What a Long, Strange Trip It’s Been Since Nixon Took USD Off the Gold Standard

The chart of SPX and gold shows that volatility was hard-wired into a macro market situation that had been relatively normal prior to August, 1971.

I love looking at pictures. Pictures are how I form words, thoughts and stories.

This picture is a story of the time since the US removed the last bastion of soundness to its money, it’s funny munny that in its near-infinite ability to be printed at will (due to no hard asset backing) has funded all manner of societal and financial progress, as Keynesian policymakers no doubt hated dragging that heavy rock around, anchoring their lofty aspirations.

Since 1971 the stock market has been set free to create wealth as the economic funding mechanism became pure finance as opposed to sweat equity and productivity. Take a loan, build it… and they will come. Boy will they ever. Take another loan, and another, and another.

When a pesky natural deflationary economic cycle tries to bring on a bust, simply call on the Hero of the moment and this natural economic cycle will be battled tooth and nail, and ultimately defeated in service to continued volatile upside to the chart above.

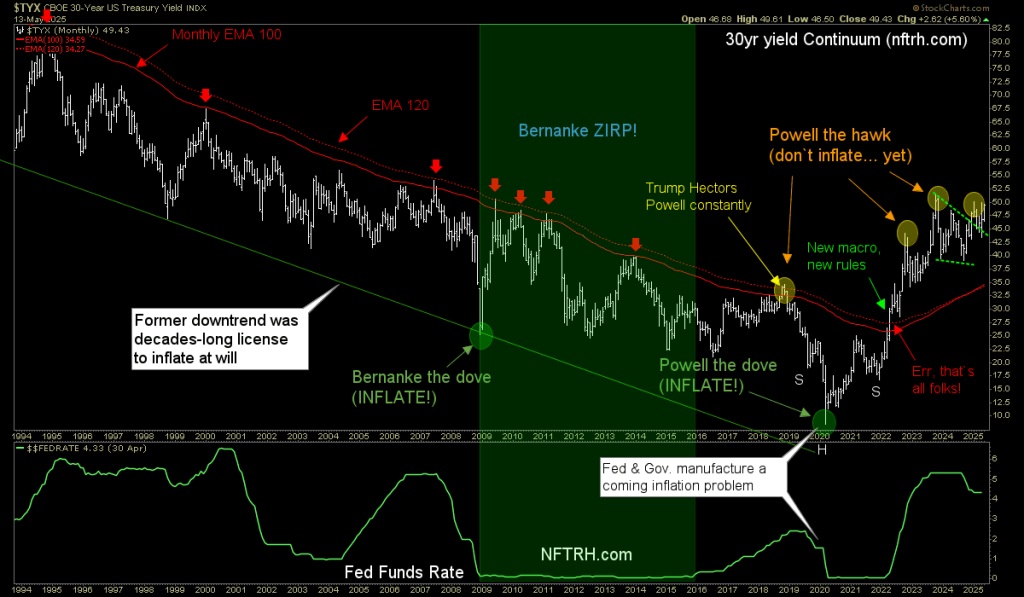

However, currently I view the rupture of the decades-long easing trend in long-term Treasury yields as a loss of license for future Heroes to spring into action. The last heroic (and massively inflationary) act was the balls out Powell bailout in Q1, 2020. The reaction to that busted the macro into a new inflationary, likely stagflationary phase.

This could work to limit policy responses to deflationary episodes or force policymakers to fight inflationary phases longer and harder than during the pleasant and bubbly era that ended harshly in 2022 with the Continuum’s unceremonious break of its previous trend in disinflationary market signaling.

When you look at pictures like these, with their implications of intense volatility and macro whipsaws, stagflationary economic limp-along with deflationary interruptions (busts) could be a good interpretation.

Speaking of busts, steepening yield curves remain on that message. Right now, with nominal yields rising the curve steepeners have an inflationary bias to them. Inflationary steepening + bust = stagflation.

It’s an entirely new era with new rules by definition of the new macro indications. It is advisable to determine those rules and adapt to them as best as possible. It’s what I (and NFTRH) have been doing since the Continuum was busted in 2022, and mainly this year as market projections are kicking in as no longer theoretical.

For “best of breed” top-down macro analysis and market strategy covering Precious Metals, Commodities, Stocks and much more, subscribe to NFTRH Premium, which includes a comprehensive weekly market report, detailed NFTRH+ updates and chart/trade setup ideas, and Daily Market Notes. Receive actionable (free) public content at NFTRH.com and subscribe to our free Substack. Follow via X @NFTRHgt and BlueSky @nftrh.bsky.social, and subscribe to our YouTube Video Channel.

********