Monetary Metals Supply And Demand

Let’s consider speculation and arbitrage, and look at what it really means when the cobasis is deeply negative, in that light. This is the case in silver.

Per the definition of cobasis = Spot(bid) – Future(ask), it means either that physical metal is being dumped on the bid, pressing it down, or that people are aggressively buying futures, thus lifting the ask in that market.

The price of silver has been falling all year, with a sharp correction in the first three weeks of August. The cobasis has been low and/or falling most of that time (though it has come up a little in the past few weeks). We suspect that both market actions are occurring in silver right now. That is, at times silver metal is being dumped in quantity in the spot market, and at other times paper silver is being bought aggressively in the futures market.

Who might be selling physical silver? The data does not tell us, but looking around at the world economy, we can guess that smaller inventories may be needed at manufacturers of electronics. People may be bringing their metal to “cash4gold” companies to get dollar cash to pay their bills. For whatever reason, in the world of the physical stuff supply is coming to market. In contrast, the demand for the paper stuff—futures—is still strong at the moment.

Readers may have a different experience—we would love to hear about it—but we see continued optimism in comments on investor sites, Facebook groups, etc. Surely, “the bottom is in” and as the prices of the metals takes off once again, silver will rise faster than gold.

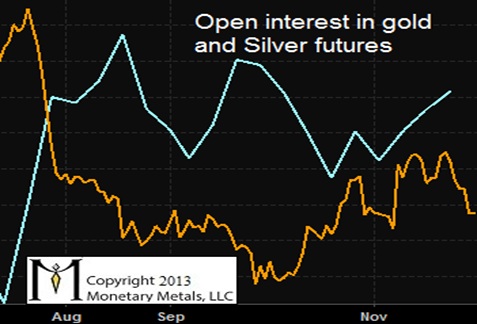

As we have written before, analysis of the open interest in COMEX futures is not so simple, but in the context of the present discussion it is interesting to take a look at the open interest for both monetary metals.

The Open Interest of Gold and Silver

The graph supports our theory that leveraged speculators (which comprise a large percentage of the change in open interest) have gotten much more excited about silver since July. By contrast, the graph suggests that they are less exuberant about gold.

Thus we have a much higher cobasis in gold at this point. The question is: will demand for silver turn around first, or will leveraged speculators capitulate first?

We would not bet our money that it will be the former.

This week was punctuated by the major American holiday, Thanksgiving. Volumes were lighter than normal and liquidity less. We take with a grain of salt both the price moves and the basis moves. The prices ended up slightly on the week.

Here is the graph of the metals’ prices.

The Prices of Gold and Silver

We are interested in the changing equilibrium created when some market participants are accumulating hoards and others are dishoarding. Of course, what makes it exciting is that speculators can (temporarily) exaggerate or fight against the trend. The speculators are often acting on rumors, technical analysis, or partial data about flows into or out of one corner of the market. That kind of information can’t tell them whether the globe, on net, hoarding or dishoarding.

One could point out that gold does not, on net, go into or out of anything. Yes, that is true. But it can come out of hoards and into carry trades. That is what we study. The gold basis tells us about this dynamic.

Conventional techniques for analyzing supply and demand are inapplicable to gold and silver, because the monetary metals have such high inventories. In normal commodities, inventories divided by annual production can be measured in months. The world just does not keep much inventory in wheat or oil.

With gold and silver, stocks to flows is measured in decades. Every ounce of those massive stockpiles is potential supply. Everyone on the planet is potential demand. At the right price. Looking at incremental changes in mine output or electronic manufacturing is not helpful to predict the future prices of the metals.

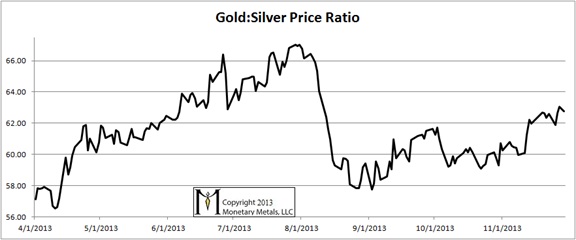

Here is a graph of the ratio of the gold price to the silver price. This shows how many ounces of silver one needs, to buy an ounce of gold. There was a small gain in the ratio this week.

The Ratio of the Gold Price to the Silver Price

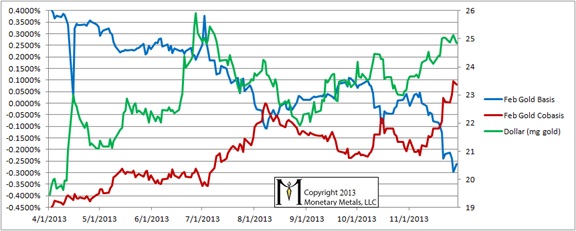

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide terse commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph. The February cobasis flirted with backwardation this week.

The Gold Basis and Cobasis and the Dollar Price

The rising cobasis, now in backwardation, combined with a basically flat price of the dollar—just under 25mg—means that some selling of gold futures is balanced by buying of gold metal. There is nothing extreme in this graph, and as we noted above, volume and liquidity were not normal this week, especially the latter part of the week.

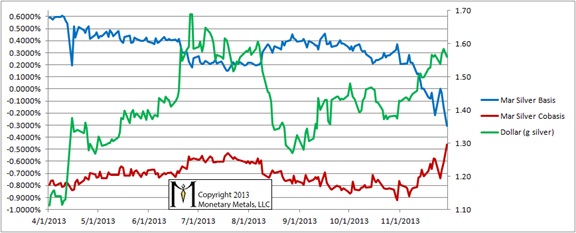

Now let’s look at silver.

The Silver Basis and Cobasis and the Dollar Price

We see a sharp rise in the cobasis, though it’s impossible to tell if this is just the poor liquidity or if this is the start of a major move (the move is not pronounced in farther-out futures). This bears monitoring in the coming week.

© 2013 Monetary Metals

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.