The Anatomy Of Volatility And What It Means For Gold

Can we use volatility to diagnose financial bubbles? Lessons from 40 historical bubbles

“We inspect the price volatility before, during, and after financial asset bubbles in order to uncover possible commonalities and check empirically whether volatility might be used as an indicator or an early warning signal of an unsustainable price increase and the associated crash. Some researchers and finance practitioners believe that historical and/or implied volatility increase before a crash, but we do not see this as a consistent behavior. We examine forty well-known bubbles and, using creative graphical representations to capture robustly the transient dynamics of the volatility, find that the dynamics of the volatility would not have been a useful predictor of the subsequent crashes. In approximately two-third of the studied bubbles, the crash follows a period of lower volatility, reminiscent of the idiom of a “lull before the storm”. This paradoxical behavior, from the lenses of traditional asset pricing models, further questions the general relationship between risk and return.”

MK note: Why are the ETH Zurich findings important now – after we have already had the first wave of a potentially larger crash?

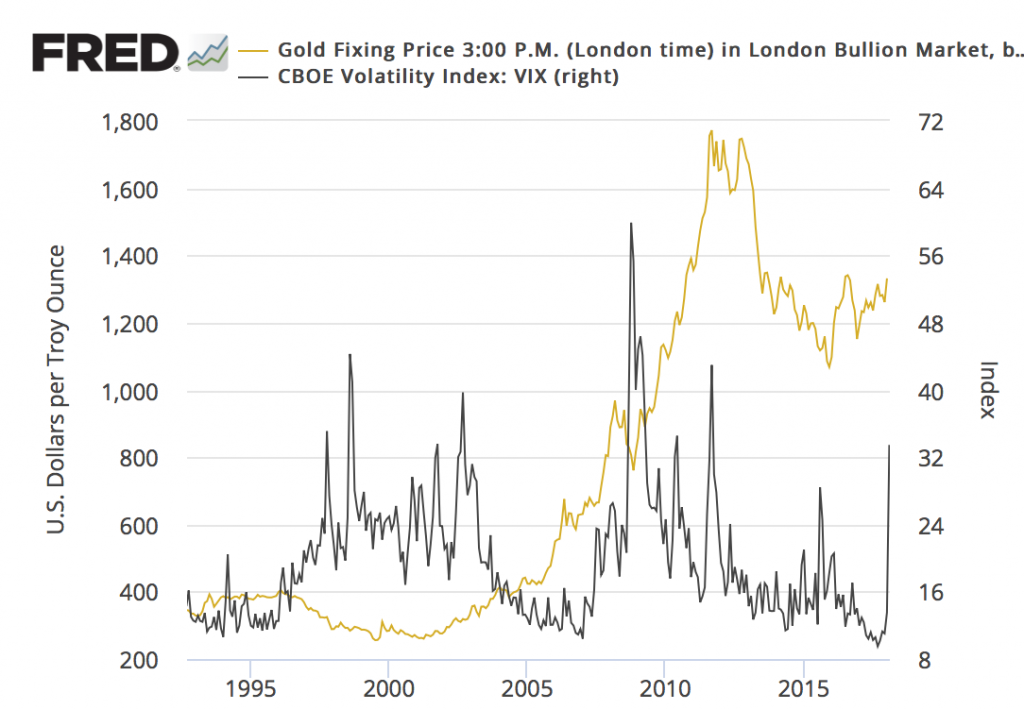

First, Sornette and company have it right, at least insofar as volatility and the current stock market bubble goes. The low volatility as shown in the chart above was the “lull before the storm.” So their theories deserve serious attention.

Second, what we have experienced thus far, as ETH Zurich goes on to point out in its lengthy study, might be only the first phase of what could develop into a full blown crash with severe implications to the economy as a whole. It uses the 1929 crash (and 39 other episodes) as an example:

“Then [after the initial crash], volatility shoots up massively, but this is clearly the direct consequence of the crash and cannot in any way be used as a precursory warning signal of the bubble. One can also notice that, after its explosive growth in October 1929, the volatility decreased in the four months following the crash, but started to increase again afterwards. This is a signature of the fact that the crash was only the beginning of what would develop into a multi-year depression that impacted severely the stock market, which would find an absolute low of 41 on July 8, 1932, corresponding to a total cumulative drop of 89% since the all-time peak on September 3, 1929.”

An interesting chart accompanies that statement (not included here but worth a close look at the link above). I include this passage not so much to suggest an outcome, i.e., deflation, disinflation, inflation, stagflation, et al, but to alert our readers that the first signs of volatility may be, in fact probably will not be, the last. In their study, they show a massive spike in volatility almost four months after the initial surge.

Third, and most importantly from the perspective of current and would be gold owners, it is important to understand that in recent history volatility has preceded upward movement in the gold price, as shown in the chart above. Volatility, as ETH Zurich points out in the first quote, may not spike before the crash, but it most certainly has surged in the past before an increase in the price of gold.

Gold has been under cross examination over the past week as to why it hasn’t gone up while stocks have gone down. Just as complacency and low volatility were the “lull before the storm” in the stock and bond markets, the hesitation to buy gold might be a reaction among investors akin to the deer being caught in the headlights. The true reaction – bolting for the woods – might be yet to come, as the chart above indicates.

Disclaimer – Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset-preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD does not warrant or guarantee the the accuracy, timeliness or completeness of the information found here. (Please see our Risk Disclosure here.)