Battle Not Over, But The Tide Has Turned

share

share

share

share

share

share

share

share

share

share

The War on Gold turned against the forces suppressing the gold price in 2000-2001 when their efforts caused gold mines to reduce production or close. Gold bulls then realised they had time on their side and could accumulate gold and of course silver as they would be well rewarded. In time. It 2011, conditions in various markets had reached a stage where there was great concern among those who favoured the fiat currencies and the might of their authority over markets. They launched a market-wide offensive to reclaim any ground they have lost. A scant few months ago, this effort started to fail; first for silver and gold and the dollar, and now it is being lost against equities as well, as the DJIA fails to hold a long sought objective at 18000. The tide has turned; the battle is being lost. The war is going one way now.

Reporting on a war is fraught with the risk of losing face. One can be so easily see a small part of it and expand that to apply to the whole war, to reach conclusions that time shows to have been wrong. Time is a terrible editor of what a reporter wrote a few years earlier and your author also did not escape; it was only in 2013 when the precious metals broke lower from a consolidation triangle, very much against what technical theory expected, it had become clear the metals bull was in a process of having its horns trimmed.

Then really long term charts recently analysed for the first time, showed that gold, silver and the dollar were changing long-term trends at the end of 2015 -- and that Wall Street was completing its sustained bull market. The DJIA managed another of its strange revivals during May in reaching 18000 last week for a second time during this rally. As anticipated in the comments last week, now that it failed to hold that level, one can say that the final retreat is in place. This reversal to happen imminently too, fits a really long-term chart of the monthly close of the DJIA.

In 2005/6 a series I wrote on Japan and the US anticipated that the US would have its equivalent of Japan’s ‘1990 moment’, perhaps as early as 2006, as prelude for a far different and worse future than that endured by Japan since their property and other markets collapsed in 1990. The main reason for this was Japanese had large savings with which to survive what happened there. US households were not in the same position, in fact the opposite, with large loads of debt. The collapse came as anticipated, but survival of the financial system was achieved in March 2009, when the Fed mortgaged the wealth of future generations by its actions. But survival did not ensure recovered health for reasons to be explained elsewhere in due course.

As has been commented repeatedly in the alternative media, ‘kicking the can down the road’ was not and is not a solution; it only created the circumstances for a new and even greater financial cataclysm. The only question is whether it will begin to erupt in 2016 of whether it can be postponed until well after the election. But come it will…and in spades, loaded for bear.

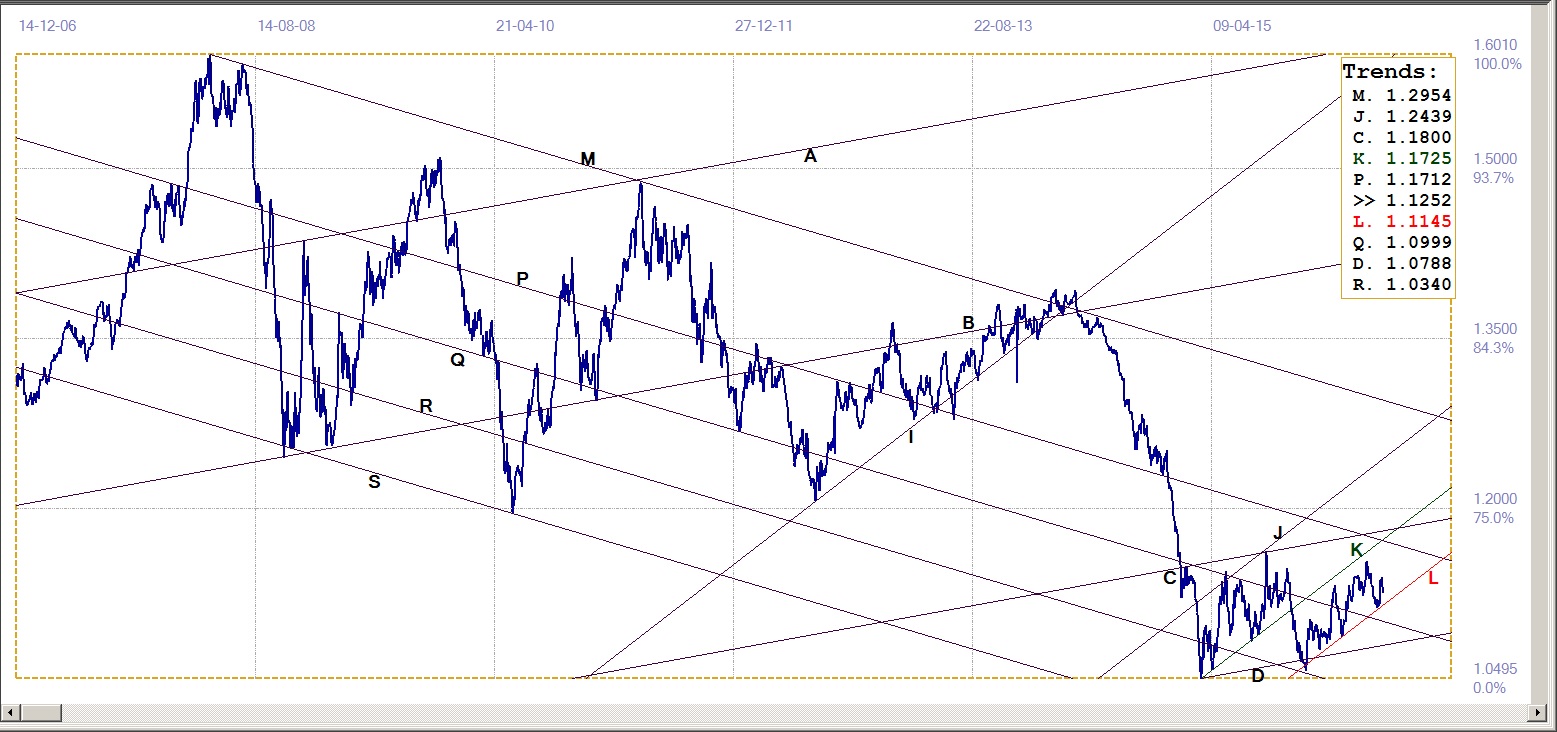

Euro-Dollar

When determined rear guard action had the dollar in a brand new rally, the euro came right to testing support at line L ($1.1145), bottom of its new bull channel, KL. The poor NFP figure provided a springboard and the euro closed the previous week with a good gain, moving clear of the bottom of the bull channel.

However, last week again saw increased interest in the dollar to weaken the euro and it retreated a little. The tone is however still bullish and remains so while the channel remains intact. The first resistance for the euro is at line K, sitting above $1.70, and therefore clearly way out of reach for the near term. However, the real test for the euro is how well it manages to keep away from the bottom of its bull channel while recovering enough to take on the resistance at line K or P ($1.1712).

Euro-dollar, last = $1.1252 (www.investing.com)

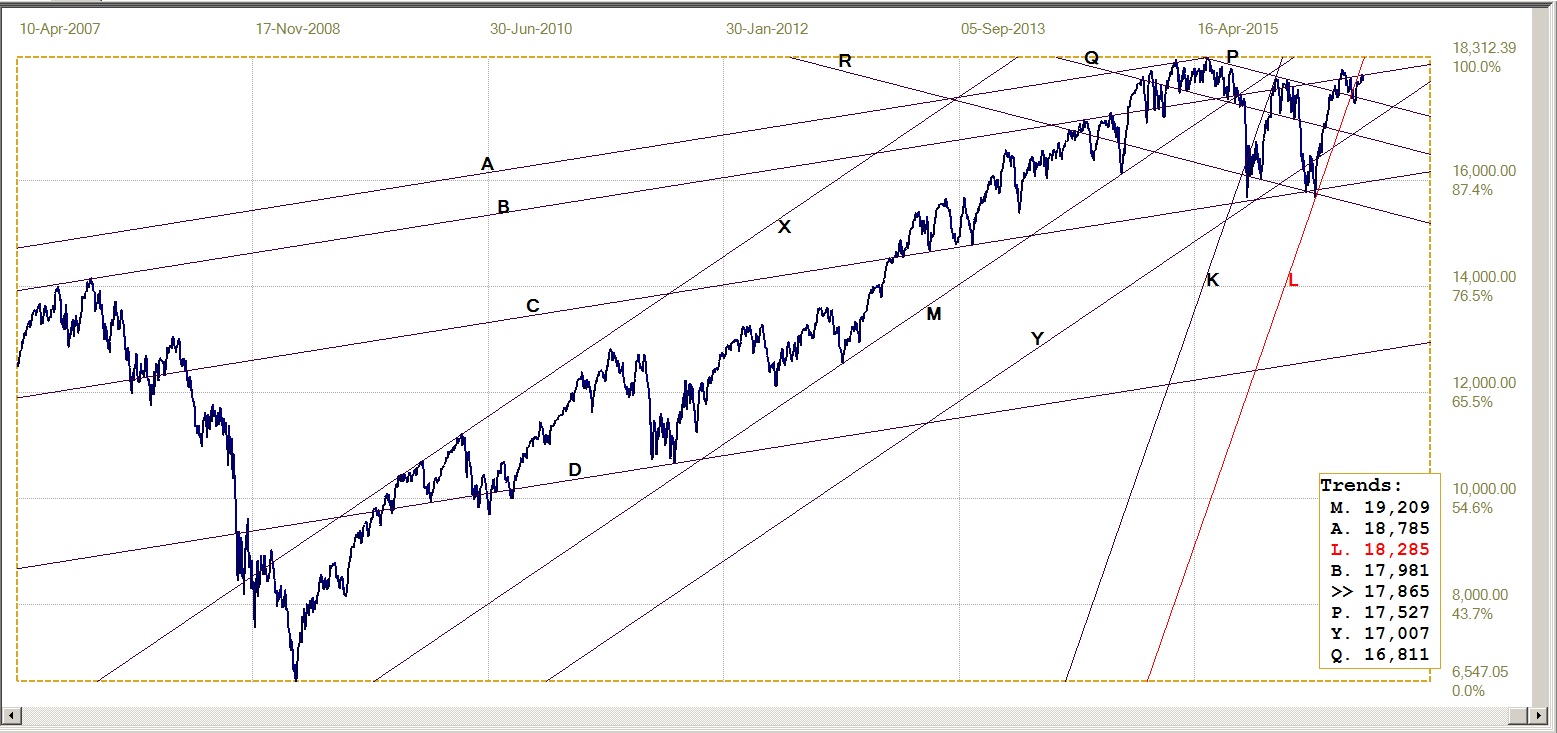

Dow Jones Industrial Average (DJIA)

The failed break above 18000 late in 2015 soon slipped below steep bull channel KL (with line L a little out of reach at 18285) and then had another stubborn rally that has again breached the 18000 level, if only for one day. This move also broke above the resistance at line B (17981), coming quite close to giving what might be a goodbye kiss to line L – if the pull back to below line B turns out to be the start of a new bear trend as is being anticipated.

Having seen how often spike lows on the DJIA reverse into new and as steep rallies, it would be presumptuous to assume that it cannot happen again. However, a long- term analysis on the DJIA monthly close indicates a good probability that the June close will be below the May close of 17787.20, perhaps substantially so. But it will still be a hard fought tussle between bulls and bears if the bears begin to take over.

Dow Jones Industrial Index, last = 17865 (money.cnn.com)

Gold PM Fix - Dollars

Gold has rebounded smartly right off the bottom of the new bull channel at line L ($1225) with its shallower gradient [Line V ($1322) is the lower boundary of the old and steeper bull channel]. Despite a good recovery, the price is still below previous resistance at line C ($1279) and also the resistance at line Q ($1293).

The physical gold exchange in Shanghai was closed on Friday with no report of any trading. They therefore missed a steady state for gold and the gains in the market on Friday and when they return to the market this week traders in Asia might feel they have some catching up to do. That should assist the gold price to move closer to the next psychological hurdle at $1300.

If gold should manage to break back into the steeper bull channel by recovering back above line V, that would be confirmation that the induced shake out to give the holders of short position an opportunity to get out at a less painful lower price is over. The total open interest has decline, but perhaps by less than what had been hoped for. The price did not linger along its lows, which would frighten more longs to close their positions, but rebounded right back and is now probably calling for sustained selling – which means many new short positions for parties who had tried to close their already large net short position and therefore relatively little to gain for the whole exercise. More so if the price now jumps close to $1300 in Shanghai.

Gold price – London PM fix, last = $1275.50 (www.kitco.com)

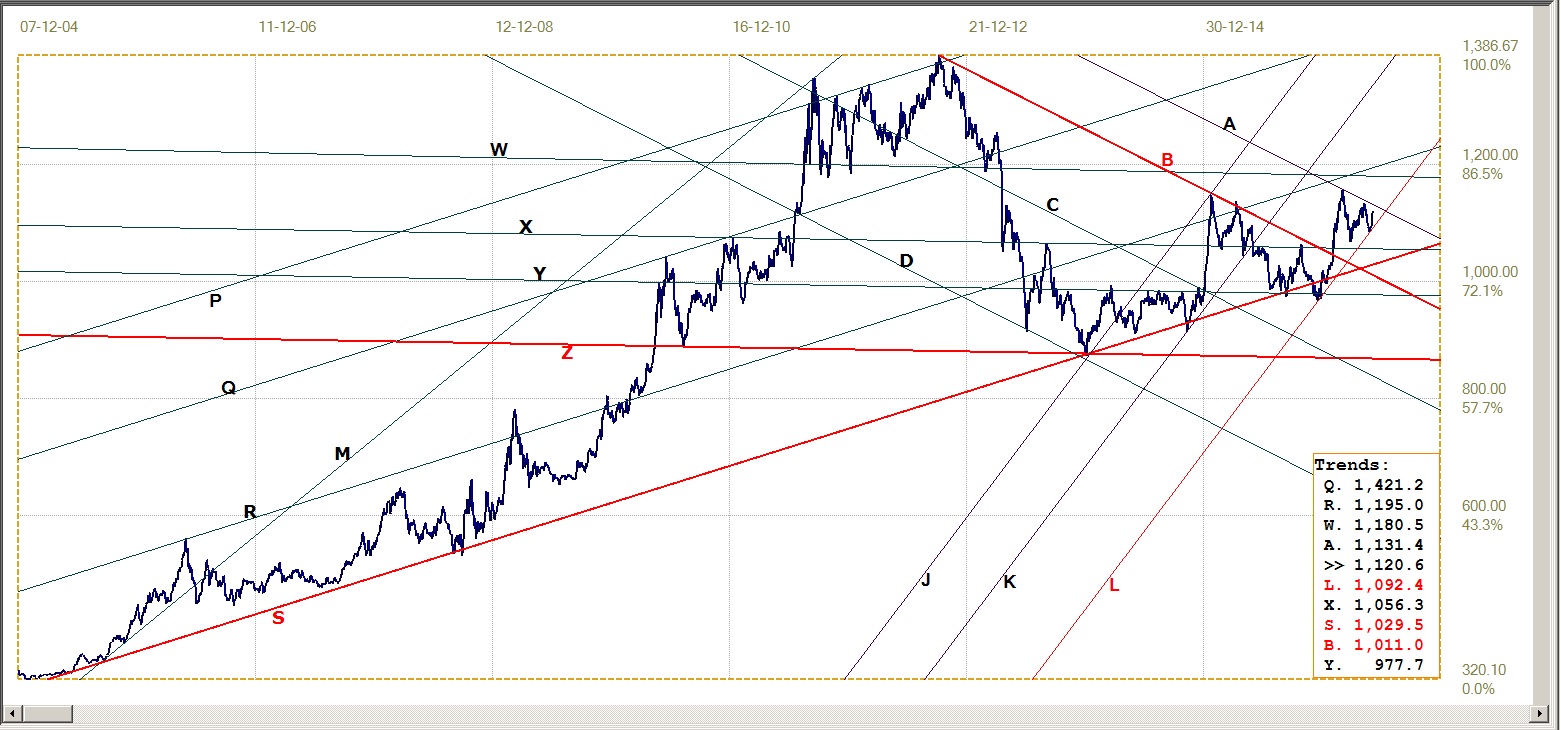

Gold PM Fix - Euro

Euro Gold Price – PM Fix in Euro, last = €1120.6 (www.kitco.com)

With both the euro and the dollar price of gold having held at support and reversed higher, it is not much of a surprise that the euro price of gold had done the same…and is still improving. The prospects look good, provided the bull channel KL (€1093) is able to hold and if resistance at line A (€1131) can be broken. The euro price is of course more subject to influence from changes in the dollar, either as the price of gold vary in dollar terms, or from changes the euro-dollar exchange rate.

Normally, these changes could in sync, with a stronger dollar implying a lower price for gold and a weaker euro, which could balance out to leave the euro price mostly unchanged, and vice versa. It is nevertheless not unknown for the euro to weaken at a time when the gold price is rising, or the other way around – which is not good for gold, while the alternative is good.

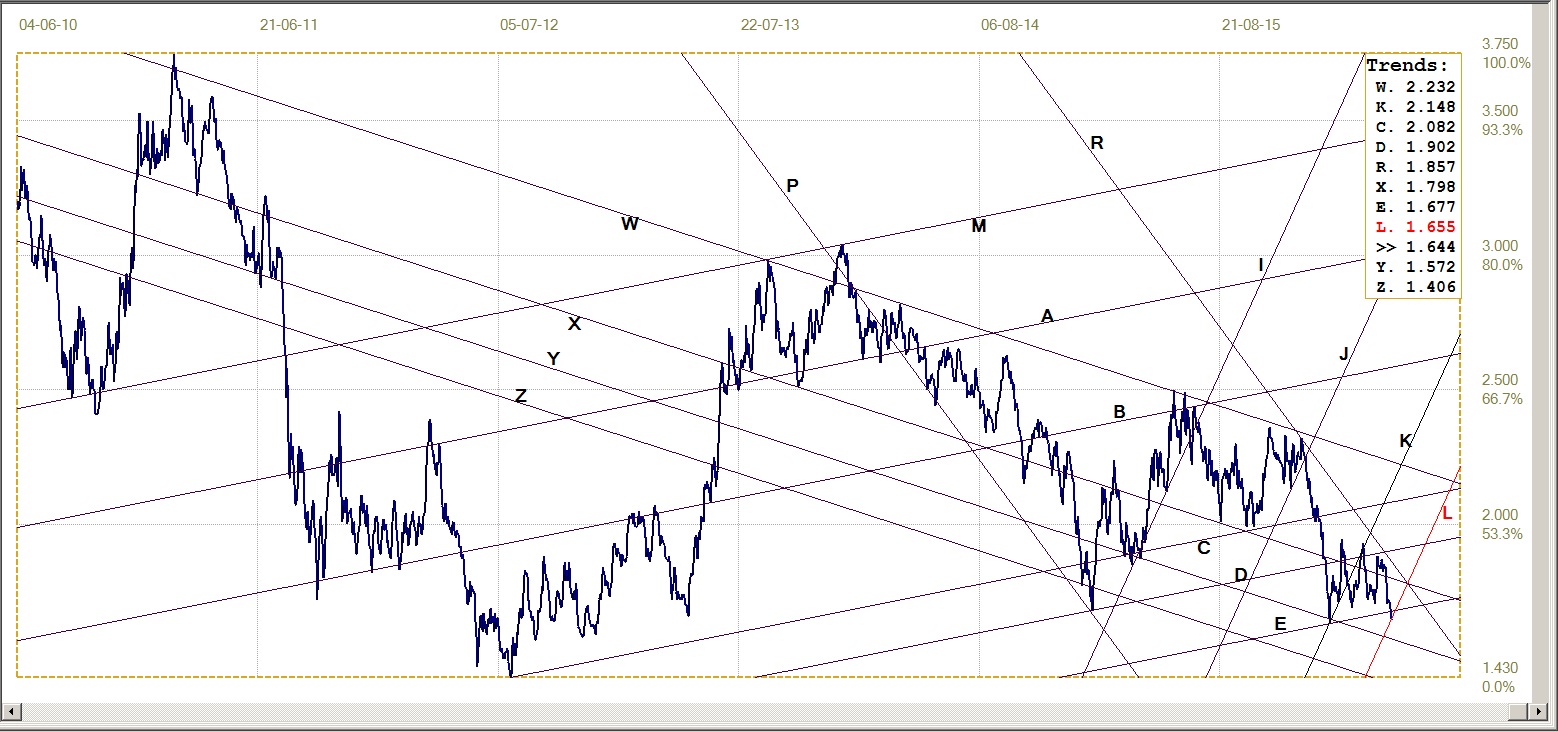

Silver Daily Fix Chart

Silver Daily Fix, last = $17.32 (www.kitco.com)

The adjustment recently made to the gradient of the new silver bull channel – from a steep gradient to the shallower gradient of the new channel KL ($16.309) – has proved to perfectly accommodate the recent weakness. As always, the gradient of the new channel is not arbitrary, but has to be derived from the gradient of master line, M. Last week silver outperformed gold in technical terms, moving higher above the $17.00 level to break above resistance at lines R ($16.71) and D ($16.89) to get into clear space with no nearby resistance as yet identified.

In light of the belief that silver has the more suppressed price, what happens this week in Shanghai after their no trading break on Friday should be closely watched.

US 10-Year Treasury Note

US 10-Year Treasury Note, last = 1.644% (www.investing.com)

The market for the 10-year US Treasury note surged last week after the DJIA failed to hold and extend a break above the strongly desired 18 000 level – clearly being subject to strong selling pressure as new sellers lock in profit at or close to 18 000. Traders far too often behave as herd animals and in this market frequent failed attempts to hold above 18 000 over recent history seems finally to have convinced a majority that they cannot hope for another rally to add some more profit.

The downside now poses greater risk than the potential profit of a new rally that is certain to be limited in its gains. On the other hand, if selling really picks up, buyers will soon disappear and leave owners of equities holding a rapidly losing asset with little support in sight.

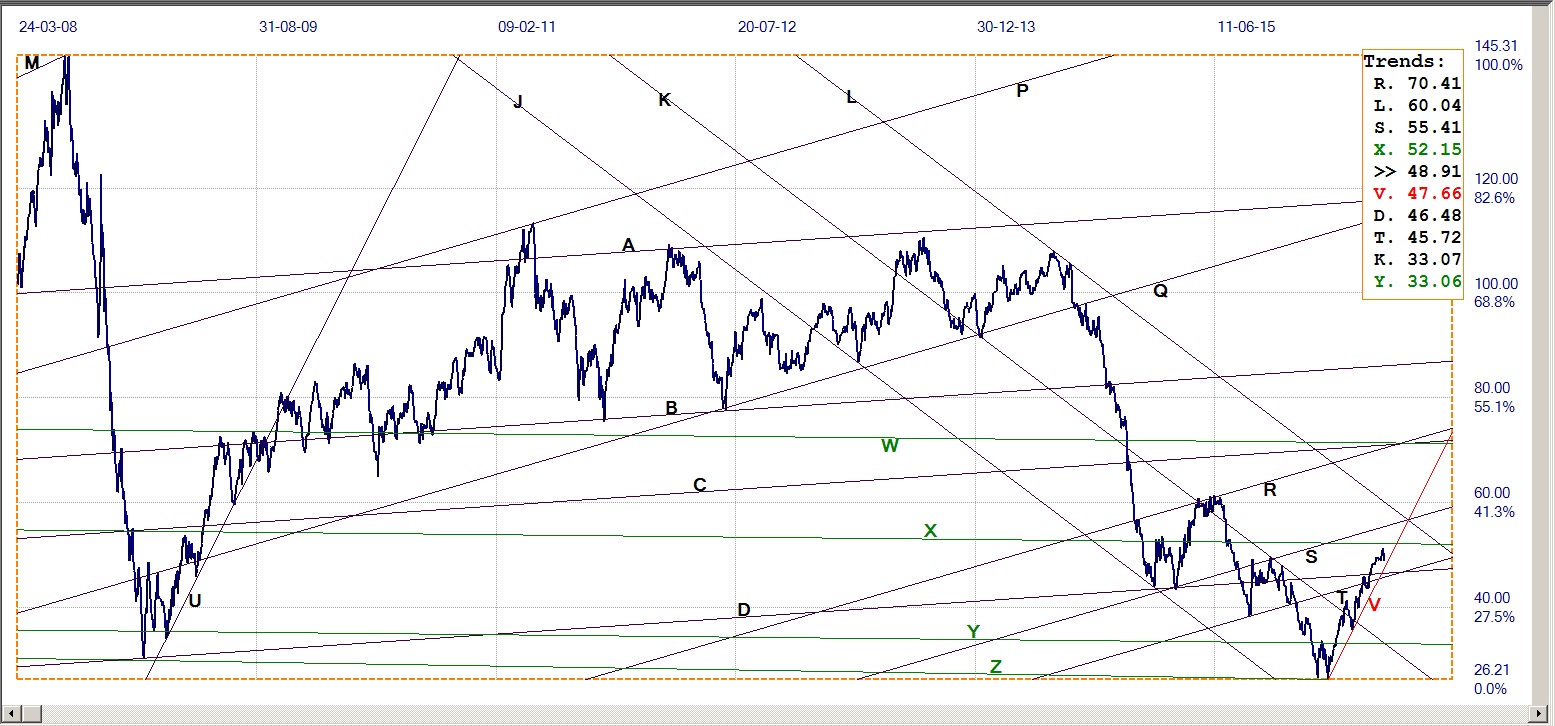

West Texas Intermediate Crude. Daily close

The new bull trend in WTI crude is still holding well clear of the steep support along line V ($47.66), but the value of line V is rising quite fast, while the move towards $50/bbl has slowed down and may have reversed – albeit this could be temporary.

As mentioned last week, the true state of the supply demand relationship remains murky and there are more rumours floating around than hard facts, so there is not much incentive to move the price in either direction. The as yet intact $50 – except on intra-day basis – is still acting as a psychological resistance and therefore the sideways trend should continue, holding below the $50 level until there is a clear reason for a new trend, either up or down, with a break to above line X ($52.15) or below line V to indicate the new trend.

WTI Crude – Daily close, last = $48.91 (Investing.com)

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com

share

share

share

share

share