven by a search for yield. That is to say, TINA (There is Nothing Else) is a significant driver to the sentiment that is out there. With interest rates low, investors have moved to take higher risk, but bond interest rates are now deeply negative in real terms, which really pushes the reach for yield and willingness to risk.

Consider the following:

Today, it’s the turn of one of our other favorite sellsider analysts, BofA CIO Michael Hartnett to grab the negative real rates torch, and write in his latest Flow Show that while the deeply negative real rates may be just what stock market bulls ordered, 10-year real rates are now at -4.6%, “a level which in the past 200 years that has been associated with panics, inflations, wars & depression, and a level today increasingly responsible for froth in crypto, commodities, and US stocks.”

Zero Hedge

We are, in other words, running our economy on the kind of high-octane monetary stimulus (low-interest rocket fuel) that is only applied in the worst of times, and times are about to get worse still because interest is rising quickly now and will be forcing interest up in an economy saturated again in debt. Bonds will be pricing in inflation. They haven’t been, but they are about to for that one simple reason I’ve given.

This move back to bond reality is one of the main mechanisms by which inflation will clobber the stock market as I’ve predicted. Once bonds are freed from the Fed’s grip so they can start pricing inflation in, we’ll switch from wildly negative real rates (negative net yield after inflation) to neutral or positive real rates, which means highly positive nominal rates in this high-inflation environment where a nominal interest rate of 6% is 0% in real terms.

As the Fed relinquishes its death grip on bond interest, the pressure to reach for yield via stocks — already at high-risk nosebleed prices in terms of what companies need to keep making in this badly cracked economy to justify those prices — will go away as bonds start pay out solid interest for those who plan to simply buy and hold to maturity bonds of short-to-mid-duration. (For bond funds, it’s all very bad news, as they make a lot of their money by speculatively buying and selling bonds — not just clipping interest coupons — and their existing bonds won’t be worth as much when new issuances are paying much more. That means they automatically have to lower their prices/values to compensate. However, if you are just going to buy bonds and clip coupons until maturity, higher yields are coming, and they are a safe haven for those who simply want to buy and hold for security. At least, they will be seen as such when their yields get high enough.)

Yes, it’s true the Fed cannot allow that because the government cannot afford it, but the Fed cannot easily reverse course on tapering it has already begun either as it did on tightening back in 2018. Why? Back in 2018, there was almost no inflation! Today, inflation is burning up the Fed’s backside. If it does back away from its tapering schedule (meaning go back to more easing or, at least, holding its QE at a high level) because markets start to falter, it drives inflation even higher.

This is going to be a phenomenal mess even if COVID doesn’t go into a fourth surge during the holidays (as is already happening in Europe and happened in the last holiday season in the US) and even if vaccines don’t see diminishing returns (as they already have) because interest cannot rise higher with so much government debt on the books and so much personal and corporate debt (where even junk bonds are priced with negative real yields) and where corporate buybacks that have been the main driver for stocks have often been funded by low-interest loans. While interest cannot rise without rapidly creating a debt crisis, Inflation cannot rise without being hugely damaging to the economy. That’s the trap the Fed has set for itself by its two decades of loose monetary policy.

That means the Fed can either 1) start moving down the path toward hyperinflation, if it wants to save markets, by going back to quantitative easing during a time of extreme and enduring shortages when inflation is already equal to its highest points in US history, or it can 2) crash all the market asset bubbles it has fueled. Both go completely against its grain, but those are its choices. It must either create a debt crisis or fuel an inflation crisis — a problem its years of profligacy and central-planning control have created for itself because of the codependency the Fed has built into all markets — particularly stocks, bonds and housing.

I don’t know if the Fed will retreat from tapering ,as many are sure it will (taking us back to negative real yields) to stop the carnage that happens to stocks and to bond funds when bonds are freed to price in current and future inflation, but I know that inflation will either lock the Fed into its tapering choice, or inflation, itself, will become the calamity. Inflation is not, in other words going to back down in time to save the Fed or the economy from the Fed’s conundrum.

So, we wind up with either a global debt crisis due to the level yields will naturally to rise to just to compensate for inflation (if the Fed does not forcibly suppress them by buying more bonds), or the Fed keeps fueling inflation’s fire with QE to higher flames until the economy stagnates under inflation’s sweltering heat and sentiment in all markets crashes in the face of the worst stagflation we’ve ever experienced. It will become, in that case, worse than the seventies because we are already at the seventies level and there are many factors causing inflation besides the current oil/energy crisis, which is already comparable in global scale to the 70s, even if for different reasons. We’re there!

Considerable pressure is already on at the Fed

So much inflationary pressure is on the Fed that, having just announced its tapering schedule, some high players at the Fed are already saying it should consider picking up the pace.

Fed Vice Chair Richard Clarida said it may be appropriate for policy makers to discuss next month whether to speed up the tapering of bond buying after inflation surged and job gains picked up.

The mere talk of that sent two-year yields on US treasuries soaring on Friday, indicating the bond market is a sleeping giant that can be roused. Wait until the Fed’s tether on interest breaks when we get seriously into its tapering regime.

Someone will certainly ask in response to my claims,

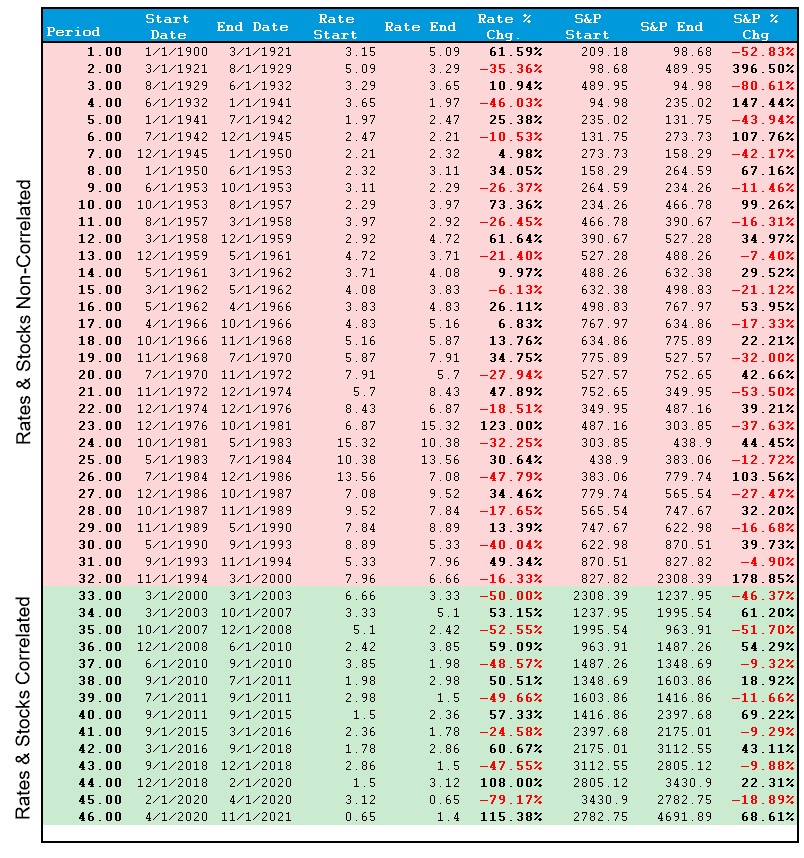

Do rising interest rates matter to the stock market? Many in the financial media and advisory community are scrambling to locate periods where rates rose along with stocks. Has it happened? Absolutely. However, it was only a function of timing until it mattered.

Actually, more a matter of the period of timing. If you go back in history, you find that prior to 2000 (this is key), when the Fed began attempting to seriously manipulate markets in order to save them from damage caused by their own greed, stocks and treasury bond interest usually moved in the opposite direction from each other. It is only after 2000 that stocks and treasury interest suddenly and reliably moved together in the same direction every time: (Meaning the present millennium is the anomaly.)

What changed? The Greenspan-put is what changed. It developed into the new market psychology when the Fed started bailing out savings-and-loans banking, then Long-Term Capital Management and then lowering interest rates down to basement levels to help the stock market out of the dot-com bust. Since then, the Fed has used bailouts, abnormally low interest rates and QE to fuel bull markets by removing risk. Now the Fed is relinquishing that control, and it is forced to do so; but nobody seems to recognize how significant that regime change will be because it is a forced change — forced by very high inflation — at a time of total market dependancy. The Fed has become the air we breathe. Markets simply expect it will be there.

Since 2000, investors have become trained like Pavlov’s dogs to recognize the ring of the bell and salivate whenever bad news meant the Fed would be leaping in with a rescue package in some form of free or easy money, but leaping in was easy for the Fed back in the days when the Fed couldn’t MAKE inflation rise to save its sorry soul. What about now when inflation is skyrocketing and the Fed (see the opening statement to this subsection) is feeling pressured to push inflation down? The Fed is now in a completely reversed environment, and I don’t think it has any idea how to navigate in an environment like this because it has never faced high inflation in an economy where markets are so dependent on its actions due to years of being there for the market as Father Fed, bailing the kid out of jail every time he goes there:

As investors became trained that monetary policy would push asset prices higher, investors sold bonds (risk-off) to buy stocks (risk-on.)

That environment of Fed dependency is altogether different than the seventies! Just keep in mind, it was easy to lower interest or to engage in quantitative easing when the Fed could’t even keep inflation up to its 2% target. Now, even by its own pathetically re-engineered inflation measures, inflation is running three times hotter than the Fed’s target, so it must act. It is acting, and it’s now talking about acting even faster, just one month past its decision to act.

Consider also the market’s mantra throughout the recent stock-and-bond glory years. “Don’t fight the Fed.” Well, the Fed is starting to reduce its stimulus now, so are you going to fight the Fed now that the Fed’s plan is to back off from fueling markets, or does what goes up with the Fed go down with the Fed?

Even the reduction of QE is not the main concern. The rise in bond interest as the Fed relinquishes control of bonds is the main concern; but, still, do you want to fight the Fed as an investor when the Fed is walking away from the table? We have reached the point I’ve been forecasting when inflation is so hot it is forcing the Fed to taper and then almost immediately to consider tapering faster. So, the realization that the Greenspan put is over will dawn on all markets; and, for the simple reason given in that Patron Post I mentioned, bonds WILL start to price in inflation.

Here is another catch to the interest-rate correlation with stocks:

In EVERY period where rates and stocks both rose, most of those gains got forfeited as interest rates slowed economic growth, reduced earnings, or created some crisis.

In other words, there was a lag, but the resultant economic slowdown did impact stocks. The Fed’s action affect stocks by creating a climate, but that climate change doesn’t happen in a day.

In the short term, the economy and the markets (due to the current momentum) can DEFY the laws of financial gravity as interest rates rise. However, as interest rates increase, they act as a “brake” on economic activity. Such is because higher rates NEGATIVELY impact a highly levered economy.

This is what I’ve been saying, and our economy is the most highly levered everywhere it has ever been. I said there would be a lag between inflation and the Fed’s response to it, and there was because the Fed was loath to raise rates. There will also be a lag between the Fed’s moves to raise interest and the market’s response, but I don’t think we’re even going to make it to where the Fed intentionally raises interest because the bond market will do that job for the Fed once the Fed relinquishes control in the very simple way I laid out in that post as being inevitable from the Fed’s taper. In other words, mere tapering of Fed QE will raise interest.

Correlation cuts both ways. When rising rates reduce earnings, economic growth, and investor sentiment, the “risk-off” trade (bonds) is where money will flow.

Sentiment does move markets, but reality moves sentiment. When the economy is falling so that earnings are dropping and bond interest is rising, stocks stop looking as interesting as they did when assured Fed stimulus and low interest were driving the economy up or were, in the very least, creating lots of money that had to get stored somewhere other than just in bank reserves, while inflation was lying low so doing nothing to eat away at earnings (producer cost inflation eating margins as well as consumer price inflation decreasing consumer demand).

We have just entered an environment that is entirely different from all of that (which we grew accustomed to as the norm over the last twenty years) because there is a level at which inflation can largely be ignored, and level at which it cannot, and we have reached that level I’ve predicted where inflation won’t be ignored any longer. The Fed has told us that. Yet, the rapidly declining economy remains dependent on Fed support, as do markets.

There comes a tipping point when interest rates do matter

It is hard to say exactly what that tipping point is, but it never gets ignored forever, though there is typically a lag, especially when sentiment is hot and heavy and wants to keep plowing upward in pure greed. In the present environment that has been coaxed into low-rate addiction by the market’s drug pusher (the Fed), I’m sure the tipping point will show up as a pretty low bar once bond interest starts rising on its own, as it soon will. Investors have only to internalize the fact that the Fed is not there for them anymore, rates are rising on their own, and there isn’t anything the Fed can do about it because Fed-fueled inflation has now lit the back of the Fed’s pants on fire, so it’s running from the flames it has helped create.

The Fed said inflation was transitory because it had to. It knows it cannot fight inflation without damaging the dependent markets (asset bubbles) it has built. I’m sure Fed officials desperately wanted to believe inflation was transitory, so “group think” enabled them to reassure each other that it was, in fact, going to be transitory.

After all, this little coven of banksters couldn’t make inflation rise for years when they wanted to even when they did more than they had ever done to make it happen. So, the Fed reasoned, if the shortages went away, inflation would surely end on its own. They weren’t just feeding the transitory narrative to the public. They desperately wanted it to prove true and hoped it would.

Now, however, they have clearly realized it will not prove true, so they have started to taper QE because they know they have to respond to inflation because they are its fuel. The shortages due to global damage from all the COVID lockdowns, as I’ve said for over a year, are not going away and will not go away quickly enough to help the Fed avoid the fight.

The fight is on!

In my next Patron Post I’ll be laying out just how precarious and historically over the top the present market is by numerous measures — more of an indication of how hard it can crash when it does come down than of when the tipping point will be reached; but be assured we don’t have far to go to hit that ambiguous point of no return.

*********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.

More from Gold-Eagle