Inflation Watch: Beware The Ides of March

President Biden has now had his $1.9 trillion stimulus package passed into law, and it will not be the last in the current fiscal year. Covid is not over and is sure to resurge with new variants next winter.

But even assuming that is not the case, we still have to contend with the aftermath of the pre-covid conditions, whereby banks had run out of balance sheet capacity combined with trade tariffs predominantly aimed at China. These conditions were a doppelganger for late-1929, and between 8 February and 20 March the S&P500 index faithfully tracked a similar course to that of October 1929.

As far as possible, this article quantifies inflationary financing of government spending from March to September last, and already sees evidence on the CBO’s own figures of that exceptional covid response being exceeded in the first half of the current fiscal year just ending. It points to something which no one has really foreseen, that the rate of monetary inflation has increased beyond the banking system’s capacity to accommodate it.

Even if the US manages to emerge from lockdowns in the coming months, the legacy of the turn in the credit cycle, trade tariffs and supply chain disruption threatens a full-scale depression. There can be no doubt monetary inflation will accelerate, and we are beginning to see the consequences in rising bond yields.

Introduction

It is nearly a year since the Fed on 23 March 2020 responded to stock market pressures and cut its funds rate to the zero bound and followed that three days later by increasing quantitative easing to $120bn every month. A further $300bn credit was to be directed at businesses, employers and consumers. The Primary Market Corporate Credit Facility and the Secondary Market Corporate Credit Facility allowed the Fed to directly support corporate bond prices for large employers. And the Term Asset-Backed Securities Loan Facility would enable the issuance of asset backed securities financing credit cards, student loans and auto loans. Credit was to be made available to municipalities through two further programmes.

And so on. Officially, the Fed was responding to the coronavirus in its role of ensuring market stability. Its emphasis on supporting businesses that otherwise would lay off employees reflected its mandate to target the highest level of employment consistent with its inflation mandate. Just in case the expansion of money led to a rise in consumer prices, last August the Fed changed the inflation target from 2% to an average of 2%, allowing itself the leeway not to change monetary policy if the target was breached.

Far more importantly, without the March stimulus the S&P500 was collapsing along with other non-fixed interest financial assets and commodity prices. If there is one thing that scares the living daylights out of the Fed, it is deflation. And that was what it suddenly faced.

A crisis in the repo market the previous September had alerted us to the inability of the banking system to further expand bank credit to support economic activity. Initially, investors paid little attention, but by early February 2020 the stock market began a sudden collapse, with the S&P losing 32% by the ides of March. For a central bank which believed in the wealth effect of rising stock prices it was vital to stave off a self-feeding 1929-style collapse in investor confidence. That was the existential threat at that time, and it had followed President Trump’s attempt to repatriate American manufacturing from China by way of imposing import tariffs on Chinese goods.

Essentially, financial and economic conditions were heading for a repeat of the Wall Street crash of 1929 which led into the 1930s depression. At that time, bank credit had expanded in the roaring twenties on top of Benjamin Strong’s monetary expansion, fuelling a stock market bubble of historic proportions. The trigger for its bursting was the Smoot Hawley Tariff Act, which was passed by the Senate in a debate between 23—29 October 1929. In the process, its scope was increased from the narrower damage limiting coverage expected in financial markets to an all-embracing tariff act, which added over 20% to the existing Fordney-McCumber tariffs of 1921.

It was that month that Wall Street crashed, with 24 October dubbed Black Thursday when the Dow lost 11% on the opening bell. The following week saw Black Monday and Black Tuesday as the falls continued.

In late-2019, the proportions of money and credit expansion relative to tariff impositions differed from 1929. The expansion of both money and credit was far larger, having accumulated over several credit cycles which were not permitted to wash out. Smoot-Hawley was global, while today’s trade tariffs were targeted mainly at the second largest economy after the US and so less extensive. However, the combination was arguably at least as dangerous as that of late-1929.

It cannot be emphasised enough not to rely solely on empirical evidence, but from a theoretical stance to consider the economic destruction from tariffs, and then combine that with the cyclical collapse of bank credit. A moment’s thought about the consequences of such a combination and the subsequent mishandling of the consequences explains much of economic history between the early twenties and the run up to the Second World War. And consequently, it behoves us to regard a similar combination in the run up to today’s events equally seriously.

In February—March 2020 the sudden collapse of stock prices was eerily similar to the September—October 1929 crash both in scale and duration. A crucial difference is that in 1929 the stock market bubble was not deliberately inflated by monetary policies, being simply a side-effect of them. Today, the Fed openly admits to an objective of pumping the stock market through QE to create a wealth effect, necessary, in the opinion of policy makers, to retain confidence in the economy.

In 1929 there was an operational gold standard that meant the depression of economic activity led to falling prices. Today currencies are pure fiat, and the agreed policy is to expand their quantities to prevent prices falling. It will not succeed in preventing a repeat depression, only serving to conceal it. A distinction must be made between the failed interventionist policies of both Hoover and Roosevelt, which hampered the markets’ adjustment and reallocation of all forms of capital, and the monetary effect. Under the gold standard there was a true reflection of the economic consequences of that fateful combination of collapsing credit and trade tariffs. Left alone, the depression would have lasted perhaps eighteen months or so, echoing the depression of 1920-21 — forgotten today, but equally deep.

Today’s interventionism is all-embracing with governments assuming that by taking total control through regulation, inflationary financing and suppression of interest rates the modern economic system will never fail. The February—March 2020 market crash challenged that assumption. The further acceleration of inflationary financing and interest rate suppression under the cover of covid lockdowns was the statists’ response. And it is important to understand in that light what happened subsequently and continues today.

The pandemic— March to September 2020

Of course, the massive monetary expansion set off last March was presented to markets and the public as a response to the covid crisis. The Fed was faced with a number of problems. With swathes of production and consumption simply shut down, every advanced nation faced a sudden collapse in economic activity which was turning out to be the largest ever seen. The dangers of the turn of the credit cycle and trade tariffs collapsing the economy and stock markets were quietly forgotten. In their place there arose an assumption, fostered by the authorities, that covid was and still is the only problem and when lockdowns end everything will return to normal. Even though a V-shaped recovery became U-shaped and then L-shaped, it is still insisted that normality will return.

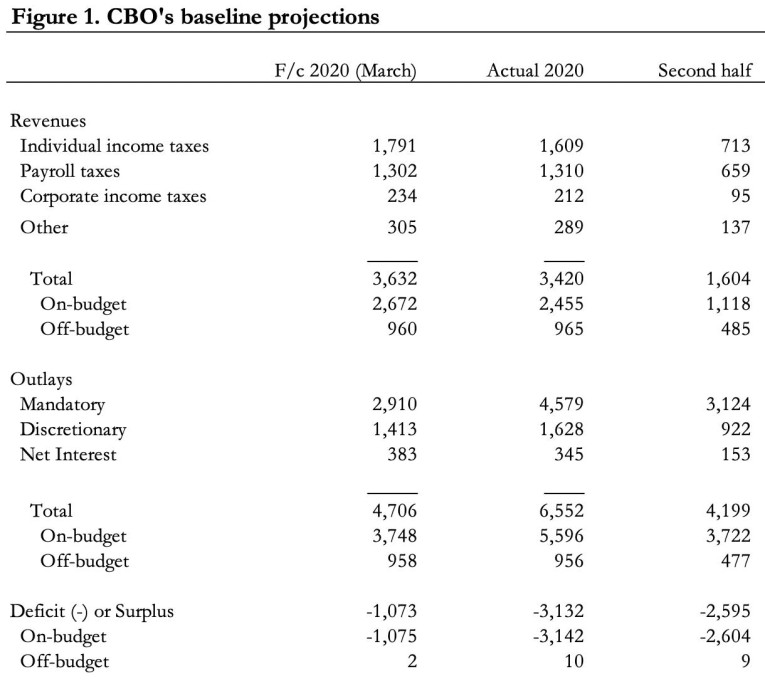

Meanwhile, in common with those of other nations, the US budget deficit simply exploded. By the end of the fiscal year to end-September 2020, it had risen to $3,142bn, representing 48% of total expenditure. But taking the second half from end-March to end-September, the damage is far worse than that concealed in the annual figures. Figure 1 extracts revenues and outlays for the second half by estimating the changes from what was known by March 2020 and the final outcome. Amounts are in billions.

The deficit between March and September at $$2,595bn was 62% greater than the $1,604bn in revenues. Put another way, only 38% of outlays were covered by revenue and the balance was raised in bond markets. To this must be added the change in the Government’s general account at the Fed, which between March and September increased by $1,262bn.

Not all this finance was directly inflationary, because the savings rate jumped during lockdowns. But during the period, the Fed’s holdings of US Treasuries increased by $1,105bn, which can be taken as a proxy for the Fed’s element of inflationary financing of the budget deficit. That leaves $2,752bn, (i.e. the $2,595bn deficit plus $1,262 on the general account less $1,105bn by the Fed) funded from other sources.

We can assume that some of the $2,752bn balance was funded by insurance and pension funds from a combination of cash flows and replacement of investments bought by the Fed through their banks as part of the QE programme. Direct public participation will account for some of the deficit financing, but the balance is bank credit finance. Acknowledging the importance of bank participation, the Fed suspended the Supplementary Leverage Ratio on 1 April for one year, specifically excluding US Treasury securities held on bank balance sheets and their reserve deposits at the Fed. This would create the leeway for the balance sheet expansion necessary to accommodate the financing of the government deficit by the expansion of bank credit as well as by QE targeted at investing institutions.

In its 1 April statement, the Fed acknowledged that liquidity conditions in Treasury markets had deteriorated rapidly, and what with significant inflows of customer deposits, banks were running out of balance sheet capacity. Six months later, bank credit has expanded by $1,250bn, much of which would have to be contracted if the suspension of the supplementary leverage ratio is discontinued as planned at the end of this month.

We can identify two emerging problems. The first is the lack of balance sheet capacity in the banking system, already noted. The second is that in the fiscal year to September, the US Government was absorbing private sector savings in quantity, making them unavailable for genuine economic investment. Instead, economic policy amounts on the one hand to preserving zombie businesses in the name of preserving employment and on the other suppressing economic progress through capital starvation. Something has to yield, and that is almost certain to result in an even higher rate of monetary inflation.

That is the background to the current fiscal year.

The current fiscal year

So far, in the first half of the current fiscal year, two stimulus plans have been passed: the first was a $900bn package passed at end-December, and the second is the just passed Biden $1.9 trillion package. Before the Biden stimulus package, the Congressional Budget Office had updated its full-year forecast to include a budget deficit of $2.258 trillion. Adding in Biden’s package, which the CBO estimate did not include, takes it to over $4 trillion, against last fiscal year’s $3.132 trillion.

Admittedly, Biden’s package can be expected to be disbursed in the coming months. But for the first half of the current fiscal year to end-March and including the Biden package the deficit commitment amounts to over $3 trillion, which compares with our estimate based on CBO figures of $2.595 for the second half of fiscal 2020. Therefore, the deficit trend is still rising, even on officially sanctioned estimates.

Further stimulus packages between March and September cannot be ruled out, if only because the pandemic has led to ongoing economic dislocation. There is no doubt that the Biden administration is exceptionally sympathetic to financing by inflation. We must also accept that evidence of higher prices for goods and services is being suppressed by CPI methods and that monetary inflation adds to the nominal GDP total. Increasing the money quantity is not just the line of least resistance, but it is being encouraged by statistical corruption and misrepresentation. The wealth transfer from wage earners and savers to pay for it, which is economically destructive, is wholly ignored.

But we keep returning to the bank balance sheet problem. Bank balance sheets have simply run out of capacity to absorb more inflationary financing. Last April, the temporary fix of suspending the supplementary leverage ratio, which penalises banks exceeding mandated levels of the relationship between total balance sheets and underlying equity, was announced by the Fed. That suspension is due to end this month, unless it is renewed. At the time of writing (10 March) there was no sign of an extension.

Elsewhere, I have written of the consequences. Put briefly, unless the SLR suspension is extended the banks will have no option but to turn away deposits, and the only way they can do this is to recover the SLR penalty costs by charging for them. In other words, the commercial banks will introduce negative deposit rates, initially for new deposits and then likely extended to existing customer balances. Since my warning that this is the case, Goldman Sachs’s banking analyst has confirmed the thesis, putting a $2 trillion number on it.

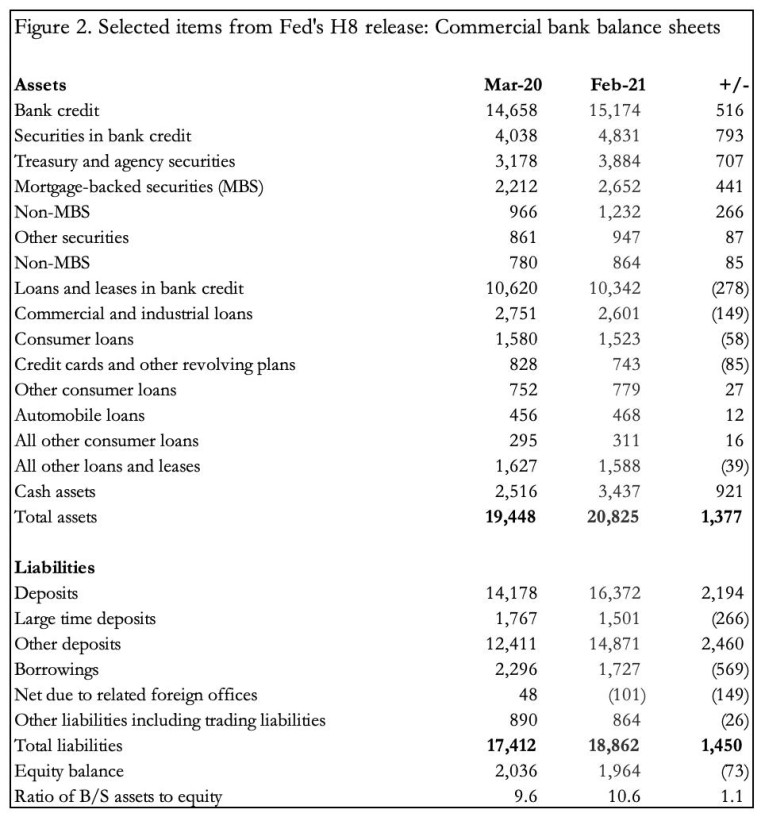

From the Fed’s H8 release (page 5), we can see that Goldman’s $2 trillion estimate appears to be derived independently from the Fed’s records. A precis of the Fed’s estimates of total commercial bank balances are shown in Figure 2.

There are a number of points worth noting, at a time of massive monetary expansion, with an increase over the year to end-February estimated at 46% measured by Austrian money supply:

-

Total assets increased by $1,377 during the period of SLR suspension. If we assume bank balance sheets had very little room for expansion in March 2020 and given the 10.6% reduction in bank equity, Goldman’s estimate of a $2 trillion excess to be clawed back in the absence of an extension to the suspension of SLR looks about right.

-

It is noticeable how banks have shifted assets from the loan business into securitisation, including Treasuries, agency debt and mortgage-backed securities. Picking out the bones of circulating capital provision for non-financials from these figures is an unrewarding activity.

-

The jump in cash assets is notable. The Fed’s footnote states, “Includes vault cash, cash items in course of collection, balances due from depository institutions, and balances due from Federal Reserve banks”. The increase of $921bn to $3,437bn makes cash balances over 15% of their balance sheets. Will this encourage the Fed not to extend the SLR?

-

Large time deposits have already begun to decline. It is not clear if this is the result of a general bank policy to discourage them or for other reasons. Nevertheless, as balance sheets hit constraints this deposit category appears to be the most likely to experience further reductions.

These numbers only reflect the current situation and will increase as the Fed continues its monthly $120bn of QE, and the US Treasury continues its funding programme. Even an extension of the SLR suspension for Treasury holdings and reserve assets at the Fed does not resolve the problem. Unless the extension is explicitly declared by the Fed to be permanent, banks will have to manage their balance sheets on the basis that the SLR will eventually be reinstated.

The balance sheet capacity problem is not going away, which means that banks will have to sell down riskier assets to make way for an increase in their holdings of US Treasuries and increases in their balances at the Fed arising not just from their own activities, but those of their investing institutional customers. This comes at a time when the non-financial economy will face enormous challenges.

Economic outlook for March to September

Pandemic lockdowns will continue after March, not just in the US but in other major jurisdictions as well. The global economy will not be free of covid this year, with the likelihood of a further resurgence with new variants next winter. At this distance, all one can suggest is that at the margin a Democrat administration is likely to favour control over personal freedom at the expense of economic activity.

Time will tell as to whether this concern is justified. Meanwhile, the damage done to leisure, air travel and tourism is substantial. Lockdowns have bankrupted shopping malls and their tenants. Whole industrial sectors have lost bankruptcy-threatening levels of sales due to the retail sector effectively closing in many parts. There have been beneficiaries, particularly online sales. But taken over the whole economy, it has been tantamount to a full-blown depression.

During this crisis, the large majority of salaried employees, who normally live paycheck to paycheck, will have suffered badly. Who can forget the food queues comprised of expensive SUVs, Mercedes and BMWs — all obviously bought on credit — as their spendthrift owners faced the reality of paycheck disruption?

The disbursement of funds by check from the government to these individuals will have helped enormously. But their indiscriminate distribution has led to a significant population minority with more money in their bank accounts than they are accustomed to hold and have been unable to spend. This is reflected in the increase in bank deposits shown in Figure 2 above. Consequently, production has been worse than decimated while inflated money is in the hands of consumers, itching to spend. And those who are unemployed have seen increased unemployment allowances.

The imbalance between hampered production and impatient consumer demand will drive prices higher. And because the effect is at the margin, prices are likely to rise faster than generally expected. To this we can add a further element, and that is the disruption to supply chains which is still causing logistical chaos. And we can also add the effects of a weakening dollar on commodity prices.

As producers try to respond to the unwinding of consumer cash balances, they will find that the constituents vital for production in the forms of raw materials and semi-processed goods will simply be unavailable or promised so at a distant future. The insufficient quantities that are available will reflect these shortages in their prices. And if they are lucky enough to find a way round these difficulties, producers ramping up production will find that the banks will be more intent on calling in loans than providing circulating capital.

Given the way it is constructed, CPI measures of inflation will fail to fully reflect the rises in prices. Food and utilities could even come under price controls — the predictable and last refuge of an inflating government. And it must be understood that a combination of the non-financial economy being flooded with consumption money will jack up nominal GDP, taken by statist planners as evidence of success. Just imagine if modern statistical method had defined the economic conditions in Germany, Austria, Hungary and Poland in the early 1920s. Suppressed evidence of price rises by CPI methods combined with money-pumping would evidence the most dramatic economic recovery. To begin with, they would be hailed as an extraordinary policy success, before an emerging realisation of the true economic condition brought about by monetary inflation. It appears that the US and other nations are embarking on this track of discovery.

But with Keynesian stimulus being seen as the only means for governments to fund their deficits, there is no escape — only escalation. It only takes a basic knowledge of arithmetic to understand that the more you inflate, the more you dilute and the more you have to inflate. Incorporate the wealth destruction factor and the process becomes hyper. The US is already on this monetary course, though very few observers yet realise it.

Pre-covid economic conditions are ignored

Even assuming an unrealistic and rapid return to pre-covid economic conditions, we still have the devastating effects of a collapse in outstanding bank credit, the collapse of banks around the world with insufficient capital to absorb the resulting losses (almost all of them), and the legacy of today’s version of Smoot-Hawley — President Trump’s efforts to close down the Chinese trade.

Supply chains are still in chaos. This is from the New York Times earlier this week:

“Off the coast of Los Angeles, more than two dozen container ships filled with exercise bikes, electronics and other highly sought imports have been idling for as long as two weeks.

In Kansas City, farmers are struggling to ship soybeans to buyers in Asia. In China, furniture destined for North America piles up on factory floors.

Around the planet, the pandemic has disrupted trade to an extraordinary degree, driving up the cost of shipping goods and adding a fresh challenge to the global economic recovery. The virus has thrown off the choreography of moving cargo from one continent to another.” Chaos strikes global shipping, New York Times, 7 March

The article goes on to say containers are in the wrong place, in African and South American ports, empty and uncollected. The disruption to America’s supply chains is on a scale related to the economy’s gross output, estimated at $37 trillion, with an additional amount for offshore imports and exports. The threat to trade finance is considerable, this week driving Greensill into insolvency – a relatively small player funded by Credit Suisse and investing institutional clients of London-based banks.

The now certain disruption in trade finance is on few commentators’ radar, yet. But with US and other banks lacking balance sheet accommodation and a desire to de-risk their exposure, it is another factor that threatens to grind the global economy to a halt. And what will be the authorities’ response? Inflate or die, or should we now say inflate and die.

Markets have an inconvenient habit of demanding recompense for anticipated inflation and the effect on a currency’s purchasing power. Whatever methods a central bank deploys for denying a currency holder’s recompense, it only succeeds in undermining its ownership; first on the foreign exchanges and then by its own people. Interest rates then rise. In the last few weeks, we have seen the heavily supressed yields on government bonds begin to rise alarmingly. But that is only the start of it. Tt will be increasingly expensive for the government to pursue its inflationary funding by having the Fed buy Treasuries at arm’s length for cash. Coupled with the lack of balance sheet space in the banking system, new avenues will have to be devised.

Perhaps the planned digital currency, which bypasses the banks, is an intended solution. Perhaps the Fed will abandon the charade of QE. Perhaps the concept of a trillion-dollar platinum coin will be resuscitated. But they are all variations on the fiat theme and will cut no ice. Pesky foreigners will still want higher interest rates, and the more the Fed lags their expectations, the weaker the currency will be.

Besides exposing the bankruptcy of government finances, rising bond yields will burst the financial bubble inflated by monetary means. When that goes, so will the dollar and all other fiat currencies that fail to take avoiding action. But markets anticipate events, so it will not require events to actually happen. The question as to when a market crisis kills off the Fed’s monetary policies and with them the financing of inflationary spending is the most important consideration facing us today.

For now, the investment establishment believes in three untruths; that the Fed will continue to control markets, that the CPI statistics are a fair reflection of the dollar’s declining purchasing power, and that economic growth is not just a money total. In the foreign exchanges a tipping point will occur when government statistics become questioned and rejected. The fall in the dollar measured against commodities and raw materials will than take on a new dimension.

Yesterday, after seeing his $1.9 trillion stimulus package passed into law, President Biden promised to announce his plans for the future. After digesting these numbers, will markets begin to make a more realistic estimate of effects on the dollar?

Postscript

Soothsayer: Caesar!

Caesar: Ha! Who calls?

Casca: Bid every noise be still: peace yet again! (music stops)

Caesar: Who is it in this press who calls on me? I hear a tongue, shriller than all the music, cry Caesar! Speak! Caesar is turned to hear.

Soothsayer: Beware the ides of March.

Caesar: What man is that?

Brutus: A soothsayer bids you beware the ides of March.

Caesar: Set him before me; let me see his face.

Cassius: Fellow, come from the throng; look upon Caesar.

Caesar: What sayest thou to me now? Speak once again.

Soothsayer: Beware the ides of March

Caesar: He is a dreamer; let us leave him: Pass

Alasdair Macleod

HEAD OF RESEARCH• GOLDMONEY

Twitter: @MacleodFinance

MOBILE: +44 7790 419403

Goldmoney

The Most Trusted Name in Precious Metals tm

NEW YORK | ST. HELIER | TORONTO

Publicly Traded Symbols: CA: XAU | US: XAUMF

© 2020 GOLDMONEY INC. ALL RIGHTS RESERVED. THIS MESSAGE MAY CONTAIN CONFIDENTIAL OR PRIVILEGED INFORMATION. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE ADVISE US IMMEDIATELY. THIS MESSAGE IS FOR GENERAL INFORMATION ONLY AND SHOULD NOT BE CONSTRUED AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY SECURITIES OR ANY OTHER FINANCIAL INSTRUMENTS. WE DO NOT PROVIDE TAX, ACCOUNTING, OR LEGAL ADVICE, AND RECOMMEND THAT YOU SEEK INDEPENDENT PROFESSIONAL ADVICE IF NECESSARY. WE CONSIDER INFORMATION IN THIS MESSAGE RELIABLE BUT WE DO NOT REPRESENT THAT IT IS ACCURATE, COMPLETE, AND/OR UP TO DATE AND IT SHOULD NOT BE RELIED ON AS SUCH. OPINIONS EXPRESSED ARE OUR CURRENT OPINIONS AS OF THE DATE APPEARING ON THIS MESSAGE ONLY AND ONLY REPRESENT THE VIEWS OF THE AUTHOR AND NOT THOSE OF GOLDMONEY INC OR ITS SUBSIDIARIES UNLESS OTHERWISE EXPRESSLY NOTED.

Notice: This email may contain confidential or privileged information. If you received this email in error or believe you are not the intended recipient, please notify the sender immediately and delete this email without forwarding or opening any attachments. Thank you for your cooperation and attention.

********