Is The Strong US Dollar Coming Again?

In March, the U.S. dollar reached a 12-year peak against the euro. The greenback gained almost 25 percent in the past twelve months and 9 percent in 2015, which was the biggest surge in 30 years. What is most important, the U.S. dollar was rising not only against the euro, but against almost all currencies in the world. It means that the ECB’s QE and negative interest rates in many Eurozone countries were not the main or the sole driver of the surge in the U.S. dollar index. So why the greenback was rising, while the reports of the U.S. economic recovery had been greatly exaggerated?

The answer is the divergence monetary policies in the world. In the first three months of 2015, 25 central banks cut their interest rates or eased their monetary policies, while the Fed was almost the only player (besides the Bank of England) considering the interest rate hike in the nearest future. The relative hawkish stance of the Fed is interpreted as the signal that the U.S. economy is in a good shape, which encourages investing in the U.S. The 10-year interest rates are almost 10 times higher than in Germany, the Eurozone’s powerhouse, so it is not difficult to understand why the capital was flowing into U.S. and the greenback was rising.

Put in another way, what really counts for the investment decisions is the relative performance, not the absolute performance. The Fed’s officials may seem undecided, impotent or deliberately playing with investors’ expectations substituting the hike by the endless talk about it; however, in comparison to the madness of Abenomics in Japan or its younger cousin, Draghinomics in Eurozone, the Fed’s credibility is high. The U.S. economy may be far from a full recovery; but the greenback is now the prettiest of the ugly currency sisters.

Just analyze the potential alternatives. Euro? The economic growth in the Eurozone is sluggish (although some economists point out that it is gaining momentum right now), mainly due to structural problems, such as inflexible labor markets and state expenditures on the level of 50 percent of the GDP (vs. 40 percent of the GDP in the U.S.), resulting in high public debt burdens and taxation. Thus, the ECB’s QE will not change anything, but weaken the euro.

Maybe the yen could win with the greenback? We do not think so. The Japanese government is the largest debtor in the world with the gross public debtof approximately 240 percent of GDP (vs. over 100 percent in the U.S.) and the fast aging society, while the size of the Bank of Japan’s balance sheet has been exploding for years. Notwithstanding the more and more expansionary monetary policy, there is no recovery whatsoever.

And what about the emerging markets? Their currencies simply do not count. They do not have the reserve status, nor are they not or safe enough. Additionally, low commodity prices hit many emerging countries and the surging greenback makes the payment of the $5.7 trillion debt denominated in the U.S. dollar held by the emerging markets much more difficult. The Chinese renminbi could be an exception; however China is facing an economic slowdown right now since the burst of one of the biggest real-estate bubble in human history. Needless to say, the Chinese crash will shake the worldwide economy, but mostly the emerging markets exporting commodities (as well as Canada and Australia, which is especially dependent to a significant extent on Chinese purchases).

So these are the reasons why the U.S. dollar has been soaring. Obviously, the expected Fed’s hike adds fuel to the fire; however it is possible that the greenback could gain even if the U.S. central bank literally does nothing. Suffice that other central banks conduct more expansionary monetary policies. And the unwinding of the emerging markets carry trade may strengthen the greenback even further. Undoubtedly, the recession in the U.S. could change the currency outlook (and investors should be aware of it), however even the end of the U.S. bull market may be positive for the U.S. dollar, if global investors choose the U.S. Treasuries as a safe-haven during financial turmoil, as they did in 2008.

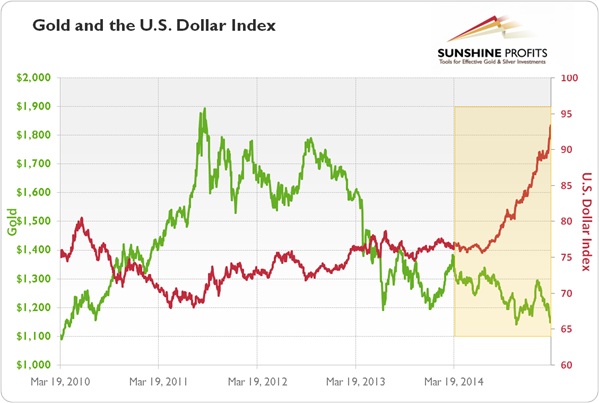

What are the consequences of the possible next U.S. dollar bull market for the gold market? Typically, it should imply the decline in the gold prices. The yellow metal performed rather poorly during the last two U.S. dollar bull markets (from 1985 to 1987, and from 1988 to 2002). However, the greenback and gold can move up together in cases of serious global financial crisis (think about the overvalued U.S. stock market) or the Eurozone’s problems. Indeed, so far gold has risen versus many major currencies and it has fallen only about 2 percent against the U.S. dollar. In other words, the yellow metal's performance is not so bad, considering the significant surge in the greenback (see the chart below), which indicates that the inverse relationship between these two safe-haven assets may not necessarily occur.

Graph 1: Gold prices (London PM Fix, green line) and U.S. Dollar Index (major currencies; red line) from 2010 to 2015.

********

We hope you enjoyed the above article. In order to read more of our essays and stay updated on the latest developments in the global central banking and currency markets, please join our gold newsletter. It’s free and you can unsubscribe in just a few clicks.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017. He is a board member of the Polish Mises Institute of Economic Education, author of several dozen scientific publications (including in such periodicals as the Journal of Risk Research, Prague Economic Papers, Quarterly Journal of Austrian Economics, and Research in Economics), and a regular contributor to GoldPriceForecast.com and SilverPriceForecast.com. His two books, Money, Inflation and Business Cycles and Monetary Policy after the Great Recession, are both published by Routledge. Arkadiusz is also a certified Investment Adviser, a long-time precious metals market enthusiast, and a free market advocate who believes in the power of peaceful and voluntary cooperation of people.