What Is A Bank…And What Is A Commercial?

Even this basic question has been made deliberately opaque by the co-conspirators at the CFTC.

Much has been made recently—and rightfully so—of the ongoing extremes being reported within the weekly, CFTC-generated Commitment of Traders report. This report, which summarizes the positions of "Speculators" and "Commercials" within the COMEX gold and silver markets, currently shows relative positions not seen in decades, if ever. As such, there are plenty of reasons for optimism and a hope for higher prices ahead. However, this may not be the "slam dunk" many analysts have projected, and it's critical that you understand why.

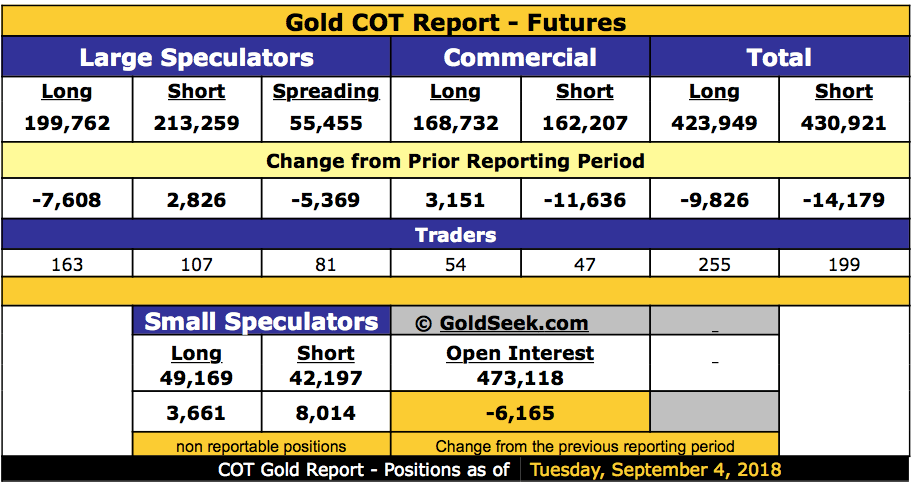

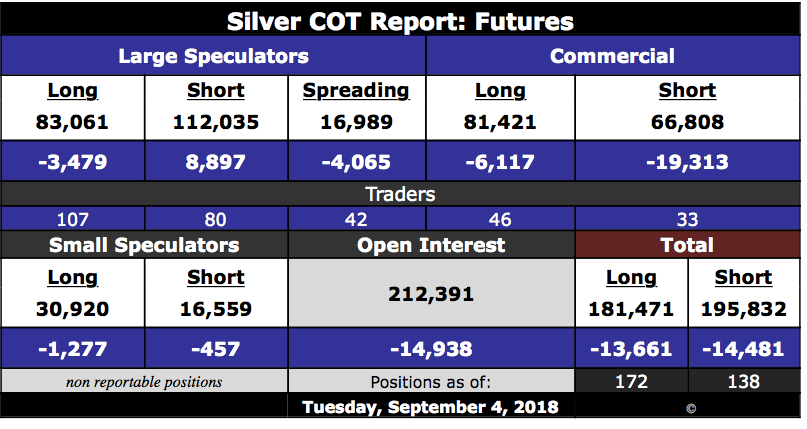

First of all, and as stated above, CoT positioning currently appears to be at extreme levels. The "Commercials" in both COMEX gold and silver are NET long—meaning they are long more contracts than they are short. For COMEX gold, this is the first time the Commercials have been net long since 2001. For COMEX silver, this is the first recorded Commercial net long in the history of the report, dating back to 1986. See below:

When applying the same CoT analysis that has served us well since 2006, the above setup appears very bullish. We've learned that when large positions build up, they invariably reverse. For example, in July of 2016, the Large Speculators in COMEX gold held a NET long position of over 316,000 contracts, while the Commercials were NET short over 340,000 contracts.

What happened next should have come as no surprise. Price was smashed, as Speculators rushed for the exits and dumped longs, setting off a chain reaction of lower lows. Using this same logic now leads to the conclusion that the Speculators will soon be forced to buy and cover their short position and that price will rise, setting off a chain reaction of higher highs.

And this might be the case. However, one critical factor seems lost in the translation here. Traditional CoT analysis was helpful when positioning was at extremes, with each side heavily long or short. Though today's positioning is historic in its position-flipping, by no measure is it "extreme". Instead of 300,000+ net positions, the sides are almost equal. The Large Specs in COMEX gold are net short 13,500 contracts, and the Commercials are net long 6,500. Is this "extreme", or is this a new equilibrium? Time will tell, but when viewed this way, you can see that the CoT is a far cry from being the automatic bullish signal that so many have proclaimed it to be.

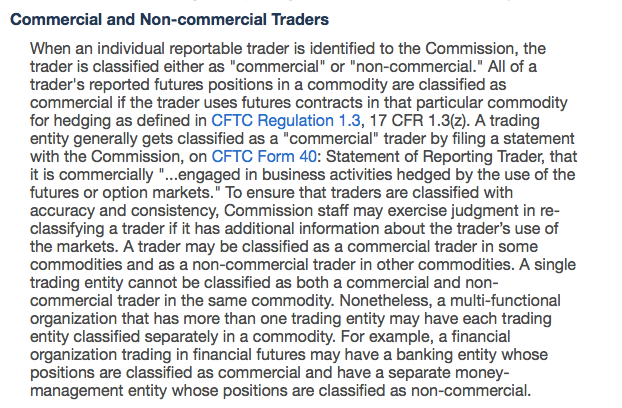

Here's the other point to consider. Over the past few days, I've seen a number of articles that falsely claim that "the Banks are now long" and that "JPMorgan is now on our side". Let me make this perfectly clear: There is nothing in the CFTC data to justify these statements. Maybe a few Banks are stealthily getting long, and maybe some others are using this Spec shorting to square off their risk. However, the actual CFTC-reported data does not allow for these blanket conclusions and statements.

Why? See for yourself. Below is a snapshot taken from the CFTC's own website. This is the official explanation of what is considered a "Commercial" trader and what is not:

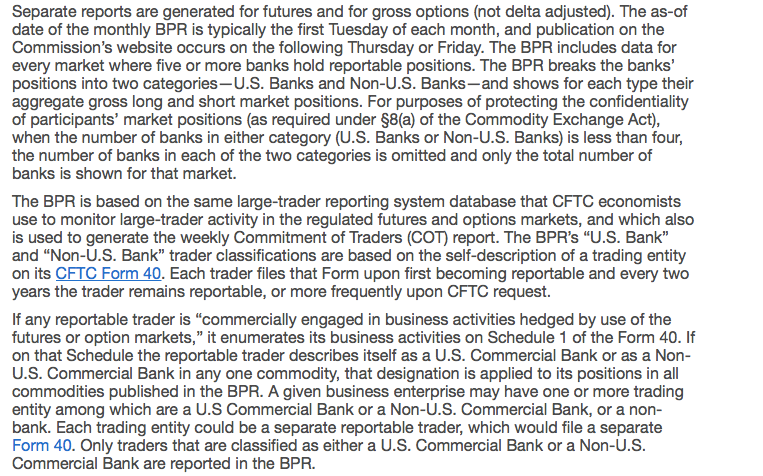

And this, taken from the explanatory notes of the monthly Bank Participation Report, attempts to explain the procedures for extracting the BPR data from the first CoT survey of every month:

As you can no doubt see, the CFTC has deliberately designed this to be opaque and confusing, particularly for the average investor or trader. The only thing that can be surmised is this:

• All Banks are Commercials, but not all Commercials are Banks

And that's about it.

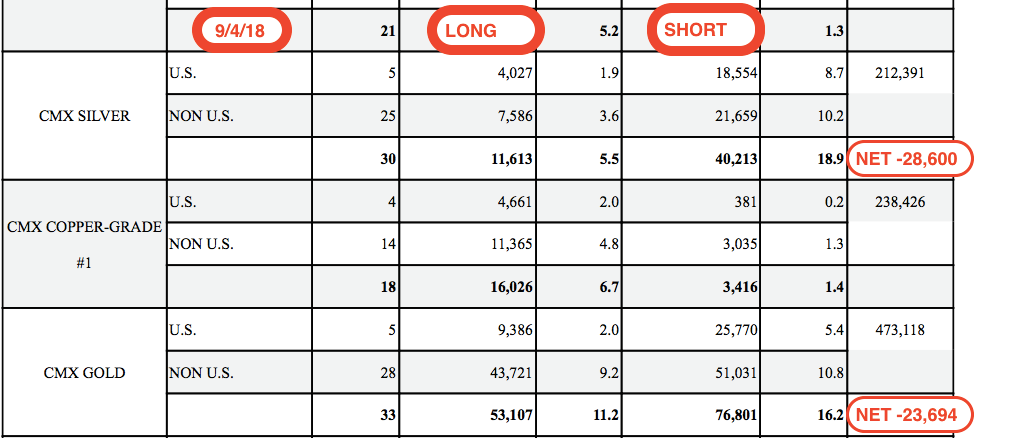

So, what does the latest Bank Participation Report reveal? While the current net positioning of the 30+ Banks that make up the report is relatively small by historical standards, these Banks are definitely NOT net long. See for yourself:

In the end, gold and silver prices may/should rally as the massive Speculator short positions get bought back and covered. Unlike the Bullion Banks, the Speculators have no gold to deliver, and they do not have infinite funds to meet the margin calls that will come with higher prices.

But a cycle of higher prices will only begin with a spark from a falling dollar, falling interest rates or a stronger yuan. Expecting a rally simply because of CoT positioning—or an alleged Bank long position—is not only wishful thinking, it simply isn't based in reality... at least as stated within the actual, CFTC-generated reports.

The views and opinions expressed in this material are those of the author as of the publication date, are subject to change and may not necessarily reflect the opinions of Sprott Money Ltd. Sprott Money does not guarantee the accuracy, completeness, timeliness and reliability of the information or any results from its use.You may copy, link to or quote from the above for your use only, provided that proper attribution to the author and source is given and you do not modify the content. Click Here to read our Article Syndication Policy.

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.