Why Gold? Why Now?

Precious metals have been on a tear this year and that is no surprise considering the current political climate south of the 49th parallel, and the geopolitical tensions throughout the globe, particularly Israel-Iran missile strikes and the ongoing war between Russia and Ukraine.

We also can’t forget the South China Sea. China is sending aircraft carriers out into the Pacific and making big waves against Taiwan.

A standoff occurred on Wednesday between the Chinese and Philippine coast guards off the Philippine province of Palawan. Three Chinese coast guard ships challenged a group of Philippine vessels about 60 miles offshore — well within the country’s 200-mile limit.

The Chinese ships took umbrage to the Philippine Coast Guard escorting what appeared to be a fishing vessel into waters south of Half Moon Shoal, an atoll west of Palawan and on the edge of the contested Spratly Islands archipelago. (Newsweek).

China claims 80% of the South China Sea as its territory.

Incidents like these — wars, territorial disputes, and bad economic news such as inflation, low economic growth or a pending recession — normally push investors towards safe havens like gold and silver along with government bonds, particularly US Treasuries, and the US dollar.

Gold has certainly benefited from safe-haven demand, rising about 27% year to date. Silver on Tuesday and Wednesday rose to levels not seen since 2012.

YTD gold. Source: Kitco

YTD silver. Source: Kitco

But something different is happening this year, and it has to do with the Trump’s administration’s aggressive trade policy — levying hefty tariffs against its trading partners whether friend or foe — and insularity.

Indeed CNBC notes that gold, silver and platinum have all posted big YTD returns as issues from market volatility to de-dollarization of central banks and the US deficit favor the metals market.

The publication says gold, silver and platinum have all beaten traditional safe havens the dollar and Treasuries, offering this explanation for why:

What’s taking place is a combination of the safe-haven trade occurring at the same time as concerns about the U.S. deficit and the de-dollarization wave among foreign central amid political shifts since President Trump’s election and a global realignment of interests.

Year-to-date, the two biggest gold ETFs, SPDR Gold Shares and iShares Gold Trust, have taken in over $11 billion — showing that the so-called “paper gold” market is alive and well.

However, while gold in previous bull runs was supported by retail investors, let’s face it, gold is expensive, and many are sitting this one out; some may be buying or waiting to buy on the dips. But higher prices aren’t stopping institutional investors, particularly central banks.

Central bank buying

The World Gold Council says gold is attracting more attention from central banks than at any time in the last decade.

In its annual central bank gold survey, published Tuesday, the WGC said 95% of respondents expect global gold reserves to increase over the next 12 months. 43% of central bank reserve managers said they plan to increase their gold holdings this year, compared to 29% in last year’s survey. (Kitco News)

Over the past three years, central banks have purchased over 3,000 tonnes of the precious metal. Analysts predict they could add another 1,000 tonnes to their reserves this year.

Demand is largely being driven by emerging market central banks, which are diversifying their holdings away from the US dollar, more so than developed market central banks.

According to Kitco, while the dollar is expected to maintain its status as the world’s reserve currency, central banks foresee a diminished role for it:

Specifically, 73% of central bank reserve managers anticipate moderately or significantly lower U.S. dollar holdings within global reserves over the next five years. Meanwhile, 76% of respondents believe that gold will represent a moderately or significantly larger share of total reserves five years from now, up from 69% in last year’s survey.

Another interesting development: Last week a report from the European Central Bank said gold overtook the euro to become the second-largest reserve asset held by central banks. (the dollar being #1)

US assets sell-off

As central banks back up the truck for gold, they are shrinking their US asset exposure, and not only to dollars.

According to the New York Fed’s latest ‘custody’ data, via the Globe and Mail, there has been a steady decline in the value of Treasuries and other US securities held on behalf of foreign (non-US) central banks.

Last week, the value of US Treasuries held at the New York Fed on behalf of foreign central banks fell to $2.88 trillion — the lowest since January. When mortgage-backed bonds, agency debt and other securities are included, the total value of foreign central banks’ US custody holdings at the New York Fed dropped to US$3.22 trillion, the lowest since 2017.

That figure has fallen by around $90 billion since March. The article directly links the $90B reduction to Donald Trump’s ‘Liberation Day’ tariffs on April 2, which swiftly tanked US stock markets and sent bond yields soaring. More than half the decline came from US Treasuries.

Meghan Swiber, director of US rates strategy at Bank of America, says the fall in custody holdings is a warning sign.

“We worry about foreign demand going forward,” Swiber wrote on Monday, pointing out that it’s unusual for reserve managers to reduce their US Treasury holdings when the dollar is weakening. “This flow likely reflects official sector diversification away from dollar holdings.”

More analysis of the New York Fed’s custody holdings was done by Fortune Magazine in an article re-posted by Yahoo Finance.

The article says that Treasuries and other assets in the custody of the New York Fed from more than 200 central banks and other foreign entities like sovereign wealth funds declined by $17 billion last week and have fallen by $48 billion since late March.

Foreign holdings of US Treasuries hit a record $9.05 trillion in March.

A pullback in bond buying from central banks could send borrowing costs higher, putting the US government in a jam. Foreign buyers represent 30% of the $28.6 trillion US Treasury market. If they no longer see Treasuries as a safe haven, the Treasury would be forced to pay higher yields on bonds to attract buyers. That would put upward pressure on interest rates for mortgages, small-business loans, and other types of borrowing, Fortune states.

Interest payments on the US debt topped $92 billion in May, surpassing every other federal expense except Medicare and Social Security. (Citizen Watch Report). More on deficits and the debt below.

Dollar exit

The decline in the value of the US dollar is, so far, one of the most newsworthy trends of 2025, along with the Trump tariffs.

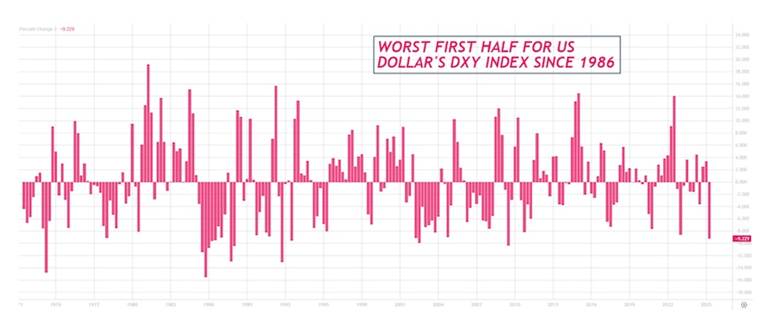

The US dollar index (DXY), which reflects the dollar’s value against a basket of other currencies, is down 10% year to date. According to Reuters, this marks its steepest first-half loss since 1986, when the greenback was still reeling from the 1985 “Plaza Accord”.

(Signed on Sept. 22, 1985, the Plaza Accord was an agreement among France, West Germany, Japan, the United Kingdom, and the United States to depreciate the US dollar in relation to the French franc, German Deutsche mark, Japanese yen, and British pound sterling.)

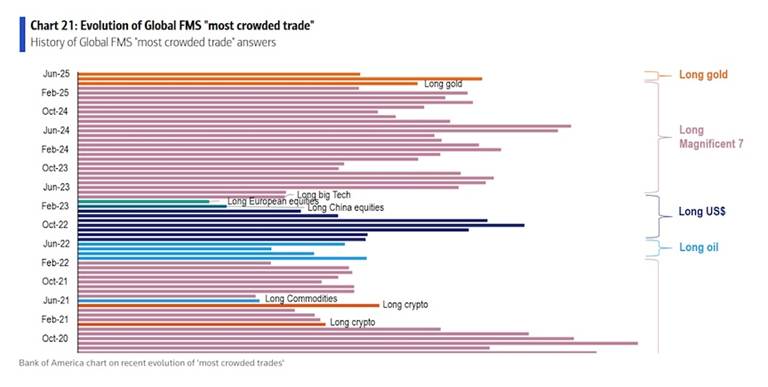

This month’s global fund manager survey from the Bank of America showed the net underweight position in the dollar is the largest in 20 years. Moreover, “short dollar” was among the top three “most crowded trades”, just behind “long gold” and “long Magnificent 7” stocks.

Reuters columnist Mike Dolan says the 20-year high in dollar underweighting by asset managers indicates both wariness of U.S. assets at large – due to concerns about the current U.S. administration’s approach to global trade, geopolitics and institutional integrity – and a more structural dollar retreat.

He quotes Vincent Mortier, chief investment officer at Amundi, saying, “The name of the game will be diversifying away from the U.S. and into European and emerging market bonds.”

Carlyle’s Jeff Currie believes the historic developments weighing on the dollar are related to long-term geopolitical shifts, defense and energy considerations.

The basis of his framework is that the U.S. retreat from international engagement – or its arm’s-length engagement, as seen over the past week in the Middle East – is making the world more dangerous and more expensive. Tariffs and capital costs are rising, while liquidity is draining.

The net result is a weaker dollar, higher commodity prices and a demand for “asset-heavy” sectors like defense…

Shifting trade patterns

Donald Trump has boldly imposed a new era of US economic policy dominated by tariffs, trade wars, and threats to the sovereignty of nations it has long considered allies (Canada, Denmark, Panama), as the second-term president aims to rewrite the rules of international trade mostly by disregarding them as he pursues an America-first agenda.

The cost to the United States of Trump’s trade war and “country takeover” rhetoric has already cost America its reputation.

Countries are realizing the US is more a liability than an asset and are looking to do business amongst themselves rather than rush into new trade agreements with the United States.

Canada provides a good example. Prime Minister-elect Mark Carney has vowed to use Trump’s anti-free trading stance to re-imagine Canada’s economy. Initiatives such as reducing inter-provincial trade barriers, building new pipelines, and fostering trade relationships with countries other than the United States are on his agenda.

New data from the Port of Montreal reveals the latter is already happening. Perhaps surprisingly, given Canada’s prickly relationship with China under former PM Justin Trudeau, trade with the Asian superpower is increasing.

The Globe and Mail reports Montreal, Canada’s second-biggest port behind Vancouver, has logged a 77% surge in two-way cargo traffic with China in the past few months, with a 22% gain in outbound shipments (i.e., exports).

And it isn’t just China. Cargo volumes from Montreal to Spain are up 147% year-over-year through May, up 11% to the Netherlands, and are 10% higher to Northern Europe.

On the other side of the country, China has become the largest buyer of Canadian oil, shipped on the Trans Mountain pipeline and loaded onto tankers on the West Coast.

The newspaper goes on to explain:

U.S. President Donald Trump has upended decades of trade ties between Canada and the United States by imposing import tariffs on aluminum, steel and other products and calling for the annexation of Canada. As companies review their business strategies and logistics in response, a growing number are reducing their reliance on the U.S. and turning to Europe and other overseas markets.

The debt

The Congressional Budget Office has projected a federal budget deficit of $1.9 trillion this year, and federal debt rises to 118% of GDP in 2035, according to the CBO.

The national debt currently stands at $36.2 trillion.

Source: FRED

In a post on X, the Times of India quotes Elon Musk, who wrote, “If [the Trump administration’s mismanagement of the economy] continues, America goes de facto bankrupt and all tax revenue will go to paying interest on the national debt with nothing left for anything else.”

The Tesla CEO quoted another X user who posted: “How did we arrive at a point in this country where 25% of all tax revenue goes to just paying the interest in $37 trillion in govt debt?”

The user backed the 25% figure up by noting that annual US government revenue is about $5 trillion, with interest on the debt currently around $1.2 trillion.

As the chart above shows, America’s national debt has risen from $1 trillion in the 1980s to $36 trillion in 2025.

Citizen Watch adds more detail to this sombre picture. In May alone, it says the government collected $371 billion in revenue, but spent $687 billion, leaving a deficit of $316 billion.

The annual deficit is already $1.365 trillion, 14% higher than last year.

Billionaire bond investor Jeffrey Gundlach warns “A reckoning is coming,” pointing to the unsustainable trajectory of US Treasury debt. Investors are starting to question whether long-term government bonds are still a safe haven.

Citizen Watch concludes: The debt crisis isn’t looming, it’s here. Are you paying attention yet? Permanent deficits are a global reality, fiat is losing its value, and the only true safeguard is owning real money is gold.

Conclusion

I agree. Owning the physical metal, and a few well-placed juniors exploring for it, is a means for both portfolio diversification and a chance to leverage the rising gold price.

The surprising thing to me in all this is how complacent consumers and investors are in the face of global turmoil. If Iran were to close the Strait of Hormuz it would instantly spike oil prices causing widespread global economic chaos.

United States involvement in joining Israel to attack Iranian nuclear facilities risks widening the war. There are up to 50,000 US troops stationed at around 19 locations across the Middle East. These bases could easily become targets.

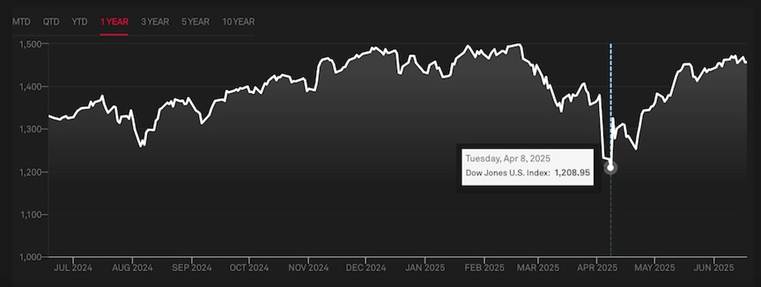

Yet consumers and investors are complacent. The CBOE Volatility Index (VIX) hit a one-year high of 52.3 on April 8, coinciding with Trump’s “Liberal Day” tariffs, but it has since settled to 21.6.

The S&P 500 and the Dow Jones Industrial Average both slumped to one-year lows at the same time but have since bounced back.

Consumer spending has been on a steady upward clip since the second quarter of 2022.

VIX. Source: Trading Economics

US consumer spending. Source: Trading Economics

S&P 500. Source: S&P Global

Dow Jones Industrial Average. Source: Google

If consumers see bad news on the horizon, they aren’t showing it in their spending habits. Bond yields are coming down and wages and jobs are strong.

It’s almost like US consumers aren’t noticing the war in the Middle East. There are a lot of reasons to like precious metals but apparently war isn’t one of them. News from the battlefield isn’t as important as financial and economic news.

The Ukraine/Russian conflict is old; the Middle East has been going to boil over for decades. Arabs and Jews killing each other is not new. Iran has been getting nuclear weapons tomorrow for 20 years. Since the bombings started last Friday, gold has fallen from $3,427.89 to $3,369.02, a loss of $58.87 or 1.7%.

It may be that the media audience is tired of war in the Middle East and is assuming a truce will be reached — hence the complacency regarding consumer spending and investing.

Hero Bullion

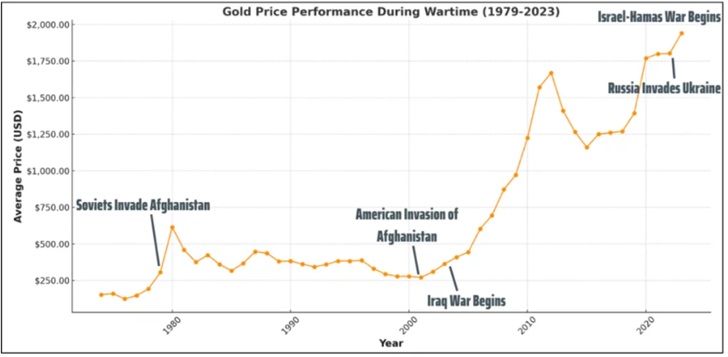

During the Vietnam War, the price of gold increased by more than 50%. Both the Soviet invasion of Afghanistan in 1979 and Russia’s 2022 invasion of Ukraine saw substantial increases in gold’s average spot price. During the Gulf War, the price of gold increased by more than 20%. During the Iraq War, the price of gold increased by more than 50%.

Of course, we can’t forget the other reasons gold has done so well, rising over 25% in each of the last two years: central bank buying, de-dollarization and de-Treasurization.

Let’s remember Elon Musk’s post on X: “If [the Trump administration’s mismanagement of the economy] continues, America goes de facto bankrupt, and all tax revenue will go to paying interest on the national debt with nothing left for anything else.”

In May alone, the government collected $371 billion in revenue, but spent $687 billion, leaving a deficit of $316 billion.

The annual deficit is already $1.365 trillion, 14% higher than last year.

The national debt stands at $36.2 trillion and will grow even more with Trump’s so-called Big Beautiful Bill.

Interest payments on the US debt topped $92 billion in May, surpassing every other federal expense except Medicare and Social Security.

Investors are starting to question whether long-term government bonds are still a safe haven, especially given the rising tide of US protectionism and the US retreat from its international commitments.

The US think the world needs them for trade when in reality, the world has other options. Canada’s bustling trade with China is one example.

A pullback in bond buying from central banks could send borrowing costs higher, putting the US government in a jam. Foreign buyers represent 30% of the $28.6 trillion US Treasury market. If they no longer see Treasuries as a safe haven, the Treasury would be forced to pay higher yields on bonds to attract buyers. That would put upward pressure on interest rates for mortgages, small-business loans, and other types of borrowing.

The US dollar index (DXY) is down 10% year to date, the steepest first-half loss since 1986.

A lower dollar is good for gold and all commodities.

A compelling part of the gold story is the best may be yet to come.

While high gold and silver bullion prices might discourage some investors, it could simultaneously create an opportunity for those who identify and invest in undervalued junior mining companies, potentially reaping substantial rewards as the market corrects its perception.

Richard (Rick) Mills

aheadoftheherd.com

*******