When What We See Makes No Sense

We perceive the world around us through glasses that are colored by our previous experiences, or likes and dislikes and very much so, our prejudices. Yet there are certain guidelines for our attempts to make sense of what we see and hear that as a rule are accepted by most people. We all agree that prices in markets are determined by supply and demand, irrespective what it is that drives demand. We respect the use of common sense in making sense of what is happening, even in instances when what happened is not common, so that an event appears to be out of the ordinary.

We know from what has happened in the precious metal markets since at least 1996, in the case of gold, that the PM market is not behaving as one would expect from the interplay between supply and demand. Supply in the mining sector as a rule is steady over time, with few if any sudden and generally brief spikes, whether up or down. As demand over time, again as a rule, is relatively steady, it could be expected that price changes occur at a steady and rather slow rate.

The fact that we regularly observe sudden and sharp changes in the price is therefore out of the ordinary – events that do not fit the common sense expectations of a world view that assumes markets are free and unfettered. It is when we observe events that run counter to our common sense expectations that our cultural biases and prejudices come to the fore. These are powerful forces that dictate how we interpret everything we observe and at which conclusions we arrive.

If one happened to live in some Asian countries, the realisation that the main dish at the meal to which our friends have invited our family will be dog meat, would make us lick our lips and we would be looking forward to a delicacy. Here in the US, none of us would expect to have Rover for lunch. Cultural likes and dislikes are seldom as conscious decisions made by the individual; these are absorbed as if by osmosis from the particular herd in which we live. It is a societal instinct that directs our behaviour, which we have to obey, or risk being ostracised by ‘the herd’ – which is a strong motivator to conform, come what may.

One conditioned reflex in markets is that when there is inflation, bond yields increase – bonds lose value, because the return of owning a bond is well into the future, when a higher inflation has eroded the value of the money that will be received. The yield on the US 10-year treasury note bottomed at 0.512% in early August last year. Then it increased at a steady rate that suddenly started to accelerate late in January as it became obvious that money printing was going into a higher gear. A reaction that is normal and expected.

The yield rose steeply, until reaching a high at 1.74% at the end of March, more than three times higher than at the low point. Since then, the yield drifted lower with some volatility, as if struggling under two opposing nearly balanced forces – one bearish and inclined to resume the trend to a higher yield; the stronger force taking the yield inexorably lower. Last week had the yield higher from 1.454% a week ago, to a high of 1.581% on Wednesday and then back to close the week at 1.443% - substantial swings in what is touted as the biggest single global market (Bitcoin?) that represent a clash between major market forces. The unexpected bond rally is counter-intuitive; it does not fit our expectations, yet there has to be a logical explanation.

Expectations of higher inflation also affect the value of the dollar. Holders of dollars as a reserve of some kind, will reduce the amount they have to limit the loss in value they otherwise will suffer over time. This should result in lowering the value of the dollar on the forex markets, as reflected in the dollar index. The dollar index reached a spike high in March last year, as mounting fears of Covid sent a flood of money into a traditional safe haven. Since then it has been in near constant decline, until early January, when it rallied again – peaked at the end of March, declined and then rallied again during the past two weeks. Since November last year it has been essentially sideways, but with a great deal of volatility – also signifying strong opposing forces.

One explanation for the rally in the 10-year Treasury and the recent period of mostly a strong dollar – also against expectations in a climate of higher inflation – would be if foreigners had become buyers of Treasuries and, by doing so, were purchasing dollars to fund their acquisitions. If this is what is happening, these markets would conform to what our common sense will expect.

However, can it really be the right explanation? Will foreigners buy dollar denominated assets when both the currency and the asset are expected to lose value at a time when higher inflation is looming? Really? Logic and common sense say that previous trends in bonds and the dollar, when both were bearish, more properly reflect the expected behaviour of foreign investors. This turnaround represents a cognitive dissonance; a condition when what one observes does not fit what is known and proper.

When knowledge and experience no longer explain what is happening, prejudices and cultural truisms are called up to bring about normality and acceptance of the state of the world. Yet, while a majority of people would put on blinkers to disregard evidence that makes no sense in the accepted world view, there will always be others who probe deeper and reach conclusions that the world is not really as it is being described by the majority. We are well aware of this in relation to the PM markets.

Commentators and the media in general disregard the regularity of strangely timed events in the gold and silver markets. When these are so blatant and obvious they have to be noticed, some silly reason is employed to explain what happened. The hard evidence of intervention is glossed over, because the herd’s world view discounts the possibility of officially sanctioned meddling in “free markets.” In similar fashion, the possibility that the Exchange Stabilisatuion Fund (ESF) or another agency might be responsible for the behaviour of the dollar and the yield – surely the Federal Reserve would not do so? – is not likely to appear in any headline.

No doubt some will say that the bond rally is a normal consequence when Wall Street comes under selling pressure. It always happens when equities top out after a bull market that investors switch into bonds as the natural safe haven. However, that does not explain the recent counter-intuitive strength and volatility in the dollar. The world remains a mysterious and interesting place and is becoming more so.

We are getting closer to an answer to the question of what Basel III will do to the PM markets. This while we are in the midst of another major Cartel panic of the scale that we saw in April 2013 and in March 2020 and – for silver – when the Cartel had to deal with a large number of silver options that had come into the money and were on the verge of being converted into futures. These are all major events in the PM markets that at the time attracted no meaningful attention from the main herd and this will continue to be so until the day when the true facts will make headlines.

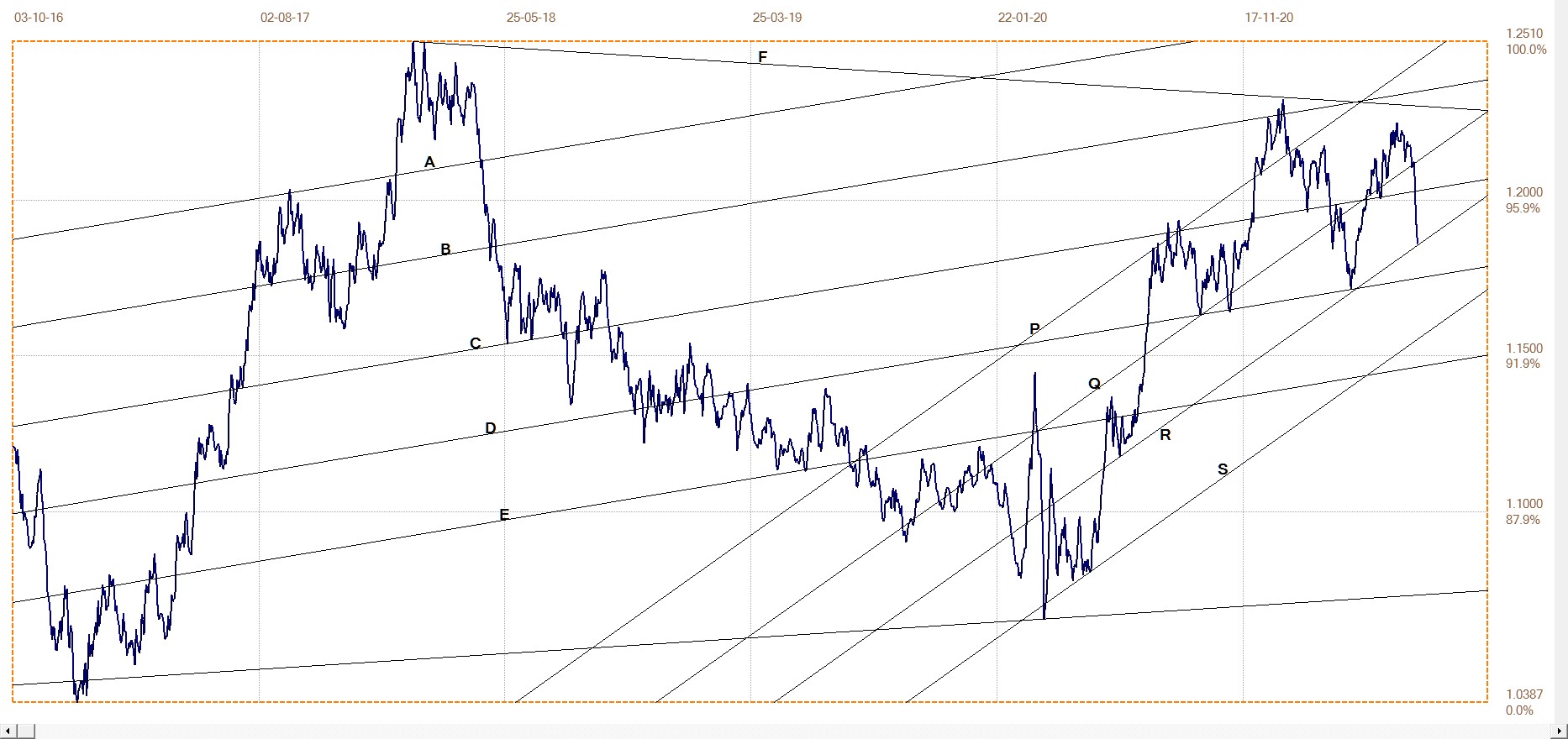

Euro–Dollar

Euro–dollar, last = $1.1860 (www.investing.com)

The steep sustained rally in the euro since its low during the whipsawing last year when the pandemic had markets in a twirl, has now settled more or less sideways in a shallower bull channel. The new dollar rally ended the recovery in the euro after the rebound off line D with a steep decline back to line R. If line R fails to hold, there is still potentially more downside for the euro before it tests the bottom on the channel at line S. That would also require a break below support at line D, which has held firm on three previous occasions.

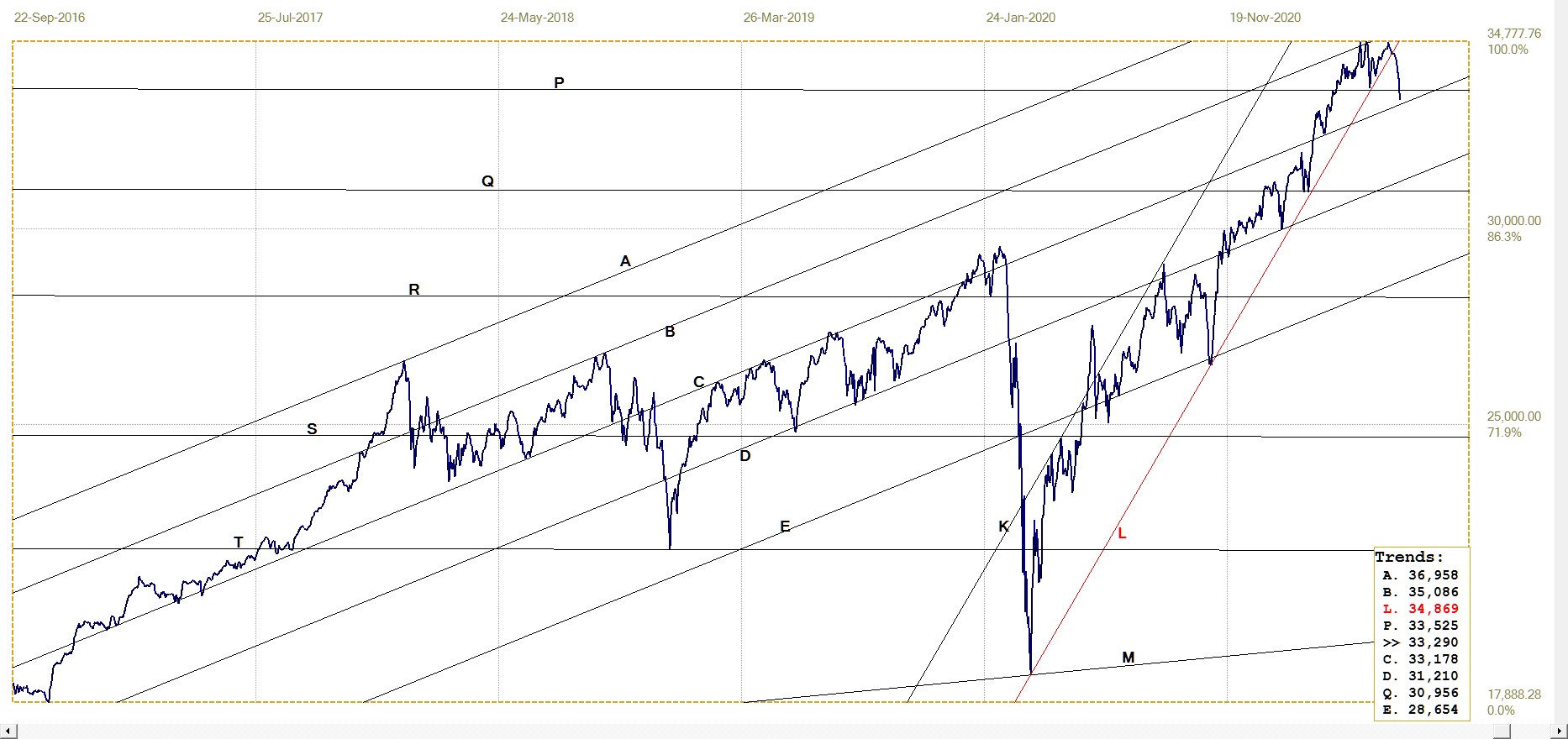

DJIA daily close

DJIA. last = 33290.08 (money.cnn.com)

Last week was the first time in ages that Wall Street closed lower on each day – five in a row, after the previous week when the DJIA was mostly range bound, but ending on a firmer note. Given the sustained support for Wall Street in recent history, it will be premature to call this sequence the start of the long awaited and widely discussed bear market. The age of miracles is not yet past, but it would nevertheless surprise to see Wall Street rally anew from here.

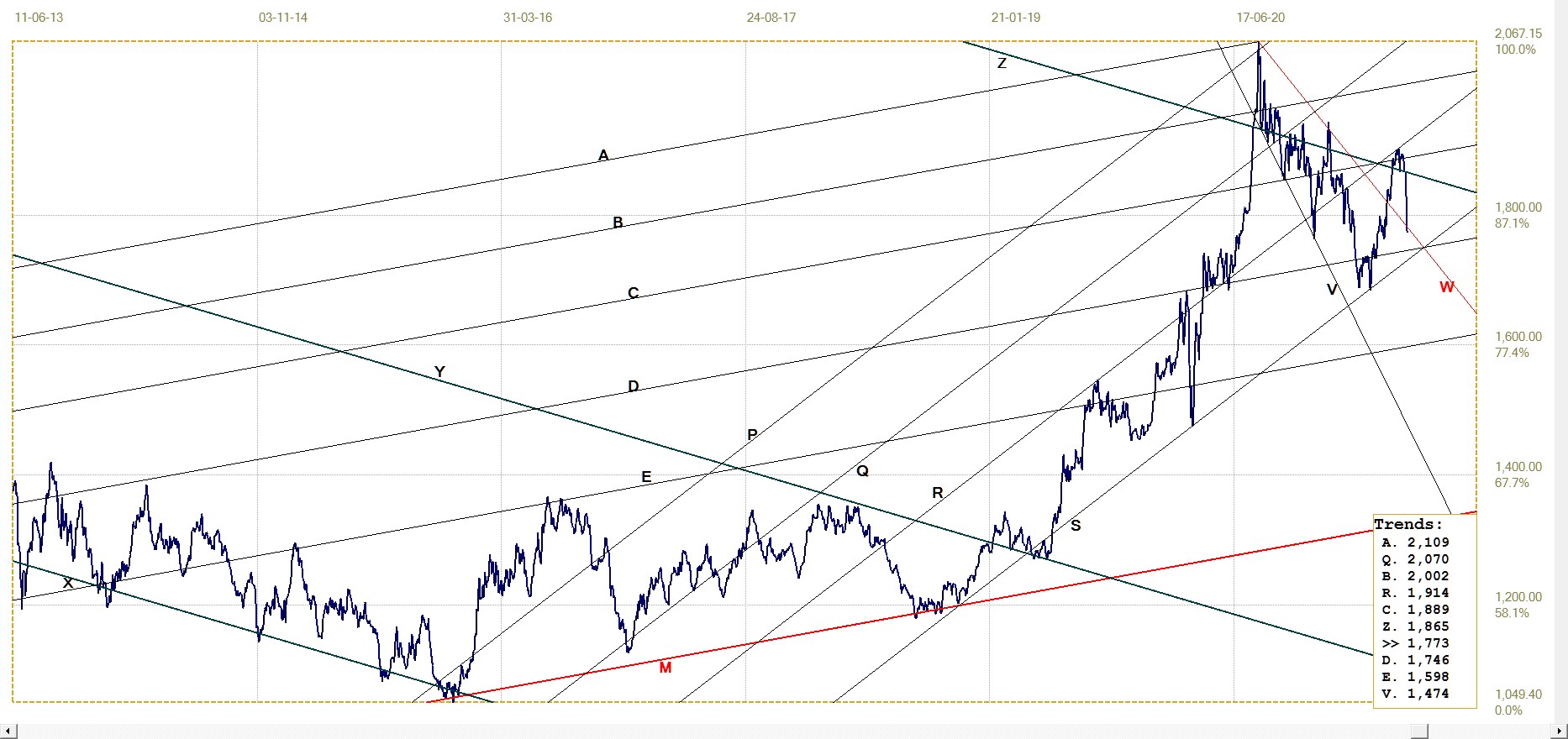

Gold London PM fix – Dollars

Just when the price of gold was getting to grips with resistance at lines R, C and Z to extend the rally off line S, the bottom fell out. Last week was a real disaster for the PM market, on a scale that has few precedents. There was the near calamitous $200 decline in April, 2013, and a few other occasions where the gold price lost more than $100 in a week, such as when the pandemic struck in March last year.

These events occur when unexpected events plunge the Cartel into a panic. They act to force the price lower, even if such a steep decline without a real and obvious reason could attract attention from the CFTC (not that this normally would be a problem; but in today’s climate where one can be canceled at the drop of a hat, it is not wise to take unnecessary risks). Of course, they won’t broadcast the reason for the panic.

After letting the price of gold improve gradually during early June, this sudden clamp down, quite early before the July options and futures come into play, comes as a bit of a surprise. Could it be that the Cartel see danger signs ahead – either from the end of the month or from a decline in available gold or silver? Time will tell.

Gold price – London PM fix, last = $1773.10 (www.kitco.com)

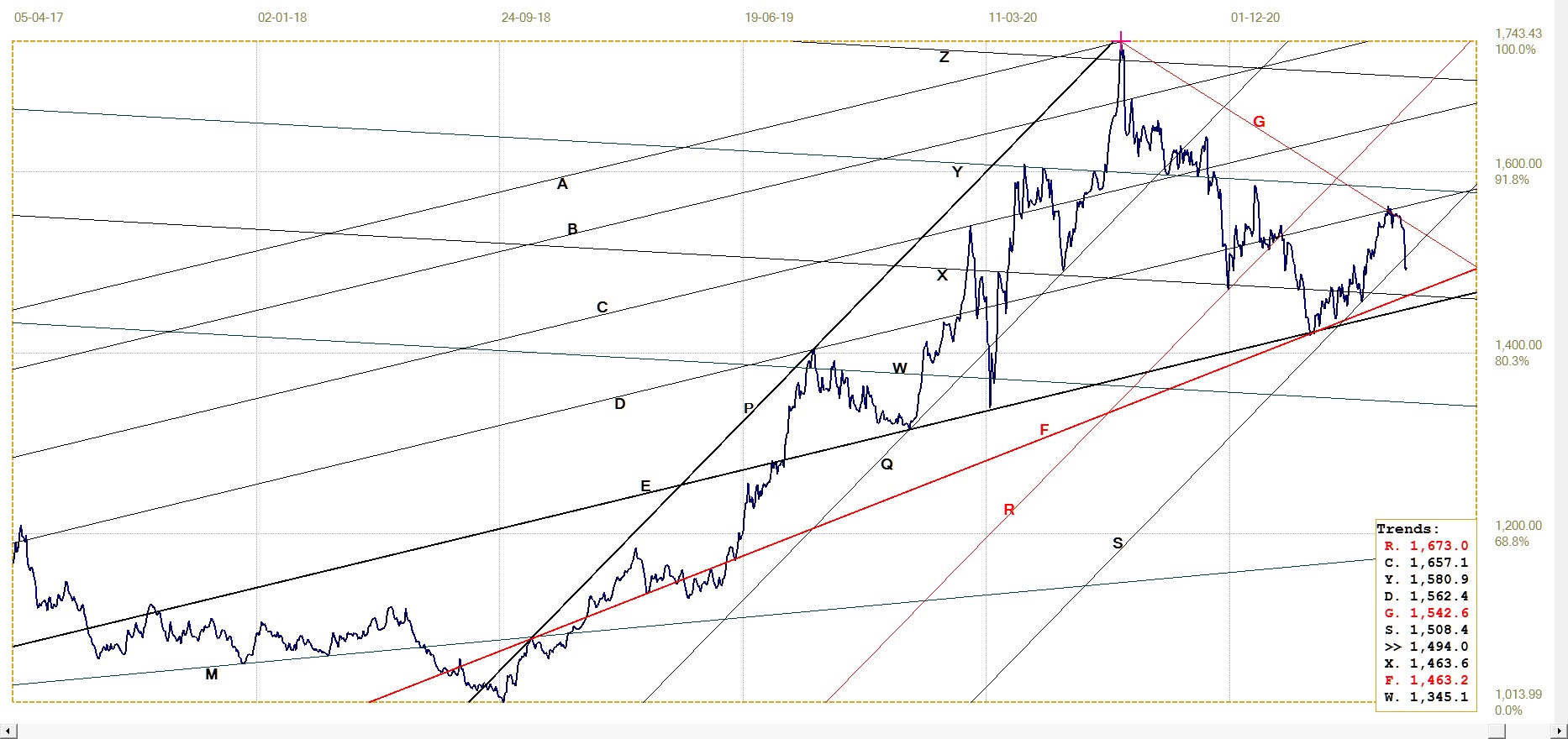

Euro–gold PM fix

Euro gold price – PM fix in Euro. Last = €1494.01 (www.kitco.com)

The initial steep rally of the euro price of gold in channel PQ could not be sustained – the dollar price of gold lagged, while the firmer euro handicapped the euro gold price. The sideways and lower trend established a broader and shallower bull channel, as well as two potential megaphones – PE and PF. Despite the sharp decline in the euro price of gold – the decline in the dollar price not being off-set by the weaker euro – the two megaphones are still intact.

Such chart formations typically enclose steep and sustained trends as is evident from the way the euro gold price has behaved in recent years. It implies a promise that as long as the megaphones remain intact, a new and steep rally in the euro price of gold is waiting to take hold. Such an event most likely would require both a strong dollar price as well as a weak US dollar.

Silver Daily London Fix

Silver daily London fix, last = $26.585 (www.kitco.com)

The chart clearly shows how silver has repeatedly been trying to again break above the price ceiling at $28. The final attempt ended with the steep decline that has now for the second time broken below the steep bull channel, JKL. Line X shows that the extent of the break below the channel on Friday reached the same degree as before, at the end of March. That was when the large position in options threatened to make a dent in the profitability of the Big Banks and they acted to prevent such a loss.

It remains to be seen whether support at line X will hold again; this time the attack on silver started early enough to continue for longer than a week before the end of the month and the end of the half year. It will be major vote of confidence in silver should the extended channel JKLX manage to contain the bull trend.

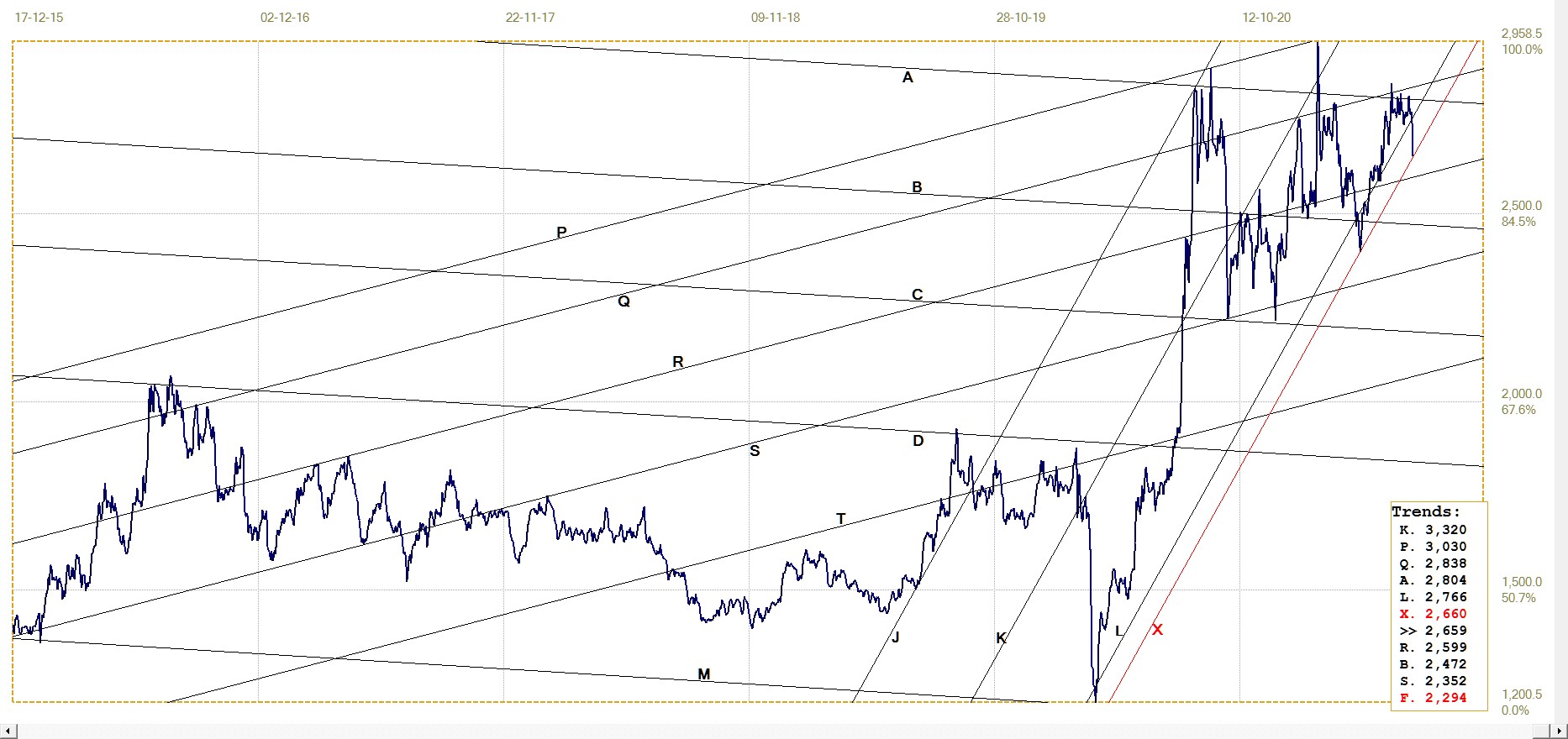

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 1.443% (www.investing.com )

The chart clearly shows the new enigmatic rally that was discussed earlier. If channel JKL is to hold and continue to contain the bear trend, line L, currently at 1.33% and increasing rapidly, sets a lower limit for the new rally. The high volatility in the yield last week is a somewhat rare occurrence; normally the yield either holds to a steady trend or it becomes quite tightly range bound.

This week should reveal whether the forces responsible for the volatility have abated and, if one were to become the victor, what the new trend would be. If the latter, the obvious outcome in this instance should be to resume the bear trend. Inflation is here to stay and increase, so that the yield should take notice.

West Texas Intermediate crude. Daily close

Speaking of inflation, the price of crude is creeping higher – at a slow pace as if the price is struggling against resistance. The initial rally in the price, mostly holding in channel KL, consolidated around line R, as if reluctant to continue higher. During June the rally resumed, the price increasing in small but consistent steps to reach a high on Tuesday and then pulling back slightly.

The cost of energy contributes to price trends across the whole economy, irrespective whether the trend is towards higher or lower prices in general. Recently, the price of energy has been an inflationary influence and while channel KL holds, this trend is set to continue. A significant reversal in this trend is required to provide evidence that inflation is to be a transitory phenomenon, as the Fed and others maintain.

WTI crude – Daily close, last = $70.91. (www.investing.com )

© 2021 daan joubert.

********