Hyperinflation Is Here

Definition: Hyperinflation is the condition whereby monetary authorities accelerate the expansion of the quantity of money to the point where it proves impossible for them to regain control.

It ends when the state’s fiat currency is finally worthless. It is an evolving crisis, not just a climactic event.

Summary

This article defines hyperinflation in simple terms, making it clear that most, if not all governments have already committed their unbacked currencies to destruction by hyperinflation. The evidence is now becoming plain to see.

The phenomenon is driven by the excess of government spending over tax receipts, which has already spiralled out of control in the US and elsewhere. The first round of the coronavirus has only served to make the problem more obvious to those who had already understood that the expansionary phase of the bank credit cycle was coming to an end, and by combining with the economic consequences of the trade tariff war between China and America we are condemned to a repeat of the conditions that led to the Wall Street crash of 1929—32.

For economic historians these should be statements of the obvious. The fact is that the tax base, which is quantified by GDP, when measured by the true rate of the dollar’s loss of purchasing power and confirmed by the accelerated rate of increase in broad money over the last ten years has been declining sharply in real terms while government spending commitments continue to rise.

In this article it is documented for the dollar, but the same hyperinflationary dynamics affect nearly all other fiat currencies.

Introduction

In the last ten years I have waged two crusades to bring attention to issues I believe to be in the public interest. From 2011, I wrote a series of articles about China’s gold policy, which had been accumulating physical gold from as long ago as 1983. The meme that gold was moving from west to east became broadly understood and almost a cliché. The second crusade was to inform the public that the business or trade cycle was only the symptom of a cycle of bank credit, which inevitably ends in a crisis of credit contraction.

It is now time for a new campaign, on a subject which I have been writing about in recent months, and that is to inform the wider public that their governments and their fiat currencies are now in a state of hyperinflation. It is not a development on the far horizon as many might think; it is already here.

What is hyperinflation?

To understand why hyperinflation is already with us is to know what constitutes hyperinflation. It is not rising prices, or a condition that exists when prices increase above a predetermined rate: rising prices are the consequence of both inflation and hyperinflation. As Milton Friedman put it, inflation is always and everywhere a monetary phenomenon, though he spoiled it by continuing, “…in the sense it is and can be produced only by a more rapid increase in the quantity of money than in output.” He was wrong on that last bit, conflating the price effect with the increase in the quantity of money. When even so-called monetarists are imprecise about inflation, let alone hyperinflation, it is hardly surprising public confusion is widespread.

There can only be one definition of hyperinflation, and that is the one headlined above, which you won’t find in any textbook. There is even no definition of it in von Mises’s Human Action, only of inflation, and that is more a description than a definition. And since it is a relatively recent phenomenon of unbacked fiat currencies, hyperinflation was never defined separately from inflation by classical economists. The difference between inflation and hyperinflation cannot be distinguished by degree either.

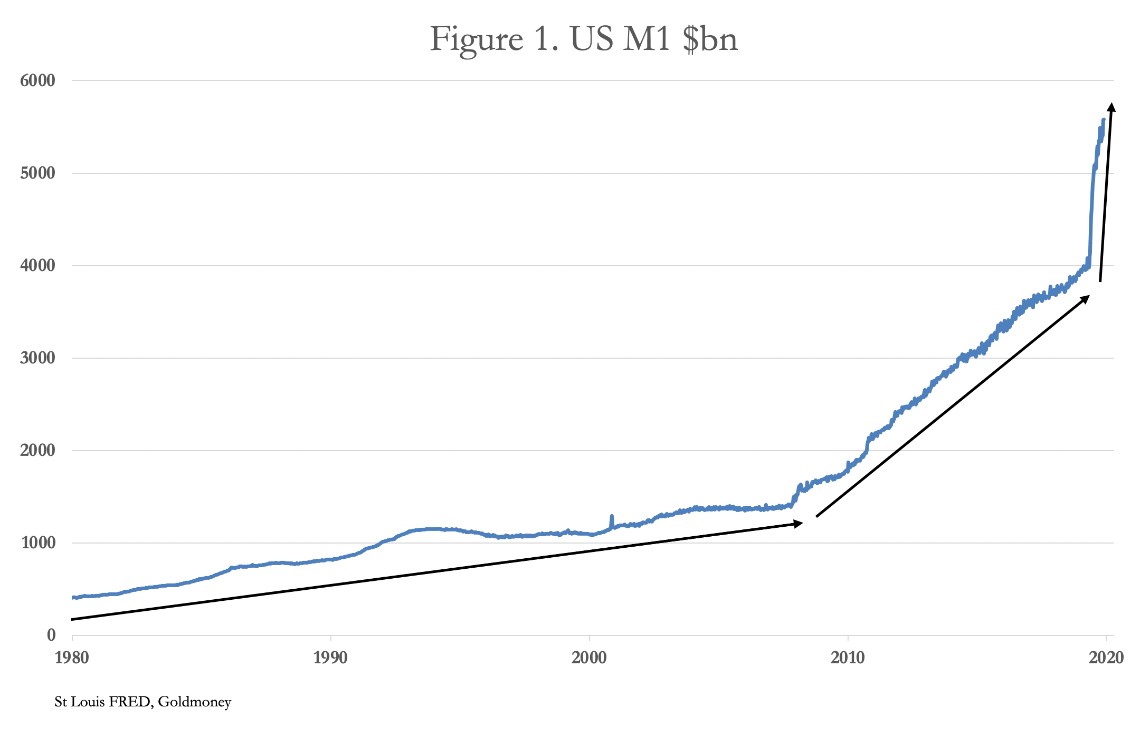

Have a look at US M1, the quantity of narrow money in the American economy, shown in Figure 1.

The progression of annualised monetary inflation from under 6% before the Lehman crisis, to 9.6% subsequently until March this year, and 65% in the thirty weeks since is clear from the chart. If the monetary authorities have the knowledge, the mandate, the authority, the ability and the desire to stop inflating the currency, we would not describe it as hyperinflation, instead deeming it to be no more than a brief period of exceptional inflation before a return to sound money policies.

But sound money was emphatically discarded in 1971, when the post-war Bretton Woods agreement was finally abandoned — not that the monetary regime at that time was in any way sounder than Adam’s fig leaf was an item of clothing. For the fact of the matter is that sound money in America was arguably abandoned long ago, with the founding of the Fed at Jekyll Island before the First World War.

As a means of funding government deficits, inflation is capable of being stopped by cutting government spending and/or raising taxes. But now, a one-off increase of 65% of narrow money is to be followed by another massive expansion already in the wings. The hope is that that will be enough, just as the original 65% increase in M1 was hoped to be enough to ensure a V-shaped recession would be followed by a return to normality.

The early stages of a hyperinflation are always seen by the monetary authorities as the only policy to pursue. They convince themselves that there are either no consequences, or that they can be controlled. An example of the genre is found in a paper by Michael T Kiley, a senior Fed economist. In August he concluded that the lack of further room to cut interest rates to deal with the coronavirus requires quantitative easing to a total of 30% of GDP, or $6.5 trillion, to offset the lack of room for manoeuvre on interest rates. Kiley writes that about $3 trillion had been enacted between end-February and end-June, leaving a further $3.5 trillion to come. If we assume the full $6.5 trillion stimulus is enacted by next February, then the increase reflected in narrow money could be to more than double it.

Kiley wrote his paper before the second coronavirus wave commenced. He was modelling an economic contraction measured in real GDP of just 10% in the second quarter (actually 9.5% — not to be confused with the annualised rate reported at 32.9%). But, as I pointed out in last week’s article, with monetary inflation running at such a rate, a dollar last February is not the same as an inflated dollar next February, being diluted on Kiley’s figures by $6.5 trillion. The consequence is some extremely damaging intertemporal shifts, as described in the Cantillon effect, whereby ultimately both productive workers and the poorest in society lose savings, salaries and social security benefits through loss of the dollar’s purchasing power for the benefit of the government, its agencies, and big business.

In his economic model, Kiley flattens the Phillips curve, apparently in an attempt to goal-seek a preferred outcome. The Phillips curve is meant to replicate graphically the relationship between inflation and unemployment, the idea being that an increase in price inflation goes along with a reduction in unemployment. Flattening it is the same as assuming that at a deemed level of full employment prices will not rise as much as previously modelled. But it is one thing to forecast such a relationship when the inflation “stimulus” is in the order of a few per cent, when arguably the public is more aware of the stimulation effect of monetary inflation than they are of the dilutionary effect on the money, but it is another matter when it is as dramatic as it is today.

We must resist the temptation to accept a mathematical relationship between prices of goods and services and the rate of employment, such as predicted by the Phillip’s curve. Whatever the level of employment, production adjusts because of the division of labour. In their dismissal of Say’s law, modern economists fail to realise that production and consumption broadly march or retreat together. Other than users of currency being temporarily conned by the initial effects of monetary stimulation, there is no enduring relationship between the quantity of money and employment.

Errors introduced by the mathematical economists through artifices such as the Phillips curve conceal the consequences of policies based on their forecasts at the outset. Consequently, the recommendations of senior economists at the Fed using economic models based upon macroeconomic assumptions give false comfort to the committees they advise. Furthermore, the annualised rate of the budget deficit since March was about $4.4 trillion, financed entirely through monetary expansion and significantly greater than covered by declining tax income.

If these conditions persist in the new fiscal year — which seems increasingly certain, Kiley’s calculation of the further $3.5 trillion stimulus underestimates the problem. According to an op-ed by Allister Heath in today’s Daily Telegraph, Larry Summers, the US economist and arch-inflationist, believes that the cost of covid-19 will reach 90% of US GDP, substantially more than Kiley’s estimate of 30%. Over-dramatic perhaps; but can we envisage that the forthcoming stimulus package, and then undoubtedly the one to follow that, will restore normality and set the budget deficit firmly in the direction towards a balance? If the answer is no, then we already have hyperinflation.

Dispensing with the assumptions of mathematical economists

The error of the Phillips curve was to not understand why there is a point in the course of inflation where the currency’s users suspect that prices will continue to rise, and that a shift away from personal liquidity and saving in favour of consumer spending ensues. That it is bound to happen beyond a certain point does not mean that the point and the subsequent effect on the general level of prices can be predicted — that is down to human action, the unpredictable response of individual actors to their changing circumstances.

The Phillips curve is not the only error when it comes to understanding the effects of monetary inflation. Finding that the relationship between the expansion of money and the effect on its purchasing power varied, the mathematical economists introduced a variable factor to ensure the equation describing the money relationship with prices always balanced. The monetary equation is as follows:

But by introducing a variable factor V to ensure the equation always balances, it disqualifies the utility of the equation itself: anything with two unequal sides can be turned into an equation by this artifice. The imagination of the monetarists brushes over this truth by giving the variable a pejorative name. By calling it “velocity of money” it creates an image of the circulation of money. From there it is easy to assume that if money is underused, velocity of circulation drops and the economy is declared to stagnate, and if its velocity of circulation increases, it is said to be because money is demanded and circulates more effectively. Falling velocity is thereby associated with falling prices for which nominal GDP is the proxy (P x T in the equation), and rising velocity is associated with rising prices and rising GDP. This concept is badly flawed, but it explains the fundamental precepts behind current monetary policy.

The consequences of changes in relative preferences

Nominal GDP is not just the other side of the monetary equation. It is also total production, and the other side of total production is the sum of consumption and deferred consumption. The correct way to regard money is not through the monetary equation and the supposed role of velocity, but to look at nominal GDP as both the total of everyone’s income and profits, and the sum of their expenditures and net savings. Only then can we consider the impact of changes in the money quantity on prices.

Money is merely a form of intermediation between the production and consumption of goods. People hold a degree of personal monetary liquidity, which when money is stable does not vary by much overall. This liquidity must not be confused with savings, which being consumption deferred, are not primarily held for their liquidity but for anticipated returns. Personal liquidity is held in reserve for personal consumption.

The general level of personal liquidity is the result of recent experiences of the value of money in terms of goods, modified by expectations of any change in the relative value of future goods. Thus, if people think the price of a good might rise, they will tend to buy it sooner than they would otherwise, and if they expect it to fall, they will tend to delay their purchase of it. In generally stable monetary conditions, this is why some prices rise and others fall.

The trouble comes if for whatever reason people as a whole anticipate a rise in the general level of prices. In that case, they will alter the relationship between their monetary liquidity and goods in favour of goods more generally, driving the purchasing power of the money down and the general level of prices up.

The effect of changes in the general level of personal liquidity is potentially a more important influence on the level of prices than the quantity of money itself. It should be evident that if the increased quantity of money in circulation is simply hoarded, there will be no effect on the general level of prices. Alternatively, if the public decides to abandon a state-issued currency, irrespective of the quantity in circulation it will lose all of its purchasing power.

The abandonment of a state-issued currency by the public terminates all hyperinflations and once the process is under way it tends to be rapid. In Weimar Germany, it was said this flight into goods and out of money began in May 1923 and lasted to mid-November. In the other European nations, which suffered collapses of their currencies in the early 1920s, the final process was equally swift.

The form of today’s monetary collapse

The first thing to consider is the current relationship of the quantity of money to the economy. US dollar M3 money supply, the broadest definition of money, has increased along with US GDP: M3 stood at $18.327 trillion last July, while second quarter GDP was estimated at $19.52 trillion. The closeness of the relationship between these two figures is explained by the nominal GDP total being inflated by increases in the money quantity. The match is never perfect, because there is always some consumer expenditure which is subject to estimates, future revisions, or simply not captured by GDP. To these we can add statistical error. Furthermore, at the beginning of the inflation there would have been a base level for GDP when money was sound from which subsequent inflations occurred.

The degree of the dollar’s loss of purchasing power is deliberately understated in official statistics. Originally, the policy was to reduce the cost to US and other governments of indexation introduced following the 1970s decade of price inflation. It is remarkable that the statistical suppression of changes in the general level of prices, now adopted in all advanced economies, is rarely questioned. Consequently, the scale of the fall in the purchasing power of fiat currencies has been ignored with some important consequences, at least for governments and their central banks, which are concealing evidence of the failures of monetary and economic policies.

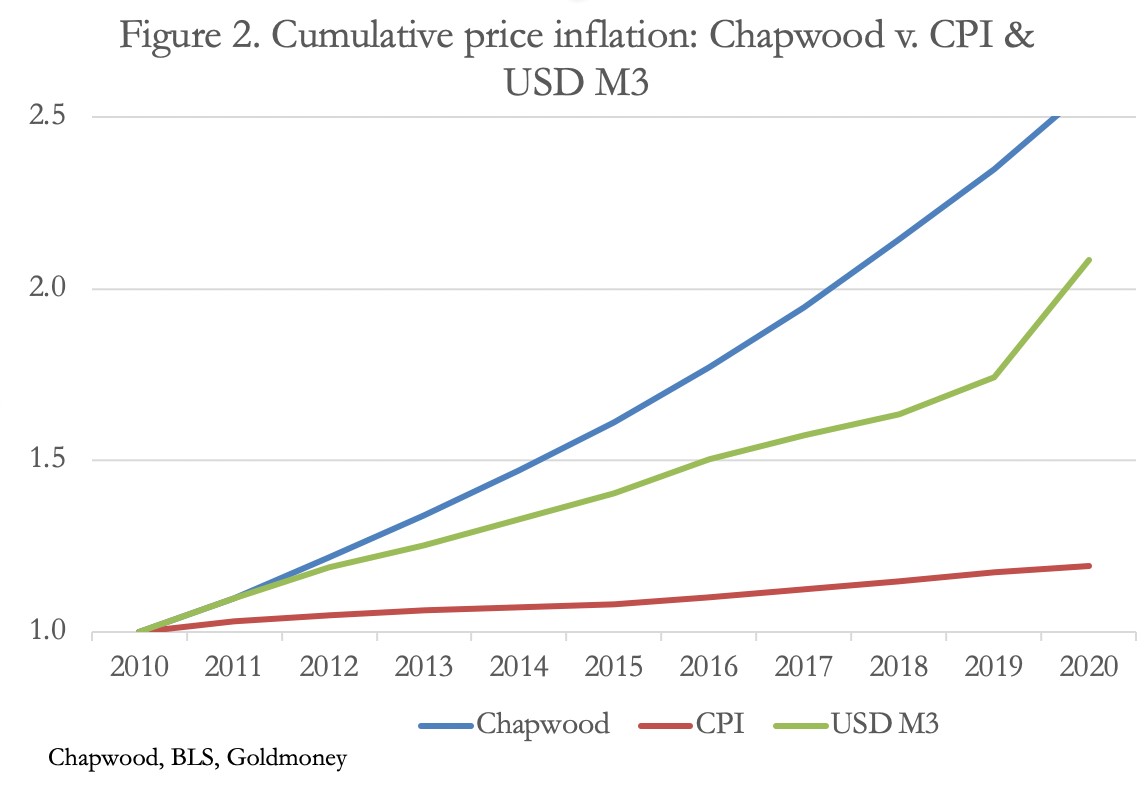

Figure 2 compares the cumulative increase in the general level of prices measured by the CPI, and the Chapwood index — comprised of “the top 500 items on which Americans spend their after-tax dollars in the 50 largest cities in the nation”. The Chapwood price inflation numbers used in the chart are the arithmetic average of the fifty cities, the last data points being end-June 2020. Additionally, the growth of M3 money supply is included.

It should be clear that changes in the general level of prices are a theoretical concept which cannot be measured, because it is different for every individual. An average is therefore no more than an indication, even assuming the evidence is not manipulated by vested interests. Bearing this in mind, the cumulative price effect of the official cities’ CPI over the last ten years is for it to have risen by only 19%, compared with the Chapwood index which rose 159%, compounding by about 10% annually. By way of confirmation that the Chapwood figures are closer to the truth, we see that USD M3 diluted the dollar by increasing 109% over the period.

The lower increase in USD M3 relative to that of the Chapwood index suggests that as well as the dilution of the dollar’s spending power in a general sense, holdings of money have also been reduced relative to the commonly bought goods in the Chapwood index. In other words, consumers appear to show a relative preference in their spending for their common purchases over their less common purchases. This could be taken to be evidence of the earliest stages of a reduction of money balances in favour of everyday purchases. It is inconsistent with the official story upon which monetary policy is based, whereby the monetary authorities and their epigones delude themselves that price inflation is contained by the two per cent annual target, with some of them even claiming price inflation is banished for ever.

Figure 3 further illustrates the ineffectiveness of monetary policy by expressing GDP in 2010 prices adjusted by the CPI (the state’s version of real GDP), by the Chapwood index and finally by M3 money supply.

The monetary authorities claim that before the coronavirus crisis they had stabilised the US economy following the Lehman crisis. Measured by the CPI, by end-2019 the economy had grown by nearly 22% over nine years “in real terms”. But because the CPI is a heavily supressed measure of price inflation, the truth is different. The Chapwood index and USD M3 tell us that adjusted by these measures, GDP has more than halved from $15,241bn to $6,818 and $7,309bn respectively, measured by a base of 2010 dollars.

To be clear, GDP is simply a money total of all recorded transactions. It does not tell us anything about their quality, or indicate the degree of economic progress, or the lack of it. As always, there have been winners and losers. We can only conclude in the most general of terms that the contraction of real values has exposed the failure of monetary and economic policies.

Where it really matters is for governments, and the purchasing power of the taxes they collect.

A modern socialising government never reduces its expenditure, and budget deficits arise as a result of a reluctance to increase taxes to match spending. Prima facie it is evidence of an emerging hyperinflation, in that the decline in the purchasing power of the currency is driving the fall in the real value of taxation receipts, while at the same time it is realised that to raise taxes would be harmful to production, consumption, and therefore government finances.

Then came the coronavirus, an unexpected hit to nominal GDP, upon which government tax income depends. And now we have a second covid-19 wave, the economic consequences of which can only be guessed. Let us not forget that before all this happened, last September there was an emerging liquidity crisis evidenced by the failure in the dollar repo market, indicating, in all likelihood, the end of bank credit expansion. And we should also remember that the trade tariff war between the world’s two largest economies brought the growth of international trade to a sudden halt.

Anyone with an eye for the economic consequences of all these developments can only conclude that in addition to the already growing gap between government spending and tax receipts, governments are not just having to rescue their tax bases from a one or two-off hit from the coronavirus, but further rounds of inflationary expansions will follow at an increasing pace. Purely in terms of money quantities, hyperinflation is already well entrenched for the US dollar and all other fiat currencies subject to the same political and factual dynamics.

When the public wakes up…

Very few are conscious that hyperinflation is already with us, the majority of people only becoming aware when the consequences for prices become obvious. And as noted above, it is not a linear process, where

M x V = P x T.

V, or velocity, must be replaced by the human factor, where preferences change between holding a reserve of money liquidity and buying goods. The final flight into goods is a rapid process, which once started is impossible to stop. We have seen that the relationship between the rise in prices, as measured by the Chapwood index and the increase in dollar M3, suggests that the earliest stages of preferences for holding money are decreasing in favour of commonly bought goods: the process appears to have been subtly under way for a number of years.

Sceptics of the hyperinflation hypothesis might argue that the US Treasury owns over 8,000 tonnes of gold and could stop the rot at any time by returning to a gold standard. One would hope so, but there is no sign that anyone in charge has the faintest clue of the true situation. Furthermore, having discarded gold as backing for the dollar forty-nine years ago it is inconceivable that the Fed and the Treasury would willingly put the clock back. Furthermore, if I am right that the Chinese state not only controls physical gold markets but has a substantial cache of undeclared bullion, reinstating gold’s monetary role would be seen to hand enormous power to America’s enemies. Besides, so long as there is any value left in the dollar foreigners are likely to swap them for gold at the US Treasury.

And that is before the neo-Keynesian macroeconomists submit themselves for retraining, expunging themselves of all their fallacies. No, the rotten ship USS Dollar is more likely to sink with the loss of all hands.

Meanwhile, the Fed announced unlimited monetary inflation on 23 March. Shortly after, China began to accelerate sales of dollars in favour of stockpiling commodities, exhibiting the change in behaviour we can expect from the wider American public when it collectively realises it is money going down and not the prices of everything rising. Did 23 March, following which China is reported to have started dumping dollars at an increased pace for commodities, mark the beginning of the final flight into goods?

It is certainly possible, in which case hyperinflation of the dollar and of most other paper currencies will likely end in a final, unexpected collapse in purchasing power in a matter of only a few months.

Alasdair Macleod

HEAD OF RESEARCH• GOLDMONEY

Twitter: @MacleodFinance

MOBILE: +44 7790 419403

Goldmoney

The Most Trusted Name in Precious Metals tm

NEW YORK | ST. HELIER | TORONTO

Publicly Traded Symbols: CA: XAU | US: XAUMF

© 2020 GOLDMONEY INC. ALL RIGHTS RESERVED. THIS MESSAGE MAY CONTAIN CONFIDENTIAL OR PRIVILEGED INFORMATION. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE ADVISE US IMMEDIATELY. THIS MESSAGE IS FOR GENERAL INFORMATION ONLY AND SHOULD NOT BE CONSTRUED AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY SECURITIES OR ANY OTHER FINANCIAL INSTRUMENTS. WE DO NOT PROVIDE TAX, ACCOUNTING, OR LEGAL ADVICE, AND RECOMMEND THAT YOU SEEK INDEPENDENT PROFESSIONAL ADVICE IF NECESSARY. WE CONSIDER INFORMATION IN THIS MESSAGE RELIABLE BUT WE DO NOT REPRESENT THAT IT IS ACCURATE, COMPLETE, AND/OR UP TO DATE AND IT SHOULD NOT BE RELIED ON AS SUCH. OPINIONS EXPRESSED ARE OUR CURRENT OPINIONS AS OF THE DATE APPEARING ON THIS MESSAGE ONLY AND ONLY REPRESENT THE VIEWS OF THE AUTHOR AND NOT THOSE OF GOLDMONEY INC OR ITS SUBSIDIARIES UNLESS OTHERWISE EXPRESSLY NOTED.

Notice: This email may contain confidential or privileged information. If you received this email in error or believe you are not the intended recipient, please notify the sender immediately and delete this email without forwarding or opening any attachments. Thank you for your cooperation and attention.

*********