Post-FOMC Contrarian Window Open

The time is now for the broad market rally to gain a following

It’s a bear market. The trends make that assertion, not me. But as noted in an NFTRH update on July 28th…

FOMC came. FOMC laid a .75% egg. FOMC rode off into the sunset until September. Meanwhile, signs of global economic contraction continue to crop up as the Fed fights the last war.

And…

The favored strategic play has been that the Fed drops its July rate hike on the market and may be done. However, if ‘inflation trades’ like commodities and signals like inflation expectations, Treasury yields and the Silver/Gold ratio rise strongly enough it may compel the Fed to hawk again. That remains to be seen. But there is a window now. That window is July 27 to September 21, when the micromanaging market regulator eggheads meet again.

NFTRH has well anticipated this window, for which the July FOMC meeting would serve as a pivot point between a grinding attempt to put on a bear rally and the genuine article, which would rally enough to create FOMO (‘fear of missing out’ for those not accustomed to jargon) among the market’s 2022 bear refugees.

Following are quick status views of various asset groups.

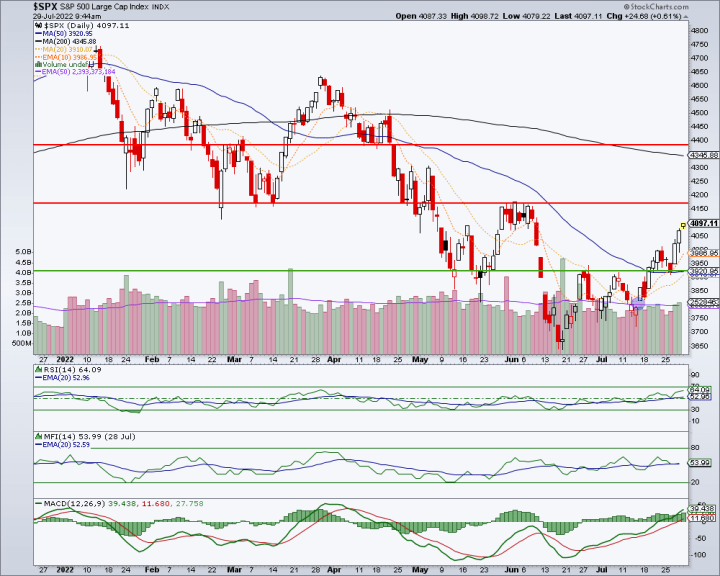

US and Global Stock Markets

Trends down, bounce in progress since mid-June in the US and on balance globally since mid-July. Using a daily chart of the world’s most watched index, SPX as a general guide we note:

- The major trend marker (200 day moving average, black) having turned down.

- As long as SPX remains below the SMA 200 it’s a bear rally only.

- You can see the objectives NFTRH has had in play by the red resistance lines.

- RSI, MFI (Money Flow Index, which thanks to a ping from subscriber Mike C I’ve added to charts that include volume) and MACD are positive and not overbought.

- Market sentiment had generally remained over-bearish (contrary positive) despite the weak bounce into FOMC week. Along with market prices however, sentiment is no longer a no-brainer.

- Within a bullish short-term projection some sectors are better than others. These distinctions are reserved for NFTRH, but think about bonds and sector correlations to them. It matters.

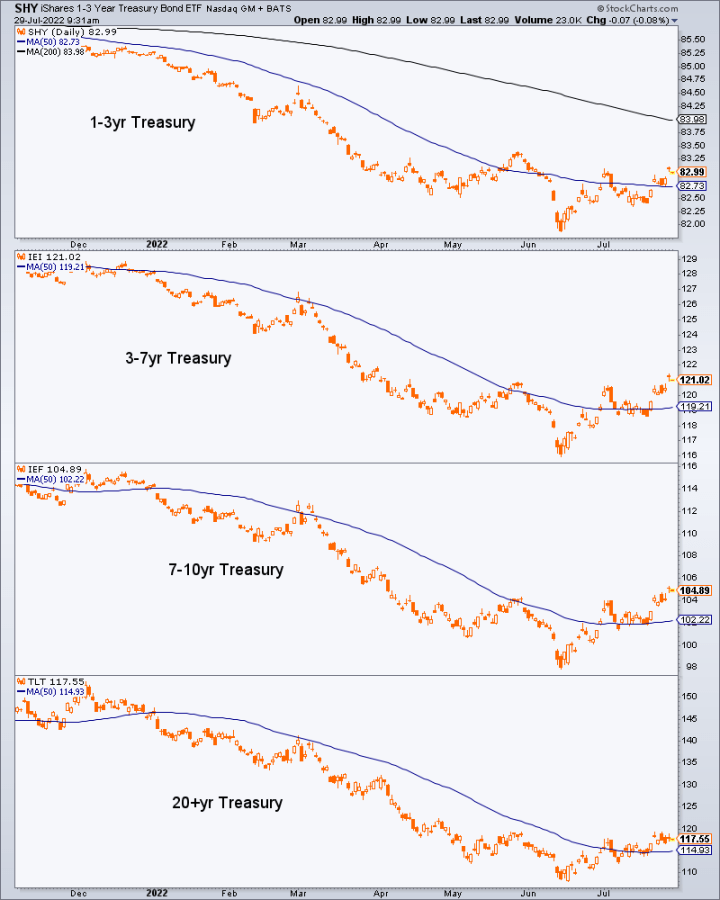

Bond Market

Speaking of which, here is the chart we have used to manage a bottoming process for the contrarian play now engaging. You can see that mid-June was peak inflation hysteria, which drove Treasury bonds to a downside blow off.

Since inflation and the fear of a hawkish Fed (which has taken its cue from rising interest rates) have been the primary fears and hence, bearish inputs for the market in 2022 the opposite, a temporary ‘Goldilocks’ phase can rise out of dis-inflationary relief (one helpful hint is that the Yield Curve, e.g. the 10yr-2yr, is flatter than a pancake in its inversion).

While the fine tuned work here will also need to be reserved for NFTRH, much like a potentially strong rally for SPX above can continue, so too can one in bonds. There may be a hard limit to the festivities, however. Flipping the situation over to its yield view (30yr), you can probably ascertain the caution area per this July 22nd post.

Assuming the rallies in stocks and bonds play out to targets, all bets are then off. These ‘bets off’ will likely register before the next FOMC meeting on September 21.

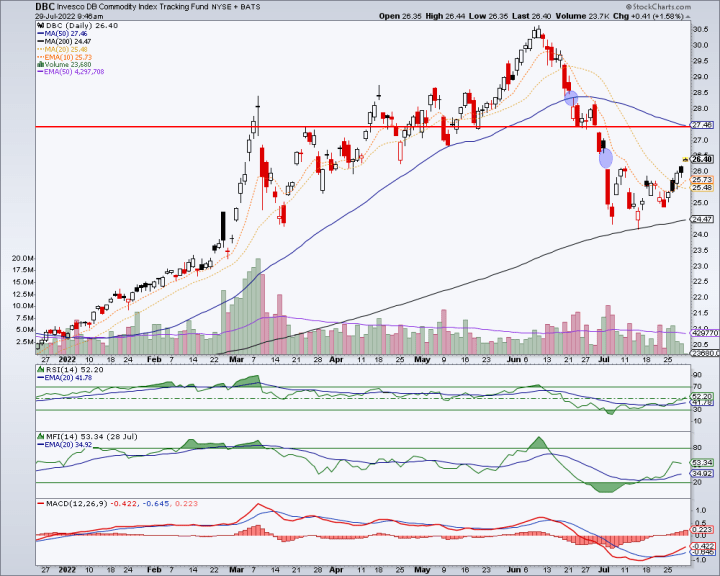

Commodities

Previously correlated to rising long-term yields, commodities finally cracked in the face of intensifying inflation and by extension the hawking Fed, as expected. But they too can be part of the relief trade, although they are not a ‘Goldilocks’ asset class. So pick and choose your commodities carefully.

CRB tracker DBC found support at the uptrending SMA 200 and as such it is indicated to be a healthy correction as the inflation problem that everybody (the public is quite pissed about inflation, after all) knew was in play finally cracked under the weight of the hawking Fed, which did what it had to do (as directed by the bond market) to keep the public mobs with pitchforks and torches at bay.

DBC will probably fill the lower gap but has an important test at the now down-sloping intermediate trend marker, the blue SMA 50.

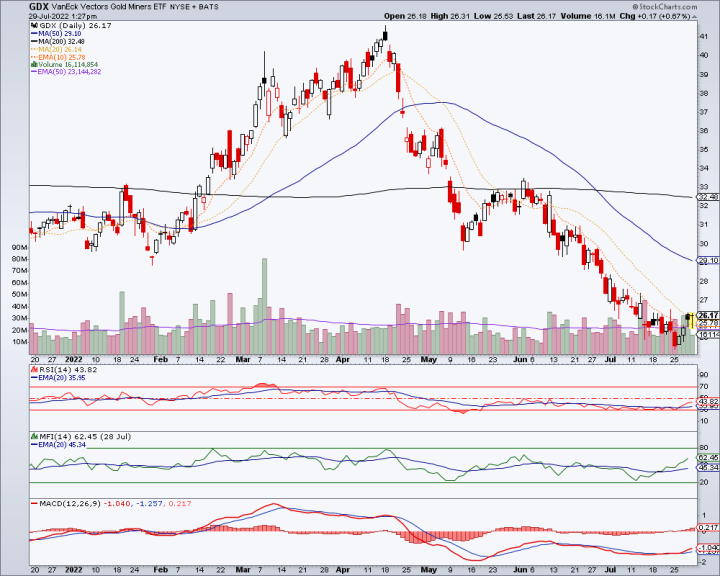

Precious Metals

Okay my buggish friends, easy now. You are not special. You are due for relief as well, but the macro market backdrop has only made a partial macro-fundamental move in the right direction. ‘Market relief’ is not a good fundamental underpinning for gold or gold stocks. Nor is ‘Goldilocks’.

I’ll say again as I have said all along since the correction was indicated to begin in August, 2020 that gold is not really about inflation and gold stocks are almost never about inflation (Stagflation could be a wildcard). Indeed, I’ve been parroting that same notion for the last 18 years to mostly deaf and naive ears. So much so that I am tired of it. Let the herds run as they will. I’ll keep the details of the reasoning mostly within the confines of the NFTRH service from here on.

Of course, with deeply oversold readings (e.g. Gold Miners Bullish Percent Index), the positive seasonal window and sentiment readings in dumps (one example being the stellar contrarian Commitments of Traders in silver) the precious metals can surely tag along. In fact, we have been noting the bullish risk/reward state of silver in NFTRH for weeks now.

With earnings season upon us there have been some good results, some poor results and on balance, a sector that has been sold down hard. Some bullets:

- Stellar Commitments of Traders (CoT) setups for gold and especially silver.

- As we have tracked consistently in NFTRH, along with silver’s epic CoT setup it also happened to be on very clear long-term support, which we micromanaged heading into FOMC week. SLV is my largest (paper) precious metals holding and given the way silver can move, my only silver holding. Who needs the volatile stocks and their political/execution risk when you can hold the volatile metal? ;-)

- Side note on silver: the ‘no brainer’ aspect of a silver bottom at long-term support is already in the books, so don’t go chasing without that understanding.

- A seasonal window bottoms in July (on average) for gold and silver. It is a low for the year in gold and only a temporary one for silver. Remember that seasonals vary in any given year. But it’s an input for consideration.

- Terribly over-bearish sentiment has been implied by the CoT and the very oversold BPGDM, gold stock indexes and many bombed out individual stocks.

- However, we are operating to lower targets, pending the contrarian macro relief window playing out first.

This is not to say that the precious metals cannot be distinguished as unique in the coming weeks, but at this time they are nothing special and you should let no gold promoter try to convince you otherwise if/as the sector rallies along with other more cyclical sectors. For reference is last week’s article: Gold Bug survivors prepare to capitalize

It could be time, but the July-September window is going to fill in a lot of blanks to the analysis. My firm lean at this time is that this is not THE rally in the precious metals complex and Monday’s low may not have been THE low. Again, only forthright and consistent work will answer the question.

Meanwhile, here is a daily chart of GDX whereby you can see a rally just getting underway as the price thus far holds above the short-term EMA 10 (orange dotted line). If that holds and it takes out the EMA 20 (gold dotted) the trend down from early June will have been broken. We will manage upside bounce targets accordingly.

Wrapping Up

Meanwhile, enjoy the remainder of your summer. If all stays to plan the terrorized 2022 sentiment profile was due for relief across many sectors. The Fed is done until September and market and economic events in the interim will dictate their stance when they return.

Labor Day seems like a good time frame to key on.

There are two very possible options. Goldilocks is going to either give way to a new and worsening inflation or a brand spanking new deflationary episode if the 2020 inflationary operation resumes unwinding, whether or not the Fed flips dovish. That by the way would be when you might want to be very interested in buying a gold stock sector low. Most will not be. The majority would be running again in tow behind their inflationist leaders.

---

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by PayPal or credit card using a button on the right sidebar (if using a mobile device you may need to scroll down) or see other options. Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.

********