It’s The US Dollar, Stupid!

Don’t let the bull-tards tell you the stock market over here is falling because of China’s problems, or Grexit, or fear of the nebulous Fed rate hike.

Don’t let the bull-tards tell you the stock market over here is falling because of China’s problems, or Grexit, or fear of the nebulous Fed rate hike.

We’ll just see about that last one now anyway!

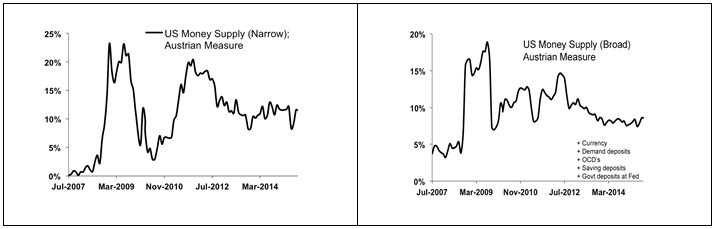

The US asset bubble is the biggest one on the planet today, and it just went pop. The currency too has rallied over the past few years on the fairy tale that everyone else is inflating while the US is about to tighten, which may have been more plausible if they just started telling it now, and the dollar had not yet gained 65% on the Yen, 35% on the CAD, 30% on the Euro or 25% against a basket of trade weighted currencies -on exactly that story. They have been talking that game for a long time in fact. The worst part about it is that it hasn’t been true, at least not until now. The Fed has expanded money the most in the post 2008 environment -more than the ECB, more than the BOC, BOE, SNB, RBA, and probably more than the BOJ if my suspicions are correct.

Even in the past year it has expanded money more than all of those except the ECB, based on recent M1 data from the OECD. In the past 3-5 yrs the US has inflated its money more than China, Russia, and Brazil; in the last 5 yrs it has inflated more than many emerging nation states, including South Africa, Korea, and India.

If this runs contrary to what you hear it underscores what I am saying -i.e., that the USD is over-valued.

Although the Fed ended QE3 late last year and money growth slowed mostly everywhere, including the US after 2011, both the growth rate and the nominal amounts of money created in the US were still greater.

[This was because the banks took back their position in the money creation cockpit in 2014.]

China is increasingly influential in world trade and politics but relative to US assets it is under owned. This is true of the Yuan as a reserve currency too. So I wholeheartedly and emphatically disagree with anyone who would claim that a China collapse can have a greater impact on world financial markets than a US collapse.

However, commodities are different. Their impact on commodity prices is huge. In fact, one reason I don’t buy the China bubble thesis at the moment is because money growth (M1) has collapsed to almost zero there, after peaking in 2010 at over 30% year over year. Their financial bubble popped years ago, and with it the commodity bubble, which basically attests to what I’m saying -i.e., that monetary conditions in places like China, Brazil, and Russia have not been as easy as the media has made out. Now, I argue, contrary to most, that Chinese authorities will use this stock market “crisis” as an opportunity to start a new bubble. They have said as much with the central bank’s response to the margin problem and its decision to devalue the currency.

But in terms of the size and scope of their financial assets, the proportion owned by foreign investors, the amount of money created by the central bank, irrational exuberance and over valuation - i.e., which bubble is bigger and most crowded - the US situation wins hands down. Importantly, we have been writing about a deterioration in the technical condition of the US stock market long before China or Greek jitters resurfaced.

The Importance of Decelerating Money Growth

I’ve covered the negative trend in corporate profits for over two quarters (in the US), as well as the extremes in sentiment and financial valuations. Most relevant in my model was the 2011-14 downturn in US money supply growth, even though it lagged many of the countries that investors think have had the easiest policies.

Austrian economist Frank Shostak made a similar argument recently about the 2011-14 downturn in his US money supply indicator -comparing it to the pre 1929 deceleration, which I thought compared better with the last downturn (2008). But it doesn’t really matter. The important part is the deceleration in money growth.

That is the early trigger for the “bust.” Recall, the boom-bust cycle is the result of an artificial suppression of interest rates. However, interest rates are suppressed due to the expansion of money supply - which is hence the ultimate root cause of the cycle. The lag is variable and can range from 1-4 years. In Mr. Shostak’s article, the pre 1929 decline in narrow money supply growth started in 1925, and ended in 1927 (i.e., 2-4 year lag).

In fact, it started turning up again going into 1928-29; this was the part that matched the 2008 crisis better.

In either case (1929 or 2008), or in most of the cases I’ve studied in the postwar period, I have found that the 5% level has proved to be a good indicator for the bust, which is why I have adopted it in my model.

However, note that we haven’t fallen below 5% since the 2006-08 period (which triggered the last crisis).

For that reason I have been reluctant to short the stock market until this year, when I saw the collapse in the oil boom at the end of 2014. I took that collapse, and the obvious internal deterioration in the stock market over the past year as evidence that the 2011-14 deceleration in money growth may indeed have been enough.

I rationalized that since money growth after 2008 was higher than the historical average, the decline to its long-term average growth rate (~7%), which was about 4% below its average post 2008 level, may have had the same impact as previous declines to below 5%. Regardless, the key engine of money growth since the Fed exited QE3 (but not ZIRP) has been the commercial banks, which ramped bank credit growth back up to the historical norm also near 7% by the end of 2014. After accelerating into the first half, total bank credit growth has slowed to about 5.5% in recent months in the US, suggesting money growth is headed below 5% anyway.

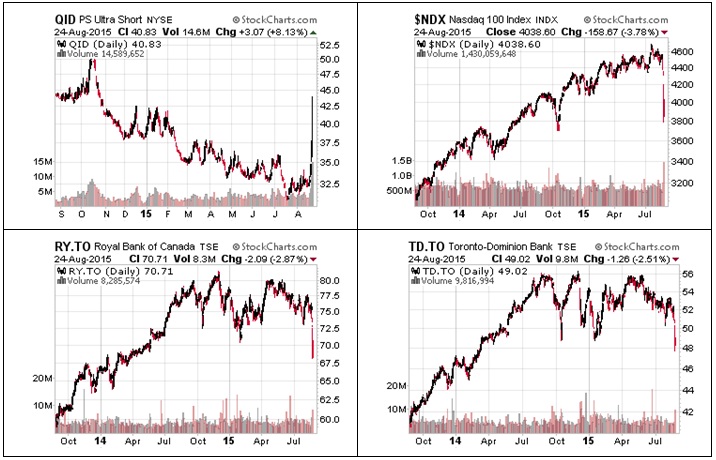

Update: Proshares Ultrashort (QID) Trade

The stock market has started to crash. I was looking for a 5-10% correction in the DJIA going into the fall -implying a move down to October’s low. I didn’t expect that low to go so soon but the bears took it out in the DJIA and the Transports way too easily! The October low is important as it represents primary or bull market trend support.

If the break holds and is confirmed by the S&P and NASDAQ in coming weeks then we will have a new bear market. It was almost too effective of a reminder that these things can happen. The short-term sentiment indicators have run to the other extreme.

All other indicators remain largely bearish however - i.e., valuation, monetary, profit trends, and technical situation. The technical deterioration I have frequently alluded to is just now becoming visible to the crowd.

The fear factor in a panic is likely to be loud enough to elicit a response from the Fed.

Be on guard for QE4 or some kind of response soon, maybe at -20% on the S&P 500 if the bulls can’t shore it up by fall. That is not an arbitrary number. It is the media’s definition of a bear market. Less has prompted new easing cycles in the past. For the DJIA that would be at about 14800, which it almost reached intraday Monday. In the S&P 500, which is down 12% as of this writing, it would be at around the 1720 level. In both cases that would mean another 8% decline, which is likely, but some ebbing may be in order after such a hit.

On July 27th I recommended buying the Proshares Ultrashort QID ETF at $32.89, putting a mental stop at about $31.37. The shares hit a 10 month high of about $44 Monday morning before closing at $40.75.

My target was the $38-42 area, and I suggested the possibility of a run to $50.

Since the target was reached feel free to book a profit, whole or partial, immediately.

Normally I wouldn’t hesitate. but something about the way this thing started coming apart reminded me that a 1987 style crash is not out of the question here. Rather than trading out our QID position, which is up 24% at the moment, I therefore decided to tighten our stop to the ~$38 level. That still locks in a 15% gross return, but keeps you long in case this thing runs all week without much ebbing. It looks like there should be support between $36-38 so keeping your stop anywhere in there might be smart (please remember that these are mental stops – subscribers will get an alert if we pull the trigger and exit a position).

I’m also tightening the stops on our bank shorts to $78 and $53 (for the Royal Bank and TD respectively) from $85 and $56 previously. My trading targets on those short positions are $62.50 and $45 (CAD’s).

Let me emphasize that I do not expect a 2008 type crisis.

I am looking for a 2000-02-type bear market with a 30-40 percent correction over a couple years, but I wouldn’t rule out a 1987 type scenario where we get a 25-30 percent crash, prompting QE4 from the Fed.

I’d bet they will put on a brave face at first but as we head towards the 20% bear market milestone their face will show consternation. What are they going to do with asset prices reeling and interest rates near zero?!

Sha-na-na-na, sha-na-na-na, sha-na-na-na, good-bye, especially for the dollar.

Gold Prices Weighed Down by Commodity Bear Market

The gold sector is ripe for an asymmetrical blast off, based on valuation, sentiment, and its position as a counter cyclical asset class. But one of the factors that weigh on gold is the collapsing commodity complex.

The reason for the commodity decline has already been pointed out but gold’s relative resilience has caused its value in most commodity terms to soar.

This ratio (Gold/CRB), for example, is at a record.

In my outlook the growth in non US money is going to pick up now and the rally in the US dollar is going to fail, not necessarily in that order. I see the anti dollar trade returning, but that could just mean gold will underperform many commodities on the way up for a while, as it did in the last USD route (2001-07).

The gold miners had their best performance in the 2001-03 period mainly coming out of an overly beaten up position. We expect that likewise in the current situation gold shares will hold up in a wall street downturn as long as I am right about the US dollar. With a lot of write offs behind them and the increase in profit margins resulting from lower energy and other commodity costs I wouldn’t be surprised to see profit surprises ahead, even on a minor upturn in gold. In any case, although the USD chart looks weak too, the gold and commodity markets are in a steep downtrend. I see this changing but the broad commodity decline is a headwind, and in the initial stages of the reversal I expect gold prices to underperform… but for gold shares to explode higher.

One way to take advantage of this situation is to buy silver. I usually prefer gold over silver; except when gold trades over about 65x the silver price. It is currently trading at 78x, which is near the high end of its historic range between about 18x (1920, 1969) and a high of 99x (1942, 1992) in the 20th century. At the 2011 high for the pm trade gold was trading at 32x the price of silver (at anywhere below 55x I prefer gold to silver).

The Deflation Ogre

Some investors are worried about deflation, or a 2008 repeat, who can blame them.

But that is what you are seeing in the miners’ shares at the moment.

If the market crashes like in 1987 or 2008 then there may be a little bit of downside in gold shares.

I have ruled out a 2008 repeat for now because I expect the Fed to overcompensate in the easy direction.

But even if I didn’t, I would rule out a repeat of the action in gold miners. Going into both 1987 and 2008 they were part of the bull market excess. I much prefer the 2000-02 model here. There are many similarities - the overvalued USD, the lopsided recovery (with US assets practically the only game in town), the extreme valuations in tech stocks relative to the miners, the gold/crb ratio, and so on. Even the deflation noise was loud back then… louder than it was going into 2008. And it was just as bad an argument then, as it is now.

I am not going to get into the economics of deflation here because I’ve beat that horse to death over the years, but I will refer you to an excellent video clip by an aspiring up and coming young economics professor named Philipp Bagus. It is a recent presentation at Mises University, and covers everything you want to know about the dreaded deflation… i.e., the different types, and whether they are necessary signals or market failures.

The two types that are relevant to us in the short term are: (1) the type that results from an increase in the demand to hoard cash (due to uncertainty), and (2) the debt-deflation ‘threat’ brought about by a collapse in fractional reserve bank credit. The former is bullish for gold, and the latter is used as pretext to justify QE.

The threat is real but as long as it is not allowed, it is not in play either. It is not up to the market, it is up to the Fed. So if you are waiting out a 2008 crisis (or deflation) to buy the gold stocks, I think you will be late.

Gold Price Technicals

The stock market and dollar trend is in the throes of a potential reversal but the gold, silver and commodity markets are still largely confined to relatively well-defined bear market trends. I’m going to give you a quick analysis of the gold price trend in particular because I believe there are some worthwhile facts to recognize.

In the graph above, note the 2011-15 bear market consists of two developments. There was a top through 2012 (descending triangle sort of) followed by a break down to the textbook target of around $1185, which held until a new downtrend became apparent in the primary sequence starting in H2/2014. But you can see that this downtrend (2013-15) really consists of two failed bear raids. The first was the break down from a 15 month descending triangle in late 2014. That break down implied a $968 objective but instead the price of gold rallied back up through the neckline ($1185) of that triangle almost instantly, which technical analysis would consider to be a failed break down. In follow up action the gold price straddled that $1185 handle to produce what some analysts referred to as a small 9 month bearish head and shoulders pattern (Oct-Jun) with its neckline at about $1140. This summer, in response to the Greek-China jitters and an initial rally in the USD, we fell through that level only to reverse back up through it again on the current market meltdown.

But we are still below the $1185 neckline.

Regardless of the good signs we have to recognize this as a downtrend, and you have to remember that the commodity trade is weighing on gold values here (as is the deflation bogeyman). I think you will see gold react very strongly if the Fed shows any weakness in reaction to the unfolding crisis. Technically speaking, the milestones are thus: short term resistance at $1185; intermediate downtrend resistance at $1250-1350; and primary bear market resistance from $1535-1635. According to our shadow gold price indicator (see front section of newsletter), fair value for the price of gold is roughly between $935 and $1804 (or $1370).

Keep an eye on those resistance levels as milestones. What you want to do is watch how gold approaches each one. Does it hesitate, is it coming up hard with momentum or is it just retracing a downward move.

I’ll keep you posted. I can’t rule out short-term downside here for as long as we remain in this downtrend and the commodity trend is down. Gold has come down a lot but is not as absurdly cheap as the miners or silver.

********

News...

I am working on many exciting things for the newsletter.

I’m writing one report where I will take you through an attempt to put a valuation on gold, and another that will reveal the last five companies to round out my precious metals growth portfolio -a portfolio of 20 companies designed to outperform the mining averages (and gold itself) in the next upswing. One of these names is a massively undervalued rare metals restructuring and takeover candidate trading below a nickel.

I think it is worth five times that today, and potentially 50 times that if I am right about the asset.

Stay tuned, or upgrade to the premium subscription to hear about it first.

Ed Bugos is a mining analyst, investment banking professional, and senior analyst at The Dollar Vigilante (an online guide to surviving the dollar crash), with more than 20 years experience in the investment business advising clients on portfolio and trading strategies.

Ed Bugos is a mining analyst, investment banking professional, and senior analyst at The Dollar Vigilante (an online guide to surviving the dollar crash), with more than 20 years experience in the investment business advising clients on portfolio and trading strategies.