Russia’s Financial Troubles: Will They Cast A Shadow On Gold?

share

share

share

share

share

share

share

share

share

share

Sanctions, terminated contracts, and a plummeting currency – Russia is facing the financial crisis specter. Can gold also be affected? In the medium term, even painfully.

While gold continues to ride the bullish wave of geopolitical tensions, confusion has arisen over whether Russia’s financial woes will support or hurt the yellow metal. For context, I wrote on Feb. 28:

Even if the recent escalation uplifts gold in the short term, the fundamental implications of Russia’s financial plight support lower gold prices over the medium term.

Please see below:

To explain, with Russia essentially blacklisted from many influential FX counterparties, the Russian ruble relative to the U.S. dollar was exchanged for a roughly 50% discount on Feb. 27. As a result, Russian's purchasing power is nearly half of what it was before Sunday's developments.

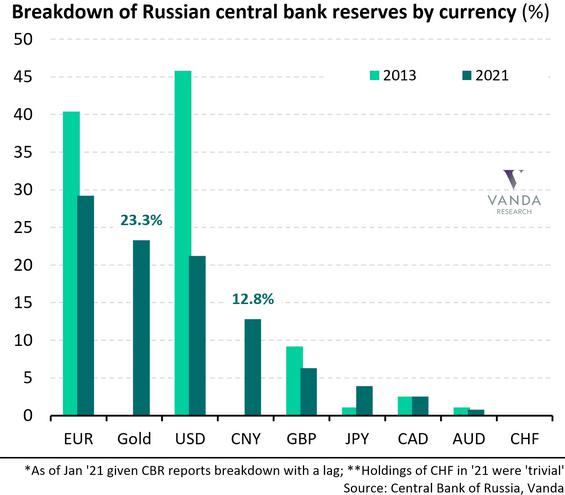

Furthermore, if you analyze the chart above, you can see that euros and U.S. dollars made up a large portion of Russia's monetary base in 2013 (the green bars on the left). Conversely, those holdings dropped dramatically in 2021 (the blue bars on the left).

In addition, if you focus your attention on the column labeled "Gold," you can see that FX has been swapped for gold, and the yellow metal accounts for roughly 23% of Russia's monetary base. Now, with the impaired state of the ruble offering little financial reprieve, Russia may have to sell its gold reserves to alleviate the pressure from NATO's economic sanctions.

As a result, while war is often bullish for gold, the fundamental implications of currency devaluation mean that gold is Russia's only worthwhile asset outside of oil. Thus, with bank runs already unfolding in the region, the yellow metal could be collateral damage.

To that point, the USD/RUB closed at roughly 105 on Feb. 28. As a result, it costs 105 Russian rubles to obtain one U.S. dollar. With the spot gold price at around $1,900 per ounce, it costs roughly 199,500 Russian rubles to purchase an ounce of gold.

In stark contrast, the USD/RUB closed at approximately 75 on Feb. 16, which means that less than two weeks ago, it cost 142,500 Russian rubles to purchase an ounce of gold at the current price. As such, in currency-adjusted terms, the cost of an ounce of gold in Russia has increased by roughly 40% in recent days.

However, after Bloomberg posted an article on Feb. 27 titled “Bank of Russia Resumes Gold Buying After Two-Year Pause,” the revelation may have caused some anxiety about our short position (as a reminder, it’s not in gold, but in junior mining stocks). For context, an excerpt from the article read:

“The central bank will begin buying gold again on the domestic precious metals market, it said in a statement. The move comes after the monetary authority and several of the country’s commercial banks were sanctioned in response to Russia’s invasion of Ukraine.”

As a result, if Russia goes on a shopping spree for bullion, could the price skyrocket? Well, the reality is that the fundamentals don’t support the sentiment. As mentioned, the USD/RUB has surged in recent days, and the sharp decline in the value of the Russian currency is extremely bearish for the Russian economy.

Please see below:

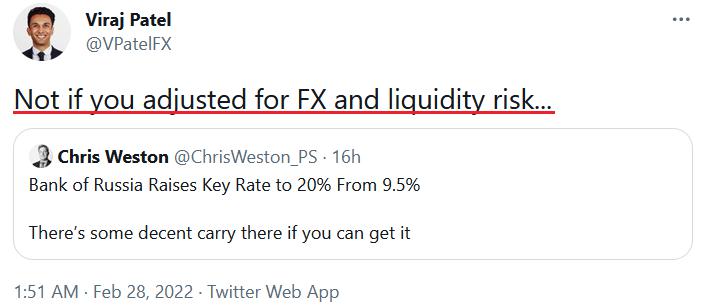

Furthermore, while Russia may want to increase its gold reserves, it’s essential to focus on what Russia does and not what it says. For example, the Russian central bank increased its overnight lending rate from 9.5% to 20% on Feb. 28. While U.S. investors fret over a 25 basis point hike from the Fed (which, as mentioned previously, should occur in March), Russia had to increase interest rates by 10.5% to help stop the ruble’s bleeding.

Please see below:

Source: Reuters

For context, higher interest rates encourage capital flows, and with the ruble in free-fall, Russia is hoping that investors will buy the currency, invest in Russian bonds, and potentially earn a 20% return. Moreover, if the currency rallies during the holding period, the carry trade would be highly lucrative for an institution willing to incur the risk.

However, the story is only sanguine in theory. In reality, though, crippling sanctions from NATO and private companies divesting their Russian assets mean that buying the ruble and other Russian securities requires a gambler’s mentality. For example, Viraj Patel, FX and Macro Strategist at Vanda Research, summed up the dynamic in a few simple words on Feb. 28:

Source: Viraj Patel Twitter

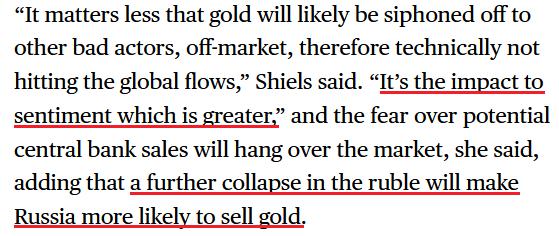

Thus, while Russia may claim it's buying gold, and who knows, maybe it will, the financial destruction plaguing the region will likely make Russia a net-seller over the medium term. To that point, if we circle back to the Bloomberg article referenced above, Nicky Shiels, head of metals strategy at MKS PAMP SA, said in the same piece that investors would interpret the actions as short-term bullish.

However, aligning with our expectations, she noted that investors have misjudged the medium-term impact of Russia's currency crisis.

Please see below:

Source: Bloomberg

As a result, that’s why I wrote on Feb. 28 that while volatility may be the name of the game this week as investors struggle to digest the implications, the geopolitical risk premium that often supports gold may prove counterintuitive this time around.

Furthermore, we shouldn't ignore the potential impact on the USD Index. For example, while the dollar basket defied expectations and rose materially in 2021, the momentum continued in 2022. However, after a sharp rally in January, investors repositioned their bets, and euro longs were in style once again. However, with the risk-on trade now disrupted by the Russia-Ukraine conflict, more downside for the euro implies more upside for the USD Index.

Please see below:

Source: Institute of International Finance (IIF)/Robin Brooks

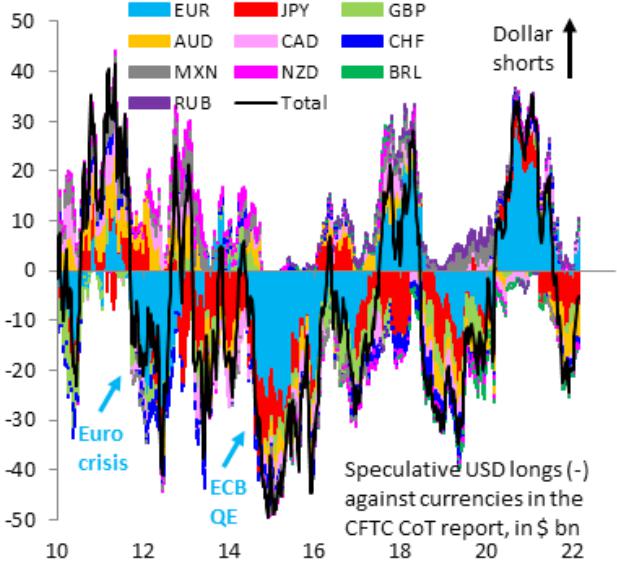

To explain, the color blocks above track the non-commercial (speculative) futures positioning for various currencies versus the U.S. dollar, while the black line above tracks the consolidated total. If you analyze the right side of the chart, you can see that the black line has moved higher recently, which signals fewer U.S. dollar long positions.

More importantly, though, if you focus your attention on the light blue blocks on the right side of the chart, you can see that speculative euro longs have increased and remain in positive territory. However, with the economic impact of the Russia-Ukraine conflict much more troublesome for the Eurozone than the U.S., speculative EUR/USD positioning still has plenty of room to move lower.

To that point, Mark Sobel, Senior Advisor at the Center for Strategic and International Studies (CSIS), wrote on Feb. 28 that “the overall impact of Russia’s actions on the U.S. economy may not be significant, assuming oil prices don’t soar, though that remains a significant risk.”

“The challenges for the ECB will be much greater in its debates over balancing the stagflationary consequences of the Russian invasion. Europe is a large net energy importer and remains dependent on Russia for oil and natural gas.”

As a result:

“European Central Bank President Christine Lagarde will feel the strain more than Federal Reserve Chair Jerome Powell. Higher oil prices will boost inflation, weaken growth prospects and stoke stagflation fears.”

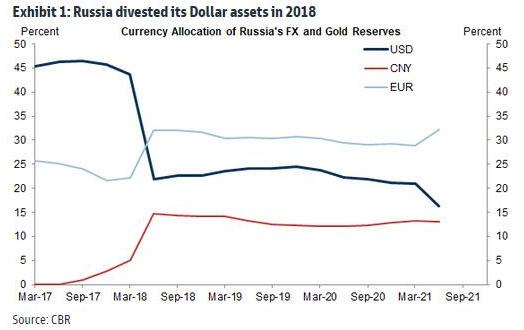

Furthermore, if you analyze the right side of the chart below, you can see that Russia’s monetary base includes more euros (the light blue line) than U.S. dollars (the dark blue line). As a result, if Russia swaps its other FX holdings for rubles (to help stop the decline), the euro has more downside risk than the greenback.

The bottom line? While Russia may put on a brave face and claim that gold purchases are on the horizon, the reality is that its materially weak financial position requires more attention to more pressing matters. With bank runs and a currency crisis already unfolding, combined with NATO sanctions and private companies divesting their Russian assets, the country’s leaders need to stem the tide before a depression unfolds.

As a result, Russia’s oil revenues and the securities it can monetize are more likely to be used to support the Russian economy, rather than to buy gold. Thus, while the yellow metal has enjoyed short-term sentiment high (and so did the silver price), the fundamentals imply a much different outcome over the medium term.

In conclusion, the PMs were mixed on Feb. 28, as the GDX ETF ended the session roughly flat. However, the recent rallies are far from troublesome. For example, I noted previously how gold rallied following the 2001 terrorist attacks and after Russia annexed Crimea in 2014. However, those gains were short-lived, and the latter resulted in lower lows in the months that followed. As a result, while the recent volatility will likely continue, it doesn’t change the bearish medium-term thesis.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of today’s all-encompassing Gold & Silver Trading Alert. The latter includes multiple premium details such as the targets for gold and mining stocks that could be reached in the next few weeks. If you’d like to read those premium details, we have good news for you. As soon as you sign up for our free gold newsletter, you’ll get a free 7-day no-obligation trial access to our premium Gold & Silver Trading Alerts. It’s really free – sign up today.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Sunshine Profits: Effective Investment through Diligence & Care

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses are based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are deemed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

********

share

share

share

share

share

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com. You can reach Przemyslaw at: http://www.sunshineprofits.com/help/contact-us/.

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com. You can reach Przemyslaw at: http://www.sunshineprofits.com/help/contact-us/.