America’s Metals, Minerals And Materials Misery

Today I revisit a subject that was prominent in the American conscious post-global economic crisis and brought to the forefront by the rare earth element and lithium bubbles from 2009 to 2011:

The United States of America depends on imported supplies for most of its industrial metals, minerals, and materials demand.

I spoke and wrote extensively about the US of A’s dearth of domestic production and dependence on risky, corrupt, unstable, and/or unfriendly sources in 2011 and 2012. Here are selected examples: (Mercenary Interview March 4, 2011; Mercenary Musing, August 6, 2012; Mercenary Video, June 9, 2012).

Over the past 14 months, the Trump administration has rolled back government regulations, streamlined bureaucracies, cut taxes, and proposed major infrastructure buildouts and tariffs on imports of aluminum, steel, and Chinese goods. Combined with a stronger economy, booming stock markets, and higher commodity prices, it seems likely that mineral demand will increase in the short to midterm. So this is an opportune time to provide an update on our overwhelming reliance on foreign sources to meet domestic mineral demand.

The United States Geological Survey publishes an annual compendium of mineral and material commodities and documents domestic production, imports, exports, apparent consumption, and official government stockpiles among other data (USGS Mineral Commodities Summaries).

Let’s start with a chart from the 2017 publication that shows US net import reliance for the 64 industrial metals, minerals, and materials with >25% dependence:

From the chart and footnote listings in the USGS document:

-

The US imports 100% of 21 mineral commodities, 50% or more of 29, and more than 25% of another 14.

-

The country imports less than 25% of apparent consumption for the following 17 materials: beryllium, cadmium, cement, industrial diamonds, gypsum, iron and steel, iron and steel slag, lime, magnesium metal, fixed nitrogen-ammonium, perlite, phosphate rock, construction sand and gravel, salt, crushed stone, sulfur, and talc.

-

The US of A is a net exporter of 16 commodities: metallic abrasives, boron, clays, diatomite, gold, helium, iron and steel scrap, iron ore, kyanite, molybdenum, industrial sand and gravel, selenium, soda ash, titanium dioxide pigment, wollastonite, and zeolites.

The 2017 United States net import reliance data for 97 minerals is summarized in the following table:

Americans should be concerned not only because of our dependence on other countries for the majority of essential industrial commodities but also because of some of the countries that we are most dependent on.

Let’s look at countries that are unfriendly, unstable, and/or corrupt and the number of materials for which we import a quarter or more (25%) of annual demand:

-

China is our primary, secondary or tertiary source for 31 commodities, mainly specialty metals and industrial minerals with small markets.

-

Russia is an important source for 12 commodities, including five major metals and one major agricultural mineral.

-

South Africa is the largest supplier of six major metals and a significant supplier of two industrial minerals.

-

Other countries with high geopolitical risk that supply one or more minerals include Bolivia, Gabon, Georgia, Guinea, Kazakhstan, Mozambique, Philippines, Rwanda, Senegal, and Ukraine.

The United States, despite being >25% dependent on foreign sources for 64 materials, holds strategic stockpiles of only 14.

The National Defense Stockpile (NDS) is the government program designed to be America’s insurance policy for commodities in times of national emergency. Its primary mandate is to eliminate or reduce dangerous and costly dependence on foreign nations for strategic and critical mineral resources during disruption of supplies. Stockpiled materials must meet three distinct criteria:

-

They must be essential for the common defense, whether for the military or industry.

-

Materials must be insufficiently available in the United States.

-

All materials must have the distinct capability of actually being stockpiled.

Let’s review the 100-year history of United States mineral stockpile policy to facilitate understanding of the present supply situation:

During and after our entry into World War I, it became apparent that the United States was deficient in many strategic minerals. In 1917, the War Industries Board recommended that future materials problems should be anticipated and ameliorated in advance.

In 1922, the Army and Navy Munitions Board was established by the War Department to plan for industrial mobilization and procurement of munitions and supplies. It established a list of 14 strategic minerals where supply was wholly or substantially dependent on foreign sources and an additional 15 critical minerals that were available to some degree from domestic sources. But there was no procurement of these 29 strategic minerals.

In 1938-1939, two Congressional acts resulted in an authorization of $100 million for a stockpile of 42 strategic and critical raw materials. However at the beginning of World War II, only $54 million had been purchased.

America’s strong industrial and manufacturing base was fully mobilized to support the war effort in 1942. Massive quantities of ferroalloys, manganese, tin, natural rubber, and other materials were imported and stockpiled. Of 15 materials in the stockpile, only three were produced domestically. The USGS and Bureau of Mines were tasked with exploring, developing, and producing domestic sources of and substitutes for critical minerals. These evaluations resulted in many new mineral discoveries and mines.

Immediately after the war, Congress passed the Strategic and Critical Minerals Stockpiling Act of 1946. The act was designed to “prevent a dangerous and costly dependence of the United States on foreign nations for supplies of these materials in times of national emergency”.

The Act funded a program to procure five years of supply based on estimated wartime consumption. It also encouraged development of domestic sources with government buying programs, credits, grants, and subsidies. By the beginning of the Korean War in 1952, stockpile objectives consisted of 75 commodities with a value of $8.9 billion. It grew to $10.4 billion in1956.

Based on assumptions by military war planners of short nuclear wars versus longer-lived conventional wars, the program was reduced to three years supply in 1958, and 63 of 75 stockpiled materials were declared in excess. In 1962, the value of these materials was $7.7 billion with only $3.4 billion required under then current war scenarios.

Due to worldwide base metal shortages, the government reduced the inventory by $1.6 billion by the end of 1965 via sales of antimony, cadmium, copper, lead, and zinc to support domestic industries. Meanwhile, the strategic and critical list had grown to 89 materials.

The stockpiling requirement was reduced to one year supply in 1970 to pay off federal budget deficits and then was changed back to a three-year goal by an Act of Congress in 1979. That act specifically prohibited using stockpile sales to reduce budget deficits.

In the early 1980s, the world was in recession, the US metals mining industry was in decline, and the stockpile was maintained. Between 1984 and 1994, it was upgraded by replacing chromite and manganese ores with ferrochrome and ferromanganese alloys and paid for by disposal of excess materials.

In 1988, management of the stockpile was transferred from the Federal Emergency Management Agency (FEMA) to the Department of Defense (DOD). Concurrent with the collapse of communism in 1989 that culminated in dissolution of the Soviet Union in late 1991, the DOD reevaluated its war scenarios and decided “to modernize the stockpile”.

This decision led to a paradigm shift in the National Defense Stockpile.

By 1992, the DOD was viewing foreign suppliers as more reliable, downsizing the military, requesting less budget money to maintain the stockpile, and lobbying to sell many stockpiled minerals to offset post-Cold War defense budget reductions. Congress approved sales of 26 minerals including cobalt, chromium, manganese, and platinum; i.e., four commodities where we were almost wholly dependent on imports from notoriously unstable countries in southern Africa and post-Soviet, crime-ridden Russia.

During the Clinton and Bush Jr administrations from 1993 to 2005, most of the remaining stockpiles were sold off to fund military benefits, health care, and retirement, war monument programs, minting of commemorative silver coins, and the general treasury to the tune of $5.9 billion.

In 1994, the National Defense Stockpile of 91 strategic minerals and materials contained only 55% of the three-year supply required by the 1979 act, with a total value of $8.9 billion versus the $16.1 billion earmarked.

In 1997, the Defense Department once again planned for one-year wars thus enabling stockpile sales to continue unabated:

-

In 1999, the earliest year for which annual reports are easily obtainable, the stockpile consisted of 40 minerals and materials with a market value of $3.5 billion.

-

In 2001, the stockpile consisted of 33 minerals and materials with a market value of $2.5 billion.

-

In 2006, the stockpile consisted of 22 minerals with a market value of $1.6 billion.

-

In 2011, the stockpile consisted of 14 minerals with a market value of $1.4 billion.

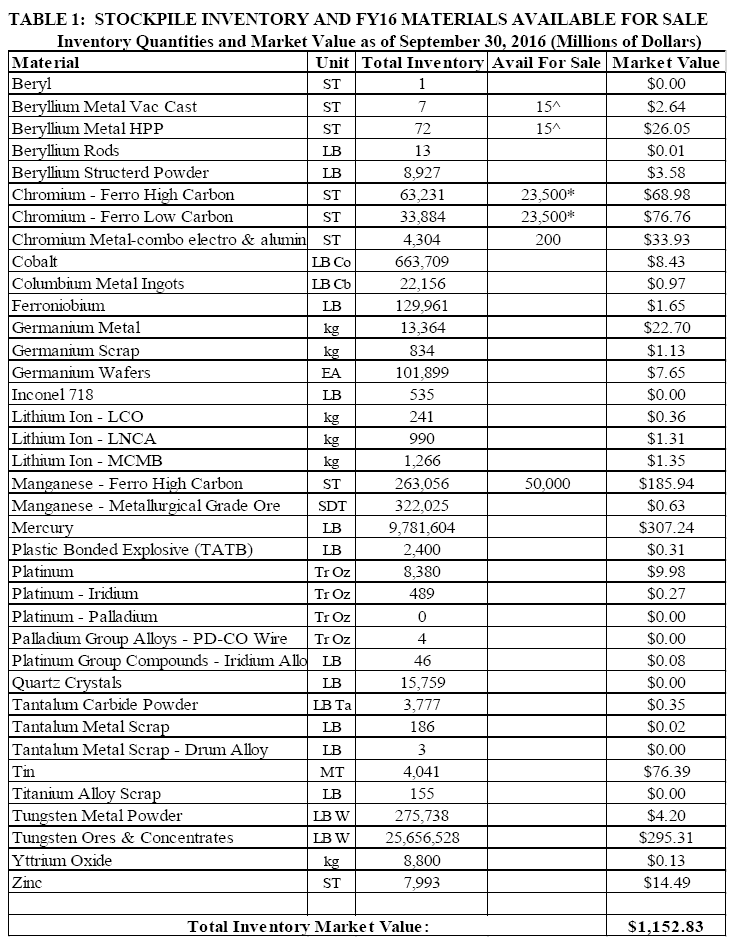

The end of fiscal year 2016 (September 30) is the latest posted annual report from the National Defense Stockpile Center documenting individual commodities and overall value of the stockpile. At that time, the strategic and critical stockpile contained 18 minerals and materials with a market value of less than $1.2 billion.

Note that for my count of 18, I grouped various stockpiled materials for specific elements (e.g., three chromium products), “columbium” (Nb) metal and ferroniobium alloy, and the platinum group metals (Pt and various alloys).

The 2016 stockpile list also shows surplus materials offered for sale:

In fiscal year 2014, the National Defense Stockpile Center had outstanding orders to purchase Cd-Zn-Te substrate materials, ferroniobium alloy, Li-ion precursors, plastic explosives, and yttrium oxide. Those orders have now been filled except for Cd-Zn-Te substrate.

In fiscal year 2018, the NDSC has orders to accumulate boron carbide, carbon fiber, europium, germanium, tantalum, tungsten-rhenium metal, and silicon carbide fiber.

Now let’s do a comparative analysis of the USGS chart and the 2016 NDSC table:

The 2016 National Defense Stockpile holds 14 of the 64 mineral commodities that are on the USGS’ chart with >25% net import reliance; it holds one with <25% import dependence (Be); and one that was declared toxic by the EPA in 2001 (Hg), and discontinued as part of the USGS import reliance compilation.

Note that I have eliminated Inconel (Ni-Cr-Nb-Mo superalloy) and plastic explosives in this discussion.

-

The US government is selling two stockpiled metals for which we are significantly reliant on imports from unstable or unfriendly sources: chromium at 69%, sourced from South Africa, Russia, and Kazakhstan; and manganese at 100%, sourced from South Africa, Gabon, and Georgia, plus Australia.

-

Of the 21 minerals for which we are 100% import dependent, five are held in the stockpile: niobium, manganese (selling), quartz crystals, tantalum, and yttrium.

-

Of the 31 for which we are dependent on China as the first, second, or third largest supplier, seven are stockpiled: cobalt, germanium, lithium, quartz crystals, titanium, tungsten, and yttrium.

-

Of the nine for which we are dependent on Russia as the first, second, or third largest source, three are stockpiled: chromium (selling), germanium, and niobium.

-

Of the 10 for which we are strongly dependent on South Africa as a major source, there are stockpiles of four: chromium (selling), manganese (selling), platinum, and titanium.

The import dependence of the United States of American for major and minor industrial mineral resources is alarming. Moreover, many essential minerals are sourced from countries with geopolitically risky, unfriendly, unreliable, unstable, and/or corrupt, fascist governments. These countries include China, Russia and its former Soviet satellites, those in southern Africa, and select countries in other parts of the Third World.

The National Defense Stockpile is designed to ameliorate US vulnerability on foreign sources if geopolitical events disrupt or cut off access to strategic and critical minerals. That said, the stockpile is now geared for short duration wars imagined by Department of Defense gamers.

It is apparent the DOD has little to no concern for industries that would not be involved directly or peripherally in an armed conflict.

To illustrate these myopic military views, the NDS is currently selling two major steel-making alloys of which we are 100% import reliant on South Africa, Kazakhstan, and Russia in one instance (ferrochromium) and South Africa, Gabon, Georgia, plus Australia in the other (ferromanganese).

That seems a recipe for disaster and in my opinion, our current situation is untenable.

That said, I am hopeful that President Trump’s rollback of onerous regulations, reduction of bloated bureaucracies, reinstatement of lands in the Western US to mineral entry, and streamlining of permitting and development processes will continue to lead to a stronger market economy and help revive domestic extractive mineral and energy industries as the coming bull market for commodities develops.

Ciao for now,

Mickey Fulp

Mercenary Geologist

*********

Acknowledgment: Troy McIntyre is the research assistant for MercenaryGeologist.com. I thank Jim Kennedy, Three Consulting. St. Louis, Missouri, for suggesting I revisit this important issue.

The Mercenary Geologist Michael S. “Mickey” Fulp is a Certified Professional Geologist with a B.Sc. Earth Sciences with honor from the University of Tulsa, and M.Sc. Geology from the University of New Mexico. Mickey has 35 years experience as an exploration geologist and analyst searching for economic deposits of base and precious metals, industrial minerals, uranium, coal, oil and gas, and water in North and South America, Europe, and Asia.

Mickey worked for junior explorers, major mining companies, private companies, and investors as a consulting economic geologist for over 20 years, specializing in geological mapping, property evaluation, and business development. In addition to Mickey’s professional credentials and experience, he is high-altitude proficient, and is bilingual in English and Spanish. From 2003 to 2006, he made four outcrop ore discoveries in Peru, Nevada, Chile, and British Columbia.

Mickey is well-known and highly respected throughout the mining and exploration community due to his ongoing work as an analyst, writer, and speaker.

Contact: [email protected]

Disclaimer and Notice: I am not a certified financial analyst, broker, or professional qualified to offer investment advice. Nothing in any report, commentary, this website, interview, and other content constitutes or can be construed as investment advice or an offer or solicitation or advice to buy or sell stock or any asset or investment. All of my presentations should be considered an opinion and my opinions may be based upon information obtained from research of public documents and content available on the company’s website, regulatory filings, various stock exchange websites, and stock information services, through discussions with company representatives, agents, other professionals and investors, and field visits. My opinions are based upon information believed to be accurate and reliable, but my opinions are not guaranteed or implied to be so. The opinions presented may not be complete or correct; all information is provided without any legal responsibility or obligation to provide future updates. I accept no responsibility and no liability, whatsoever, for any direct, indirect, special, punitive, or consequential damages or loss arising from the use of my opinions or information. The information contained in a report, commentary, this website, interview, and other content is subject to change without notice, may become outdated, and may not be updated. A report, commentary, this website, interview, and other content reflect my personal opinions and views and nothing more. All content of this website is subject to international copyright protection and no part or portion of this website, report, commentary, interview, and other content may be altered, reproduced, copied, emailed, faxed, or distributed in any form without the express written consent of Michael S. (Mickey) Fulp, MercenaryGeologist.com LLC.

Copyright © 2018 Mercenary Geologist.com, LLC. All Rights Reserved.