Time To Go Defensive – Reasons

I think it is a time to become defensive with your investment portfolio, since equity markets are likely to experience at least a +30% drop between now and October 2019. i.e. It is better to make a little less in the next 15 months than to lose 30%+ of your portfolio. If gold breaks above $1 400 in the next few months, it also may be prudent to put some money in Gold.

Introductory Notes:

-

Most crashes unfold over 2-3 years. The 1929 crash ended 89.1% lower 4 years later; 1973 ended 50% lower 2 years later; 2000 ended 50% lower 2 years later and 2007 ended 50% lower 2 years later. They all started in the September – November period. I think we are in for another big drop Sept / Oct this year or latest next year;

-

We are due for a “bad” crash, but after that, we will enter a boom of note as we reap the future tech benefits promised by Automation, Robotics, AI, Gene Editing, etc.

-

Distorted picture: The wild card in all this is the fact that we cannot trust the markets, since historic measures of economic activity clearly do not work as well as they used to in this new industrial revolution economy, which suggests we need new measures. Add to this the fact that most official statistics like Inflation, GDP growth and Unemployment are manipulated to appear more bullish. Furthermore, the market’s risk pricing mechanism is broken because interest rates were artificially supressed;

-

We often use the USA as a proxy for world markets because, what happens in the USA will almost certainly happen rest of the world. The USA accounts for about 25% of global GDP, has massive economic influence and has the most comprehensive homogenous statistics which makes it the easiest to analyse and quote.

Reasons why Equity markets are likely to crash sooner rather than later:

-

This Bull Market is long in the tooth? It is now 9.5 years old and equal to the longest bull market on record. While records are there to be broken, it does imply that the we will see the end sooner rather than later and that the downside risk is likely to be far bigger than the upside potential. This implies that it is time to look at a more defensive strategy. i.e. More in Cash, Money Markets, Bonds, Gold? and Silver?;

-

The peak is already behind us? US Equity Markets peaked in January 2018, with the Monthly, Weekly and Daily RSI at “never seen” overbought levels of 93-95, which suggests that was the peak. To date they have had a 10% pullback, but this could easily morph into a minimum 30% correction or a 50%+ crash. From a Technical Analysis point of view, the Monthly MACD has clearly rolled over and it seems likely that the Weekly MACD peak that is currently unfolding will display strongly bearish divergent signals leading into seasonal weakness. If so, we should see the S&P form a bearish double header at the January peak level of 2880 within a month or two;

-

First ever multi market crash? Traditionally “aggressive” Equities and “defensive” Bonds are negatively correlated, which means you could get out of Equities into Bonds in the event of an Equity market crash. However, following central banks’ zero interest rate policies and with most bonds outside the US still near zero, both Equity and Bond markets are at record levels, which means there is nowhere to hide. Regardless, any crash in Equities would still result in a flight to the safety of Bonds which means yields would then definitely go way below zero – NB! Negative “Real” rates are great for Gold (and Silver);

-

Share buy-backs artificially elevated markets? Due to low interest rates, companies have been buying back their own shares at a record pace with borrowed money, as the returns earned by the company exceeded the cost of debt. Buy-backs artificially elevate stock markets and often peak before major corrections/crashes. i.e. Rising rates will put a stop to buy-backs, which will slow Equity market growth and hurt those companies when their earnings fall and debt service costs rise;

-

Excessive gearing? Despite companies sitting on record piles of cash, which is a bad sign, the Gearing of many companies deteriorated in the past decade as they borrowed to buy back shares, etc. A recently published list showed that only 2 companies on the S&P 500 are still AAA;

-

Corporate Bond Market risk? Most Corporate bonds are now covenant light, which means lenders have no protection in the event the Company ends up in difficulty or goes belly up. Corporates debt is unusually high at present and the percentage of Covenant Lite loans has climbed from below 50% in 2014 to over 75% recently;

-

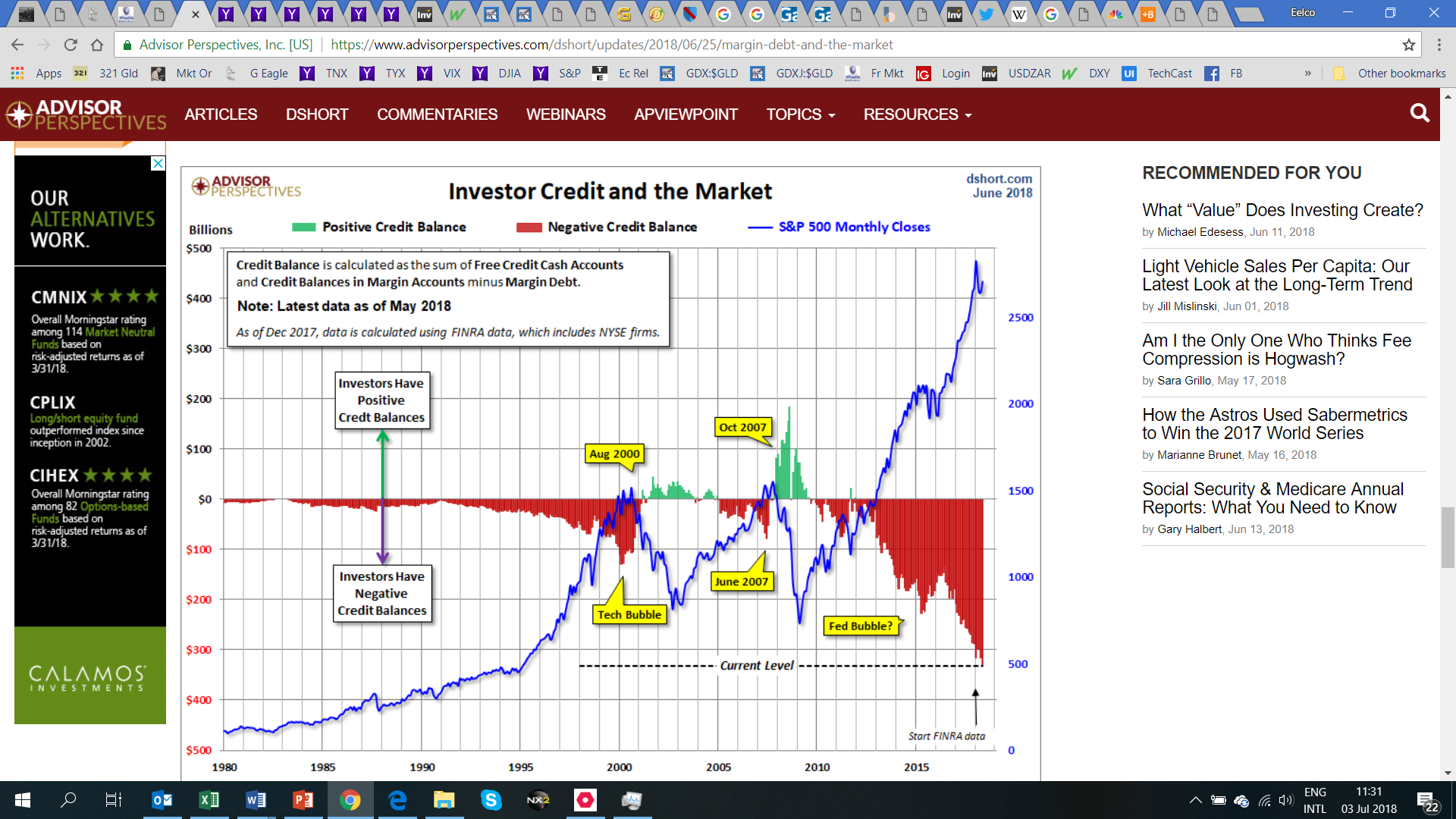

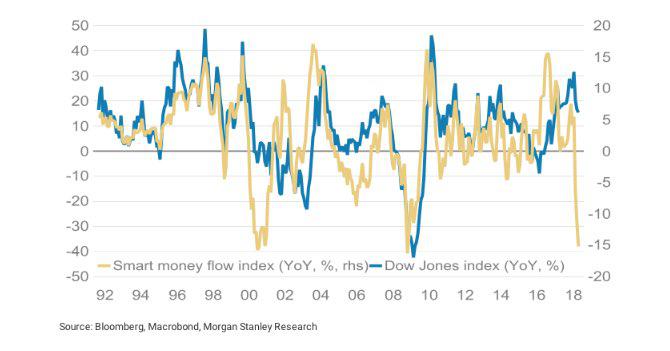

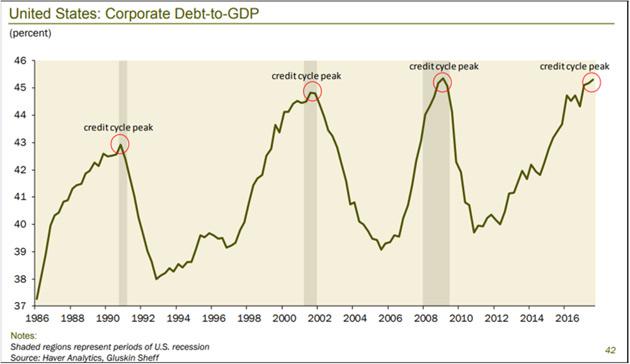

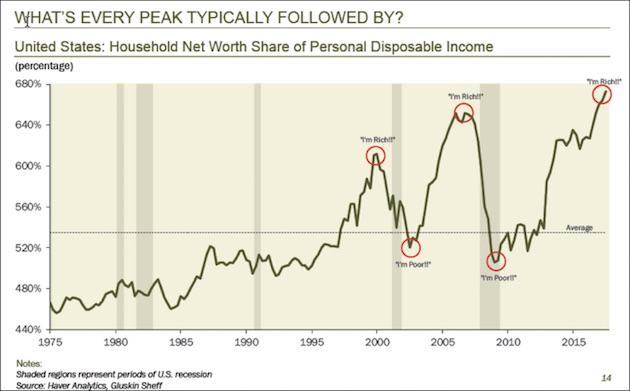

Valuations stretched by any metric? Broadly speaking, most indicators are looking worse than they did at the last few Equity peaks – and even 1929. I will show a few charts at the end to illustrate that Margin Debt is at nose bleed levels, the smart money index just fell big time, etc;

-

Mid-term blues? US markets often correct in the 2nd year of the presidential term and most corrections happen in the Sept-Nov period;

-

Quantitative Tightening (QT) may precipitate a bear market? i.e. If Quantitative Easing (QE) underscored a boom, it is logical to assume that QT could bring recession. There is a scary correlation between this bull market and the growth of the balance sheets of the Fed and other Central Banks. Commencing with zero and negative interest rates to stimulate the economy in 2008, the Fed/Central Banks later introduced QE1, QE2 and subsequently open ended QE3. The markets corrected at the end of both QE1 and QE2 and appear to be correcting as QE3 is being unwound at an accelerating rate, which jumps to $40bn per month from end August and peaks at $50bn per month from December. In addition, the EU is stopping its QE programs in December. Will Adam Hamilton’s statement “The Fed’s QE giveth and so the Fed’s QT taketh away”, prove prophetic. I think so – and probably later this year;

-

Bull market not convincing? Adam Hamilton suggests this was a “Fake boom”. Booms are normally accompanied by 4%-5% growth, not the paltry 2% growth we have seen this past decade and, worse still, the aforementioned boom was largely on the back of the FAANG/tech stocks (Facebook, Apple, Amazon, Netflix and Google). If they are stripped out the rest of the stock market’s performance was a joke;

-

Risk of flash crash? High frequency trading has introduced a new level of risk, in that HFT provides liquidity, which it could quickly withdraw in the event of a crash. This could be exacerbated by the fact that the current investment bias favours passive investing via ETF’s, which could topple quickly, rather than value investing;

-

End of falling interest rates? US Bond Yields (interest rates) dropped for 36 years from 1980 – to historic lows end 2015 and were zero to negative in most developed countries. This “free money” propelled Bond, Equity and Property markets to record highs. The Fed has been raising rates and plan to continue into year end. As mentioned, rising rates are bad for Bond, Equity and Property markets as follows:

-

Bond prices are inversely correlated to rates, so a sustained increase in rates will precipitate a Bond market crash / collapse;

-

Equity prices are benchmarked against 10 year “risk free” bond yields, which means falling rates boost equity prices and rising rates depress equity prices;

-

Property prices are inversely correlated with rates, because mortgage payments become progressively less affordable as interest rates rise, which hits both existing and prospective mortgage holders; Furthermore,

-

Rising rates will quickly bring a stop to stock buybacks.

-

-

Future of Rising interest rates? Interest rates are now rising and have clearly popped up above the 37-year declining resistance line. My view is that they will soon fall in response to a significant market correction or market crash, to retest that resistance line now turned support, before commencing a 10-20 year rising rates cycle / trend. Furthermore, inflation seems to be rising, which suggests rates will play catch up;

-

Is rising inflation here to stay? Rising inflation is never good for Equity markets, as it begets rising interest rates, because investors want an above inflation return on investment. Since it seems to be manifesting in commodities, it may be worth getting into resources after the correction/crash, as it is likely to be a protracted cyclical rise;

-

Trade wars & other geopolitical risks? What will be the effect of Trump’s Import Duties and the reverse duties implemented by targeted countries? Will we see a full-blown trade war? At the very least they will slow exports and have an inflationary effect on imports as they push up prices, both of which are inflationary. Bottom line, in the short term to medium they will be bad for equity markets, until the US has geared up to manufacture locally and consumers get used to the higher prices arising from protectionist policies;

-

Pension funds could and should reduce their exposure to Equities? Worldwide, most Pension Funds are either at risk or in trouble, as they struggled to meet the required 7.5% - 8.0% returns. During a decade of negative real rates they were compelled to reduce their exposure to low yielding bonds and increasingly invest in risky assets to achieve acceptable returns, which is contrary to their implicitly conservative mandate. At some point they will have to aggressively sell Equities. Furthermore, most penson funds have been pushed to the brink of actuarial insolvency due the global decline in contributor ratios and the fact that pensioners are living longer;

-

Global markets are down – Emerging markets down 20%, Hang Seng down 15%, Banking stocks really getting smacked, etc.;

-

Debt Bubble? Due to low/negative interest rates, it made no sense to save. Therefore, the world went on a Debt binge, with Sovereign, State, Corporate and Private Debt rising to record levels. However, it is important to understand that Debt bubbles burst when interest rates rise enough to make the squeeze hurt and that debt is future consumption brought forward. This means we will have a significant drop in consumption when current and future debt becomes unaffordable, or markets crash. This will translate into a double whammy for business as they will face rising interest rates, rising inflation rates and falling sales;

-

Deficit spending – the root of all evil? Governments all engaged in deficit spending to increase welfare/entitlement spending to buy votes. This year USA debt will rise at more than $1Trillion per annum and this should accelerate as social security and medi-care go cashflow negative about now. The problem with this is that the debt is growing faster than the population and the economy, which means it becomes ever harder to pay back, which is why Central Banks tried to suppress rates. Worse still, greedy politicians have created a debt so high it can’t be repaid by future generations and, at some point, there will be a backlash that will compel austerity. NB!. A cut back in government spending will knock employment and Equity markets;

-

US Tax breaks? The recently announced tax breaks will undoubtedly have a positive effect in the short term, however, by next year the benefits will have normalised. This implies the markets may still go up for the next 6-8 months;

-

Inverted yield curve? The yield curve is progressively flattening and may invert in the next 3-6 months. In the event that it does invert, this is usually followed by a significant recession / crash within 6-8 months;

-

We are in a tech transition era that will create imbalances in the markets in the short term as old tech companies are replaced by new tech companies (business models);

Defensive portfolio would be as follows:

-

Reduce your exposure to Equities/Shares as these will be worst hit. One would certainly want to reduce this to at most 50% of your portfolio, so you score if Equities continue to rise, but are not too hard hit if they fall;

-

Increase your exposure to Cash and Money Markets – probably 20-25% of your portfolio;

-

Increases your exposure to Bonds – albeit only for the duration of the crash – probably 20-25% of your portfolio. If there is an Equity Market correction / crash, this would initially drive interest rates down, which is good for bonds;

-

Watch Gold. If Gold breaks above $1 400 in August / September, I would put 10% of my monies in Gold;

-

NB! This needs to be discussed with your financial advisor, as it is merely a suggestion and not advice. However, advisors often remain bullish until it is too late, so I would bear that in mind.

A few of a plethora of charts that reflect that most metrics are at or near record highs:

I always like to look at this chart from Advisor Perspectives (below), that is updated monthly and surely does not make me feel warm and fuzzy.

I find Jesse Felder often posts great charts that I do not see everywhere. However, in the analysis he also talks about the fact that market drivers have changed. https://thefelderreport.com/2018/05/30/whats-behind-the-rapid-plunge-in-the-smart-money-index/

John Mauldin it always reliably objective and he posted these charts that suggest a peak is near. i.e. Neither chart suggests that there is a ton of upside in the wings.

10 Year Treasuries popped over the line – likely to correct before multi decade boom

*********

Eelco Lodewijks (South Africa).

I am a semi-retired engineer, not a qualified financial advisor. I like to teach people how to think about their investments, rather than to tell them what to do. The above opinions do not constitute financial advice.