Inflationary Floodwaters At The Brink

When I was a very young boy, schoolchildren were not driven to school or to the bus stop; they walked from their houses, usually in groups, with older boys instructed to look after both the younger ones and the girls, lest they get lost.

In my case, I had to trek about three miles on the shoulder of Airport Road, with cars and buses and trucks rumbling by on their daily commutes, beside a sizeable ditch that every spring was filled to the brim with a six-foot deep torrent of floodwater that gushed toward Etobicoke Creek several miles away. Being a curious young whippersnapper, before the melting snow had a chance to completely thaw and turn the frozen ditch into a mini-rapids, not unlike the Niagara River, I used to build mini-dams out of mud, ice and snow to try to block the trickle of water, just like I would look at in the encyclopedia Mum kept in the living room.

Alas, no matter how industrious I was nor the density of the materials, there was nothing that could ever stop that water from finding its way downstream. It would either creep around the edges of my cleverly conceived obstruction or it would just blast its way forward, taking shards of wood and mud and ice with it.

I was reminded of this last weekend while going for a drive up into the Kawartha Lakes. Driving through the little town of Buckhorn, the melting ice in Buckhorn Lake was cascading down a rock chute into Lower Buckhorn, making such a din that you could barely hear the person in the passenger seat telling you to "Slow the **** down!" As I am prone to do, I was driven to analogies to the financial markets, and watching this thunderous wall of water crashing through everything in its path, what sprang to mind was how this thunderous wall of stimulus money being thrown at the American economy and financial system could ever prevent a devastating flood of hyperinflation in its wake.

Digging deep into my bag of economic and financial market trivia, I find that there is simply no amount of "productivity gain" that can offset the massive pressure being exerted on prices, and no matter what the former stock salesman Jerome Powell tells you, Fed policy has only one concern (as in "master"), and that is the banking system.

The late Richard Russell, whose "Dow Theory Letters" was my market "bible" for over 30 years, until his passing six years ago, used to always tell his readers to "follow the money." That was especially true when he spoke of Fed policy. Were he alive and writing today, he would surely point to the banking system as the ultimate beneficiaries of this larcenous largesse being bestowed upon holders of bank collateral through Fed bond buying and governmental interventions. After all that has been said and done since those insidious REPO actions started in late 2019, it is residential real estate that has been blown into a bubble of epic size and proportion, with countries such as Canada and Australia leading the way in "bubbliness."

Here in my native province of Ontario, it is impossible to afford a single-family detached home for anything less than $500,000, and anywhere within the Greater Toronto Area (the GTA), $1,000,000 gets you a postage stamp. Sadly, it is the wealthy immigrants who are buying up all the land, with second- and third-generation Canadians relying on parental or grandparental financial assistance in order to own lodging. The net intent of pro-inflation policies of the Bank of Canada is to protect the collateral that underpins mortgages, because with workers no longer needing to sit in the petri-dish cubicle next to a coughing coworker, commercial real estate is in big trouble. So as long as housing remains buoyant, the gaping balance sheet hole represented by leaking commercial loan portfolios can be plugged at least for awhile. Otherwise, there is nothing good about a housing market that forces young families to be in debt for the rest of their lives just to have a roof over their heads.

The only way this plays out is with wages. The average wage of workers in countries whose central planners are promoting higher bank collateral values is going to rise dramatically to increase affordability and serviceability. And therein lies the trap for the policymakers the world over. The 1% that own all the stocks and bonds and all the real estate and all of the banks around the world are going to face a day of labor market reckoning, and the last time we saw wage demands out of control was in the 1970s. To wit, it was the 1970s "stagflation" that saw muted economic growth against rapidly rising prices that drove gold and silver (and copper and oil) into the stratosphere. And there is no amount of wood and mud and ice and snow that can prevent that very torrent of inflation from proceeding down to Etobicoke Creek.

Gold prices have been acting somewhat better since I called the first bottom on March 9 at $1,680, and then again on March 30, at the same price level. Despite the fact that I have taken two nice trades out of those $70 bounces that have helped to keep the wolf away, I am not that "happy." While many of you will be dismayed to read this, I am worried about the precious metals looking out to the second half of 2021. Rather than staring at bark, I am forced to rise above the trees and look down at the forest below me in order to make a rational assessment of the current state of the precious metals, given the stark reality of the situation.

Here we are, in the spring of 2021, after trillions upon trillions of phony stimulus dollars have been injected into the system, with another US$3 trillion in "infrastructure spending" (managed by the banks, of course) looming on the horizon, and gold sits 16.5% off its all-time high. Silver is trading at around 50% of its 2011 high despite massive demand and physical offtake. In fact, if we are to believe the pundits, physical offtake of gold and silver is at record levels. So, if that is the case, why, pray tell, are neither of these monetary metals at all-time highs?

Oil and housing are in full recovery mode; Bitcoin is at nearly $60,000 per coin; stocks are at record highs; technology is booming, yet the two historical safe haven assets, with 5,000-year roles as "guardians of wealth," cannot seem to mount anything vaguely resembling a sustainable rally. Since gold's top last August, we have been wallowing in the dentist's chair for an eight-month root canal (sans novocain), having to listen to clueless bubbleheads brag about their new $100,000 driverless Tesla, paid for with their cryptocurrency winnings that also pay for the $30,000 repair job caused when the driverless Tesla rammed into a bread truck. "Maddening" is an understatement.

For now, it is my belief that $1,670-1,680 will hold as the low for gold, but I will be watching the HUI very closely, along with silver, for confirmation that something more ominous is not in the cards. The near-term problem for both metals is that the bond yields are rising in response to the escalating CPI, which puts downward pressure on "real" rates of interest. Unfortunately, it is not relevant that the stated rate of inflation by the Department of Labor Statistics or the Commerce Department is bogus; the algobots that are running rampant in the Crimex futures pits smack our monetary metals around based upon these numbers. And you can't explain to your local merchant that you cannot pay for the groceries because "the government is fudging the numbers."

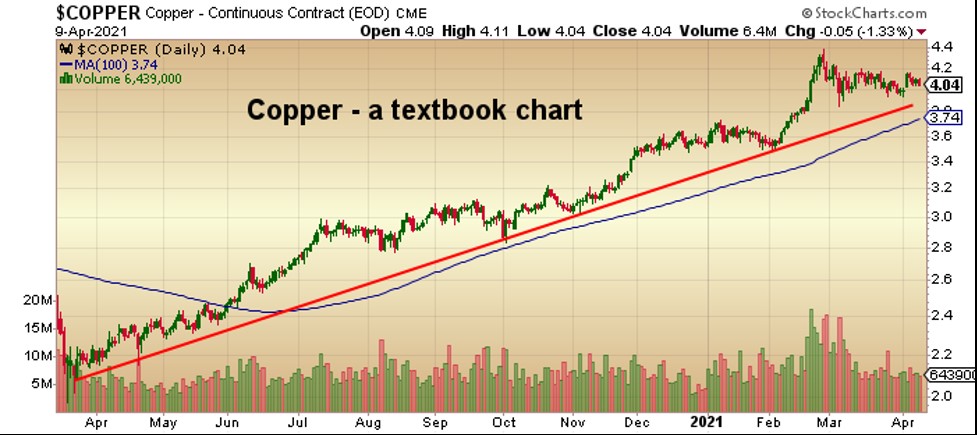

Copper and uranium remain the two pleasant surprises for me here in the second quarter of 2021, with Western Uranium & Vanadium Corp. (WUC:CSE; WSTRF:OTCQX) (CA$2.47/share; US$1.94/share)stealing the limelight in the 2021 GGMA Portfolio, having closed the week up 122.49% year to date. Subscribers participating in a February unit financing at CA$0.80 have been more than surprised by the performance of WUC, but I am first to admit that anyone participating in uranium producers or developers are enjoying spectacular performances. UEC, UUUU, and PALAF are all up sharply, but not nearly as much as WUC, whose 55 million pounds (lbs) of U3O8, worth US$1.7 billion sitting at the Sunday Mine Complex in Colorado, is certainly "noteworthy."

I have a new copper story developing and am eagerly awaiting the closing of a unit financing this month in order to launch my Special Situations report. The entire concept of copper taking on the "#1 Electric Metal" moniker in the second half of 2021 has me fascinated more and more each time I read reports from the major banks and the multinational producers around the globe.

Copper is in shortage now, and it is not going to get any less so anytime soon. More importantly, debunking the argument that "the best cure for rising prices is rising prices," with a smirking reference to latent supply rushing in to satisfy FOMO (fear of missing out) demand at important price points, new copper supply does not arrive with the stroke of a pen or the flicking of a switch. It takes billions of dollars to build a new copper mine capable of meeting global needs and it also takes years to build one. This is why I see this current commodity supercycle dominated by electricity needs everywhere we look, and if there is one metal that sits at the forefront of electrification, it is copper.

I see the US dollar price for a pound of copper through $5.00 by the end of summer, and $6.00 in 2022, and since the lag time between high prices and the arrival of new supply will be significant, copper prices could get "silly" long before the new project supply is able to calm the market back down. Therein lies the opportunity for junior copper developers, especially ones with significant in-ground resources and the management teams to execute.

My prerequisite for investment led me to this new opportunity, which I will be unveiling, and it is with great anticipation that I await the closing of this final round of financing prior to the arrival of news flow associated with acquisitions and nascent production capabilities.

Finally, if you liked my story about springtime ditch dams and chaperoning little girls to grade school, wait until next week when I tell you about "class trips to the barnyard."

Never mind.

Originally published April 10, 2021.

Follow Michael Ballanger on Twitter @MiningJunkie. He is the Editor and Publisher of The GGM Advisory Service and can be contacted at [email protected] for subscription information.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.Disclosure

1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Western Uranium & Vanadium Corp. My company has a financial relationship with the following companies referred to in this article: Western Uranium & Vanadium Corp. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Western Uranium, a company mentioned in this article.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Charts and graphics provided by the author.

*********