The Wealth Effect – Cui Bono?”

With the world’s eyes focused on Syria, which we deal with extensively in our most recent client brief (and yes it does affect us all personally), there has to be some happy news. What better a way to gin up the idea of the wealth effect than a big run up in the stock market and reports of a ‘booming’ housing market? They are two of the biggest contributors to the notion that people are getting rich, aren’t they? After all, the wealth effect has drive consumption in America for the past decade. As usual, however, the now completely impotent and subjugated mainstream press only tells half the story. Or not even half really. So once again, Jim, Joe, Bob, Chris, Axel, Peter, John, and yours truly among many, many others will do their job for them. We don’t have media badges. We don’t wear three thousand dollar suits or have makeup done for us before we talk or write (at least most of us don’t!) but you’d better start to listen and listen good.

When it comes to ANYTHING in today’s world you’d better think first about cui bono – who benefits. If it isn’t you, then it is time to turn it off and ignore it. If I’ve already offended you, then too bad. The gloves are off this week and, as those of you who have been reading 2cents since it was a three paragraph blog back in 2006 can already tell, I’m pretty fired up. Let’s get into the meat of the issues of the day. There are two main areas of focus this week – those that compose the ‘wealth effect’ in America, the housing market and the stock market.

Concomitant to both of these issues is a discussion of what the not-so-USFed may or may not do next week when it meets for what will likely be Bernanke’s last go around at the FOMC table. He’ll be an obscurity a month from now most likely, tucked back in his little hole somewhere brainwashing another generation of unthinking minds that borrowing ad infinitum is the answer to all that ails everything. The man was the perfect puppet though. A simpleton who really had no convictions of his own that he had to unload to take the job. At least his predecessor had convictions at point and some of them were very valid. So, very soon, we’ll have a new puppet in the ‘temple’ but it will business as usual. While the precise details of that business are yet to be known, you can be certain it will not be in your best interests.

Central bank policy has a very direct influence on the wealth effect, especially in this country since it is virtually ALL based on debt, so interest rates matter a great deal. Bernanke’s penultimate act next week is supposed to be the grand finale for the diet version of the maestro. It is supposed to be the beginning of the exit of the decade long monetization scam perpetrated on the world for the purposes of increasing the wealth ‘effect’ while actually devouring real wealth. The cruelest of paradoxes, monetization is the benevolent philanthropist and the heartless thief all in one ugly package.

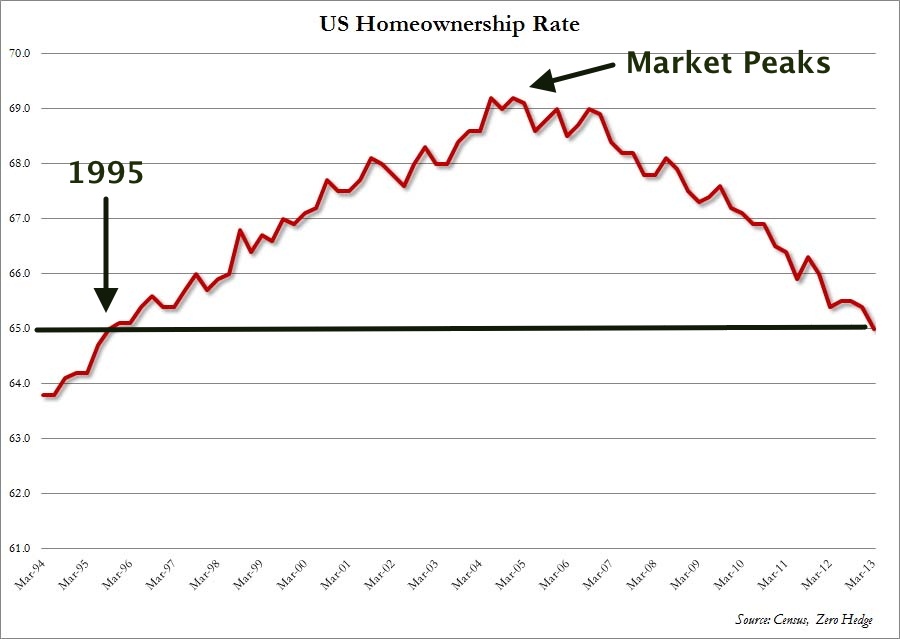

The Housing Market – Recovery or Rentalmania?

The mainstream press has been tripping over themselves to pronounce the next great bull market in housing. 2006 is here again. I could put a hundred quotes inline here and make that point, but if you’re reading this column, chances are you’ve already heard all the tripe because you pay attention to such things. So I’ll spare you your appetite and just get into the serious business of throwing cold water all over this absurd and ridiculous notion. Yesterday, Bloomberg News reported that JP Morgan is relaxing its lending standards in what the severely compromised news outlet called a ‘booming’ US market. I’ll give a very small amount of credit, however, because they did mention one of the biggest reasons the market is moving. From the article:

“Prices in some of the hardest-hit markets have rebounded faster. Las Vegas gained 24.9 percent, Phoenix showed a 19.8 percent increase, Detroit rose 16.4 percent Miami-area values were up 14.8 percent.

Private-equity firms such as Blackstone Group LP building rental businesses and other cash buyers have helped lift house prices in cities showing some of the biggest gains. Their mass purchases have made it more difficult for borrowers seeking mortgage financing, as they compete for a shrinking supply of properties.

In Florida, lenders including JPMorgan and mortgage insurers this year removed many of the additional requirements that had helped to push the share of cash buyers above 45 percent in the second quarter, said Rob Nunziata, co-Chief Executive Officer of FBC Mortgage LLC.”

Nearly half of all transactions were because of cash buyers in the second quarter. And the actual admission that cash buyers are what have been pushing prices up. Now who are these people? Who are these cash buyers? Well, you’ve got the vulture Blackstone Group, a private equity firm (read white shoe boys) and we know there are a lot of foreigners in here too, buying up cheap property. Fundamentally I’ve got no problem with someone buying something because it is on sale. We all do it. The problem exists when your cronies in the banks create the fire sale and very small groups make money on both sides of the cycle. And there’s an even bigger problem when the government not only rubber stamps this as acceptable behavior, but uses tax dollars to bail out the very people who made the mess, many of whom are now taking advantage of bargain basement prices and will rent these properties back to the same people who got thrown out of them in foreclosures (many of them illegal) over the past several years.

It is pretty obvious: the little guy was missing out on his second chance at the American nightmare of paying upwards of 2 and a half times what a house is really ‘worth’. So we have to relax those standards don’t we? Profits are being lost. Cash buyers, while great for those selling, are terrible for mortgage lenders. And those pesky interest rates have been going up too, slamming the door on a ton of these folks. That is the REAL story here and the one that isn’t being told. So, since rates are going up, we have to ameliorate some of these impediments to home ownership. We’ll go subprime again. Many places the banks are already going 0% down again. Back to the same old bag of tricks one more time. One more property grab. Detroit prices are up 16.4%? The city is bankrupt, the jobs are gone, and yet house prices are up 16.4%? We’re becoming a nation of renters again.

The American dream isn’t working out so well, is it? Even with the big ‘recovery’ in the economy and the housing markets spoken so often of on smellevision, it doesn’t bear out even when you look at government numbers on the subject. I am quite certain the housing numbers are just as biased as the best the government has to offer when it comes to jobs, inflation, and other important metrics.

The Stock Market – Funny Money Versus Fundamentals

I’ll readily admit, the situation with the stock market could easily go a couple of ways, again, depending on Bernanke the puppet and his final act. If the tapering of monetization actually begins, one would expect the global equity markets to take quite a hit since most people have correctly surmised that it is funny money and not fundamentals that have pushed prices this far. However, I’m going to throw a counterpoint out there for consideration. What if they begin tapering (or at least profess that it is happening) then run the markets up so they can say ‘See, you guys were all wrong. The markets weren’t going up because of QE, they were going up because economies are getting stronger!” Can you see it? I certainly can. Let nothing surprise you over the next few months, but I suspect most of you already know the truth. It is monetization, aka quantitative easing, that has been propping up the markets.

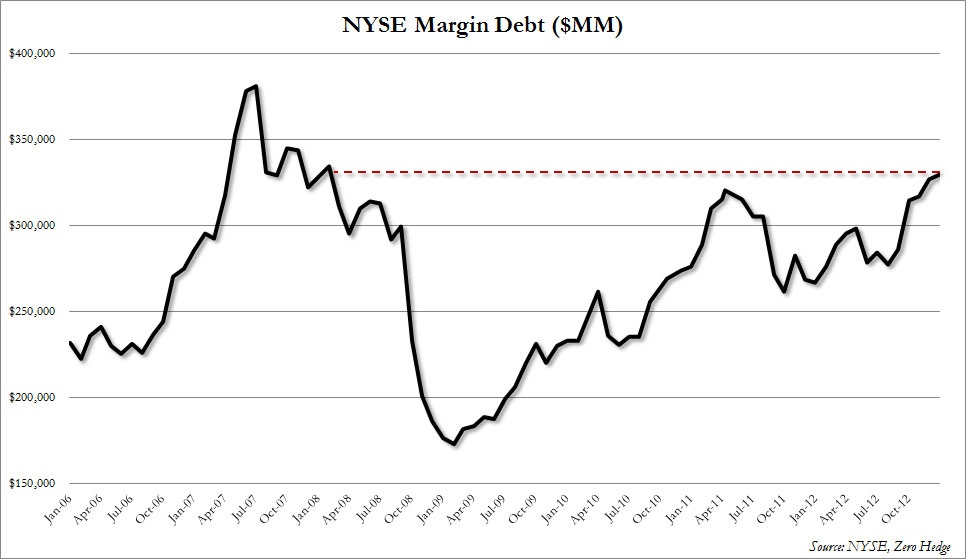

A few months ago, leverage ratios on the NYSE went above the levels at the market peak in 2007. The banksters are at it again, setting up for another big blowout. When? Who knows? Where do you think margin comes from? It is debt. Pure and simple. It is one bank, institutional investor, or hedge fund borrowing money from another to make bets. If they win, the effect is magnified. If they lose, however, they can be wiped out in a single day. The higher the margin, the less of a move it takes to wipe them out. Keep this in mind as you take a look at the chart below:

As was mentioned earlier, we’re right back at 2007 again. We all know what happened after that. But we’re so much smarter now, right? We’ve learned from those ‘mistakes’ of the past, right? I’d assert they weren’t mistakes, just like the decision by the courts in this country regarding Sentinel Group wasn’t a mistake. Just like the FDIC-BOE resolution on the failure of G-SIFIs wasn’t a mistake. Just like Paulson playing Chicken Little after Lehman, then changing his mind after he got $750 billion of your kids’ future wasn’t a mistake. They didn’t make many (if any) mistakes, but we’ve certainly learned almost nothing, of that I am quite certain. We’re right back to business as usual, happily consuming while our country’s endowments and our very freedoms are swiped right out from under us by a beast system that is too sinister for many people to even comprehend.

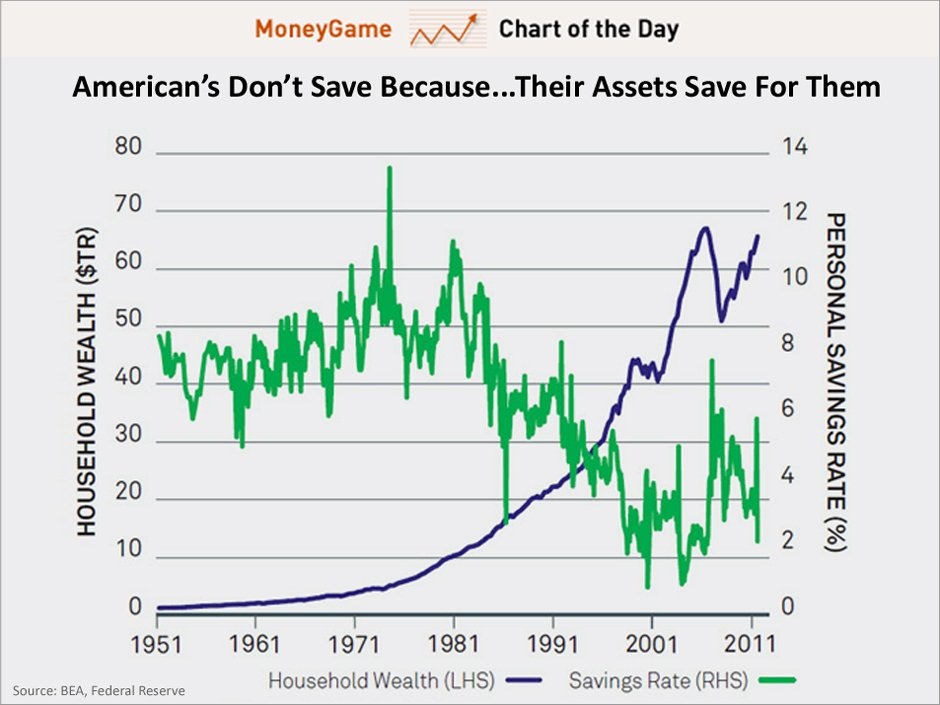

But at the same time, as markets go up, people feel wealthier. The below chart shows a nice bit of this propaganda:

Americans don’t save because their assets save for them. Note that neither of these series is discounted for inflation. Go back a few issues of 2cents and look at the absolute explosion of consumer debt that started in the early 1990s. A more appropriate title for the insanely misleading graphic above would be ‘Americans don’t save, they go into debt instead.’ This type of rationale is almost as idiotic as they guy who wrote that book ‘Retire on the House’ back in the heyday of the real estate market.

Back in 1951 when the above chart begins, people owed next to nothing and didn’t have much either. Now we have more stuff, but we are borrowed up to our earlobes to get it. Which situation is better? Well it's a wash, right? Obviously most Americans don’t have a problem with getting up in the morning, commuting ever-increasing distances, working more hours, and taking second and even third part time jobs just to make payments on their debts that will likely still be there when they write their final check. They don’t have a problem with having credit cards that reverse amortize because they don’t know better than to make the minimum payments. They don’t have a problem sending their kids to get a four year degree in which they’ll rack up an average of $45,000 in student loans, then be confronted with a job market that consists of retail, fast food, and other service sector type low paying jobs. There are exceptions for sure, but this is the reality for the majority of our kids.

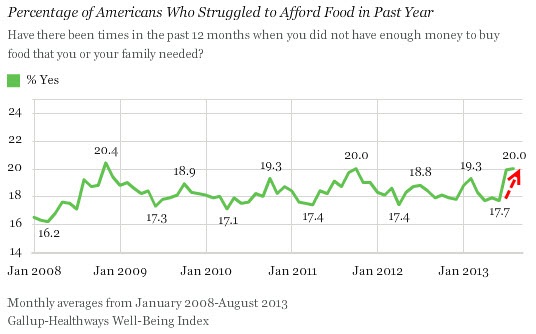

Now personally, I’ve got a huge problem with all of this, but this is the world of Keynesian ‘economics’ at the micro level. The government does it and gets away with it, why can’t we? The final graphic explains why. Think about how much higher these numbers would be if we didn’t have the government breadline program called food stamps?

Now, all the talk of the new housing boom and surging equity markets aside, how wealthy are we really? Remember, at the end of the day, the wealth effect is nothing more than what it says. It is a perception, not reality.

********

Andrew W. Sutton, MBA Chief Market Strategist Sutton & Associates, LLC www.sutton-associates.net[email protected]