Will Chinese Gold Demand End 2014 With A Boom?

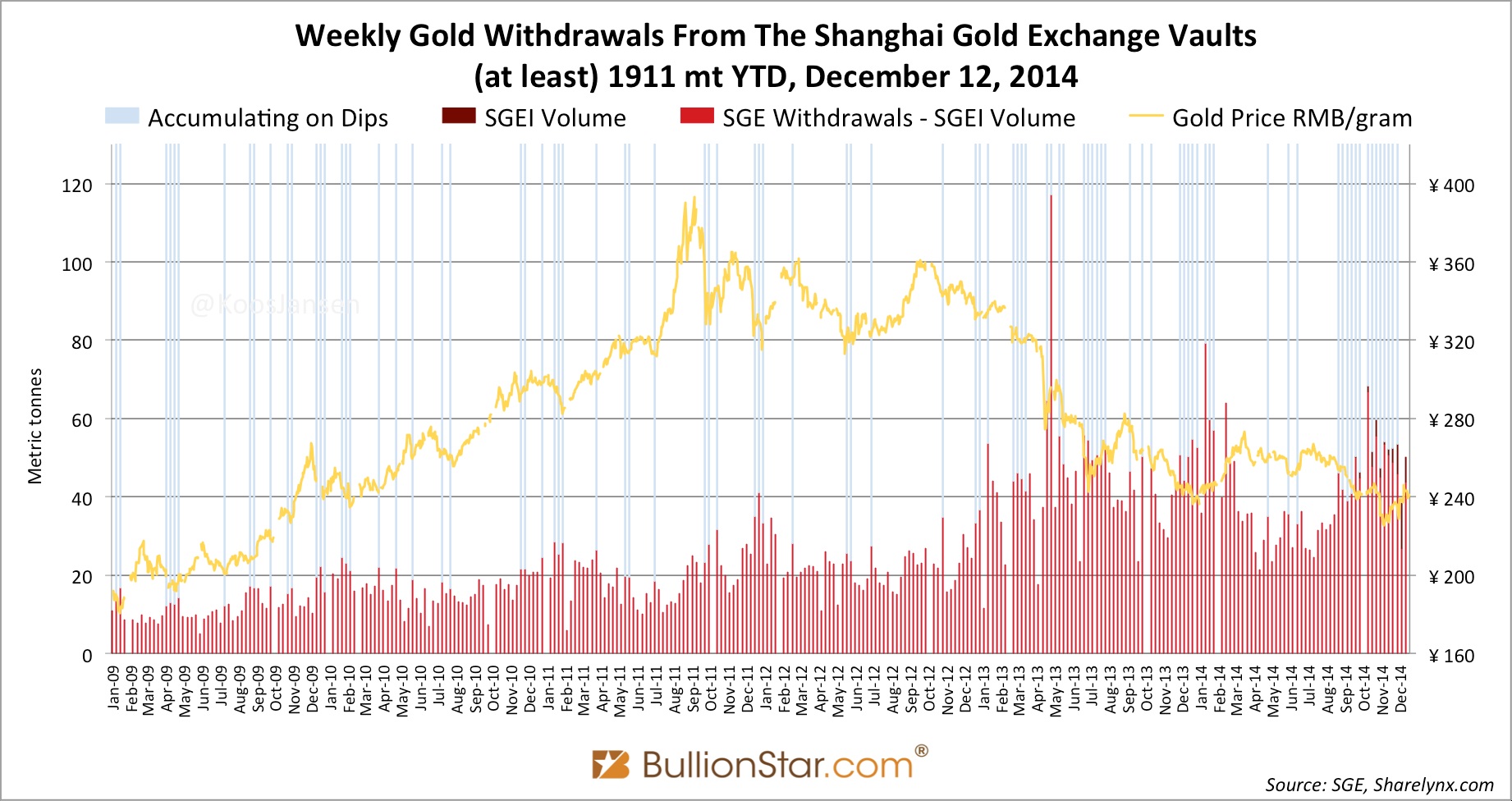

Shanghai Gold Exchange (SGE) withdrawals in week 50 (December 8 – 12) accounted for 50 tonnes, year to date 1,955 tonnes have been withdrawn.

SGE Withdrawals In Perspective

I have written about this before, but I just want to make sure I have clearly shared my view on this subject (if you’ve read all my previous posts regarding withdrawals you can skip this chapter).

Many blogs are tracking SGE withdrawals currently, using it as the yardstick for Chinese wholesale gold demand. While partially true, I would like to emphasize this yardstick has become elastic.

Before the SGE’s subsidiary, the Shanghai International Gold Exchange (SGEI), was launched total SGE withdrawals provided us a clear view on Chinese wholesale gold demand, as the SGE is the exchange where all import and domestically mined gold is required to be sold first (in addition to scrap) before entering the Chinese domestic market. This clear view is now blurred.

The SGEI facilitates gold trading in the Shanghai Free Trade Zone (FTZ). Physical gold trading in the FTZ is completely separated form the Chinese domestic gold market, which is a closed market; bullion exports are prohibited and only 15 banks are licensed to import bullion. The banks that enjoy a PBOC bullion import license are:

- Shenzhen Development Bank / Ping An Bank

- Industrial and Commercial Bank of China

- Shanghai Pudong Development Bank

- Agricultural Bank of China

- Bank of Communications

- China Construction Bank

- China Merchants Bank

- China Minsheng Bank

- Standard Chartered

- Bank of Shanghai

- Industrial Bank

- Bank of China

- Everbright

- HSBC

- ANZ

The gold traded on the SGEI can be withdrawn from the vaults in the FTZ by foreign enterprises and shipped abroad, these SGEI withdrawals are captured in the total SGE withdrawals (only aggregated withdrawals are disclosed) and thus distorting our view on Chinese wholesale demand.

Would we get our clear view back if SGE and SGEI withdrawals would be disclosed separately? No. This is because Chinese domestic banks are also trading on the SGEI, when they withdrawal from the vaults in the FTZ they can import this gold into the mainland without it being required to be sold (again) through the SGE.

The trading volume/purchases on the SGEI (contracts iAu100g, iAu99.99 and iAu99.5) can be:

- Not withdrawn at all and thus not distorting our view on Chinese wholesale demand.

- Withdrawn by foreign traders and thus distorting Chinese wholesale demand. If we knew how much these withdrawals accounted for we could subtract them from total SGE withdrawals to have a clear view on Chinese wholesale demand. Unfortunately we don’t know these numbers.

- Withdrawn by Chinese domestic banks to be imported into the mainland and thus being part of Chinese wholesale demand.

This is what we (I) know at this stage. Concluding weekly Chinese wholesale gold demand is at most total SGE withdrawals, at least total SGE withdrawals minus SGEI trading volume.

For example, in week 50 total SGE withdrawals accounted for 50,027.5 Kg. Total SGEI trading volume accounted for 6,159 Kg. Meaning Chinese wholesale gold demand was somewhere in between 50,027.5 Kg and 43,868.5 Kg (50,027.5 – 6,159). Year to date Chinese wholesale gold demand is somewhere in between 1,911,230 Kg and 1,955,090 Kg (at least 1,911 tonnes).

Needless to say, if more information is disclosed by the SGE I will report about it as soon as possible.

Furthermore; Chinese wholesale gold demand is supplied by import, mine and scrap. The amount of mine supply we know from numbers of the China Gold Association (CGA), in 2014 it will be approximately 451 tonnes. The composition of the other two supply flows is not known, for this we have to make estimates based on numbers from previous years. In 2012 scrap (through the SGE) was 232 tonnes, in 2013 it was 247 tonnes. This year scrap is likely to be substantially higher. How come? By way of measuring Chinese wholesale gold demand as described above, it was at least 1,841 tonnes in the first eleven months of this year. The Chairman of the SGE said on a conference import was (approximately) 1,100 tonnes over this period and mining had to be 416 tonnes, setting scrap at 325 tonnes.

Nevertheless, China will import far more than 1,100 tonnes in 2014, added to 451 tonnes of domestically mined gold, the Chinese people will add about 1,700 tonnes to their reserves. Assuming the PBOC doesn’t buy gold through the SGE.

Will Chinese Gold Demand End 2014 With A Boom?

Seasonally December and January are strong months for Chinese gold demand, but will they be this year? To answer this question let’s have look at the next chart.

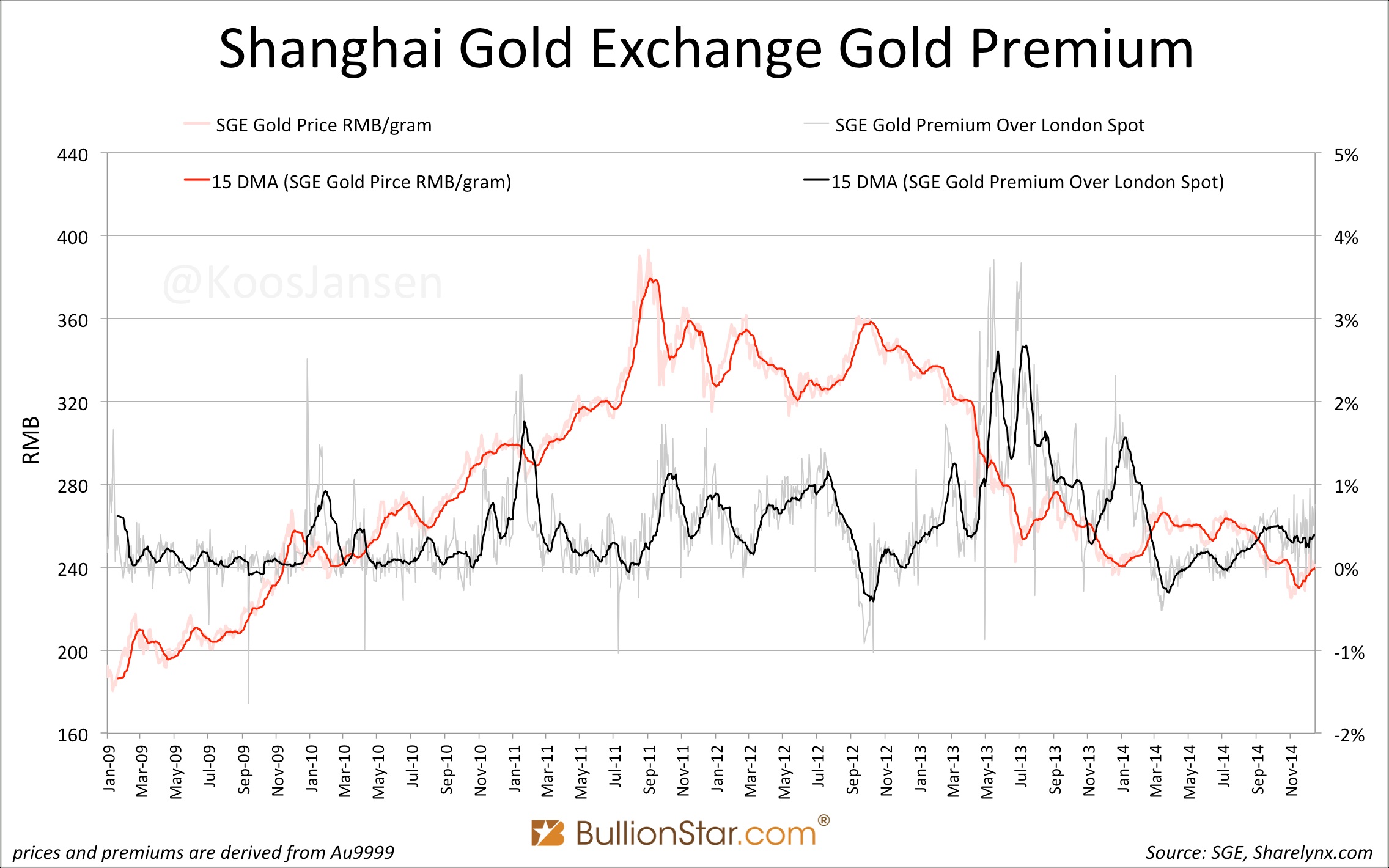

We can see elevated withdrawals every December and January. Additionally, it’s clear the Chinese rather buy gold when the price is declining than when it’s rising, unlike Western gold investors. This thesis is also supported by the fact SGE premiums often move inverted from the price of gold.

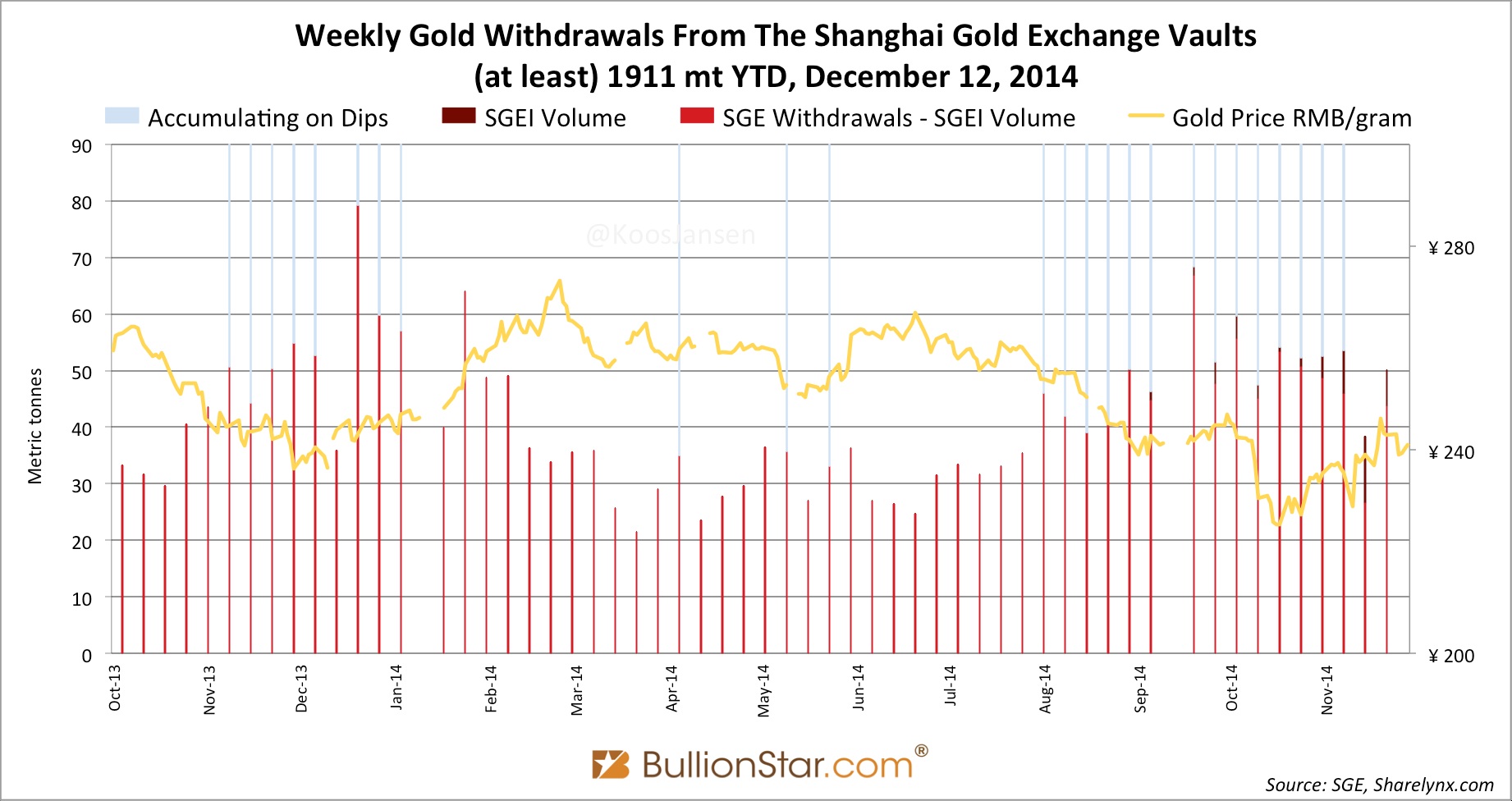

Now let’s zoom in on the former chart.

Though withdrawals are strong, in my opinion demand is somewhat held back by a rising price of gold in the past few weeks. How withdrawals/demand will develop around New Year is (of course) partially determined by the direction of the price of gold. If the price of gold continues to rise in renminbi I expect it will further dampen Chinese demand around New Year and Lunar Year.

Chinese Gold Trading Volumes

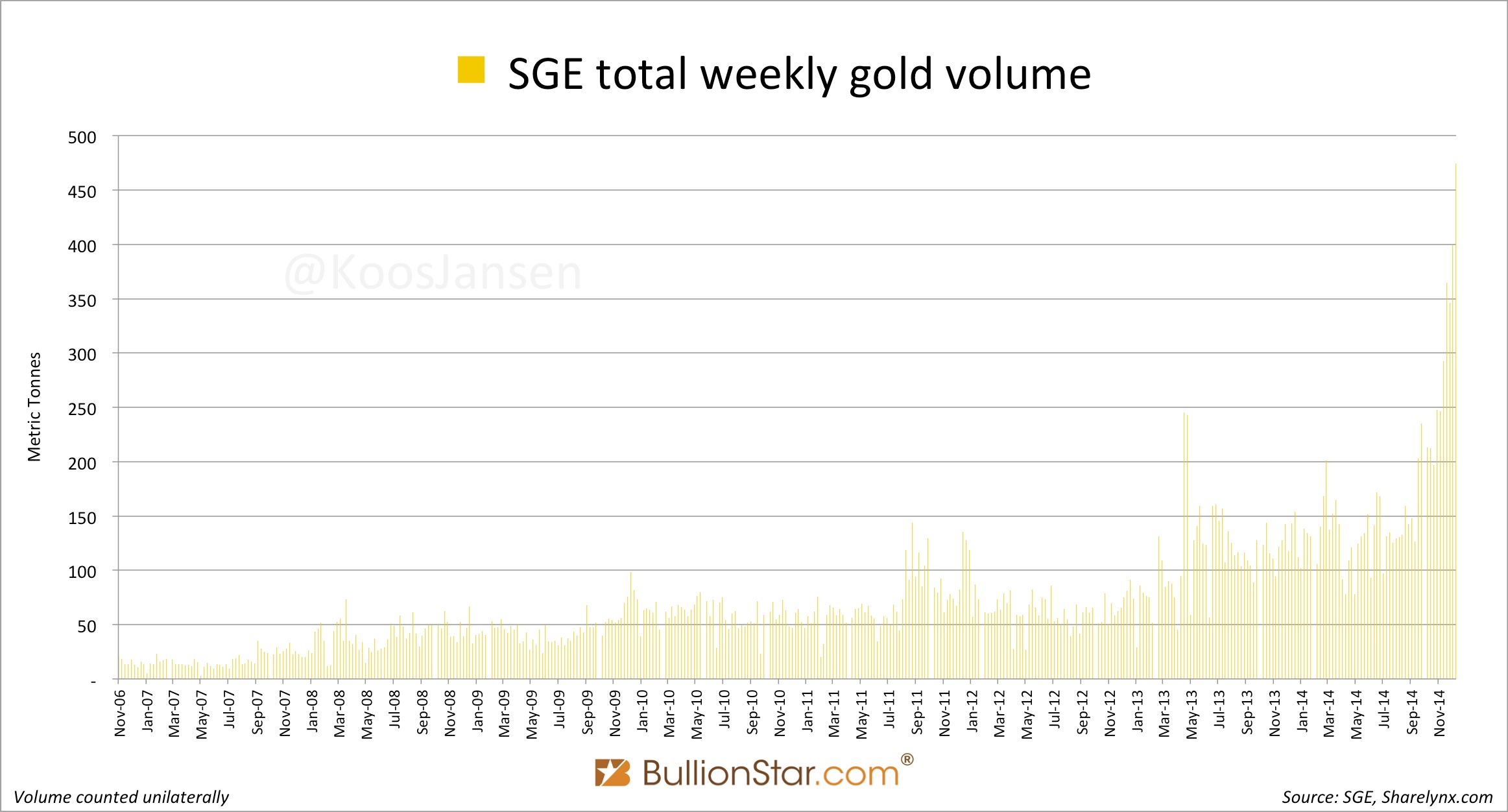

Worth mentioning is that SGE gold trading volume is going up exponentially since a couple of weeks. The biggest drivers are the Au(T+N1) and Au(T+N2) deferred contracts. On November 3, 2014, the SGE adjusted the specifications of these contracts – that hadn’t been traded at all since October 2013, after which volumes skyrocketed. In week 50 the volume of these contracts combined accounted for 95 tonnes, which is 20 % of the total SGE gold volume traded (474 tonnes).

Red: trading volume of Au(T+N1) and Au(T+N2) counted bilaterally. Purple: total SGE gold trading volume in week 50 counted bilaterally.

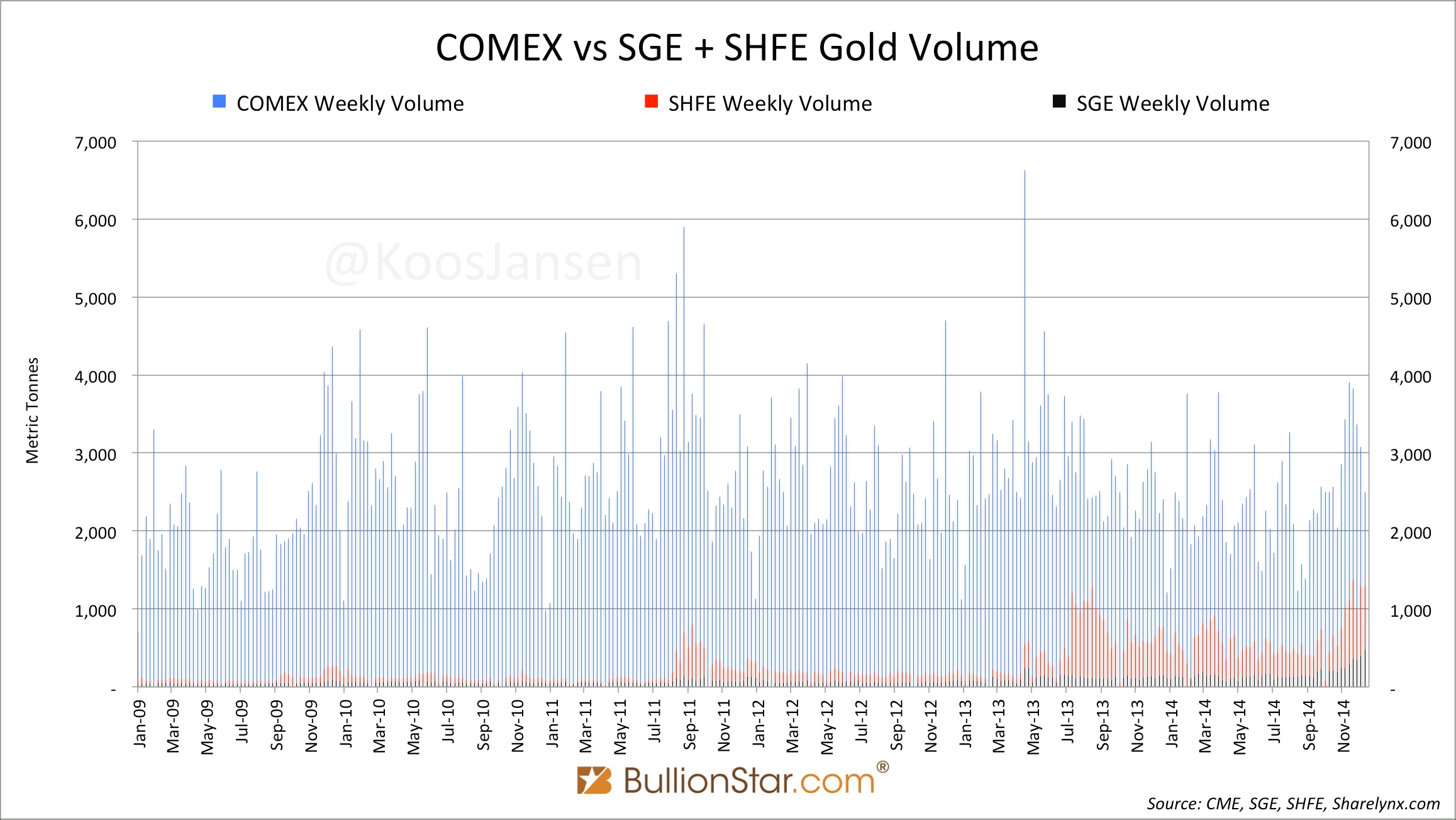

Total gold volume traded on the SGE combined with the total gold volume traded on the Shanghai Futures Exchange (SHFE) accounted for 1,309 tonnes in week 50. This amount was more than half the gold volume traded on the COMEX in the same period (2,507 tonnes). I don’t see a trend of declining volumes on the COMEX, but I do see a trend of surging volumes in China, that are now starting to near COMEX volumes.

Courtesy of https://www.bullionstar.com/

More from Gold-Eagle