Inflation Is Just Getting Started – Got Gold? Got Silver?

A portion of the commentary below is from the latest issue of the Mining Stock Journal. Recent trading action in gold, silver and the mining stocks lead me to believe that a major move in the precious metals sector may have started. You can learn more about my newsletter by following this link: Mining Stock Journal information

The nature of inflation is widely misunderstood and misinterpreted. “Inflation” and “currency devaluation” are tautological – they are two phrases that mean the same thing. When the money supply increases at rate that is greater than the wealth output of an economic system, it reduces the value of each marginal dollar created (for the pedants, I’m not going to delve into the difference between bank reserve creation and money supply – the two are inextricably linked). Dollar devaluation has been occurring since the early 1970’s. The value of the dollar relative to gold (real money) has declined 98%. In 1971 $40,000 would buy a 4,000 square foot home in a good suburb. Now it takes $700,000 on average to buy that same home.

Price inflation is the evidence of currency devaluation. The CPI is not a real measure of price inflation. The CPI is methodically massaged – starting with the Arthur Burns Federal Reserve (it was his idea) – to hide the real degree of currency devaluation from all of the money that has been printed since 1971. The CPI report is little more than a tool for political propaganda. In addition, the Fed has made the public’s ability to measure the money supply considerably more difficult over the past 15 years. In 2006 the Bernanke Fed stopped reporting M3, the most accurate measure of the money supply. You can’t see M3 past March 2006. Why? Early in 2021, the Fed changed definitions of M1 and M2. Why? The Fed has done this to disguise the true amount of money supply that has been created over time.

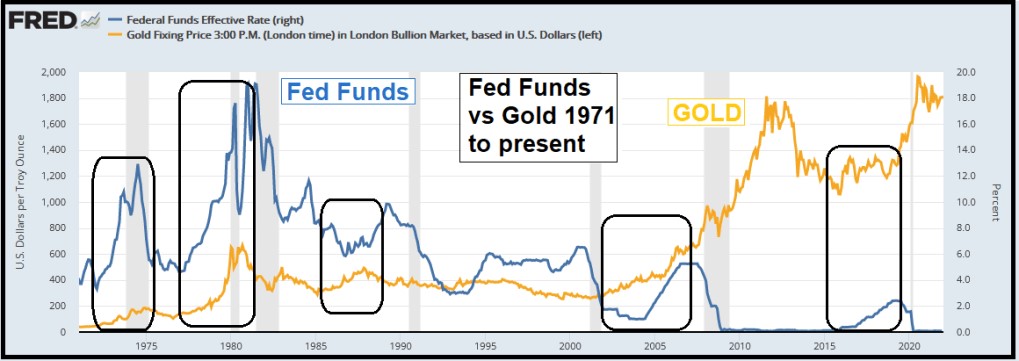

The M2 money supply has increased at annualized rate of 20.2% Since February 2020. The M2 measurement is now 90% of GDP vs 44.4% at the beginning of 2000. Going into 2022, gold is considerably mispriced relative to the amount of currency that has been printed. And silver, at a gold/silver ratio of 79, is extraordinarily mispriced vs gold. Now that the Fed seems intent on tightening its monetary policy per the FOMC meeting minutes released last week, what happens to the price of gold when the Fed begins a rate hike cycle? I’ve mentioned this is the past, but Adam Hamilton, who publishes his Zeal Intelligence newsletter, did a statistical study which concluded that some of gold’s best rate of return periods going back to 1971 have occurred when the Fed goes into a rate hike cycle. The chart I prepared shows this:

Contrary to the mainstream narrative – seeded in ignorance, I might add – that gold moves inversely with interest rates, in the modern fiat monetary system gold rises when the Fed hikes the Fed funds rate. I’m sure you can find Hamilton’s piece using Google to get numerical specifics.

The rationale behind this is that, in every instance, when the Fed finally acknowledges that price inflation is a problem that needs to addressed with tighter monetary policy, flight to safety money moves into gold because the market has determined that the Fed is way behind the inflation curve and the start of a rate hike cycle is the signal to the market that inflation is going to get worse. Furthermore, the Fed will not act quickly enough to get ahead of the problem.

Since the 1990’s, the Fed tends to start an interest rate hike cycle at a time when the economy is already rolling over. Gold’s price rise along with the Fed funds rate is the expectation that the Fed will have to cut its rate hike cycle well short of plan in an effort to re-stimulate the economy. You can see that in the chart above in which each rate hike cycle since the mid-1980’s gets shorter then is abandoned and reversed at a lower Fed funds rate.

To the extent that there’s weakness in the precious metals sector connected to the Fed’s shifting policy stance and the resultant blood bath in the stock market, I expect the weakness to be short-lived and the dynamic reflected in the chart above will kick-in. I also think that a severe economic recession will force the Fed to abandon its tightening stance by mid-2022 and resume its money printing and near-ZIRP monetary policies. This will serve as rocket fuel for the precious metals sector.

********