LBMA Confirms Upcoming Publication Of London Gold Vault Holdings

Just over a week ago I wrote an article highlighting that the Bank of England has begun publishing monthly data on the total quantity of gold bars held within the Bank of England vaults in London. See “Bank of England releases new data on its gold vault holdings”.

This new gold vault data was first released in early April 2017 and covers gold bar holdings at the Bank of England for every month-end for the last 6 years. Going forward, the Bank will publish updates to this dataset every month, on a 3-month lagged basis.

The move by the Bank of England to publish this data was first reported by the Financial Times in February and was supposedly part of a broader gold vault reporting initiative which was to include vault holdings for all 7 of the London Bullion Market Association (LBMA) commercial precious vaults in London. These commercial vaults are run by HSBC, JP Morgan, Brinks (on behalf of itself and ICBC Standard), Malca Amit, Loomis and G4S. While the Bank of England had single-handedly gone ahead with its side of the reporting initiative, the precious metals vault holdings data from the LBMA was conspicuously absent when the Bank of England made its move. As I wrote in my article last week:

“The London Bullion Market Association was also expected to publish gold vault holdings data for the commercial gold vaults in London, but as of now, this data has not been published, for reasons unknown.”

“While the Bank of England has now followed through with its promise to publish its gold vault holdings, the LBMA has still not published gold vault data for the commercial gold vault providers, i.e. its members HSBC, JP Morgan, ICBC Standard Bank, Brinks, Malca Amit, Loomis and G4S. Where is this data, why is there a delay, and why has it not yet been published?”

However, as if by magic, the LBMA has now just issued a press release titled “LBMA to publish Precious Metal holdings in London vaults”. Coincidence, perhaps. But whatever the case, the LBMA development is timely, and the press release, which is actually a combined press release from the LBMA and one of its alter egos, London Precious Metals Clearing Limited (LPMCL), makes interesting reading, but unfortunately at the same time is still quite vague, and appears to suggest that some of the vault operators in question have been dragged kicking and screaming to the start line.

Summer of 2017

The statement from the LBMA reveals that:

“from summer 2017 the LBMA will be publishing the gold and silver physical precious metals holdings of the London vaults, with the platinum and palladium holdings to be published at a later date”

The statement also clarifies that “the data only includes physical metal held within the London environs” and that it will cover “aggregate physical holdings”.

Given that the LBMA and Bank of England work very closely, its disappointing and bizarre that the LBMA didn’t coordinate the vault data release at the same time as the Bank of England, because, at the end of the day, this is just some simple holdings data we are talking about, and all the vaults concerned know precisely how much precious metal they are holding at any given moment.

As a reminder, the Bank of England established by the LBMA in 1987, the Bank of England is an observer on the LBMA Management Committee, and the former head of the Bank of England Foreign exchange Division, Paul Fisher, is the recently appointed ‘independent‘ chairman of the LBMA Management ‘Board’ (formerly known as the LBMA Management Committee). See “Blood Brothers: The Bank of England and the London Bullion Market Association (LBMA)” for more details.

Representatives of the two large commercial vault operators in London, HSBC and JP Morgan, also sit on the LBMA Board. Additionally, representatives of the vault operators HSBC, JP Morgan, Brinks and ICBC Standard Bank also sit on the LBMA Physical Committee and all of the vault operators are represented on the LBMA’s Vault Managers Working Party.

The reference to ‘aggregate physical holdings‘ in the press release is also potentially disappointing as it seems to imply that the LBMA will not break out its vault reporting into how much gold and silver is held by each of the 7 individual vault operators in and around London, but might only publish one combined figure each month end.

A reporting format in which each vault/operator is listed alongside the quantity (tonnes or thousands of ounces) of gold and silver held by that vault operator would be ideal. For example, something along the lines of:

Gold (tonnes) Silver (tonnes)

- HSBC x x

- JP Morgan x x

- ICBC Standard x x

- Brinks x x

- Malca Amit x x

- Loomis x x

- G4S x x

- Bank of England x no silver

Quantity per vault is the approach taken in the daily precious metals vault reports that COMEX releases on its approved vault facilities in and around New York, as per an example for gold here. HSBC, JP Morgan, Brinks and Malca Amit submit inventory levels to COMEX for that report. Likewise, HSBC, JP Morgan, Brinks and Loomis submit inventory levels in New York to ICE futures for its version of the gold futures inventory report.

Given that the individual vault operators based in New York report precious metals inventory to COMEX and ICE, is it too much to expect that many of the same vault operators cannot do likewise for their London vault facilities?

It remains to be seen which date ‘summer 2017” refers to. This seems like a bizarre non-committal cop out by the LBMA not to have announced a definitive date for beginning to report vault data. Summer 2017 could mean anything. Assuming they are talking about the northern hemisphere, summer could mean anywhere from May to August or beyond.

If the LBMA data is on a 3-month lagged basis in the same way that the Bank of England data is, the first tranche of LBMA vault data could neatly be released after 30 June and would cover month-end March 2017. As a reminder, the Bank of England gold vault data shows:

“the weight of gold held in custody on the last business day of each month. We publish the data with a minimum three-month lag”

Why the vault data on a platinum and palladium can’t be published at the same time as the gold and silver data is also puzzling, because the London Platinum and Palladium Market (LPPM) is now officially integrated into the LBMA following a change in the LBMA’s governance and legal structure in 2016, so both sets of data are now under the remit of essentially the same Association.

It also remains to be seen whether the LBMA data will have a 6-year historical look-back as the Bank of England data does, or whether it will just begin with a one month-end snapshot? For consistency with the Bank of England data, the LBMA vault data should ideally cover the same time period, i.e. every month beginning at January 2011. In short the LBMA press release is lacking quite a lot of detail and unfortunately invites guesswork.

The Importance of the Vault Data

Turning quickly to why this gold vault data is important. Simply put, at the moment there is little official visibility into how much physical gold is stored in the London Gold Market, and how much of this gold is available as “liquidity” to back up the market’s huge fractional reserve gold trading volumes. Albeit for silver.

In my coverage on 28 April of the Bank of England data release, I had phrased the relationship between physical gold and gold trading in the London market as follows:

“this physical gold stored at both the Bank of England vaults and the commercial London vaults underpins the gargantuan trading volumes of the London Gold Market”

Interestingly and somewhat synchronistically, in its 8 May press release one week later, the LBMA uses very similar phraseology, as well as the identical verb ‘underpins’, when it states that:

“the physical holdings of precious metals held in the London vaults underpins the gross daily trading and net clearing in London”

Another coincidence perhaps, but the LBMA is now also saying that the physical gold bars which they will report on starting in summer 2017, and which the Bank of England has just started reporting on, literally ‘underpin’ or support the massive volume of gold trading in the London Gold Market.

“Net clearing” refers to London clearing volumes for gold and silver that are processed through the LMPCL’s clearing system AURUM, and that are published each month by the LBMA, a recent example of which, covering month-end March 2017, can be seen here. In March 2017, an average of 18.1 million ounces of gold (563 tonnes) and 203.2 million ounces of silver (6320 tonnes) were cleared each trading day.

Since trade clearing nets out actual trading volumes, these clearing figures need to be grossed up to reveal the true trading figures. Using a 10:1 ratio of trading to clearing, which is a realistic multiplier as discussed here, this would be equivalent to 5630 tonnes of gold and 62,200 tonnes of silver traded each day in the London wholesale gold and silver markets. On an annualised basis, for gold, this would imply that the equivalent of over 1.4 million tonnes of gold are traded per year in the London gold market, quite an amount, seeing that less than 200,000 tonnes of gold is said to have ever been mined throughout history.

The LBMA press release goes on to say that:

“Publication of aggregate physical holdings is the first step in reporting for the London Precious Metals Market.

The next step is Trade Reporting.

The collection of trade data will add transparency to the market and provide gross turnover for the Loco London market. Previously gross turnover had been calculated from one-off surveys or estimated from the clearing statistics.“

With the LBMA vault reporting being the first step, but only coming out in the summer of 2017, its anyone’s guess as to when LBMA trade reporting will be coming out, a project which has been bandied about in the financial media and by the LBMA for nearly 3 years now, but which must take the record as the slowest fintech formulation and release in the history of London financial markets, ever.

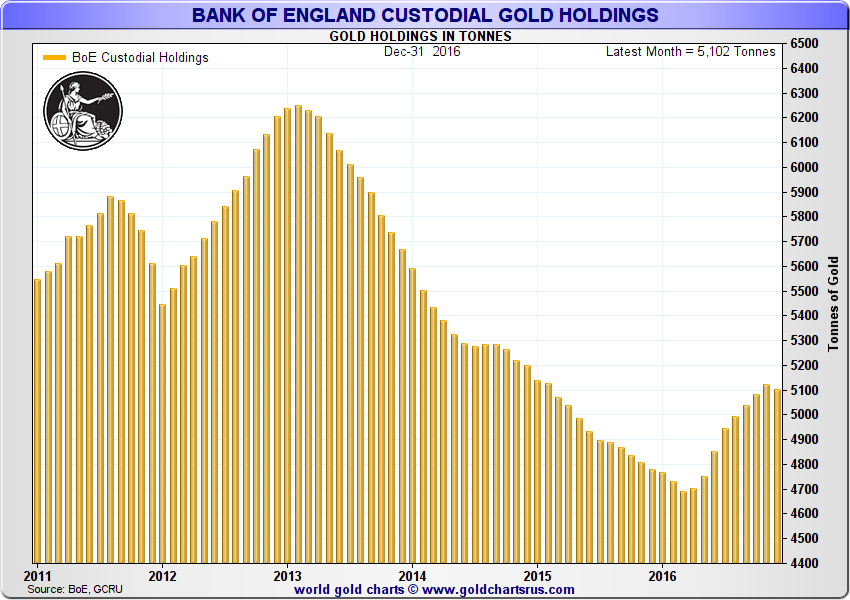

Source: www.GoldChartsRUS.com

The Bank of England’s latest physical gold holdings for January month-end 2017 is only in the region of 5100 tonnes of gold bars. Furthermore, since the LBMA say that there are only about 6500 tonnes of gold in the entire London market, the LBMA commercial gold vaults in London have to hold far less gold than the Bank of England. Add to this the fact that the gold in the commercial vaults is mostly held on behalf of gold-backed Exchange Traded Funds (ETFs).

Given the above, it becomes increasingly clear than when the LBMA does decide to release gold vault holdings figures sometime in summer 2017, whatever figure(s) is released, will most likely confirm that there is very little gold in the London market which is not claimed to be owned by either a central bank or a gold-backed ETF. It will also provide a field day for all sorts of theories and calculations about the true ratio of gold trading volumes to gold bar vault holdings, and how much of this gold is allocated and earmarked, and how much can be considered a combined bullions banks’ float.

A Quick Calculation

Its possible to go someway towards estimating a minimum figure for how much gold to expect the LBMA to report on the commercial vaults when it begins vaults reporting this summer. The same exercise could be conducted for silver but is beyond the scope of this analysis. For gold, when such a figure is calculated and added to the amount of gold in the Bank of England vaults, it gives a grand total of how much gold is in the combined LBMA and Bank of England vaults in London.

A large number of high-profile gold-backed ETFs store their gold bars in LBMA vaults in London, mainly in the vaults of HSBC and JP Morgan. The HSBC vault in London holds gold on behalf of the SPDR Gold Trust (currently 853 tonnes) and ETF Securities (about 215 tonnes). The JP Morgan gold vault in London holds gold on behalf of ETFs run by iShares (about 210 tonnes in London), Deutsche Bank (95 tonnes), and Source (100 tonnes). An ABSA ETF holds about 36 tonnes of gold with Brinks in London. In total, these ETFs represent about 1510 tonnes of gold. For the approach used to calculate this type of figure for gold-backed ETFs, please see “Tracking the gold held in London: An update on ETF and BoE holdings“.

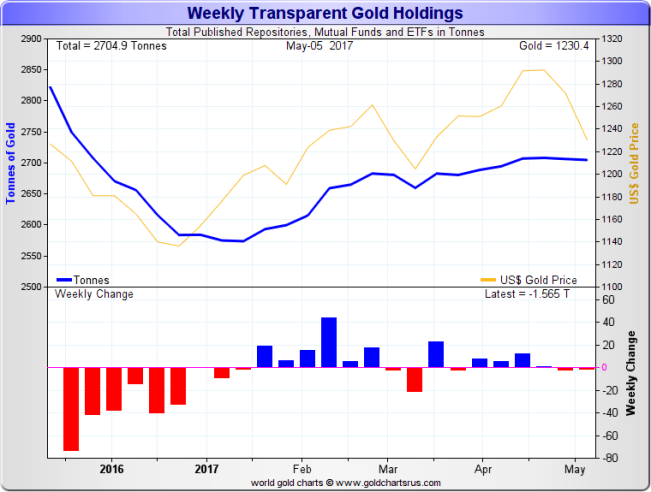

ETF gold holdings (most of which are stored in London) have been relatively static since mid-March 2017. See chart below. Therefore if the LBMA starts reporting vault gold holdings for a month-end date such as month-end March 2017, it would probably reflect about 1500 tonnes of ETF gold, mostly held by at HSBC and JP Morgan vaults in London. This is assuming that some of the ETF gold is not held in sub-custody at the Bank of England vaults.

Source: www.GoldChartsRUS.com

Until the LBMA starts its vault reporting, its unclear how much other gold is in the commercial vaults in London above and beyond the ETF holdings. However, non-monetary gold regularly flows in and out of the London Gold Market from gold trade with countries such as Switzerland. While March 2016 to October 2016 was a period in which the UK was a strong net importer of non-monetary gold from Switzerland, since then the UK has been a net exporter of gold to Switzerland, and has exported 325 tonnes of gold from October 2016 to end of March 2017. Therefore, whatever data the LBMA starts reporting, it logically should reflect the renewed outflow of gold from London to places like Switzerland and would tend to suggest that whatever excess bullion bank float gold is in the London commercial vaults, it is less than it would have been in the absence of these renewed outflows.

The vaulting page of the LBMA website still has there are:

“6,500 tonnes of gold held in London vaults, of which about three quarters is stored in the Bank of England”

While this web page text is probably slightly out of date, a literal interpretation would imply that 4875 tonnes of gold are in the Bank of England (which is not too far from the actual figure) and that 1625 tonnes are in the commercial vaults (which would mean that very little non-ETF gold is in the commercial vaults).

The Bank of England claims to have about 72 central bank customers with gold accounts, For month-end January 2017, the Bank of England is reporting that there was approximately 5100 tonnes of gold in its vaults. At least 3800 tonnes of this gold is claimed to be owned by 34 known central banks. See “Central Bank Gold at the Bank of England” for more details. That would leave about 1300 tonnes of gold at the Bank of England owned by a selection of other central banks and bullion banks. As to how much gold the bullion banks hold at the Bank of England is not clear, but since central bank gold holdings are relatively static (at least when excluding gold lending), then most of the month-to-month movements in Bank of England gold vault holdings are most likely due to bullion bank activity.

As to how easily bullion bank gold holdings at the Bank of England can switch to or be transported to the vaults of the commercial vault operators in London is also unclear, as logistics is a secretive area of the London Gold Market.

So with (1500 ETF tonnes of gold + X) in the commercial vaults, and 5100 tonnes of gold in the Bank of England vaults, this gives a grand total of 6600 tonnes of gold + X in all the vaults of the London as of early 2017. X could be 400 tonnes, it could be 1400 tonnes, or it could be any other figure of similar magnitude. My guess is that there is not that much gold in the commercial vaults above and beyond whats in the gold-backed ETFs. Maybe a few hundred tonnes or so. However, we will have to wait until the dog days of ‘summer’ in London to know this definitively.

Ronan Manly

E-mail Ronan Manly on: [email protected]

More from Gold-Eagle