Bank Exchange For Physical Use Falls Sharply

share

share

share

share

share

share

share

share

share

share

At Eric Sprott's urging, we've been monitoring the daily abuse of the Exchange For Physical process since late 2017. However, since late March, the daily totals have fallen off dramatically. Why?

Again, the "Exchange For Physical" process is an arcane feature of the COMEX futures market that allows a party to exchange a contract for "physical metal" off-exchange, usually in London. Abuse of this process accelerated in 2017, and we've been documenting the absurd totals for nearly three years. Below are just a few links to previous articles on this subject:

- https://www.sprottmoney.com/Blog/comex-exchanges-f...

- https://www.sprottmoney.com/Blog/one-full-year-of-...

- https://www.sprottmoney.com/Blog/exchange-for-physical-craig-hemke-04-122019.html

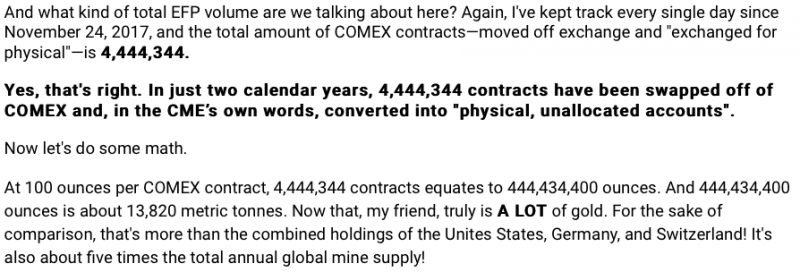

From that third link posted in December of last year, note this key passage on the enormous volume of these transactions:

And EFP abuse actually accelerated in the first three months of 2020. In fact, the first fifteen trading days of March alone saw a total of 290,847 COMEX contracts shifted off-exchange and "exchanged for physical". That's an average of nearly 20,000 contracts per day and more than 29,000,000 total ounces or over NINE HUNDRED METRIC TONNES in just fifteen days! In fact, just one day alone—March 12—saw 38,469 COMEX contracts "settled" this way.

But something has since changed. When The U.S. Fed announced QE∞ on March 23, it appeared to momentarily break the COMEX market. The spread between spot and futures exploded to nearly $100, and many bullion banks have since reported extreme losses in trading that day. The most notable is HSBC, which is said to have lost as much as $200,000,000. See this link: https://uk.reuters.com/article/uk-hsbc-gold-filing...

And now, in the fifty-two trading days since April 1, the total volume of EFPs has been just 182,798. That’s an average of just 3,500 contracts per day...a drop of over 80%. In fact, on May 29, only 789 EFPs were posted. Again, compare that total to the 38,469 on just March 12!

So what's going on here?

Well, it's clear that the bullion banks were abusing this process to make a steady, simple, and relatively risk-free profit each day by arbitraging the price fluctuations between New York and London. In essence, buying or selling a COMEX futures contract in New York and then selling or buying a spot contract for delivery in London and capturing the spread between the two. If you're HSBC and doing this with 10,000 contracts, a simple $2 spread nets you a tidy $2,000,000 profit. Good work if you can get it.

All is well and fine for this trade so long as there's physical metal to deliver versus your spot sale—and this is where the entire machine fell apart in late March. Many mints, mines, and refineries were closed due to Covid-19, and the supply chain of physical metal to the highly leveraged global gold market broke down in spectacular fashion. Without physical metal to deliver, the bullion banks playing the EFP game were forced to close positions in a true short squeeze. The result? It wasn't just HSBC that (literally) took it in the shorts. See this regarding CIBC: https://www.reuters.com/article/us-cibc-gold/canad...

And now there are multiple reports of bullion banks closing up shop in New York and moving their trading operations to London and elsewhere. Did this collapse of the easy money COMEX EFP trade facilitate these moves?

- https://www.bloomberg.com/news/articles/2020-06-12...

- https://www.reuters.com/article/us-health-coronavi...

- https://www.wsj.com/articles/a-scramble-for-gold-is-redrawing-the-map-of-the-market-11591867007

So what does this imply for the highly levered derivative contracts of the COMEX? In March, the CME Group was quick to rush a new contract into existence designed to satisfy delivery demands with fractional ownership of London Good Delivery bars. So far, however, demand for this contract has been abysmal, with only a paltry twenty-five contracts currently being issued and held.

*********

share

share

share

share

share

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.