This Is Not Your Eighties Stock Market

“Among other things, these dismal employment ratio numbers tells you why the Wall Street patter about PE multiples being at or below historical norms is so wrong-headed. The capitalization rate for the American economy should be falling because the dependency burden faced by workers and entrepreneurs is soaring at rates never before witnessed…what is really embodied in today’s report is more evidence that America’s dependency ratio is still rising and that the already crushing burden of the welfare state will weigh ever more heavily on an economy that is visibly failing…Yet as the burden of taxation and public debt resulting from these trends weigh ever more heavily, it leaves the mad money printers resident in the Eccles Building stranded in an impossible corner…Unless they wish to destroy the monetary system and keep money market rates at zero forever, they will have to normalize interest rates. And rising interest rates [means] 300-400 basis points at minimum…In that context, capitalizing S&P earnings at 20X reported profits on the eve of the coming storm is a fool’s errand. And you can look it up.” David Stockman’s reaction to Friday’s employment report

With regards to the “dependency ratio” he means the number of people of working age that are not working compared to that quantity in 2008. It has grown immensely. But I don’t want to steal David Stockman’s thunder. His analysis of the significance of Friday’s employment report is first class and everyone should read it. After reading it you will not be surprised about why the stock market gave up Friday’s gains early this week, and why the Fed is in no hurry to normalize anything let alone rates.

Let me restate that last part. ESPECIALLY rates.

The bulls drove stock prices up hard on Friday in reaction to the report, threatening to end the malaise that took over the month. It was not to be, at least not yet, but in their drunken arrogance they could not resist kicking gold while it was down by piling on record short positions in order to break it down, like silver. They pushed hard; driving gold prices to their $1180 support level hoping to get the final hold outs to throw in the towel. It may seem a bit irrational to short a buyers’ market at its four year low but not if you have a blank check! -Or if you are trying to shake the tree for a lower re-entry point?

Although the weak hands are all gone, the length and depth of the post 2011 downtrend in gold and the commodities markets has weakened even the strongest hands, many of which are worried now that we may be going to $1000, or $900, or worse before resuming the bull market -who knows when.

The Ned Davis Seed

An potent aspect of the now failing bear raid in gold was the Ned Davis call for the metal to possibly revisit $660, which was announced only a day or so ahead of the employment report (coincidentally?).

Here’s the actual video with Davis’s analyst, http://video.cnbc.com/gallery/?video=3000316674.

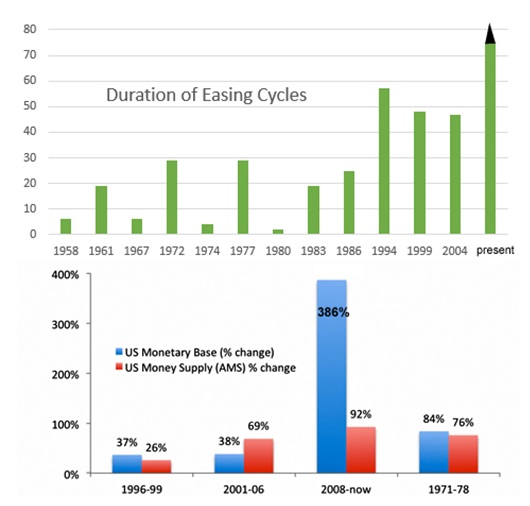

His premise was a comparison of the current environment to the 1980’s, the end of the last commodity bull market, borrowing a chapter out of the Goldman Sachs case for lower gold and commodity prices – i.e., improving economic growth and higher “real” bond yields. But this economy is nothing like then.

His premise was a comparison of the current environment to the 1980’s, the end of the last commodity bull market, borrowing a chapter out of the Goldman Sachs case for lower gold and commodity prices – i.e., improving economic growth and higher “real” bond yields. But this economy is nothing like then.

The 1980’s economy was the product of a Fed that abandoned the exact policy that it is pursuing today without abandon. It is the exact opposite!

The 1978 Fed let the rate of interest go – it let the market determine the right or natural level – and stopped printing money. Importantly, it was willing to tolerate the deflation and allowed the malinvestments to clear. Today’s Fed is breaking records in all the wrong ways. Indeed, it doesn’t even have the option of doing what the Volcker Fed did in the late seventies anymore.

What Mr. Stockman doesn’t concede in his analysis is that the Fed can no longer afford the luxury of saving the monetary system if it wants to forestall a government failure. The public debt has grown much larger now and the cost of servicing that debt at higher or normalized interest rates is prohibitive.

The dilemma that the powers face is whether to sacrifice the financial system in order to save the government from default by inflating the debt away or let the government fail to save the dollar.

I’d vote for the latter, which is why you can rest assured we won’t get it!

I could go on about the differences between now and then: how Reagan was voted in on a laissez faire platform and even promised a return to sounder money (even if it was a ruse) whereas Obama has promised to give everything away and is taking us down the road toward greater central planning.

Almost everything about the current situation is different than that period. The differences are so stark I’m amazed anyone would even believe the comparison. At any rate, it was a good set up for Friday.

There is no question that the current boom is unsound because of its reliance on central bank policy.

While the policies they Reagan pursued in the 1980’s were not sound, the period leading up to his election included a massive cleansing of imbalances that put the economy on sounder footing.

If Americans elected a conservative or laissez faire president in 2012 instead of a socially progressive democrat, and they spent the last two years privatizing industry (instead of socializing it) and letting interest rates find their own natural level things would be different. But since this is not the case then we can only conclude that Davis’s analyst has been drinking too much out of the Fed’s punch bowl.

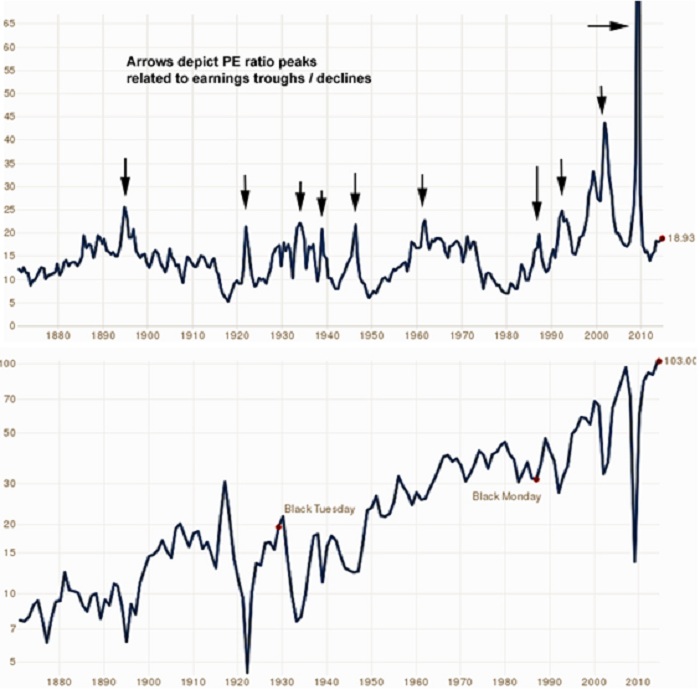

The Stock Market is NOT Trading Below Historic Norms

In the graph below I want you to take note of the S&P 500 PE ratio calculated back over 100 years by Robert Shiller. The average PE ratio is 15. If you take out the peaks that occur due to outsized drops in earnings that number falls a point or two. Today it is close to 19x for the S&P 500 and 16x for the Dow Industrials, and over 20x for the other averages –Transports, Utilities, Nasdaq, etc. Excluding the late nineties tech bubble, that is about as high as it has ever gotten with earnings still growing.

Records have been set in terms of the price/sales ratio as well.

The “capitalization” rate that Stockman referred to is basically the PE ratio. He is saying that since the labor participation rate is so low the PE ratio should be lower. Another reason he thinks the PE ratio should be lower is that it should reflect normal interest rates, which he would estimate at 5-6 percent on the 10yr note. In my analysis of the equity risk premium I believe that the market has factored in a bit of an increase in yield, say to about 4 percent, but it would not like Stockman’s guess so much.

The post 2008 recovery in the stock markets is almost 66 months old now. It has been the best and strongest rally since the 1994-2000 Bull Run, and only a few points short in terms of that extent – the equivalent would be if we were at Dow 20000 by now, hence we are a bit short. Certainly the nineties should be a tough mark to beat. Many things went right for the American economy in that period.

But this market is nothing like those of the eighties and nineties.

This market is a complete and utter charade.

It is propped up by the most massive manipulation in interest rates and asset values in history. Bond yields have not been this low and have not seen this much intervention since the fifties and sixties!

The Psychology of Our Predicament

In every case, historically, it has always ended the same way, even when the boom was initially on sounder foundations –which it definitely is NOT today regardless of how often they repeat the word “goldilocks” on bubble tv. Certainly it’s always easy to pick a top with the benefit of hindsight.

But in the heat of the moment the security of the crowd is often more comforting.

It is a survival instinct. We huddle in with the crowd, hoping perhaps that the sharks pick off the wounded contrarians at the outer edges…those straying from the mean. Unlike other animals, we are endowed with the ability to think for ourselves but when fear (or greed) enters the picture it is not easy to think clearly, and instinct takes over. One of the aims of a risk management strategy is precisely to help investors check those emotions at the door so they can make rational decisions in the heat of the moment. If you are worried about this bear raid in gold then you likely have too much exposure or leverage and should take steps to reduce it. The cost of this move is that you will be giving up some of the early gains in the higher beta stocks at the outset of a turnaround. The upside is more sleep.

But I’m not too worried. Sure, we could still be off. I continue to maintain that the worst of it is behind us, and even if we went to $1000 hindsight will count that call correct when the bull market returns.

Extreme market conditions such as these don’t happen often but when they do they are always difficult to manage because they test the boundaries of our expectations and also convictions.

In my 25 years I have seen these extremities maybe three times: 1999, 2007, and now.

They are never easy. In the US market my career has spanned four periods where the stock market has traded at current or higher levels. But this is the only time in my life I have ever seen bond yields pushed to such extremities that, as Stockman notes, they are fooling stock investors too.

Market Outlook

The bounce off of 1180 support was solid. I liked it. I’m not sure we’re out of the woods yet, but it was encouraging. It was distressing to see the market give up almost all of its overnight gains Wednesday in one quick volume-less trade just ahead of the announcement of the minutes of the last federal open market committee meeting (mid September). A cynical client remarked that Goldman wanted to load up. What makes it worthy of mention is he said that to me before we found out what the FOMC said.

The upshot was that the Fed was worried about the strength of the dollar and the weakness of the global economic landscape, which everyone took to mean that rates wouldn’t be normalized quickly.

That’s the Fed essentially telling other central bankers to pony up.

But the dollar comment was interesting. The Fed almost never remarks on that. Bad sign for dollar bulls if they thought that Yellen views dollar policy like Greenspan. It is interesting to note also that the FOMC news generated a buy everything signal, causing gold to rally along with the stock market.

In recent weeks I had started to think it was going to turn into a safehaven trade instead of a dollar trade, but this might have changed that up, or it might simply have added fuel to that fire.

There were encouraging signs in some of the softs this past week boosting our DBA etf; but energy, wheat, silver and platinum prices have weighed heavily on the commodity trade, and hence gold.

I think the softs, metals, and the grains are oversold but a case can be made for lower energy prices in the short term, which would no doubt provide some relief to Wall Street – with bond yields ratcheting higher again, and equity valuations so stretched – and may continue to weigh on the gold/silver trade.

Silver in particular is worrisome, having broken down from a descending triangle implying a $15 objective. It may be no consolation to hear me say that would be one helluva buying opportunity.

But it is true.

At any rate, if the reversal in the USD continues lower here and the ECB steps up its own money printing that may all become moot. We’ll have to see. But we are positioning ourselves now for the next bull market leg in the precious metals. When this market turns it will go higher than anyone currently thinks. The bullish extremes of the Dow are easily matched by the bearish extremes in gold.

********

Subscribe to the premium letter to access my recommendations in this sector.

(Source: Ed Burgos: www.dollarvigilante.com )

Ed Bugos is a mining analyst, investment banking professional, and senior analyst at The Dollar Vigilante (an online guide to surviving the dollar crash), with more than 20 years experience in the investment business advising clients on portfolio and trading strategies.

Ed Bugos is a mining analyst, investment banking professional, and senior analyst at The Dollar Vigilante (an online guide to surviving the dollar crash), with more than 20 years experience in the investment business advising clients on portfolio and trading strategies.