The Numbers Are Breaking down, but What they Mean and Where They Are Heading Looks Worse

Belaboring the Job Market

After writing about the faulty economic numbers put out by the federal government (or not put out on time as if they were hiding them or are figuring out how to continue forward while downsizing), we have another report that came out on Friday that shows the job numbers are less positive than they initially sounded, as I suggested earlier. On Thursday, I quoted Gregory Mannarino who said the job numbers could be seen as a “eulogy” for the still-born Trump economy or as “economic hospice,” so I promised to dig into the misfiring numbers in this Deeper Dive.

In the first reports, the numbers were not strong but not terribly weak either, and that was all it took to stimulate the stock market higher. The next report, which I thought was likely closer to reality, took stocks back down. The labor report that came out on Friday may help settle the dispute because it says that “over 7-million Americans are unemployed, the most since 2017,” and it tells why it won’t get better anytime soon. So, the overall picture, at least, is one of continued slow decline.

The number of people who said they were unemployed in May jumped to an eight-year high if the pandemic era is excluded, offering clear evidence that jobs have become harder to find during a chaotic period for the U.S. economy.

There is that word again, arriving only a couple of months after the year that I said would be the Year of Chaos. We hear it all the time now.

The number of unemployed is now at the highest level since 2021, when the U.S. was still recovering millions of jobs lost at the outset of the coronavirus pandemic. It’s the highest tally going back to February 2017 if the pandemic period is omitted.

The pandemic unemployment, of course, was caused by the outrageous national layoffs mandated by Trump during 1.0, then mandated again under Biden by his Trump vaccine firing mandates. That one-two blow created single worst crash into unemployment (because it was government-forced) the world has likely ever seen. Talk about overreaching government!

“Cracks in the façade of labor market resilience are now starting to show,” said Scott Anderson, chief U.S. economist at BMO Capital Markets.

The unemployment rate is still quite low, at 4.2%. But it’s almost a full percentage point higher than it was a few years ago, when it matched a half-century low of 3.4%.

While the unemployment numbers are still barely creeping upward, we have to bear in mind that many of the DOGE cuts were delayed by courts that questioned their legal legitimacy. Though unemployment is not rising much yet, a slowdown in hiring (new jobs) has become quite evident with one bad report followed by another abysmal report, and the reasons given by business managers, CEOs an owners is clear:

Businesses say they are reluctant to hire more workers because of the trade wars launched by President Donald Trump that have threatened sales and raised doubts about the strength of the economy.

The number of new jobs created in the three months from March to May, for instance, slowed to 135,000, compared with 232,000 as recently as January.

For now, companies are waiting to see if there is a resolution to the trade conflicts before taking on the added cost of hiring more workers.

The Trump White House has dialed back most of the newly announced tariffs to allow for negotiations, but so far there hasn’t been much progress in striking deals.

The Bureau of Lying Statistics reported on Friday more figures that show unemployment overall is not rising much, though hiring is stalling (which means people are clinging to their jobs):

The number of people jobless less than 5 weeks increased by 264,000 to 2.5 million in May. The number of long-term unemployed (those jobless for 27 weeks or more) decreased over the month by 218,000 to 1.5 million. Both measures were little changed over the year. The long-term unemployed accounted for 20.4 percent of all unemployed people in May.

From payroll processor ADP, on the other hand, we saw on Thursday that new hires fell considerably. So, while not a lot more people lost their jobs, a lot fewer gained jobs; and I trust the ADP report far more because 1) it’s not government, 2) it is raw payroll data—how many people were added to the payrolls they process and how many subtracted, and 3) they don’t have any incentive for controlling or massaging the numbers.

They do not, however, look at the entire economy. One can only extrapolate what their very large customer base for processing payrolls means for the overall nation. Of course, neither does the BLS look at the entire economy. There data is also filled with extrapolations and guesstimates before it gets reported. At least, one organization reports only the facts about the data they processed.

On Tuesday, stocks got a big boost when the BLS told us all that the labor market was performing almost as smoothly as a Jaguar luxury automobile:

Employers increased job openings more than expected in April while hiring and layoffs also both rose, according to a report Tuesday that showed a relatively steady labor market.

The Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey showed available jobs totaled nearly 7.4 million, an increase of 191,000 from March and higher than the 7.1 million consensus forecast by economists surveyed by FactSet.

Of course, job openings are not the same as hires. However, if openings are going back up, then presumably hires are likely to rise in the next month as those positions are filled. However, the BLS is clearly struggling from its downsizing, so even less accurate than its former poor performance. Its reports are often stuffed with massive seasonal adjustments that are larger than all the raw data in its reports, and it has for years now seen a sharply falling number of participants in its surveys. So, I have less confidence in it than ever. It has also always seemed to me to be biased toward making the numbers look as good as it can justify for the administration it serves.

Some economists continue to put their faith in the BLS:

“The labor market is returning to more normal levels despite the uncertainty within the macro outlook,” wrote Jeffrey Roach, chief economist at LPL Research. “Underlying patterns in hirings and firings suggest the labor market is holding steady.”

But economists are nearly always the last to see a recession coming. You can be standing in the middle of a recession that eventually becomes officially declared to have begun months before the time where you are standing, yet during that time, you’ll be hard pressed to find more than one or two economists who will say anything stronger than “We would give a 35% chance [or maybe, at most, they’ll say 50%] of a recession starting in the next six months.” They are a timid lot. There are few mainstream economists who have the guts to stand nearly alone against their colleagues.

Jeff Cox at NBC chooses, rather than denying the data’s validity, to simply put it in perspective:

I’ve been reporting from time to time how the quality of jobs has been significantly deteriorating, going all the way back through the Biden administration. So, I don’t think we can blame what little decline we’ve seen so far on the DOGE firings, but it does reveal there is more weakness in the labor market than shows on face value.

I don’t think we’re going to be able to get a clear picture of the truth right now while we’re in such a state of turmoil and flux; but I do think, if all of the DOGE cuts (or even a good number of them) make it through, we’ll see more than just a decline in government jobs (already down by 20,000 in the latest BLS report) because there will be knock-on effects from the businesses that largely served those workers who also layoff staff. Then as tariffs cripple some businesses, they will go from the present hiring freeze talked about in some of these articles to laying off staff.

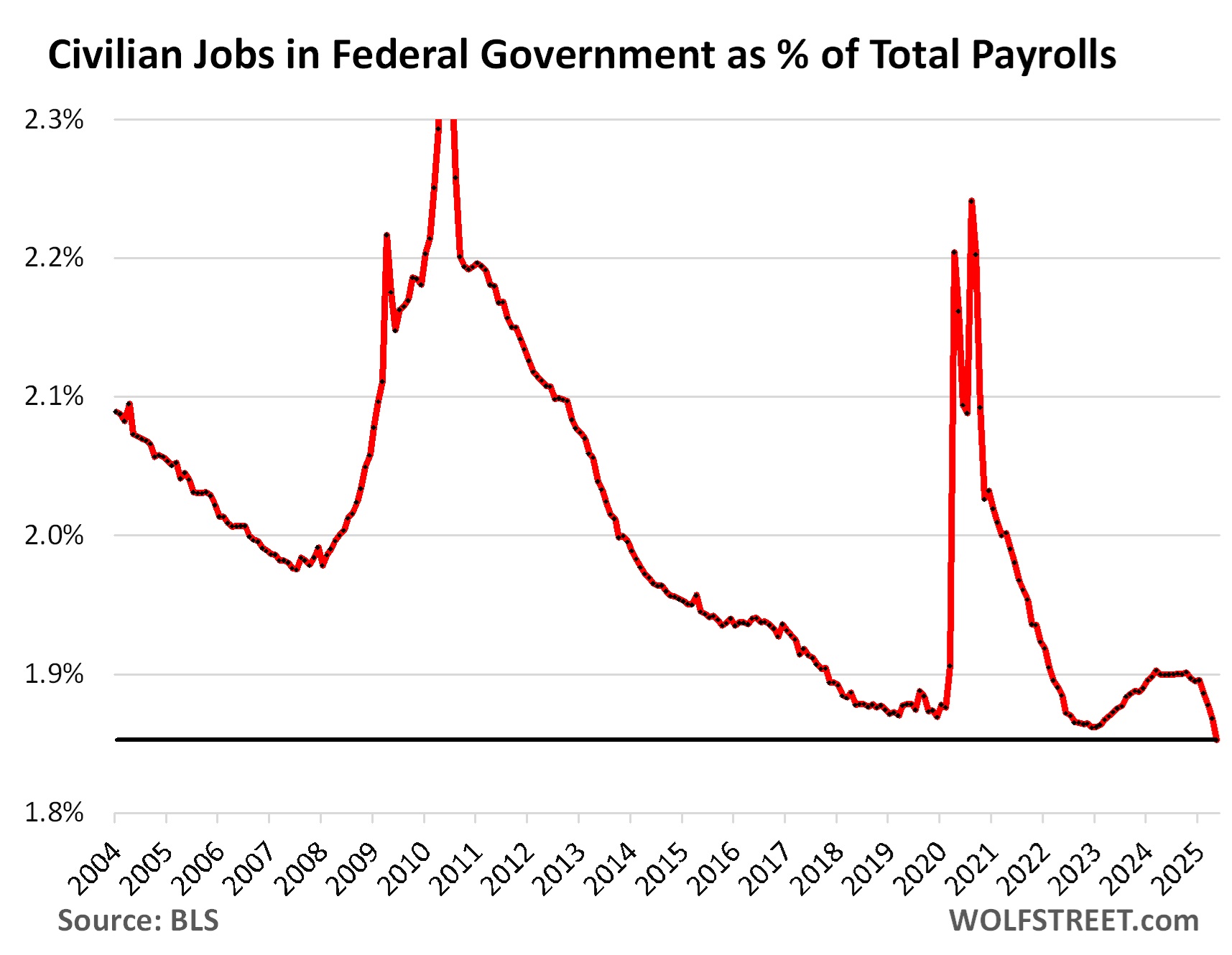

You can see here where the government jobs have already gone:

The dominoes will start to fall, and DOGE continues to seek and recommend cuts, even though Elon is gone. Plus there is this, which is how most of the layoffs have happened:

But the payrolls data still doesn’t show the full effects of the federal government job cuts so far: Workers on paid leave or receiving severance pay are counted as employed until they stop being paid.

And government payrolls don’t include employees working for companies that have contracts with the government and that are now getting laid off. These workers are counted in the various nongovernment categories, such as in the huge category of “Professional and business services,” where employment has been stagnating in recent months. (Wolf Street)

Also, as Trump is given latitude by courts to fire cheap immigrant labor, it is likely that not all of those low-paying jobs will find Americans willing to fill those jobs at that price. (And why should they? Immigrants suppressed those wages for decades, so those jobs have a lot of catching up to do to become desirable to Americans.) That means companies will have to seriously inflate their wages and/or benefits for those jobs or mechanize the jobs or decide not to produce whatever those workers produced, causing shortages. Hence, more inflation pressure.

The need to trim and even perhaps slash government workers in many places is real, but we have to also be real about the pain of the amputations as well as the extent to which those job losses will be disabling. Trump is, of course, counting on his tax cuts and his tariffs to stimulate the economy and to move jobs state-side. It could be that they will do that enough to offset the stalling or, at least, lack-luster labor market. (I’ve included a video at the end here by Adam Taggart, interviewing Lacy Hunt, where Hunt explains why Big Beautiful Bill will provide very little stimulus, except from military spending.)

********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.