Is Your Bank Safe? - A Look At Citibank

Over the last few months, we have written several articles outlining our views of banks in general. We explained the relationship that you, as a depositor, have with your bank is in line with a debtor/creditor relationship. This places you in a precarious position should the bank encounter financial or liquidity issues. Moreover, we also outlined why reliance on the FDIC may not be wholly advisable. And, finally, we explained that the next time there is a financial melt-down, your deposits may be turned into equity to assist the bank in reorganizing.

So, at the end of the day, it behooves you, as a depositor, to seek out the strongest banks you can find, and to avoid banks which have questionable stability.

While we outlined in our last articles the potential pitfalls we foresee with regard to various banks in the foreseeable future, we have not provided you with a deeper understanding as to why we see the larger banks as having questionable stability. Over the coming months, we intend to publish articles outlining our views on this matter.

First, we want to explain the process with which we review the stability of a bank.

We focus on 4 main categories which are crucial to any bank’s operating performance. These are: 1) Balance Sheet Strength; 2) Margins & Cost Efficiency; 3) Asset Quality; 4) Capital & Profitability. Each of these 4 categories is divided into 5 subcategories, and then a score ranging from 1-5 is assigned for each of these 20 sub-categories:

- If a bank looks much better than the peer group in the sub-category, it receives a score of 5.

- If a bank looks better than the peer group in the sub-category, it receives a score of 4.

- If a bank looks in-line with the peer group in the sub-category, it receives a score of 3.

- If a bank looks worse than the peer group in the sub-category, it receives a score of 2.

- If a bank looks much worse than the peer group in the sub-category, it receives a score of 1.

Afterwards, we add up all the scores to get our total rating score. To make our analysis objective and straightforward, all the scores are equally weighted. As a result, an ideal bank gets 100 points, an average one 60 points, and a bad one 20 points.

If you would like to read more detail on our process for evaluating a bank, feel free to read it here:

Our Methodology & Ranking System: Banks - SaferBankingResearch

But, there are also certain “gate-keeping” issues which a bank must overcome before we even score that particular bank. And, many banks present “red flags,” which cause us to shy away from even considering them in our ranking system.

As mentioned before, it is difficult to overestimate the importance of a deeper analysis when it comes to choosing a really strong and safe bank. There are quite a lot of red flags to which many retail depositors may not pay attention, especially in a stable market environment. However, those red flags are likely to lead to major issues in a volatile environment. Below we highlight some of the key issues that we are currently seeing when we take a closer look at Citibank (C).

Large share of revenue is generated in emerging economies

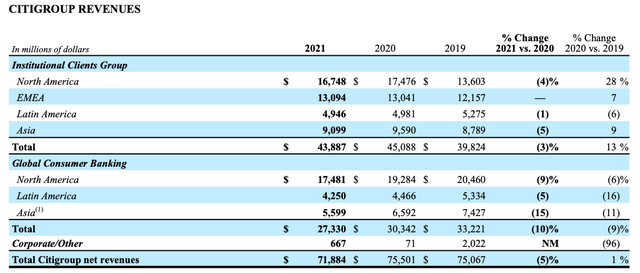

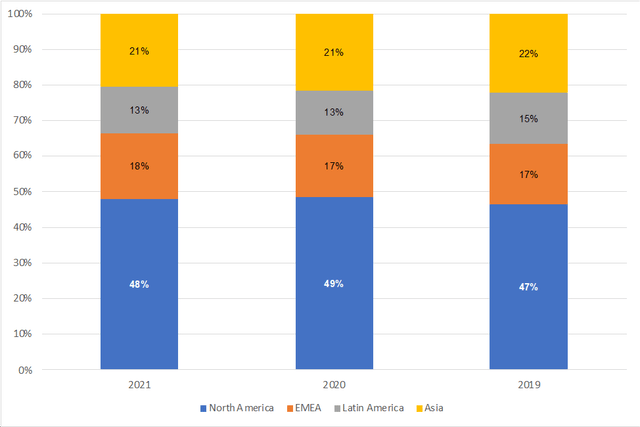

If we look at Citi’s revenue breakdown by regions, we will see that North America, which includes the U.S., Canada, and Puerto Rico, has been generating less than 50% of the bank’s total net revenues over the past three years.

As the chart above shows, more than 30% of the bank’s revenue in 2021 were generated in EMEA and Latin America. Both of the regions are considered emerging markets, which historically have been very volatile and unpredictable especially during the global recessions. Asia corresponded to more 21% of Citi’s revenue, and this business is mostly related to China, including Hong Kong. Given China has been a fast-growing economy for many years now and maintains high reliance on exports in the global trade, a potential global recession would very likely also hit China more than developed economies. As such, more than 50% of Citi’s revenue are being generated in quite volatile emerging economies. It is important to note that should a sharp global economic slowdown occur, Citi’s non-U.S. revenues will be impacted not only by a fall in lending, lower non-interest income, trading losses and securities revaluations, but also by a depreciation factor as the USD tends to appreciate against the EM currencies in a bear market environment.

High-risk loan mix with significant exposure to credit cards

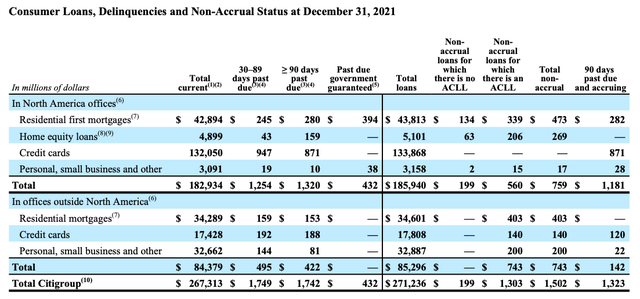

As of the end of 2021, Citi’s gross loan book was $668B, of which $271B were retail loans. Some readers might already know that Citi has large exposure to unsecured retail lending, particularly to credit cards.

But we would like to highlight that, once again, given that unsecured consumer loans are one of the riskiest business segments for a bank in a volatile environment, provisioning charges on the segment could increase dramatically. Below is a breakdown of Citi’s retail loans.

As the table shows, credit cards correspond to 56% of Citi’s total gross retail portfolio, and to 72% of its U.S retail book. Although the share of credit cards in the non-U.S. business is much lower, we note a quite high share of personal and small business loans, which is also a concern, in our view, given that these loans were granted in emerging economies.

Securities book includes large amounts of foreign bonds, equities and OTC derivatives

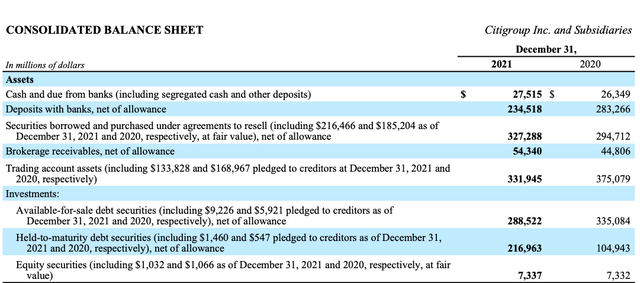

If we sum up net amounts of repo securities, trading account assets, and investments, then, as of the end of last year, Citi had almost $1T of securities on its balance sheet. For comparison, its gross loan book was $668B and CET1 capital was $149B as of the same time period.

We will take a closer look at each of these three parts of the bank’s securities portfolio.

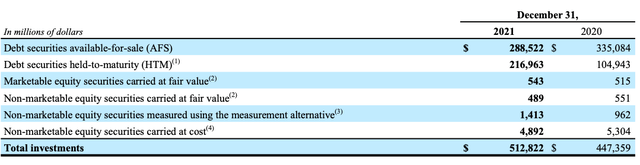

Investments, which consists of debt securities available-for-sale (AFS), debt securities held-to-maturity (HTM), and equities, were $513B as of the end of 2021.

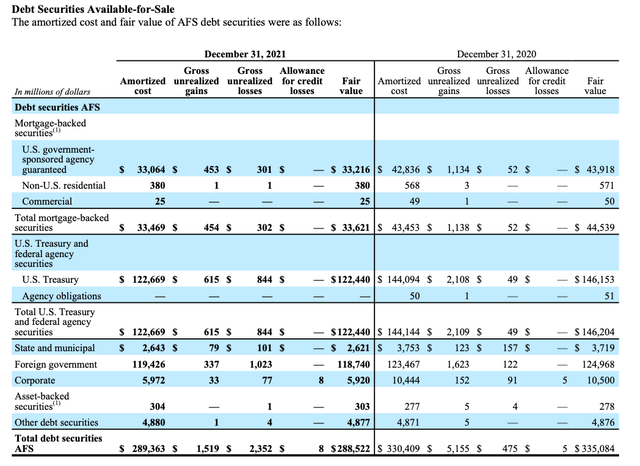

Below is a breakdown of the bank’s AFS book. While exposure to U.S. Treasuries is relatively safe and conservative, a high share of foreign government bonds, which were 41% of total AFS portfolio, does look like a concern, in our view. As a reminder, any changes in fair value of AFS book are reflected in AOCI (Accumulated Other Comprehensive Income), and, hence, while they do not affect earnings, they have an impact on capital, which, as we often say, is crucial for any bank in a volatile environment. Given that a global recessionary shock could lead to very sharp movements in foreign government bonds, Citi’s capital is at risk, in our view.

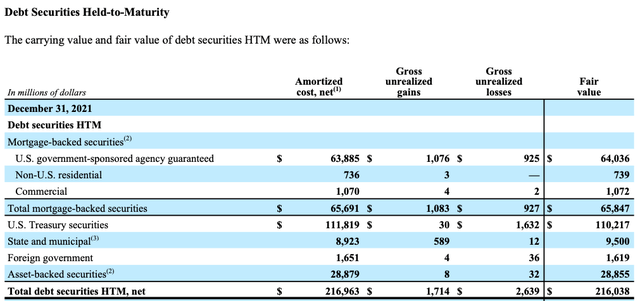

The bank’s HTM book looks more conservative as there is exposure mostly to Treasuries and MBS.

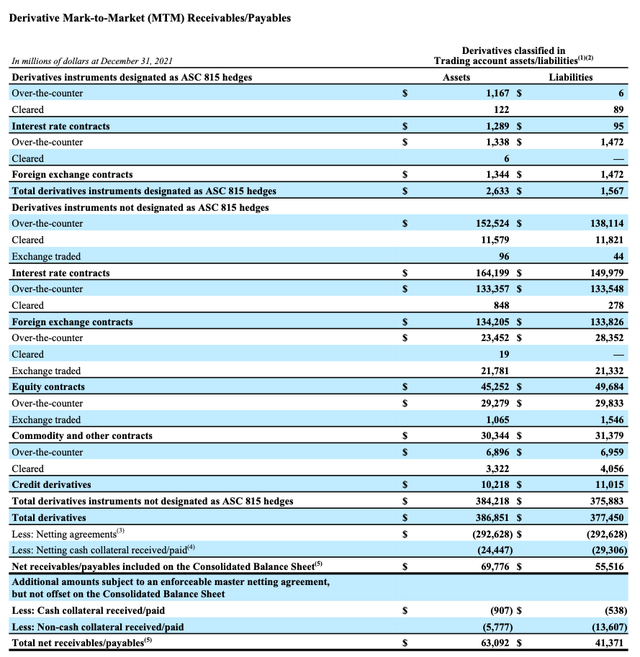

The second-largest part are trading account assets, which consist of trading non-derivative assets and trading derivatives after netting and collateral, which were $262B and $70B respectively as of the end of 2021.

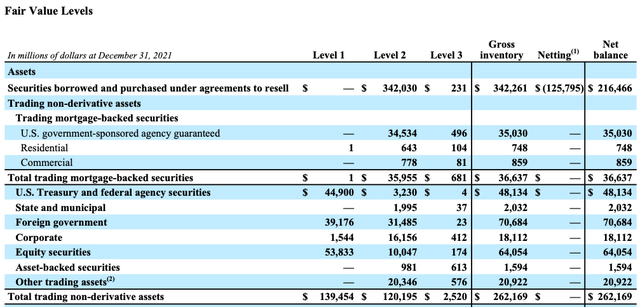

Below is a breakdown of trading non-derivative assets. As was the case with Citi’s AFS book, foreign government bonds correspond to quite a significant share: 27% as of the YE2021. Moreover, there were $64B of equities or 24% of trading non-derivative assets, as well as $21B of other trading assets, which include mostly investments in precious metals and commodities.

Trading derivatives after netting and collateral were $70B. The table shows a breakdown of these derivative MTM receivables and payables.

Our concern here is that majority of Citi’s derivatives are over-the-counter (OTC) contracts. In its 10-K, Citi made a note on the difference between OTC, cleared and exchanged derivatives:

“Over-the-counter (OTC) derivatives are derivatives executed and settled bilaterally with counterparties without the use of an organized exchange or central clearing house.

Cleared derivatives include derivatives executed bilaterally with a counterparty in the OTC market, but then novated to a central clearing house, whereby the central clearing house becomes the counterparty to both of the original counterparties.

Exchange-traded derivatives include derivatives executed directly on an organized exchange that provides pre-trade price transparency.”

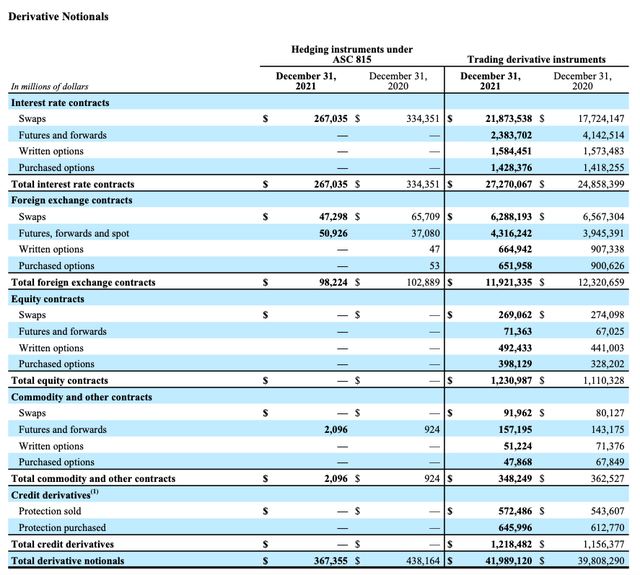

Obviously, OTC contracts are the riskiest type of derivatives, especially in a recessionary environment when there is a high chance of a counterparty default risk. Additionally, if one is really bearish on the market and expect a wave of defaults among large banks, then it is well worth taking a look at Citi’s total derivative notionals, which were a whopping $42T as of the end of 2021.

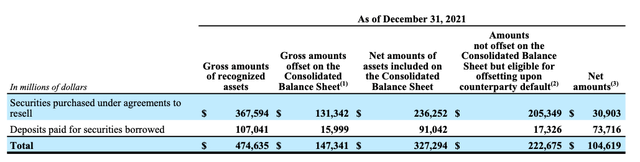

Finally, there are securities borrowed and purchased under agreements to resell or the so-called repo securities. Securities purchased under repo agreements generally do not bear any credit risks and there are offsetting amounts in case of a counterparty default; however, as shown below, there is still some net exposure, which would worth taking an eye on in a bear market environment.

To sum up, as of the end of the last year, Citi has $253B of foreign bonds and equities. This is already much higher than its CET1 capital of $149B, and this $253B figure does not include other bond instruments, net amounts of repo securities, or any derivative-related assets.

Recent Fed stress tests suggest a potential capital loss of $64B

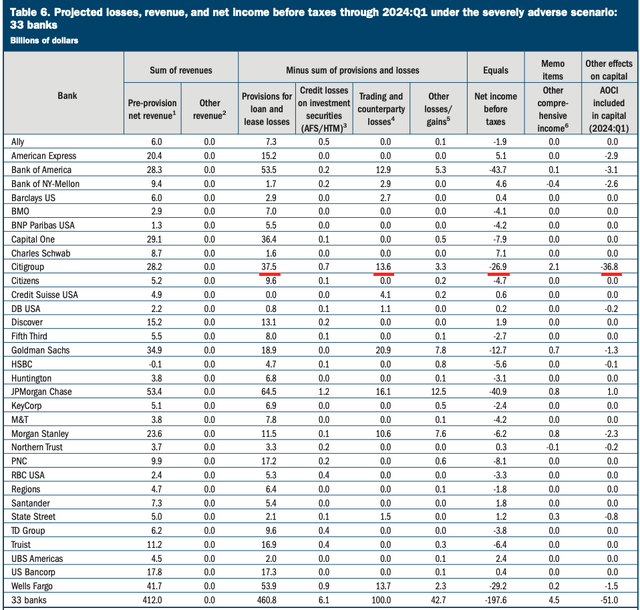

Last month, the Fed published stress-test results for 33 U.S banks. As shown below, under the severely adverse scenario Citi posted a net loss of $26.9B and a negative impact on AOCI, which included in capital, of $36.8B. This suggests a total capital loss of $64B or around 43% of Citi’s CET capital as of the YE2021.

Those losses are due to the reasons we discussed earlier: 1) provisions for loans losses are driven by high exposure to credit cards; 2) trading and counterparty losses are due to Citi’s securities book, including repo transactions; and 3) a large negative impact on AOCI is most likely driven by AFS book revaluations and a high share of revenues from emerging economies.

However, it is important to note that the Fed’s assumptions for its severely adverse scenario are quite mild, in our view. In particular, Fed assumed a relatively short-lived market correction and a V-type recovery of both the markets and the global economy. Should a market correction and a recession be more prolonged (more than 12 months) the negative effects on Citi’s earnings and capital would be much more significant.

The bottom line

In contrast to Citi, the Top U.S. 15-banks we have identified at SaferBankingResearch.com generate 100% of their revenues from the U.S., have a low-risk loan mix with minimal exposure to unsecured lending and have a very conservative securities book, which consist predominantly of U.S Treasuries and U.S municipal bonds. Importantly, as opposed to Citi, our Top-15 banks do not have any derivatives and equities on their balance sheets. Moreover, Citi has more red flags, which we did not discuss in detail due to the limitations of the article. However, all our Top-15 banks have been tested for these red flags to ensure their long-term stability.

********

Avi Gilburt is a widely followed Elliott Wave technical analyst and author of ElliottWaveTrader.net, a live Trading Room featuring his intraday market analysis (including emini S&P500, metals, oil, USD & VXX), interactive member-analyst forum, and detailed library of Elliott Wave education. You can contact Avi at: [email protected].

Avi Gilburt is a widely followed Elliott Wave technical analyst and author of ElliottWaveTrader.net, a live Trading Room featuring his intraday market analysis (including emini S&P500, metals, oil, USD & VXX), interactive member-analyst forum, and detailed library of Elliott Wave education. You can contact Avi at: [email protected].

More from Gold-Eagle