10 Big Steps Down The Road To Recession

First, a decline in manufacturing, and then a slump in service industries, now a broad-spectrum inversion of the yield curve hitting its most critical metric this week, unemployment finally starting to rise again, a one-year relentless housing decline across most of the nation and the world, carmageddon pressing car dealers to offer big incentives once again just to hold sales flat, shipping everywhere sinking rapidly, broadly deteriorating general business conditions, plus tariff troubles for the US throughout the world — all of these economic stresses have gotten remarkably worst in just the past month.

At the same time, the stock market has soared back up to its three-time ceiling (now four-time) and managed to clear microscopically above that level. Apparently, the last recession was such a great recession, the stock market believes more of the same would be the best thing that could happen. And why not, the last recession made 10% of the US richer and 1% fabulously richer. Investors, it would appear, couldn’t be more delighted to see so many forces pushing the entire global economy — US now fully included — back into recession for another go at the best of times for the one-percent crowd.

With their best interests in mind, let’s take a closer look at all that is happening on that downhill run to recession — all the things that give investors sugar-plum dreams at night about the Fed being forced to inject more monetary narcotics into the market. Let me lay out all the recent hopeful signs that the economy is crashing just in time to force the Fed’s first interest-rate cut after a couple of years of rising rates — that cut of coke that the market is now demanding.

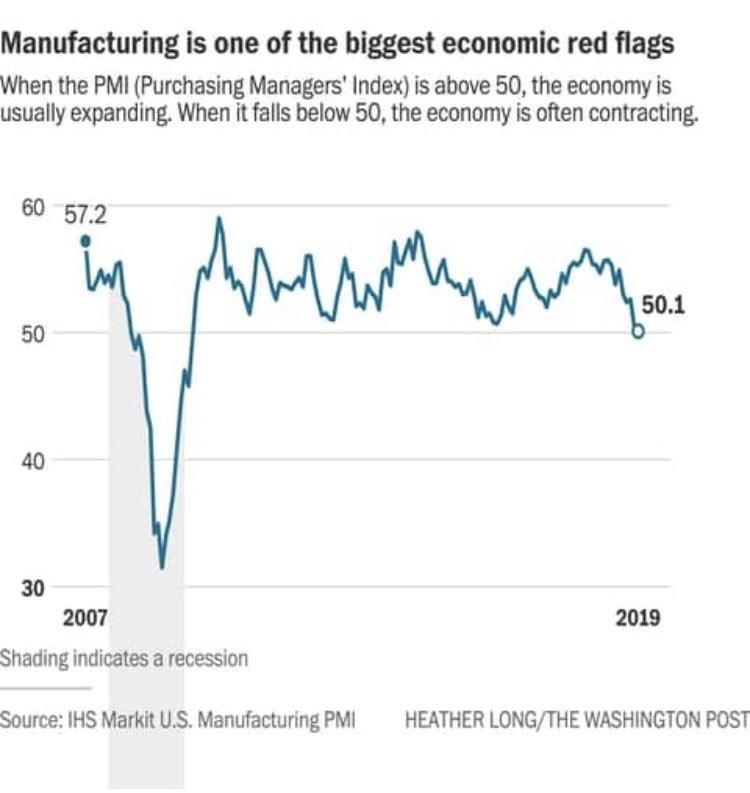

1. Factory orders/manufacturing are in repetitious months of decline

In May, factory orders fell 0.7%, month on month, which is the third decline in four months. April’s decline was revised lower to -1.2%. Within those figures, sales of transportation equipment plunged 4.6%, transportation being particularly indicative of where the overall economy is going. A look at the actual trend line makes the meaning of these drops much more apparent:

After months of decline, the ISM shows no signs of a bottom forming.

Here’s another view:

We are now the closest we’ve been to actual economic contraction since the Great Recession. Up to now, all talk has been about slowing growth. Now we are on the cusp of actual contraction (which means the same thing as recession if it lasts six months or more).

What is seen for manufacturing in the reports above is consistent with recent results from the Dallas Fed Manufacturing Survey, which crashed below the worst analysts’ estimates in June:

Things don’t look any better in the Empire State Manufacturing Survey:

Both are back in their contraction zones.

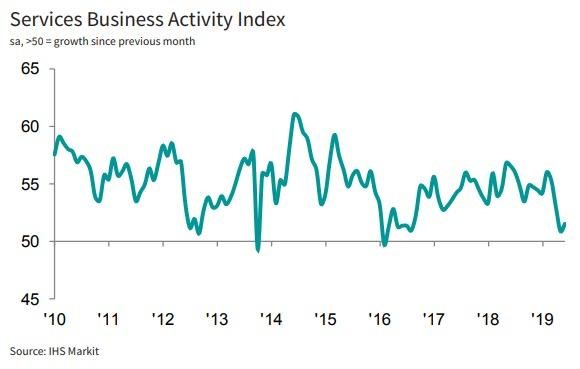

2. Services sector finally joins the fall

Many who have been seeing this decline play out over months in the manufacturing sector have been hoping that the services sector will save the day. Services have been holding up much better than manufacturing, so perhaps that sector of industry would carry the economy over this slump. However, as you can see in the graph below services are no long doing much better: (Anything below the 50 line represents economic contraction.)

Though serviced did see a minor uptick in June, it was barely visible and still leaves the service sector very near the “50” line. This keeps them just about at a three-year low, hardly encouraging given the massive business tax cuts in the US over the last year and a half that were accompanied with massively increased government spending. At the same time employment in the services industry dropped by its most in sixteen months. So, all that boost is creating now apparent lift at all.

An improvement in service sector growth provides little cause for cheer, as the survey data still indicate a sharp slowing in the pace of economic growth in the second quarter….. A major change since the first quarter has been a broadening-out of the slowdown beyond manufacturing, with the service sector growth now also reporting much weaker business activity and orders trends than earlier in the year. “Hiring was hit as firms scaled back their expansion plans in the face of weaker than expected order inflows and gloomier prospects for the year ahead. Jobs growth was the weakest for over two years and future expectations across both services and manufacturing has slipped to the lowest seen since comparable data were first available in 2012….

The services sector employs more than 80% of all American workers. But, hey, that’s good for Fed addicts, right?

“With momentum clearly fading, it won’t be long before the Fed begins cutting interest rates,” said senior U.S. economist Michael Pearce of Capital Economics.

Yay. Let’s all join in hoping the economy crashes spectacularly so stocks can benefit all over again from years of more free Fed funds than they’ve ever seen before! The One-Percenters are already stocking champagne for that day when Great Recession 2.0 is finally announced.

3. The yield curve just inverted at its most critical level:

The bond market flashed yet another warning signal for investors on Wednesday that a downturn for the economy may be coming. Despite the S&P 500 hitting new all-time highs, the yield on 30-year U.S. Treasury bonds briefly dipped below the overnight fed funds rate, a signal that has preceded the past five U.S. recessions.

Economists have known for quite some time that yield curve inversions tend to be reliable predictors of business contractions (recessions).

4. Unemployment has begun to rise at last

The first upticks in unemployment typically are one of the last events to happen before a recession begins. So, renewed hope for the one percent is not far off. While the number of job layoffs remains near a half-century low, initial jobless claims have started to rise:

The four-week monthly average of claims, considered the more stable report, has also begun to rise, albeit incrementally. The pace of hiring has dropped, but the pace of firing has not yet risen.

With the unemployment rate at a nearly 50-year low of 3.6%, good help is hard to find and companies are reluctant to let go of workers. The economy would have to stumble badly to get firms to start handing out pink slips en masse.

Whenever unemployment has settled this low, an uptick in joblessness soon begins, and recession always begins shortly thereafter:

Historically, a trough in the unemployment rate also tends to be a reliable predictor of a business recession.

Well, good, then; the trough is already forming, and it doesn’t have to form for more than 2-3 months before recession is here. That uptick in job losses is particularly notable now in the bellwether small-business sector, where falling jobs haven’t looked this bad since the Great Recession (ADP’s worst plunge in jobs in this sector since 2010):

*********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.