Rising Rates Falling Assets

Last week, we wrote about the concept of discounting. This is how to assess the value of any asset that generates cash flow. You calculate a present value by discounting earnings for each future year. And the discount rate is the market interest rate. We said:

“If the Fed can manipulate the rate of interest, then it can manipulate the value of everything…

…

There is no other rate to use, other than the market rate. You don’t know the right rate any better than the people who centrally plan our economy. The problem is not that the wrong people are in the job. The problem is not even that they use the wrong magic formulas to determine what rate to set.”

The Fed cannot make a company more profitable, but it can reduce the discount rate so that market participants are willing to pay more for its shares. We noted that no one knows the right rate any better than the Fed. Thus, the only rate to use is the market rate. But we did not really make the case in favour of using the market rate.

Without an arbitrage theory of economics, it might be hard to prove this. One could say that there is a certain elegance in using the market rate, but then one could argue for various fudge factors to adjust the market rate too.

But arbitrage cuts to the chase. Suppose you could borrow $1,000,000 at 2%. That means you pay $20,000 in interest. But suppose you can buy $1,000,000 worth of stock that generates 3% earnings. That is, it earns $30,000. There is a profit to be made in this trade.

We are deliberately leaving aside three issues. One is the risk of owning equity, which is on top of the risk of owning debt. Two is the choice of which interest rate to use: Fed Funds Rate, 6-month LIBOR, 5-year corporate AA bond yield, etc. Three is whether to look at earnings vs dividends.

But these details aside, it is simple conceptually. If one can borrow at 2% to buy a 3% yield, there is an actionable arbitrage.

Price is set at the margin. So long as institutions can pay more because they can borrow cheaply, then everyone else must compete with them. They must pay more, too, if they want to buy stocks. So the price of stocks is bid up which is the same as saying that the discount rate is pushed down. The discount rate is pushed towards the market rate of interest.

This is another way of saying the Fed manipulation of interest rates is pernicious. In a free market, if participants could borrow cheap to buy stocks, they would push up the interest rate (or at the least push up the rate for financing stocks). But the Fed does not administer a free market. It sets the rate, based on a political rather than economic or market process. The act of borrowing to buy stocks does not push up the interest rate. It only pushes down the discount rate.

And this leads us to a conclusion that should be self-evident, but is actually controversial. The price of all assets tends towards the inverse of the interest rate. As interest rates fall, asset prices rises. This is no mere correlation. We commit no fallacy of Ad Hoc Ergo Propter Hoc here. The asset price rises, because the marginal buyer can borrow at the market rate to finance the purchase. All other market participants must either pay the price, or stand aside. And what asset manager wants to say that he sat out of a Great Bull Market? If he did, would he have any assets left under management?

Besides, few investors even see the problem. They think of it as a Great Bull Market, which they believe is the sign of a strong economy.

We have written tons of material on the capital destruction wrought by falling interest rates. And tons more on the process of conversion of someone’s capital into someone else’s income during a period of rising asset prices. Last week, we argued that there is no way to say that prices are too high except by reference to discounted future cash flows. Which means that as the market rate of interest falls, prices should go higher.

And today, we’re arguing that falling interest rates causes rising asset prices. And rising rates (which everyone but us seems to think is the new trend) cause falling asset prices.

Many say that the advantage of the gold standard is consumer price stability. They point to the price of gasoline before 1913 (around 26 cents) and today. Wouldn’t it be great if you could fill up your Ford F-150 Lighting for $5.20? This is an economic fallacy, as of course wages were much lower in 1913 also.

And it’s not a compelling argument to most people. If you don’t believe us, we encourage you to go out there and talk to lots of people. Tell them we need the gold standard to prevent inflation. Tell them what gas cost in 1913. Then see if even one of them has been converted to the gold standard.

Our argument today is that unstable asset prices harm investors. Rising asset prices fuels a conversion of wealth to income, to be spent. No one wants to be the Prodigal Son and spend his family estate. But everyone is happy to spend most of their income.

Then falling asset prices causes defaults and bankruptcies. It sets back long-term savers by decades. And the problem is even worse for investors who use leverage (such as the institutions who borrow at the market rate to buy stocks). Rising rates contracts the asset base, which supports the debt.

In the unadulterated gold standard, the rate of interest is stable. Hence asset prices are stable. No one who understands this argument can dismiss it and keep advocating for irredeemable currency.

Supply and Demand Fundamentals

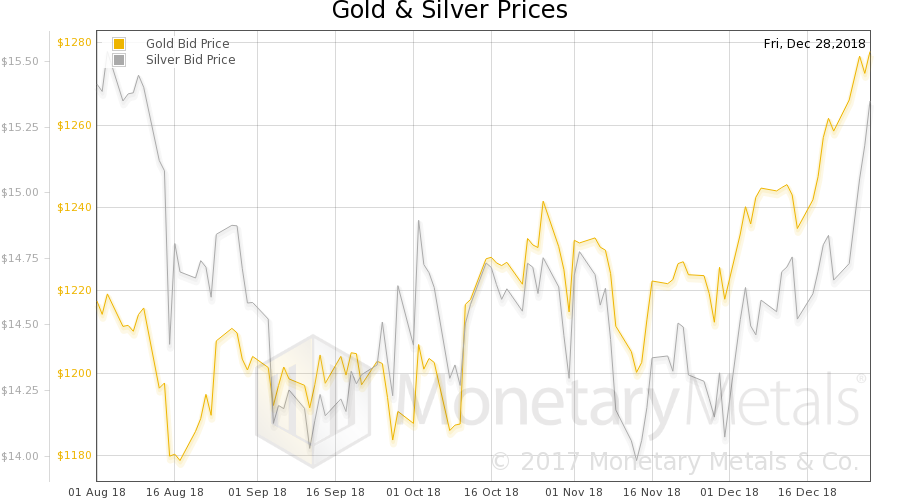

This week, the price of gold rose $25, and that of silver $0.60. Is it our turn? Is now when gold begins to go up? To outperform stocks?

Something has changed in the supply and demand picture. Let’s look at that picture. But, first, here is the chart of the prices of gold and silver.

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio). It fell sharply this week.

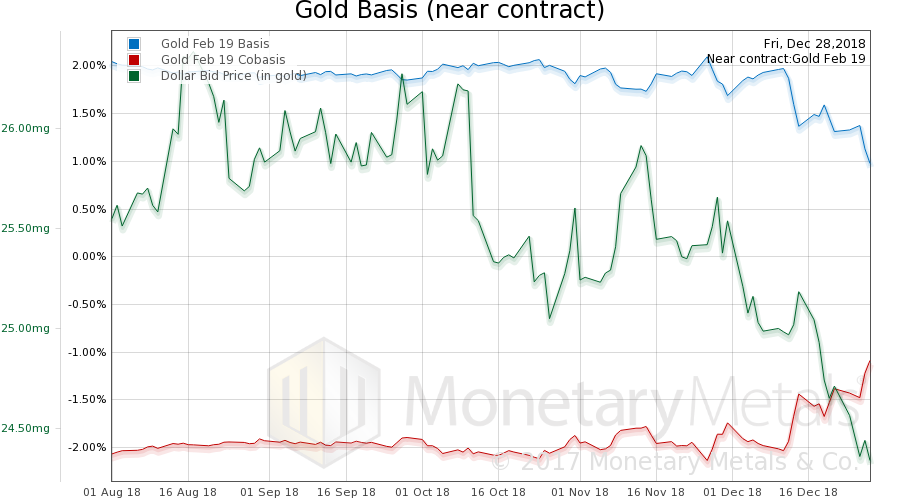

Here is the gold graph showing gold basis, cobasis and the price of the dollar in terms of gold price.

Notice the price of the dollar (i.e. inverse of the price of gold, measured in dollars) moving opposite to the scarcity of gold (i.e. the cobasis). Gold is becoming scarcer to the market, while its price is rising. This is not a move driven by leveraged speculators arbitraging their gold market to stock market expectations or Wall Street betting that gold will go up when stocks go down. Or at least not only that.

There’s buying of metal here.

The Monetary Metals Gold Fundamental Price rose another $18 to $1,325.

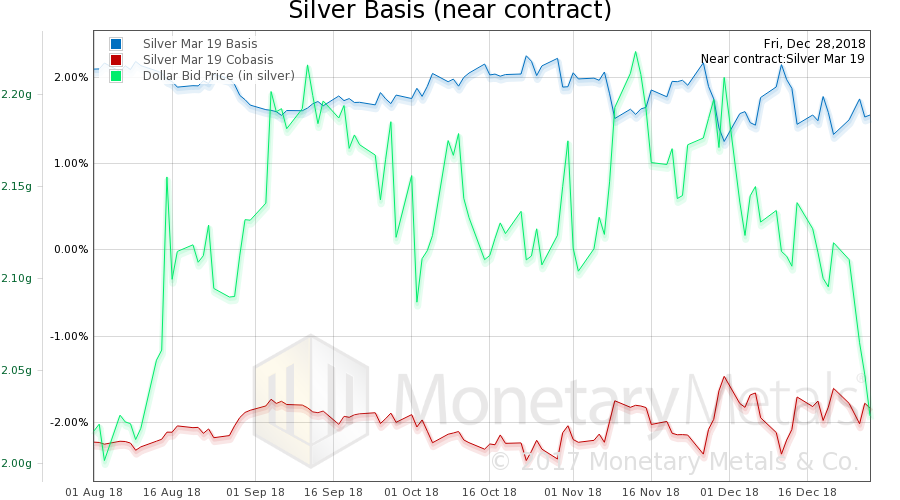

Now let’s look at silver.

In silver, we see a similar trend. We had a much bigger price change proportionally. And the cobasis dopped, but not a lot. There is buying of silver metal too.

And unlike in gold, the Monetary Metals Silver Fundamental Price rose 68 cents, to $15.79.

It makes sense, in our broken monetary system, that if people perceive the stock market as having topped then many people may begin to turn to precious metals to be the next bubble. Others begin to heed the now out-of-fashion idea of having some money set aside, apart from their portfolio. If the Fed’s Great Bull Market could falter, then maybe the Fed is not omnipotent and it makes sense to reduce risk?

Whatever the reasons, we think the stars may be aligning.

© 2018 Monetary Metals

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.