The Relentless Road To Recession

“Show me the data,” demand those who cannot see a recession forming all around them and who keep parroting what they are told about the economy being strong because it is what they want to believe; yet, the data look like an endless march through a long summer down the road to recession.

And that is what you are going to get in this article, a seemingly endless parade of data along the recessionary road. This is for the data hounds.

As we end the summer of our discontent when few would deny that most economic talk turned toward recession and, as we begin the time when I said the stock market appears it may fulfill my prognostication of another October surprise, it’s time to lay out — again — the latest data that support my summer recession prediction. We’ll have to wait until next year for the government to officially declare a recession if one did start in September. (Yes, September is a summer month.) In the meantime, the data stream is a long line of confirmation.

I’ve been reminded that extraordinary claims (such as the recession declaration in my last article) require extraordinary proof, and I agree. After all, no one else is saying the recession has begun, though a small number of economists have said it might be happening now. For everyone’s benefit, but especially for those who refuse to give up their own unsupportable and, yet, undying belief that the “economy is strong,” here are the facts on parade.

Pardon the length of the article because I fully intend to overwhelm you with evidential support of my “extraordinary” claim in order to strip off the economic blinders by shear preponderance of evidence. After all, recessions are circumstantial, and circumstantial argument in court of law requires a preponderance of evidence. So, particularly for those who have said, “show me the money,” here is a barrage of data so obvious that I wonder how anyone has missed it all.

(I also know from experience that, if I only present a few major pieces of evidence, those who want to deny how truly bad our economy is will say I am just cherry-picking the data. On the contrary, while you can reasonably pick over various pieces of data below for how reliable any one piece is (as is usually the case in economics), the overall stream is broad and deep across all sectors of the US economy and has been for months! In fact, most of the data have gotten worse from one month to the next … with no sign of its downward march relenting.)

Manufacturing a recession

The biggest evidence that we began entering recession came from the IHS Markit’s Purchase Manager’s Index (PMI) which showed early in the summer that manufacturing had slid into recession. “Not to worry,” wrote almost everyone at the time. “Manufacturing is less than 20% of the US economy, while the services sector is holding strongly above recessionary levels. Plus consumer sentiment is strong, so it will carry us through this manufacturing slump.”

These were desperate pleas by bulls doing all they could to maintain their bullheaded denial and to support their stock-selling pitches or stock-buying euphoria. Let’s examine their claims.

To the contrary and completely against the media flow, I claimed that the services sector would join manufacturing soon (so take off the rose-colored glasses) and so would consumer sentiment. The latter, I’ve noted in the past, is more of a lagging economic indicator than a leading indicator. Consumers have to feel the pain or sense plenty of reason to be afraid before sentiment turns and starts to change buying decisions.

Manufacturing continued to “slump” throughout the summer to where the ISM Factory Index has now hit a ten-year low (at 47.8). That is so low it takes manufacturing back to its low at the start of the Great Recession, reflecting …

a continuing decrease in business confidence. September was the second consecutive month of PMI® contraction, at a faster rate compared to August…. The New Export Orders Index continued to contract strongly…. Consumption … contracted at faster rates … primarily driven by a lack of demand.

Institute for Supply Management

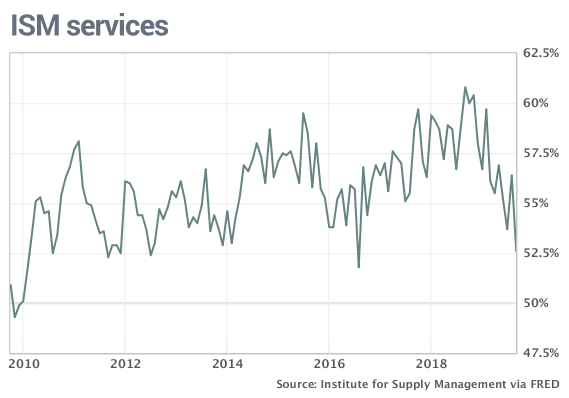

Services no longer serving investor denial

Late in the summer, the US Services sector did as I said it would and cut off its engines to enter a glide pattern, falling from 56.4 in August to 52.6, still above the neutral 50-point level. (Anything below that is considered recessionary.) However, that low altitude was well under economists’ radar, who expected only a slight decline.

Other than an anomalous blip down in 2016, this is the lowest the services gauge has hit since we were just climbing out of the official part of the Great Recession. The descent was surprising enough that it took the NASDAQ and Dow down for a brief intraday touch-and-go, bouncing off the tarmac at the elevation of their 200-day moving averages.

If you look at their steep trajectory in the services industrial sector, it looks more like a nosedive than a glide toward a smooth landing:

“Look out below is what purchasing managers from services industries are shouting at the markets as the fears of recession continue to mount,” MUFG [Mitsubishi UFJ Financial Group] chief economist, Chris Rupkey wrote in a note. “This downturn is starting to spread….“

The dour news took the 2-year US treasury yield down again to its lowest in two years.

U.S. Treasury yields slumped Thursday after an indicator of service sector activity suggested a key pillar of the American economy may be more vulnerable than thought…. Thursday’s data could suggest cracks are forming in a foundation of the U.S.’s expansion.

The ten-year treasury also lopped of seven basis points, and the thirty-year cut six.

Just in case you think the above data are off, the IHS Markit services sector purchasing manager’s index for September held steady, but is at an even lower altitude of 50.9, while the New York Purchasing Manager’s Index plunged to actual recessionary levels not seen since we were just entering the Great Recession in both its forward outlook and current business conditions.

Chicago PMI agrees:

So much for the idea that service businesses, which are about 80% of the business economy are holding their heads recession. At best they are right on the border of recession now. At worst, they are well into it.

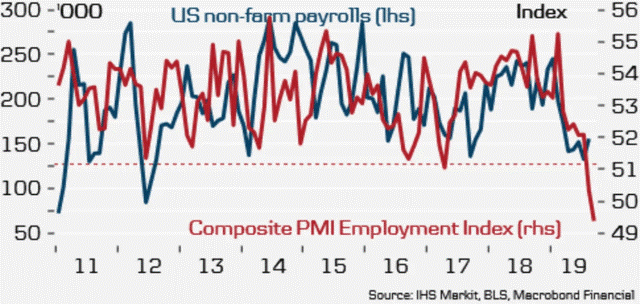

Employment presents equal opportunity for either side of the argument

Speaking of PMI, the employment portion of the indices looks worse than it’s been since we officially emerged from the Great Recession:

That was the ISH index. Joining to confirm, the ISM index now shows …

… the employment gauge dropped to a five-year low of 50.4% — barely above the cutoff point that separates net hiring from net layoffs…. The pair of ISM surveys clearly point to a sharp loss of momentum in the U.S. economy.

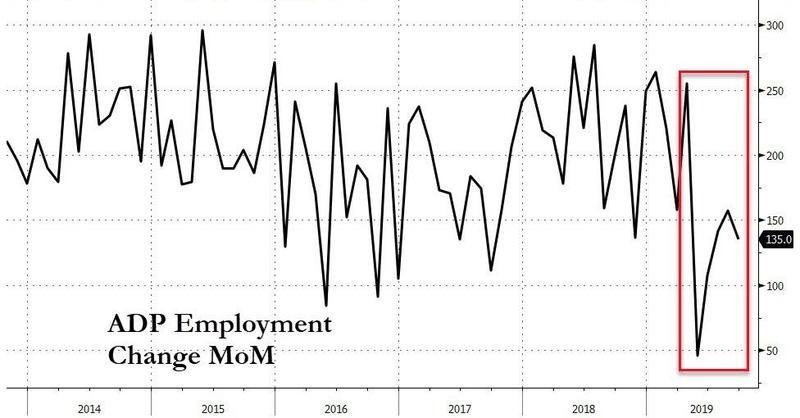

ADP employment stats also just disappointed a little in that, following a severe plunge in the spring, we saw a jump halfway back up during the summer. That, however, is now turning its head back down in a sad nod:

If you want to argue based on how it jumped back up, hold on a minute here with me. Sure it did, and the downturn again was small; but you can see a much larger overall downward arch proscribed by repeatedly lower lows and repeatedly lower highs.

Moreover, if you read here regularly, you already know that the Bureau of Labor Statics (I prefer calling it the Bureau of Lying Statistics because its numbers are adjusted based on optimistic fantasies (almost always in the direction of better-looking results than the raw numbers tell) reported that its “new jobs” reports for an entire year had overestimated new jobs by HALF A MILLION during the prior March-to-March period.

The truth is that “new jobs “have been slightly recessionary for a year

“The job market has shown signs of a slowdown,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “The average monthly job growth for the past three months is 145,000, down from 214,000 for the same time period last year.”

Zero Hedge

As I’ve pointed out below, anything below 150,000 new jobs a month is recessionary because it doesn’t even keep up with growth in the labor pool due to population growth. (Of course, people coming into the labor force who cannot find new jobs are not counted in the headline unemployment number because they’ve never been employed to begin with. So, they cannot become “unemployed” by being eligible for unemployment benefits.

Jobs are now also being cut across the surveyed companies for the first time since January 2010, as firms have become more risk averse and increasingly eager to cut costs,” said Chris Williamson, chief business economist at IHS Markit.

To take an honest look at employment, you need to consider this week’s positive unemployment count in context with all of the above before you make too much of the week’s new low in unemployment. Historically, unemployment only has to go up a very small amount before a recession begins. Like this:

As you can tell, the start of a recession has nothing to do with how low the unemployment bottom goes. All that matters is when the bottom is put in. So, the start of a trough (just beyond the reach of the graph above), fit my recession predictions precisely. Unemployment numbers during the summer turned slightly back up. However, this week, unemployment smacked back down to a fifty-year low at 3.5%. Like this:

That leaves unemployment as one statistic that is again running somewhat against my recession claim, albeit barely because this week’s data run up against the latest new jobs number, too, which was far from impressive, leaving the stock market relieved to believe the Fed will cut rates again in October. The latest flimsy number of 136,000 net new jobs remained below the 150,000 baseline level required to keep up with labor force growth (by which I mean population growth moving up to labor age — the people not counted on the unemployment graph above … like those coming out of college). Economists were expecting new jobs to come in right at that baseline, so the new number undershot already low expectations by about 10%. That is why stocks shot up in hope the pathetic number would assure more Fed easing.

Moreover, we now know that each monthly statistic put out by the BLS has been (on average) about 43,000 too high over the past year by their own admission. (To see how distorted numbers have been in the recent past, you can read these two other articles of mine: “It’s Been a Great Recession for a Few” and “How’s That Recession Coming, Dave?“)

In all, I’d say that leaves jobs looking weak and unlikely to continue supporting a low unemployment rate, but for the moment not fully joining my recession claim either. The Economic Cycle Research Institute agrees that job support against recession is over:

According to our research, the consumer is likely to become more wobbly than most expect. ECRI’s is all about the timing of turning points. January 2019 saw the cyclical peak in jobs growth, and it [the downturn from that peak] is far from over. Both nonfarm payrolls and the household survey year-over-year growth are in cyclical downturns…. While there’s been lots of celebration about the supposedly strong jobs market, just because nonfarm job prints haven’t undershot consensus expectations, people are missing the forest for the trees, which the chart makes plain. Nonfarm payroll growth is already at a 17-month low, and the household survey is even weaker…. And we already know that the top nonfarm payroll line will be revised down by half a million jobs, when we get the benchmark revisions in a few months…. Growth in ECRI’s Leading Employment Index, which correctly anticipated this downturn in jobs growth, is at its worst reading since the Great Recession.

Did you get that? Worst since the Great Recession! (And that’s the one stat that is, for the moment, stubbornly refusing to fully substantiate my recession claim. So, that is no longer much of a counter-argument.)

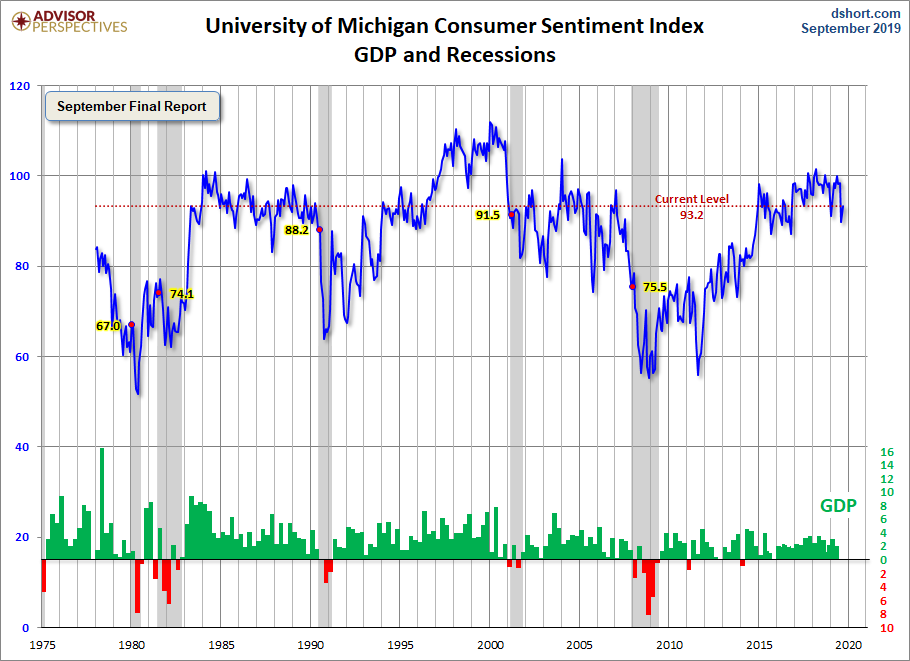

Consumer sediment

Consumer sentiment, which ECRI described above as “wobbly,” has begun to settle, but it, too, is still positive. It may, however, be turning the corner just as ECRI says jobs have. It has a long way to go, however, to catch up with manufacturing’s decline.

Another measure — U-Michigan’s consumer sentiment gauge — shows sentiment floating at the level it has twice in recent years been at right at the opening season of a recession. So, recession have been known to begin at this height:

It appears sentiment could be turning, and sentiment is a slightly lagging indicator, being nothing more than a reaction — a feeling people have about the economy. Feelings don’t change until the climate around us begins to change. You don’t feel a chill until the temperature starts to fall.

Notice in the graph above that recessions start as soon as sentiment puts in a top, and then sentiment falls like a rock to the bottom of the river as soon a recession begins. It looks evident to me that the top is in.

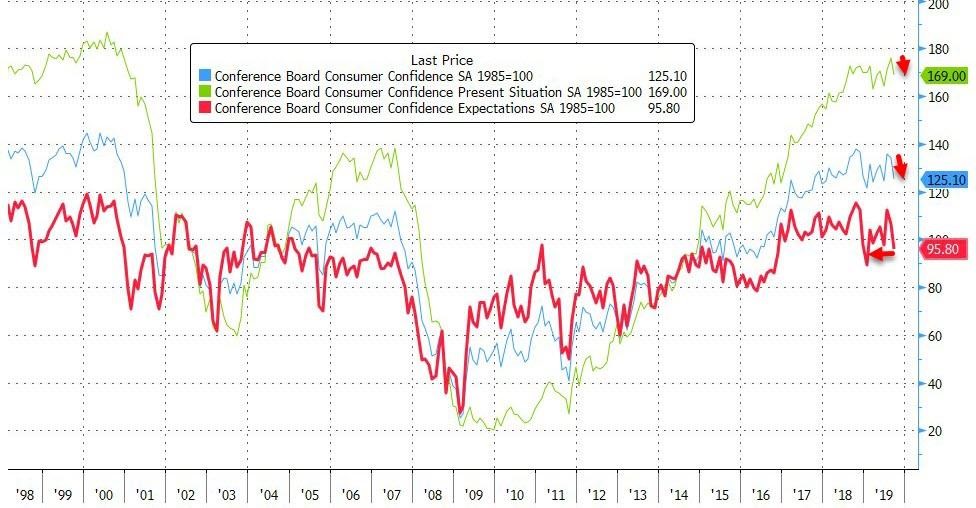

By another measure, however (the Consumer Confidence Board), the last time consumer confidence fell this much in the last three years was last December when stocks crashed more than 20%:

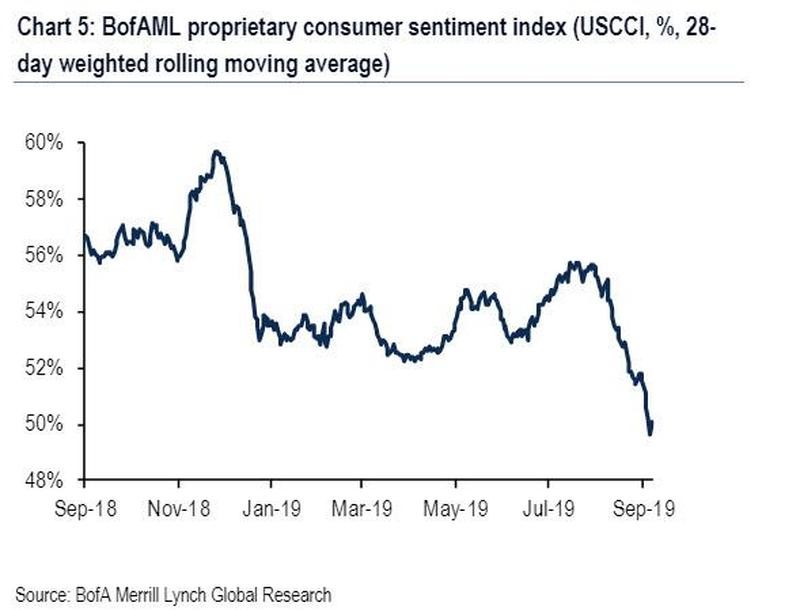

And here is one more particularly graphic measure of consumer sentiment’s decline for a preponderance of evidence:

So much for summer’s rosy idea that the service sector and consumer confidence would pull us through the already-begun manufacturing recession. Notably, in that respect, consumer purchasing plans have already declined for homes, cars, and large appliances.

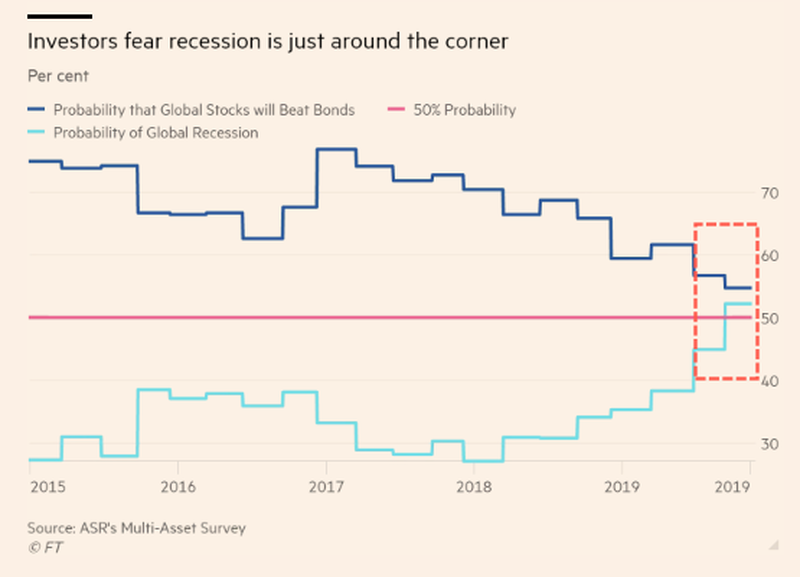

Of course, we know the stock market has been completely divorced from economic realities for a long time, so how about investor sentiment?

Not much better.

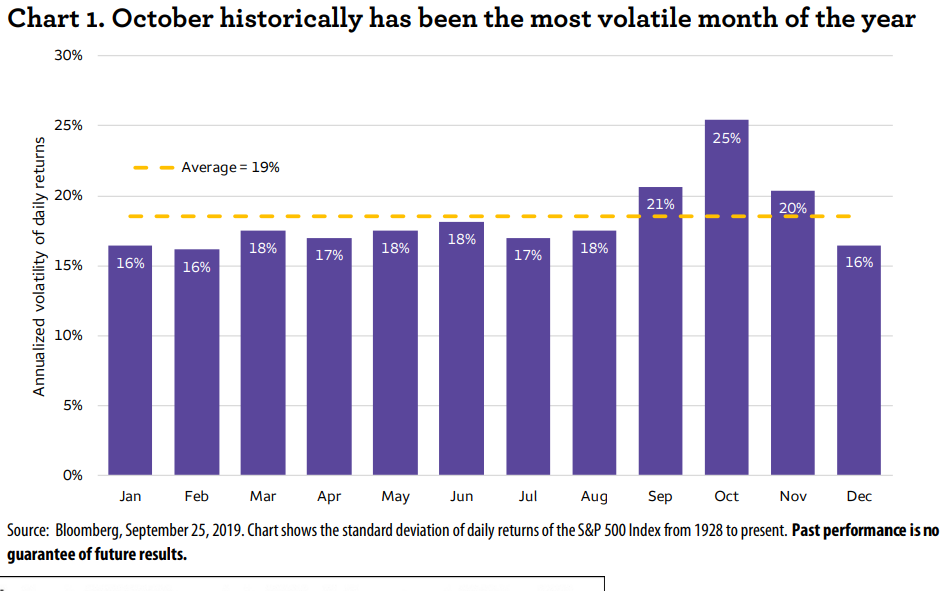

October surprises with a bang

October is known for delivering chilling surprises in the US stock market? I’ll let a picture suffice:

While it is too early to know how far down this month’s riotous first week in stocks will take down the temperature, this October had its worst start to any quarter since the start of the Great Recession. The first-week plunge hit hard enough to blow up Wall Street’s Fear Index in what could be its biggest pop on record:

The Cboe Volatility Index … a gauge of bullish and bearish S&P 500 options bets that tends to rise as stocks fall, was on pace for its biggest rise to a quarter on record. The so-called fear index was up about 29% in the first two days of October, which would eclipse the 24.58% gain for the index back in the fourth quarter of 1992.

By mid-week, all major US indices had broken below their moving averages:

So, even though we don’t know yet how big October’s surprise will turn out to be, it began by busting some records in a start that trumps the start of last year’s big autumn fall.

Already considered an unusually volatile period for the stock market, which has logged historically ugly October declines in 1929, 1987 and 2008, worries about geopolitics and growing signs of domestic and international economic weakness have fueled bearish bets and sent stock-market optimists, at least momentarily, scurrying for cover in assets perceived as safe.

In September, Morgan Stanley’s chief equity strategist Michael Wilson took us back to last October as he described the chill he feels in the autumn air:

As we head toward the end of the third quarter, I can’t help but think it feels very similar to last year in many ways… The S&P 500 is near its all-time high at 3000, while the MSCI EM Index and the Topix sit 20% and 15% below their highs and the Eurostoxx is 7% lower, leaving all these indices exactly where they traded a year ago…. Long-duration sovereign debt has been the best investment by far over this period, with 10-year Treasury yields 50% lower than just 12 months ago. To put this into context, over the past 50 years such a dramatic move in yields over the prior 12 months has only happened twice – during the global financial crisis in 2008 and the European sovereign debt crisis of 2011-12.“

And this week, treasuries all reinforced September’s move by retrenching to those lows.

Wilson concluded,

We’re moving from the perception that this is late-cycle to a belief that it’s end of cycle.

JPMorgan’s Nick Panagirtzoglou feels the same concerns rising around him:

One question we are often asked by our clients is about the similarities and differences to last year…. Could last year’s correction be repeated into the fourth quarter of this year?

After laying out numerous nearly identical data comparisons, Panagirtzoglou notes a key difference:

But there is no doubt that the most important difference to last year is that central banks are now easing policy via both rate cuts and quantitative measures rather than tightening which was the case during 2018.

I have noted graphically in previous articles, however, that Fed rate cuts always start just before the start of a recession and then follow it all the way down. So, a pattern of needing to continue rate cuts means the first cut or two were not insurance cuts but fit exactly the pattern at the start of ALL recessions. And, as Panagirtzoglou indicates and as we’ve all seen from September’s bursts of QE-sized flash cash, the Fed is clearly trapped on a course or rate cuts.

As even Panagirtzoglou admits,

The idea that central banks easing can prevent an equity correction from taking place is facing several key, and increasingly growing challenges.

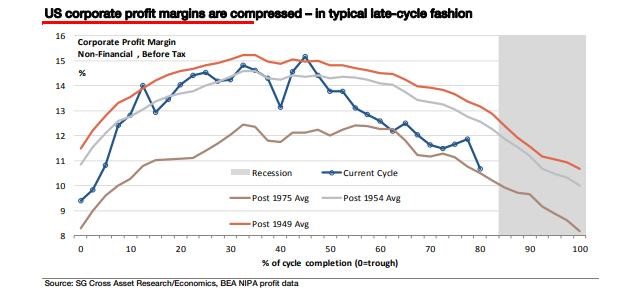

And why should stocks get better? Look at where corporate profit margins currently sit relative to when recessions typically begin:

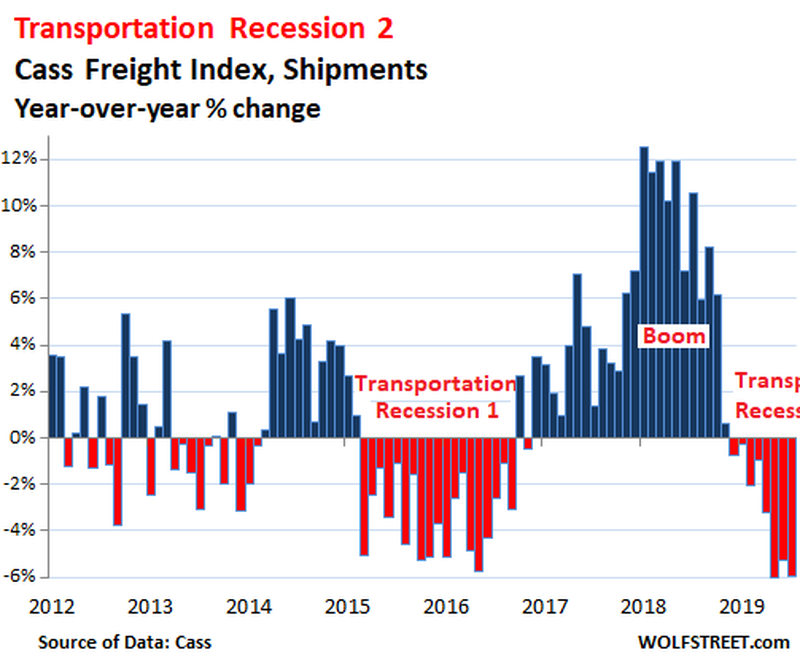

Transportation stocks are seen as leaders because any slowdown in any sector of the economy slows transportation. Trannies had been going down all year, but started to improve ahead of the stock market’s October downturn. After a brief turn back up, however, they have returned to their downward road with the rest of the market. The trainee decline during the summer resulted in the carnage of 4,500 truckers losing their jobs just in July and August. A year ago, companies couldn’t hire enough drivers to keep up with rapid growth. Now it seems they cannot fire enough.

That all looks like this:

Not a pretty picture.

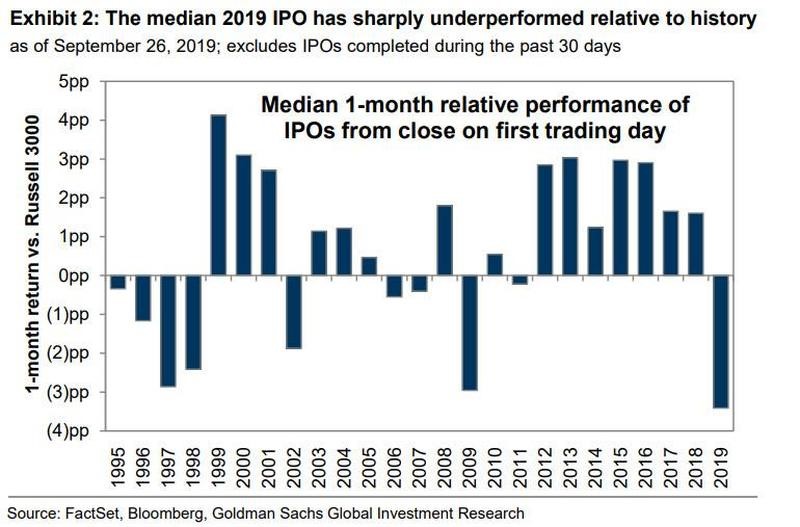

IPOops

One particularly interesting kink in the stock market’s fall has been the failure of IPOs by snazzy companies that make no money. 2019 is looking like it could be the worst year for Initial Public Offerings in history. Spectacular fails like WeWork and Peloton have led to much reminiscing about the dot-com bust.

How bad is it?

Goldman, one of the largest beneficiaries in this arena, has an answer:

In other words, IPO performance is worse so far than the dot-com bust days or any year on record. That’s the median of returns, not total returns, so the remaining months of the year could move the median up or down. Regardless, it sucks like a drain hole at the bottom of investment banks, which have seen their revenue streams flushing away along with their stocks.

Eulogizing, Morgan Stanley’s Wilson says,

It was one heck of a run, but paying extraordinary valuations for anything is a bad idea, particularly for businesses that may never generate a positive stream of cash flows…. The problem is that some stocks in the public markets still need to fall back to earth, and they reside in the secular growth category.

Insanely speculative money is drying up … at least in the non-profit for-profit sector. Uber’s not so uber anymore, and Lyft has lost its lift, and many companies that were about to have their own IPO parties are walking away in the sudden drought of investors.

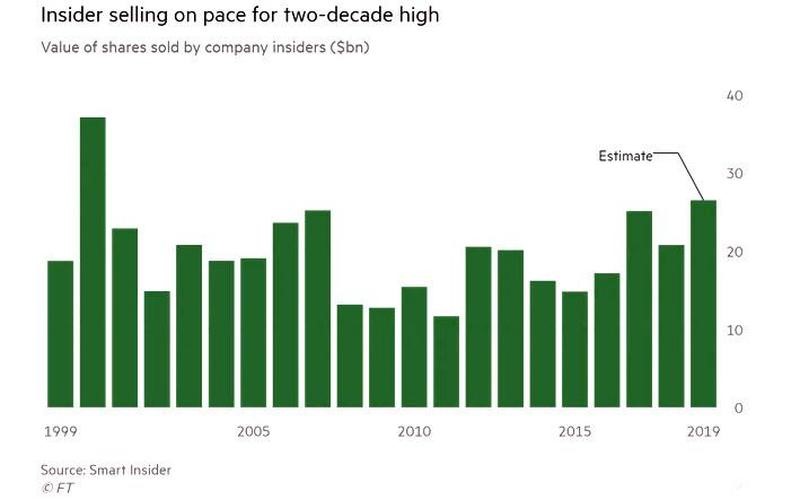

Insiders stepping out

In another sign of the times, the insiders are walking away from their own stocks, too. Stock buybacks are being used to cash out corporate executives in a flow that makes a twenty-year high.

Who knows better if their stocks are overpriced than those who float along at the top? So, it should be concerning when you see …

“executives across the US are shedding stock in their own companies at the fastest pace in two decades, amid concerns that the long bull market in equities is reaching its final stages … which would mark the most active year since 2000, when executives sold $37bn of stock amid the giddy highs of the dotcom bubble.

Financial Times

The rush of cash out the door includes bags carried by executives from the failed IPOs (such as WeWork, Uber and Lyft) but also the executives of mega-wealth families. The families big enough to have their own family financial offices are making a pre-crash dash for cash (such as execs at Walmart and Estée Lauder).

Family offices are stockpiling cash, as they see a recession on the horizon. A majority of the 360 family offices surveyed for the 2019 UBS Global Family Office Report expect the economy to enter a recession by 2020 and about 42% of family offices said they are raising cash reserves. “There’s more caution and fear of the public equity markets among ultra-high-net-worth investors,” said Timothy O’Hara, president of Rockefeller Global Family Office.

In other words, the smart money is getting into the lifeboats. What would you think if you saw the captain of your ship throwing his personal stash into one of the lifeboats?

When you can’t find stock buyers to be your lifeboat, what do you? Well, if you’re on the board of a vast corporate ocean liner, you vote for the company to buy your stocks back with its own cash. If it doesn’t have enough cash, you vote for it to take out a big loan or issue lots of bonds. You take the money, the company gets the debt, and you’re gone!

As huge as corporate buybacks were in 2018, they’re up 20% YoY in 2019. Coincidentally, so is corporate debt issuance — record debt for record buybacks. Sound like a last hurrah? If you don’t think the captains of industry are jumping ship, you’re either not paying attention to the action around the lifeboats, or you’re in denial.

Corporate unprofits

Speaking of companies that make no money, it turns out that is not only true of the failed IPOs; it is generally true of most US companies. Who cannot see in the following graph that, across the board, the profitability of US companies (as shown in one graph earlier) matches these bottom-feeding IPO companies. The change in corporate profitability is not only as bad as it ever gets but is at a level that is equal to or worse than all previous periods of recession:

Of course, most financial publications have focused all year on earnings because earnings are an expression of profits after taxes, and the huge corporate Trump Tax Cuts made it easy to disguise flatlining or declining profits as improved earnings. Moreover, earnings are divided over outstanding shares, and massive stock buybacks over many recent years (over $1.2 TRILLION just since the Trump Tax Cuts!) have massively reduced the divisor in that number.

But who cares about underlying truth anymore? All year, we’ve heard “earnings came in strong.” That is nothing but smoke, mirrors and blatant self-deception if you put any stock in it. In spite of the huge benefits of tax cuts and buybacks, even earnings only came in stronger than expectations that had already been substantially lowered quarter after quarter! That is truly pathetic!

The bar was set so low they had to dig a trench to set it in; yet, profits — as expressed in “earnings” after hugely lowered taxes and record buybacks — barely stumbled over the bar. As the graph above proves, profits are literally abysmal. The decline in actual profitability has NEVER gone this low for this long, even during the worst of recessions! You can also see the decline started forming LONG before the Trump Trade War. We are certainly already in a deep and long profit recession.

However, in our new Wonderland World of economic denial, only headline numbers like “earnings” matter. No one cares what’s under the hood so long as there is a headline the algorithms can latch on to. No one thinks.

I hold to an old-fashion view that the longer you float along in denial about underlying the reality, the further and harder you are going to fall when your eyes open one day and you see there was nothing under any of what you believed in. You are a cartoon, running out over a cliff who will fall to reality as soon as you look down.

Here is why falling profitability will eventually matter, even in the pretend stock market. It is getting harder and harder to keep those headline “earnings” numbers up now that the year-over-year, bottom-line boost from tax cuts is moving into the rear-view mirror, while the ability to continue buybacks will become strained by record levels of corporate debt taken out already to achieve those buybacks.

As you can see below, with all the help of tax cuts and the buybacks they funded from the start of 2018 to the present, the best the Dow Jones Industrial Average could manage was to flatline:

Given the historically massive stimulus it has taken just to flatline, that’s a pretty dead market, if you ask me. That’s a market that is constantly being hit with the defibrillator paddles but is staying flat on its back.

The existence of the present fantasy world that keeps believing we’re in a bull market is why I’ve said I don’t think stocks will lead us into the recession because denial is so deep right now, but the market will come down when the downdraft of recession sucks it down. All investors have to do is look down without their blinders, and they’ll see they walked far past the edge of the real cliff.

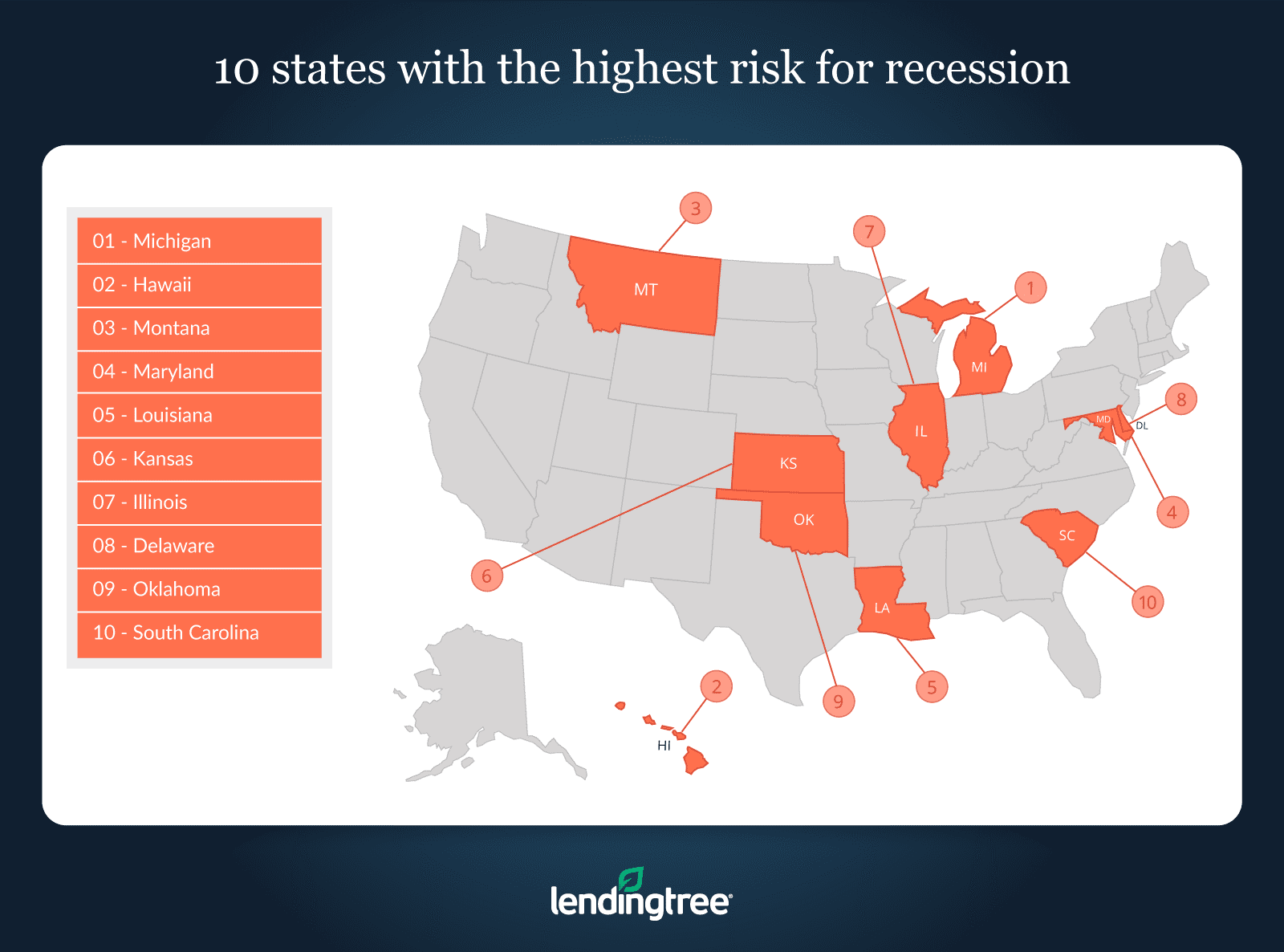

Some states already in recession

The Philadelphia Federal Reserve Bank created what it calls the “Coincident Economic Activity Index” to gauge economic development in a state’s economy. The index seeks to map the trend that is happening in state GDP:

The coincident indexes combine four state-level indicators to summarize current economic conditions in a single statistic. The four state-level variables in each coincident index are nonfarm payroll employment, average hours worked in manufacturing by production workers, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average). The trend for each state’s index is set to the trend of its gross domestic product (GDP), so long-term growth in the state’s index matches long-term growth in its GDP.

Philadelphia Federal Reserve Bank

Similar to measuring GDP for the US to determine an economic recession based on there being two quarters of economic decline, the state index shows whether individual states have experienced two consecutive quarters of declining economic activity:

Philadelphia Federal Reserve Bank

Because the Fed’s index is monthly, Lendingtree has compiled the monthly index results into quarterly results to match better with the way recessions are determined based on GDP:

If a state has a negative year-over-year growth rate in its coincident index for two or more consecutive quarters, then we’ve considered it to likely be in recession.

Based on their compilation of the Fed’s state indices, Lendingtree has determined several states that they believe are already in recession or will be entering recession in the fourth quarter. At the top of the list are Michigan, Hawaii, Montana, and Maryland:

Though our model predicts that most states will still be in good shape by the end of the year, these rosy outlooks can turn gloomy quickly. This is because economic circumstances, especially on the state level, can change very quickly. Therefore, just because there isn’t a high likelihood that most states will experience weak economic fundamentals by the end of the year doesn’t mean that they are totally in the clear for the foreseeable future.

Bear in mind that the labor statistics that underlie the Fed’s contribution here via its indices for each state come from the Bureau of Labor Statistics, and the BLS reported earlier this year that it has been overestimating new jobs lately by half a million a year, so things may actually be worse than the state indices show and are not likely to be better.

The three horsemen of the apocalypse

I’ve been saying for three years that three major markets would all play a significant role in the next economic collapse. Those markets have, as predicted, worsened continually throughout that time, so let’s see how they did over the latter part of summer.

Carmageddon keeps piling up

Carmageddon is no longer just hitting US automakers:

“Grim Start to U.S. Auto Sales Stirs Alarm That Collapse Is Here….” Toyota, Honda, Nissan suffer double-digit drops in September…. While a fuller picture will emerge Wednesday when General Motors Co. and Ford Motor Co. are due to report, the poor performance suggests that overall deliveries of cars and light trucks could come in worse than the 12% drop anticipated by analysts, based on six estimates…. The severity of the slide stokes fears that a long-anticipated car sales collapse may be arriving. The slowdown puts auto dealers already struggling with shrinking profit margins in an even more precarious position.

It was an across-the-board car wreck.

And, of course, September was the month when Moody’s downgraded Ford’s $84 billion in corporate bonds to junker status, which makes Ford the largest crashed auto corporation in the US bond market.

Retail Apocalypse

Retail’s slide continued unabated and is no longer constrained to brick-and-mortar store. Retail stocks have fallen; and, on some days, Amazon has led the downhill charge. So have sales. So has the number of companies that continue to exist.

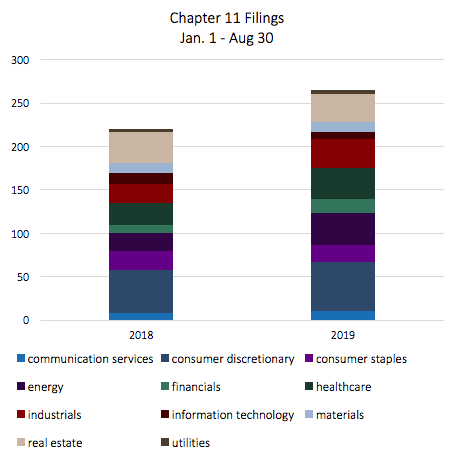

In brick-and-mortar, Forever 21 was the latest big brick to fall. Bankruptcies like Forever 21 are on the rise, and store closures all across retail are higher already than they were in the whole of 2018; yet, 2018 was a terrible year for retail stores. (See: “Retail Bankruptcies Rise, Store Closures Skyrocket in First Half of 2019“)

In fact, bankruptcies of all kinds are up:

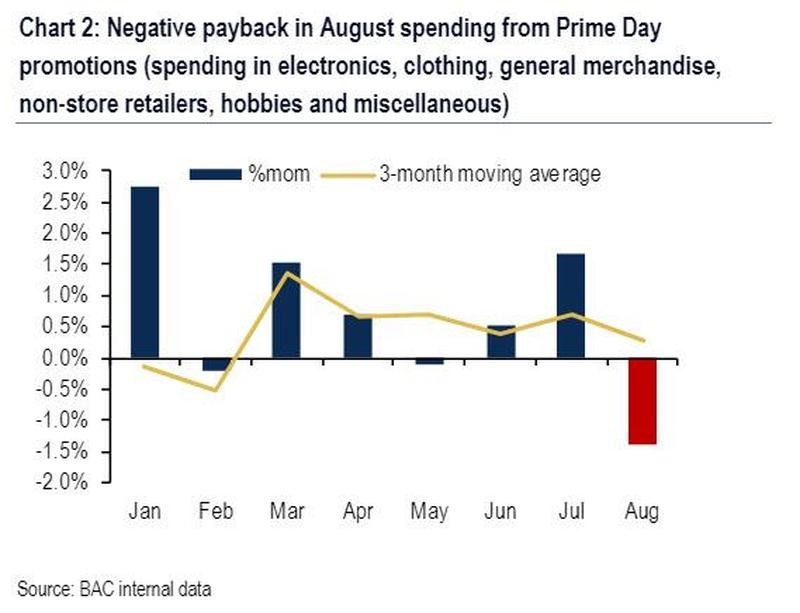

While Amazon Prime Day briefly reversed a yearlong downtrend in all retail minus auto, retail gave all of that back up in August:

And all of this was while consumer sentiment was still up. Where will it go and how fast if consumer sentiment continues to slide?

Housing market collapse

One market has seen some improvement. Sort of. After more than a year in sales declines, the housing market saw improvement in sales in the past month or so. However, I remind people that no trend in any market is ever a straight line. All falling markets have upward moves along the way, and all rising markets have downward moves.

One highly notable thing that did turn for the worse in housing was that pricing finally joined the decline in sales. I’ve cautioned all along that huge inertia in housing keeps prices from falling because our homes are usually our most valuable asset. Therefore, sellers wait out the market as long as they can before they finally start to surrender value in order to chase sales.

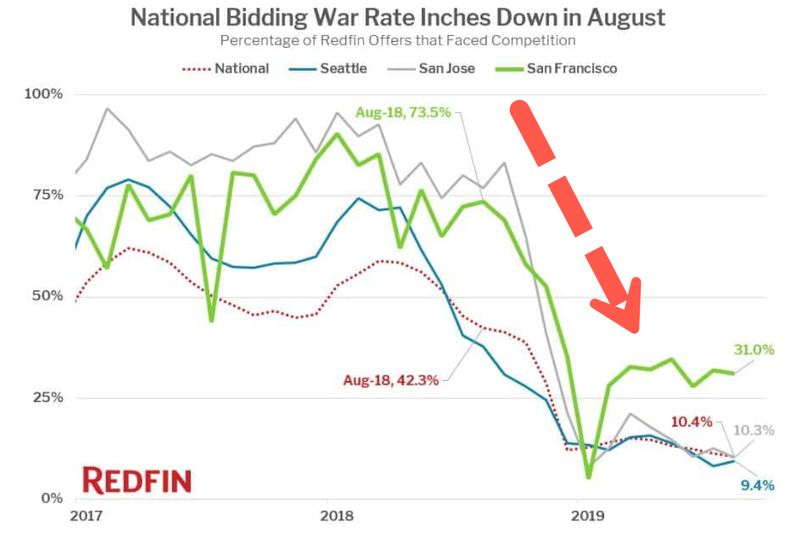

Twenty-three cities in California (one of the nation’s hottest real-estate markets started to see housing prices fall this summer. Some of these cities were among the last to join the previous housing-market collapse. The cities in decline included Cupertino, Mountain View, Palo Alto, San Jose, Santa Barbara, Santa Clara and Berkeley. In many places, the price drops were quite high, exceeding 10%.

“Oh,” you can say, “It’s just because of the fires.” That is probably partially true, but …

Seattle — also one of the last to join the last big crash — is now seeing price declines. No fires or natural disasters there. Manhattan is also seeing major price declines. No fires or hurricanes there. Fox described it as “free fall.” CNBC calls it “the biggest tumble since the financial crisis.” (Are you starting to see a theme here where stats everywhere are now shadowing the last to big recessions?) “A buyer’s market,” they are saying.

Here’s a good discussion of the causes to New York’s real-estate plunge as well as the huge inertia sellers typically have toward dropping prices:

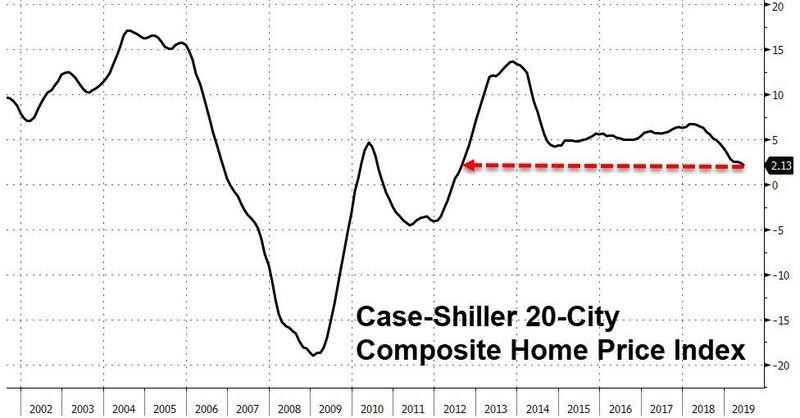

The Case-Shiller Composite Home Price Index shows that the growth rate in housing prices has collapsed as far as it had right at the start of the Great Recession and to about the same point it climbed back up to when the Great Recession was officially declared over. The national market is, in other words back down to the double-dip belly levels of the Great Recession period:

Economist Robert Shiller has already warned that the U.S. housing market might crash and home prices could start declining. And now, the monthly housing trends report for August 2019 from Realtor.com (a real estate listing website) suggests that a housing downtrend might be around the corner…. Weak price growth stokes fear of a potential U.S. housing market crash…. Realtor.com’s latest data reveals that the median listing price for a home in the U.S. … declined 1.8% month over month…. What’s alarming is that the U.S. housing market traditionally picks up the pace during the summer months, but that doesn’t seem to be the case this time. Realtor.com points out that the July to August decline was the largest seen since 2012 when the site started compiling U.S. housing market trends. The latest data from Realtor.com adds to the pall of gloom over the U.S. housing market and exposes us to more data points that indicate a crash might be on the way.

Those are some strong voices now joining my own claims that the downturn I called over a year ago is now starting to bring down prices (a delay between sales decline and price decline I said from the start you could fully expect).

Housing construction finally started to pick up in some areas, but continues declining a lot in other normally strong markets. For example, San Diego County, one of the nation’s hottest housing markets, saw 43% fewer homes built in the first half of 2019 as compared to the same period I the previous year. Housing construction (single- and multiple-family) in the whole of southern Cal is down 25%.

Yields curve, recurve and recurve again

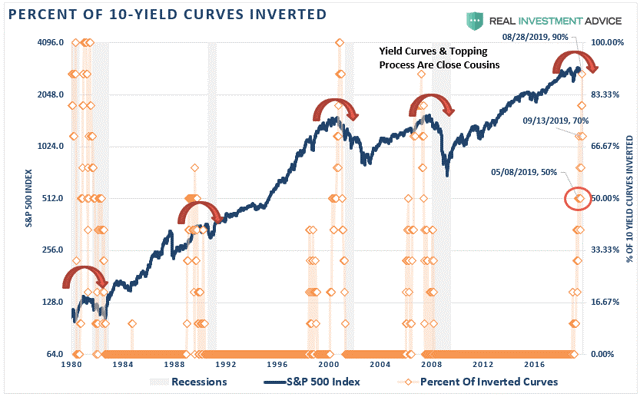

Then there is the continuance of that whole yield-curve thing that everyone says is predictive of recession. For a moment it started moving back toward normal, then its belly started stretching back down.

Remember this graph?

As you can see in the graph above, the in and out and back in again is just part of the normal topping pattern that immediately precedes a recession. Yield curves across the spectrum sit at the same deep and broad level of inversions they were at last time I presented this graph, only now we’re a month further closer to the gray zone (or in it and don’t know it because it hasn’t been officially declared).

In conclusion

Need I say more?

Along the way, another major statistic has done something else I predicted it would do this year … far ahead of anyone else that I’ve read (though I’m sure some others have probably said it). I stated unequivocally that the US annual deficit would surpass the trillion-dollar mark this year, even though all that government largesse would take the economy nowhere. The economists I read were saying it would do that next year, but I’ve claimed all along that the Trump Tax Cuts and spending increases would fail so badly that we’d break the trillion-dollar deficit barrier this year.

What is different this time than other years when the deficit was this high is that in the other years, we were trying to climb out of the Great Recession. This year was supposed to be the year of plenty, the year of a great America when the Fed’s recovery or the Donald’s economy flew like a balloon over the 4% GDP mark. I’m here to say it is a lead balloon, and its not flying any further. You can deny it because you hate to face facts, but the facts ALL line up. We didn’t get much lift for our trillion-dollar deficit.

What is also different is that our last monumental deficits of similar size came after a few years. This year’s federal deficit plots a new trajectory of inter-galactic flight as far as the eye can see.

If all of this doesn’t prove recession is now, given the two data points that remain a bit reluctant to join the parade (unemployment and the brief housing uptick), it certainly presents a preponderance of evidence that recession is either already sitting on our heads, or it’s certainly about to kick us in the butt.

It seems we are at a curious moment in time. Parallels to late 2007 are running through the markets now. This doesn’t mean the market’s fate will play out as it did then, but the ingredients are there and all that’s needed is a trigger.

Much more data are available to tell the story of summer’s fall into recession

For anyone still insisting, as the permabulls do, that the economy is strong, I’ll leave it to you to track backward through my earlier articles this year that laid out similar streams of data, showing the relentless march toward recession throughout the late spring and summer months. Here is a list of those written since summer began (with a summary of the many data sources quoted): (So, don’t anyone say I have not presented enough data to support my case all summer. You just have to follow this website to find it.)

How’s That Recession Coming, Dave? Cass Freight Index, Yield curve inversion, “recession” as the new obsession on Google and in reportage, National Bureau of Economic Research’s recession indicator, U-Mich Consumer Sentiment Index, numerous employment gauges, bond defaults, manufacturing indices, a large list of recent mainstream articles about the economic downturn.

The Drip, Drip, Drip of Recession Cass Freight Index, Dow Transports, US manufacturing (PMI), bond yields, bank stocks and forward guidance, retail apocalypse update, year-on-year decline in stocks, earnings recession, housing decline, New York Fed’s “most-reliable” recession indicator, the Leading Economic Index.

A Long Shadow Creeps over the Economy This Summer BASF and Fastenal as harbingers of the general economy, freight rates, institutional investors “buckling up,’ Chinese trade strains.

Ten Big Steps down the Road to Recession Manufacturing indices, services sector index, yield curve inversion, unemployment upturn by various gauges, IPO problems, housing sales and construction data, Carmageddon update, Cass Freight index, Morgan Stanley’s Business Conditions Index, trade deficit.

*********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.