Awakening The Tiger – Precious Metals In 2022

Interest Rates Rising: A Very Bullish Signal For Precious Metals

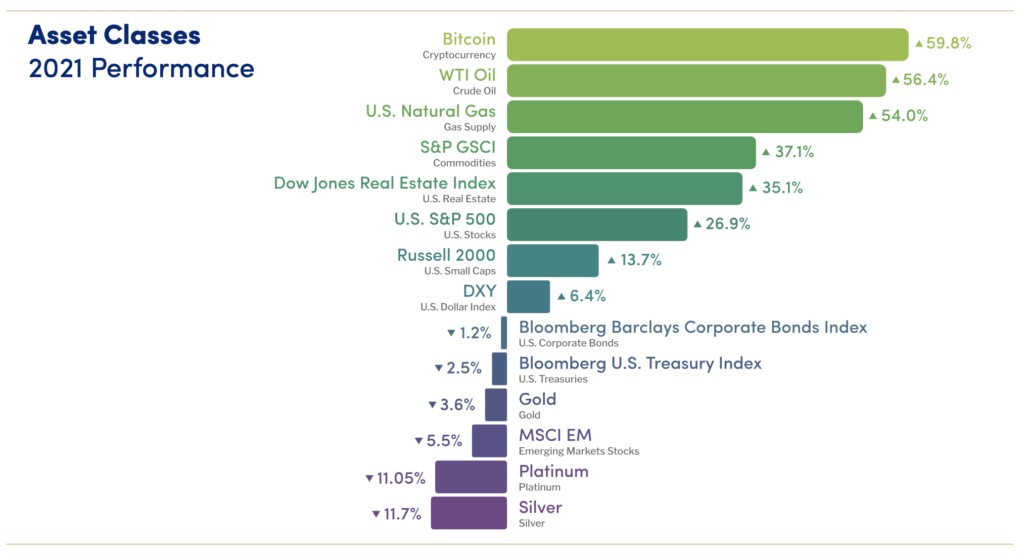

As we enter 2022 and reflect on how each asset market performed the previous year, initial conclusions would suggest that for precious metals, the price action performance seemed highly contradictory. A deeper analysis, however, suggests that the market moves have been exclusively driven by Central Banks and their gigantic liquidity programs, with once-in-a-lifetime ‘lockdown’ anomalies also having a negative impact on certain assets, for example Platinum.

Alongside this realisation, it becomes easier to comprehend the signals that a major global macroeconomic turn in fortune is upon us, one that is once again led by our Central Banks and in particular, the USA, Europe, and China.

Precious metals such as Gold are a crisis hedge, or more accurately a confidence barometer; and this premise has always held true historically. Confidence in our global monetary system is fraying at the edges, and in this article, I hopefully elucidate to the readers the growing negative macroeconomic landscape, which is extremely bullish for precious metals, especially in the context of their considerable undervaluation presently.

Why did asset price moves in 2021 look highly contradictory at first glance?

Last year broke historical records. One of the main drivers was US Money Supply, measured by the expansion of broad money supply; which grew at a rate of over 30% YoY in 2021 alone. This has never been seen before. In fact, The Fed’s overall policy response (a myriad of liquidity schemes throughout this pandemic) are without precedent and 2021 was very much in the heat of the after-burn of this vast expansion in liquidity. Broad economic inflation is always a monetary phenomenon; and such an expansion of the money supply always has an initial lag effect of up to between 18 and 24 months, before headline inflation starts feeding through the system. The collective jawboning from The Fed that inflation was and is transitory is simply a public misnomer and we accurately surmise that their true policy is in fact, a monetary debasement through inflation. To this effect, they are, of course, achieving their goals.

So, with that in mind, it is no wonder that Bitcoin, oil & natural gas, the overall commodity complex, followed closely by global stock indices and real estate have led the overall charge in asset price appreciation. With FIAT currencies being hard-line and publicly ‘debased’ and ‘real nominal’ interest rate yields setting new records for being the most steeply negative yields in over 70 years of peace-time history in US recorded data.

The markets have therefore reacted predictably, off the back of colossal Central Bank largesse, with this torrent of excess capital rushing into stocks as well as the overall commodities complex. The start of this commodity super-cycle is now firmly upon us as predicted, and a significant diversification and exposure to this asset class at this juncture must be deemed critical. Cryptocurrencies also had a spectacular year (the near 50% correction since the November highs notwithstanding) as sovereign currency was and continues to be, heavily debased in value.

With broad money supply growing over 30% YoY and the supply of Gold (as a finite and limited resource) only expanding by just 1.5% per annum; alongside those incredibly important metals to industrial growth such as Silver and Platinum, why then were their respective performances in 2021 so contradictory to the price rises observed in commodities and cryptos?

So Why Exactly Did Precious Metals Underperform in 2021? Was It a Short-Term Phenomenon?

Gold suffered a small annual loss in price of -3.6% vs USD in 2021 (Gold was however higher in AUS, EUR, JPY etc), which is the worst negative annual performance since 2015. The USD did have a very strong annual gain of +6.4% on the FX markets.

As a contextual reference point, Gold rallied +24.6% in 2020 and + 18.9% in 2019 versus the USD.

Net buying of Gold by global Central Banks in 2021 remained very strong, while SPDR Gold Shares, the largest Gold ETF (exchange- traded fund) posted net outflows of over US$10 billion into early December. This is the largest outflow since 2013 and equivalent to roughly 193 tons of Gold bullion. Total ETF Gold selling was 287 tons. Official physical Gold buying by over 14 sovereign Central Banks more than compensated, by ‘net’ buying over 400 tons of Gold in pursuit of balance sheet diversification, as per the last estimates for 2021.

Gold “appears relatively out of favour at the moment,” (by investment houses) said Evy Hambro in early December 2021, global head of thematic (identify macro-level trends) and sector-based investing at BlackRock in an emailed response to questions. Though he did say that the current negative investor sentiment toward bullion presents “more upside risk than downside risk next year” in 2022.

Gold is often used by pension, wealth managers, hedge fund managers and real-asset money managers as a portfolio diversification and insurance protection against negative knowns or unknowns, whether it is macroeconomic or geopolitical developments. The tsunami of money provided by governments and central banks following the first wave of the Covid-19 outbreak in 2020 and into 2021 helped reduce short-term macroeconomic risks and hence ETF Gold sales revenue and new Central Bank liquidity poured into equities sending the stock markets sharply higher. As a result, the wealth market was more focused on garnering net growth by buying into the stock markets and commodity sectors in 2021 off the back of this mind-boggling Central Bank largesse.

Silver has a strong price correlation to Gold and its price was naturally tempered by lacklustre investment demand and diversification in 2021. With the great economic slowdown off the back of global lockdowns, came a sharp reduction in the manufacturing of solar panels and a whole host of other industrial applications requiring Silver. When taken together with the increase in mine production of Silver in 2021 (vs. 2020) the price picture becomes somewhat self- explanatory.

2021 also presented considerable problems with a severe global semiconductor micro-chip shortage. This shortage was so prevalent that car manufacturers were forced to reduce production dramatically throughout the year. In the UK for example, car production plummeted to a new low in July 2021, marking the worst July performance for the industry since 1956! We have all seen the developments in the 2nd hand car market with prices for available vehicles being raised sharply higher due to very strong demand and extreme wait times for new vehicles of anywhere between 6 months to 12 months for new orders placed.

Further evidence of the severity of the semiconductor chip shortage and the impact it has had on the car, van and truck production industry can be extrapolated from the following numbers: a very basic Ford Focus typically uses circa. 300 to 450 micro-chips, whereas most modern combustion engine cars have very complex electronics and can use between 1,500 to 3,000 chips, one of Ford’s new electric or hybrid vehicles can utilise up to 3,000 chips per car. Tesla cars typically have over 3,000 chips per car.

Semiconductor chips are used to power a variety of vehicle and truck features, from power steering and reversing cameras to emergency braking systems and skid control, engine management systems, emission controls and navigation systems. With a forced slowdown in production, this caused global auto industry conglomerates to pull back almost entirely from metal purchases as well as other components required to build vehicles and rely on their metal stockpiles during lockdowns in 2020 and 2021, the latter of which was further exacerbated by the industry-debilitating chip shortage. This directly affected the industrial demand for Platinum which is used heavily within the catalytic converter in order to reduce noxious oxide pollutants. Despite the semiconductor chip shortage, which is due to be eradicated this year, automotive demand for Platinum is forecast to grow by well over +20% in 2022 as a function of the headlong and rapid substitution out of Palladium and into Platinum, as well as the higher loadings of Platinum required to meet ever tightening emissions legislation.

In 2021, we also had the major ACP processing plants coming back online in South Africa, having been rebuilt after blowing up in early 2020. All this excess aggregate that had been built up from continued mine production during 2020 and early 2021 was pushed through the plants at breakneck speed, with plants running well over processing capacity recommendations. The mining producers however needed to process and sell this aggregate into the market quickly as cash flow injections were essential. With an artificial short- term overload of excess metal being sold into the market while at the same time industrial end-users were being forced to hold back their metal purchases (as a result of chip shortages); this directly impacted prices within the Platinum market.

Investment demand was also damaged by the extreme mass media marketing and new fandangled love affair with BEV’s (Battery powered Electric Vehicles). The ongoing narrative being that Electric Vehicles are going to take over all fleets of the world, which is total hyperbole and an entirely irrational assessment of the actual roll- out and implementation of BEVs. Real world economics somewhat being ignored, concerning vans, trucks and heavy vehicle solutions are not suitable for BEV’s, the limited commodities available to produce batteries on the global stage, gigantic infrastructure replacement costs and necessary build-out of our electrical grid systems to support a growing fleet size, emerging markets and economies will continue to focus solely on ICEV’s (Internal Combustion Engine Vehicles) make this BEV reality unworkable.

There is also the simple and unequivocal fact that BEV’s are not green and are not solving the energy production issue whatsoever. They are simply pushing pollution out of cities and into urban areas where giant energy production plants burn gas, coal, oil, wood pellets and nuclear power to supply the enormous amounts of electricity required.

The investment markets (extremely influential in the prices of precious metals) have consequently thrown the ‘baby out with the bath water’ with respect to several of these precious metals in 2021. This is a situation that we are resolutely confident is about to change.

How Is The Macroeconomic Picture in 2022 Setup in Relation to Precious Metals?

A macroeconomic regime change is upon us; one that is being driven by inflationary forces alongside persistent economic stagnation and hence deflationary forces, ultimately stagflation. All the ingredients are well in place for a secular shift in the inflation outlook over the medium-term horizon (over and above monetary debasement) due to extreme and growing aggregate supply shortages.

CPI (the newest version of the government’s ‘suppressed’ inflation metric) has been rising sharply across almost all economies, and long-term inflation expectations have been rising in tandem. These forces are exceptionally deep rooted and extremely stubborn and therefore we must expect inflation over the coming years to not only be volatile, coming in waves and mini-cycles and not simply in one direction higher, the inflation genie has been firmly extricated from its bottle.

Long-term (inflationary) policy drivers will be clearly based on:

- Fiscal and monetary tailwinds supported by the need to devalue overwhelming and rising debt burdens across all sectors, as well as huge shortfalls in unfunded obligations such as pensions,

infrastructure builds, medical care, etc.

- Chronic underinvestment (CAPEX) in basic resource industries at the core of the supply chain and within the overall commodity complex (China has been especially focused on this and is very vulnerable).

Let us focus on two of the largest industrial nations on earth that contribute to over 42% of global GDP: The US and their economic policies and direction and China with their industrial juggernaut. Their collective economic issues and policy directions will provide a clearer view of the direction we are heading towards.

The US and Also Europe

Monetary policy over the last few years has been wholly centred around flushing tsunamis of liquidity throughout the economy. This quantitative easing or (QE) more popularly recognised as money printing, bolstered classic asset markets such as property and stock indices, enabling ever-increasing debt growth and leverage with the support of zero percent interest rates. This is about to radically change over the short to medium term in the Western world.

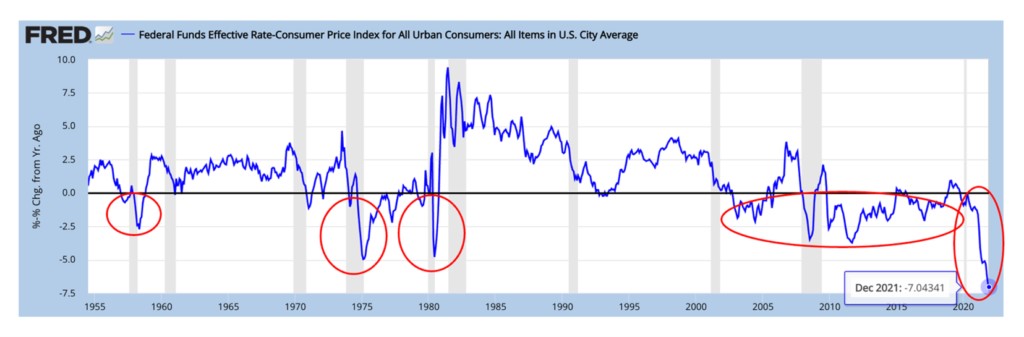

The US and indeed the UK and Europe have steeply-negative real interest rates, the worst such incidence in peace-time history. The US has actually broken their own historical record for real negative interest rates; which are now even more negative than during the ‘financial repression’ of the 1950s that was required to pay for the build-up of debt during the Second World War by debasing the currency, then again we had the extreme inflation decade of the 1970’s (more accurately recorded as stagflation of the 70’s) during which period they were forced to raise interest rates close to 20% to fight inflation.

Since the financial crisis of 2010 monetary policy authorities have attempted and successfully managed to push real rates again into negative territory for as long as possible (financial repression through debasement). Unfortunately, at this juncture, they have quite simply lost control.

The US Federal Reserve finds themselves in a position where they have lost control of inflation and at serious risk of losing confidence in the system itself, that would otherwise continue to attract investment flow capital and growth dynamics. This is leading to a situation whereby they lose control of the debt markets with debt collapsing and bond yields (interest rates) soaring and in turn, this will drive a collapse in asset markets, property and equities in particular, being priced to perfection and extraordinarily debt leveraged. This will cause the collateral valuation bubble that has been holding up the gigantic debt mountain (currently surpasses 900% of GDP) to burst.

- Total debt is calculated as the sum of liabilities of household, business, local state and government, federal government and corporate and financial institutions.

The Fed needs to act, and they need to act fast, but raising interest rates could have ramifications that stem way beyond the territories of their control.

China

They are facing growth and debt issues and they currently seem to be in the opposite monetary position of the US who are looking to tighten monetary policy while China has been lowering rates recently and pumping cash into the financial system. China has well recognised and long-term structural problems which cannot be ignored and are probably best described as ‘dark political and economic clouds on the near to medium term horizon’. The ‘sea change’ in China as compared with the 90’s and 2000’s is being driven across multiple fronts.

In no particular order:

Ageing and negatively skewed demographics are pointing to a -15% population fall within the next 15 years as well as a similar sized shrinkage of the working age population. By 2050 over half a billion people in China will be over 60 (well over one third of their population) placing an incredible strain on their underfunded and underdeveloped welfare system. The considerably higher savings ratios deemed necessary for the ageing population will in turn undermine the government’s former policies for pushing China into a consumer-based economy.

Inequality of wealth distribution across the country is extreme and even has a great effect on education, income spreads has been actively discriminating against women which is causing growing social fragmentation.

Ecologically speaking, China has severe issues with water shortages, topsoil degradation and pollution, which have all raised serious political tension with South Asia as China is now targeting upstream sources of water coming directly from the Himalayas.

China also has severe shortages of raw materials. They are not self- sufficient in food, energy, hard commodities nor metals to support their industrial powerhouse. This is very inflationary over the short, medium and long term horizons as a result of cost-push inflation on commodity demand curves.

China’s leader Xi Jinping has instigated an authoritarian new rule of law, quite obviously a new direction of heading towards state- owned industries and re-nationalisations in many cases. State owned enterprises are recognised as being up to 30% less productive than privately owned Chinese enterprises. These state-owned industrial enterprises and conglomerates are widely recorded as being at least 20% less productive than their competition in the West.

Acute issues: Capital Output Ratio is negatively skewed with low productivity, higher savings requirements by its populace in the face of burgeoning retirement costs. This will contribute to an ever- expanding debt mountain at governmental levels. Both public and private debt is estimated at being well over 300% of GDP. China needs ever-increasing foreign investment and income, at a time when their new anti-capitalistic business model is causing grave concern and strain with overseas investors.

In the 1990’s China issued a policy of land sales and development which was promoted as a form of higher saving for the people of China. This policy has directly led to a property bubble that is only historically matched by Japan’s extreme property bubble of the late 1980’s (eg. commercial and residential property within the Tokyo metropolis collapsed in value by 74% between 1989 and 2015).

Up to one half of China’s economy is attributable to the property economy of the last 2 decades, 80% of personal wealth is now tied up in property and one third of local state municipalities and local government tax intake is derived from property transactions. Clearly property prices are unsustainable and falling hard alongside property developers moving rapidly into bankruptcy. Based on urban migration patterns, it will take close to 10 years for all available vacant properties to be taken up, a truly massive overhang or property glut.

What all of this is beginning to point towards, is that the Chinese economy is heading into very low growth and economic stagnation strangled by very high and growing debt loads, falling property prices adversely affecting wealth and savings, poor age demographics, while their overall demand for commodities coming from outside of China will remain extreme – stagflation.

Conclusion

It is important to examine closely what governments and Central Banks are actually doing rather than what they are saying. Physical precious metals today are the ultimate analogue tangible asset in a world of leveraged, digitised and financialised assets. Central Banks themselves have been on a massive Gold buying spree for the last 11 consecutive years.

2021 was a very disappointing year for precious metals; but has the major trend turned and are the next few years about to get very exciting for metals?

The world has a great many risks from geopolitical and trade tensions, war footings, global supply/demand deficits across the commodity complex, a new direction for monetary tightening in the West, a severe global debt crisis with extreme debt leverage, gargantuan global infrastructure developments – especially in the energy sector and the prominent agenda for climate and pollution controls; all adding to the extreme strains on demand for precious metals. One must also take in consideration that historically, precious metals outperform when interest rates rise.

We are in the throes of an outright monetary debasement, causing financial repression of a scale that both the USA and Europe have not seen in post war peace-time history. This is a destruction of currency value or a stealth population tax with the sole policy intention of reducing the phenomenal debt load. This crisis is exceptional and must neither be understated nor misunderstood.

Asset prices in the traditional classes such as stocks and housing have been pushed into the realms of risk and overvaluation metrics that have not been seen in the last 100 years. So, a re-shifting and re-weighting of portfolios into the commodity complex and precious metals is now slowly underway and is being led by smart money.

The US, Europe and China’s forward looking macroeconomic indicators (as briefly explained above) are leading us squarely into stagflation. Stagflation is an unenviable situation where inflation remains high (great demand for commodities alongside aggregate supply shortages and crippling debt loads; that require inflating away through currency debasement) and the economic engine growth rate slows (in this case, stagnating as a result of the strangulation of overvalued asset prices and worsening political and economic headwinds).

The US bond markets are beginning to send signals of a recession on the horizon in the USA and this is likely to happen in 2023, although could be triggered in late 2022. Put simply, the Fed is being pushed into monetary tightening by politics and the inflationary pressures that have been let loose, with new measures designed to curb the inflation of an overheated economy by increasing interest rates and reversing QE (monetary tightening). This in turn will trigger an economic slowdown which will be accompanied by falling asset markets (as visibly seen last few weeks). With debt servicing costs rising and incomes falling (together with falling asset prices) this will then lead to a period of policy reversal once more, with renewed monetary expansion from the Fed as they attempt to stave off the very worst effects of a possible severe recession, without ever actually containing the inflation monster in the first place.

We have rising short term yields (1, 2, 3, 5 year yields) while the long end of the curve is flattening. This is sending clear recessionary signals. You have interest rates going up at the short end and going down or flattening at the long end of the curve. When interest rates move ever further on the short end and lower on the long end, this creates yield curve inversion, which has preceded every recession of the past 50 years.

China will continue to support their economy with monetary aggregate expansion, loose monetary policy and debt growth instigated by the government, alongside aggressive demand for commodities over the next few years (especially metals) which will fuel cost-push inflation.

The semiconductor microchip order shortages are now being filled and with this, new car, van and lorry production back-orders will ensue, fuelling extremely strong demand for Platinum, at a time when mine production and Platinum ore grades continue to fall. This does not even account for the rapidly rising demand curves emanating from the new and global push into Hydrogen, where the electrolysis process for green Hydrogen production and for the process of then turning that Hydrogen into electrical energy, requires Platinum (as well as Iridium).

Silver industrial demand is rising rapidly as our global governments push for this global energy transition, with solar, electrification, medical, pollution and water purification controls pushing the demand curves ever higher for Silver. Of course, Silver also benefits from the investment global shift required for prudent asset diversification and accumulation as a monetary or crisis lifeboat.

Why Rising Interest Rates Do Not Hurt Gold? In Fact, the Opposite

This is absolutely not the case and quite the opposite has occurred historically. The only way rising interest rates will hurt the performance of Gold, is if the central planners could actually push interest rates to net real positive territory without harming the economic fundamentals of the economy. At this juncture, this would mean a series of interest rate rises in the USA to over +7.5% (as the CPI inflation metric is presently over 7%). Interest rates at those levels would however, cause their economy to collapse along with their banking system.

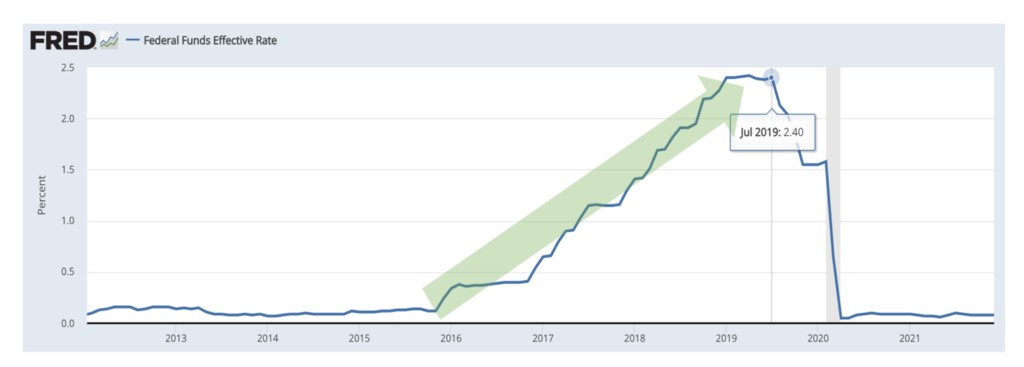

From late 2015 into 2019, the Fed raised interest rates from 0.06% to 2.45%. During this precise time period, Gold rose vs. the USD by +49%.

From June 2004 to June 2006, the Fed raised interest rates from 1% to 5.25% and Gold rose from US$382 up to US$728 (+90% return) during that same time frame.

From 1972 to 1980, the Fed raised interest rates from 3.30% to 19% (by 5.75 times!) and Gold rallied from US$42 up to US$878 (or by 20.9 times!).

In the period from 1974 to 1976 when the Federal Reserve actually lowered interest rates gold actually fell in that same time period, when the interest rate hikes started again in 1977 was when gold started rising quickly yet again.

Interest rate rises do not hurt the Gold price or precious metals; and to suggest otherwise simply overlooks historical data and misinforms the investing public.

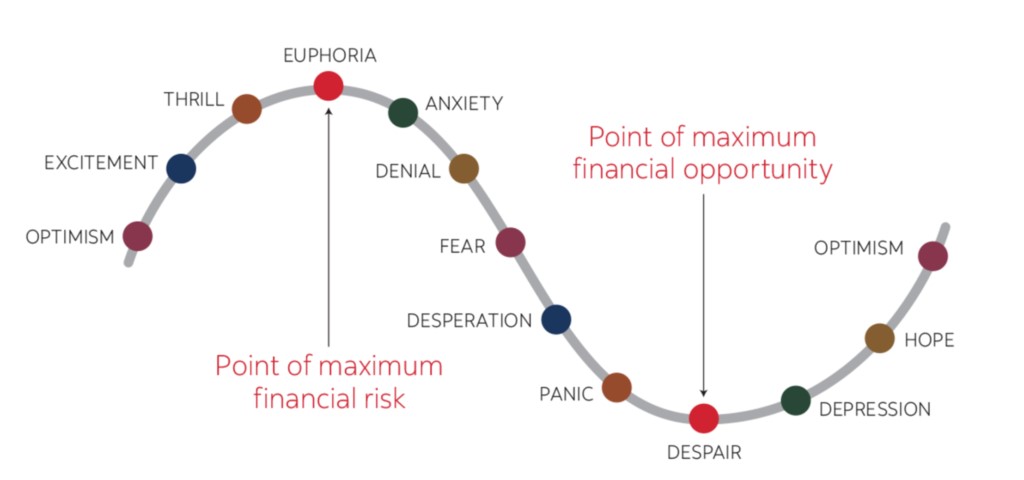

Sentiment Cycles

Do not let your emotions get in the way of making smart investment decisions. Within a protected asset portfolio, understand the level of diversification required and maintain a clear understanding of the macroeconomic and geopolitical situation moving forwards. With this approach, you can then be better placed to fully grasp why precious metals offer an exceptionally attractive investment thesis; and then determine how such a portfolio of metals should be optimally weighted at this stage.

It is notoriously difficult to separate emotion from the realities of market action and price overextensions (either up or down) and this tends to lead to unchecked emotional decisions, giving rise to suboptimal investment choices.

Dr. Daniel Crosby wrote the book ‘The Behavioural Investor’, a psychologist and academic of behavioural finance; and he reminds us that our emotions can’t be trusted when it comes to making investment decisions.

“The fact that your brain becomes more risk-seeking in bull markets and more conservative in bear markets means that you are neurologically predisposed to violate the first rule of investing, “buy low and sell high.” Our flawed brain leads us to subjectively experience low levels of risk when risk is actually quite high, a concept that Howard Marks refers to as the ‘perversity of risk’.” – Dr. Daniel Crosby

Like the stock market, our emotions are cyclical. The cycles of emotions experienced as an investor can range from pure euphoria to utter despondency (and lack of hope).

At the end of 2021 and into the first week of January 2022 we were clearly aware that sentiment towards precious metals had evolved into a range of emotions from panic and despair, both from the market in general as well as from several of our clients. The hard facts and research however, continues to demonstrate a clear buying opportunity.

We utilise the whole arsenal of metrics and differing market analysis to make the right decisions from a portfolio perspective, and a clear understanding of cycles (time-frame) in particular are ALL IMPORTANT. Understanding where we are in the overall cycle and whether this trade is going to continue for 2 or 4 years or even longer is paramount. We then encourage our clients to optimise their entry and exit levels within particular mini or micro cycles within the overall cycle time-frame.

Pinpointing extreme highs and lows is a difficult exercise, but we can all be very successful in maximising our returns by understanding which asset class we must have ample exposure to in each part of the economic cycle.

Forecasting precise price action is fraught with danger, though knowing where we are in the various cycles on the back of a great deal of research and analysis gives us very strong assurances indeed on the price direction and when to expect the fireworks.

We are facing war footings with Russia, China may well utilise this European diversion to make their own incursions into Taiwan, especially considering their massive semi-conductor microchip shortage and technology gaps with the West. We have monetary tightening in the USA which is going to wreak havoc with several vulnerable asset classes and growing cost-push inflationary pressures across the commodity complex which clearly demonstrates itself in the numbers as stagflation trends globally.

We are expecting precious metals to have a particularly volatile year ahead because of these severe economic and political headwinds, and we are forecasting healthy price appreciation in 2022 for the calendar year overall. Leading us into 2023 and 2024 were we expect explosive rallies to materialize in the precious metals.