Will Trump End The Fed?

For many months, the price of gold has been driven by the Fed’s moves and the prospects of interest rate hikes. Therefore, the natural question after the Trump victory is how his presidency will affect the Fed’s actions and, thus, the gold market. There are several ways the Trump’s presidency may influence the U.S. central bank.

First, the new president could replace Fed Chair Janet Yellen (as well as Fed Vice-Chair Stanley Fischer), as he stated once that he “would be more inclined to put other people in”. Although Trump was critical of her, the law only permits the president to remove a member of the Board of Governors “for cause” and historically this authority has never been abused. In theory Yellen could resign, however it seems unlikely (and it would be rather uncommon in the Fed’s history). Therefore, the Fed’s leadership will probably not change until 2018, when Yellen’s and Fischer’s terms expire (in February and in June, respectively). Hence, the impact on gold should be limited, as the change will be over a period of several months and markets will manage to gradually price in.

The key issue is who could replace Yellen if Trump does not reappoint her (several names float around, including Martin Feldstein, Larry Kudlow, Artur Laffer, and John Taylor). On the one hand, Trump said at the first presidential debate that she has kept rates low for political reasons and that low interest rates have created economic bubbles. Hence, if Trump really opposes low interest rates, we will see a more hawkish Fed Chair, which is rather well not good news for the gold price market (unless faster hiking triggers a recession, which is an excellent scenario for the price of the yellow metal). On the other hand, Trump also mentioned he likes low interest rates, as they enable him to refinance the country’s debt and boost government spending on infrastructure. Therefore, although Trump-the-candidate was highly critical of Yellen, we believe that Trump-the-president may soften his positions. Even if he does not reappoint her, we do not expect radical acceleration of normalizing interest rates as it could risk recession.

Second, although the fate of Yellen is not determined, Trump may quickly influence the Fed by fulfilling the vacancies on the seven-member board of governors (as the Senate controlled by Republicans blocked a vote on Obama’s two nominees). The names of potential candidate are yet unknown, and although Trump may appoint slightly more hawkish governors, revolution is not very likely. Therefore, the impact on the gold market should be limited, but a lot depends on new governors’ views on the path of interest rates.

The third potential impact is that the Republican Congress may introduce legislation reforming the U.S. central bank which will not be vetoed by Trump. For example, some Republicans support the idea of an annual audit of the Fed’s decisions by the Government Accountability Office, an arm of Congress. Such legislation would diminish the independence of the Fed, which should be fundamentally positive for the gold market; however it does not need to translate into significant short-term moves of gold prices.

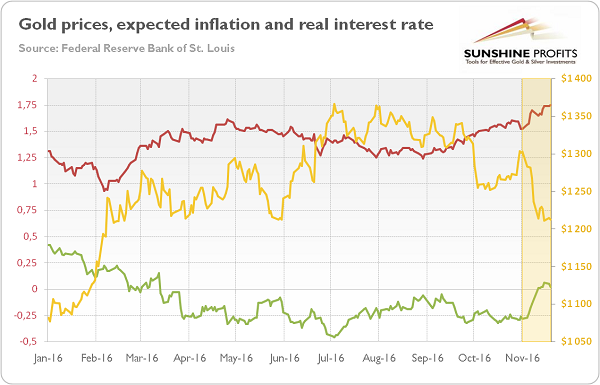

Although all these personnel and regulatory changes could be very important, the Fed’s response to Trump’s political program should be the key driver of the price of gold. So far, the Fed was the only game in town. However, with larger contribution from the government, the U.S. central bank could hike interest rates with greater freedom, considering that the more expansionary fiscal policy would neutralize a more contractionary monetary policy. It implies lifting interest rates at a faster pace, which should be generally negative for the gold market. In other words, if Trump boosts the infrastructure spending as he promised, the GDP and inflation will increase. The fiscal stimulus and higher inflation rate should give the Fed more room to maneuver, especially that the positive stock market response to the Trump’s victory enables the U.S. central bank to hike interest rates in December. Indeed, the president-elect’s calls for infrastructure spending during his victory speech have already driven up inflation expectations (derived from 5-Year Treasury Constant Maturity Securities and 5-Year Treasury Inflation-Indexed Constant Maturity Securities), as one can see in the chart below.

Chart 1: The price of gold (yellow line, right axis, London P.M. Fix), the market inflation expectations (red line, left axis), and the real interest rate (green line, left axis) from January 4, 2016 to November 22, 2016.

Theoretically, the boosted inflation expectations should lift the price of gold, since many investors consider a yellow metal (although it is often a wrong assumption) an inflation hedge. However, as chart shows, the real interest rate also rose. The jump in real interest rates (represented by the yields on 5-year Treasury Inflation-Indexed Security) – which resulted mainly from the expected increase of budget deficits and more expansionary fiscal policy – is not good news for the gold market, as the yellow metal is usually negatively correlated with the U.S. real interest rates.

The bottom line is that the Trump’s presidency may significantly affect the Fed’s functioning, and thus the gold market. The president will fill two vacancies in the Board of Governors and will probably replace the Fed’s Chair and Vice Chair in 2018 (as neither Yellen nor Fischer is welcomed by the Republicans). It means that four of the seven Fed Governors will be Trump’s appointees. Although it is unclear who would replace Yellen, quite likely the new leadership would be less dovish, which is not good news for the gold market. Moreover, the increased government spending and higher deficit expectations will probably raise real interest rates, which would put the yellow metal under downward pressure.

Arkadiusz Sieron

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017. He is a board member of the Polish Mises Institute of Economic Education, author of several dozen scientific publications (including in such periodicals as the Journal of Risk Research, Prague Economic Papers, Quarterly Journal of Austrian Economics, and Research in Economics), and a regular contributor to GoldPriceForecast.com and SilverPriceForecast.com. His two books, Money, Inflation and Business Cycles and Monetary Policy after the Great Recession, are both published by Routledge. Arkadiusz is also a certified Investment Adviser, a long-time precious metals market enthusiast, and a free market advocate who believes in the power of peaceful and voluntary cooperation of people.