Benefits Of Owning Precious Metals Vs The Derivatives

Many people ask me whether or not they should invest in gold stock indexes, or the GLD or SLV ETFs. They often point to the difficulty of securing physical precious metals versus the ease of purchasing the derivatives through an exchange. I am going to give some thoughts here, and focus on the costs of each investment option.

The GLD and SLV ETFs

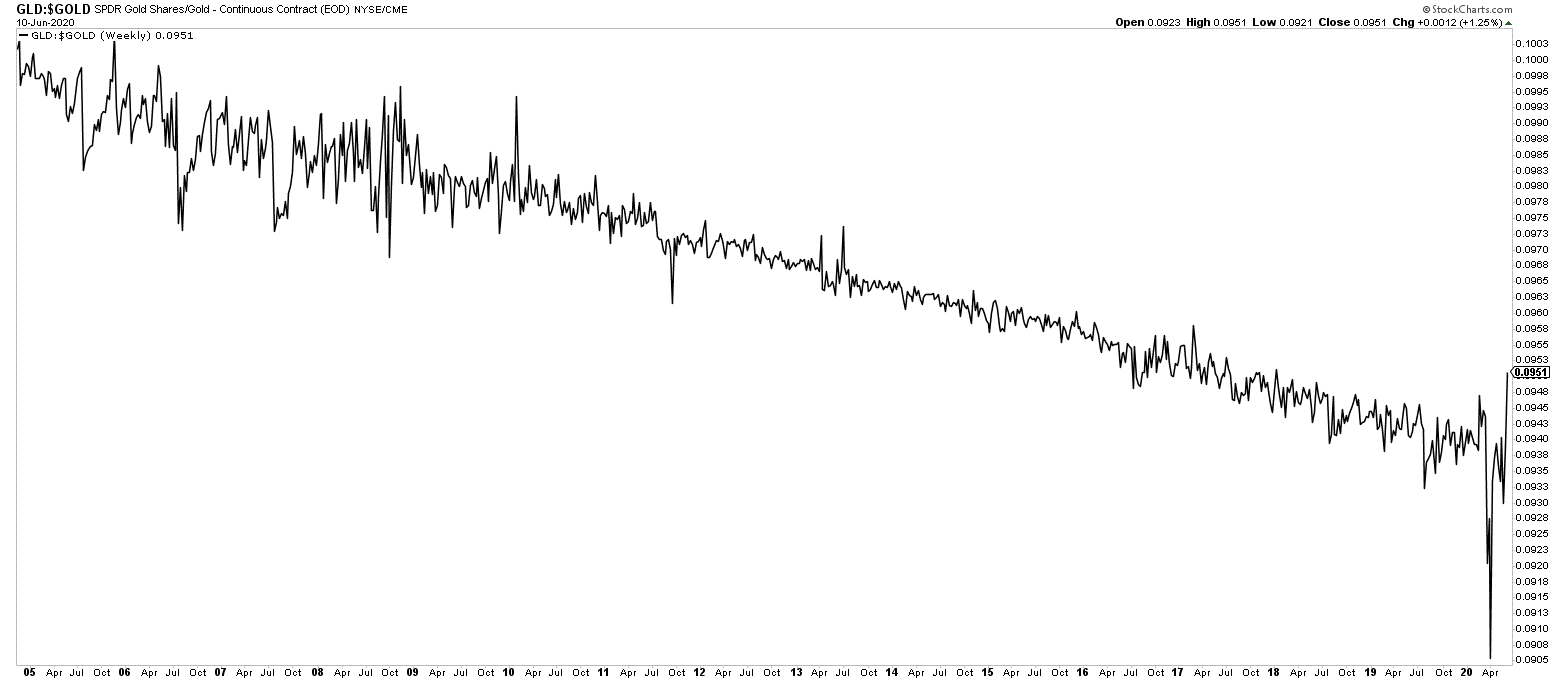

Here are some charts that show precious metals advantages over the derivative options. First, we will start with SPDR Gold Shares (GLD). Note – all charts courtesy of Stockcharts.com.

Just before I get into the chart analysis, I want to refrence a recent interview that I had with Nick Barisheff, CEO of BMG Group, discussing the numerous pitfalls of owning the GLD ETF. While I will not go over the title risks specific to that investment vehicle, you can refer to that article for a detail review of them.

We can see that when GLD is matched to the daily gold price, we see a descending trend line. Meaning, GLD has under-performed the physical gold price during that time span. While GLD may be easier to own, it comes with management fees that degrade its performance compared with gold. Further, there are no redemption rights in GLD for regular share owners; only the Authorized Participants may withdraw the metal. Therefore, there is no safety in owning a share of the GLD.

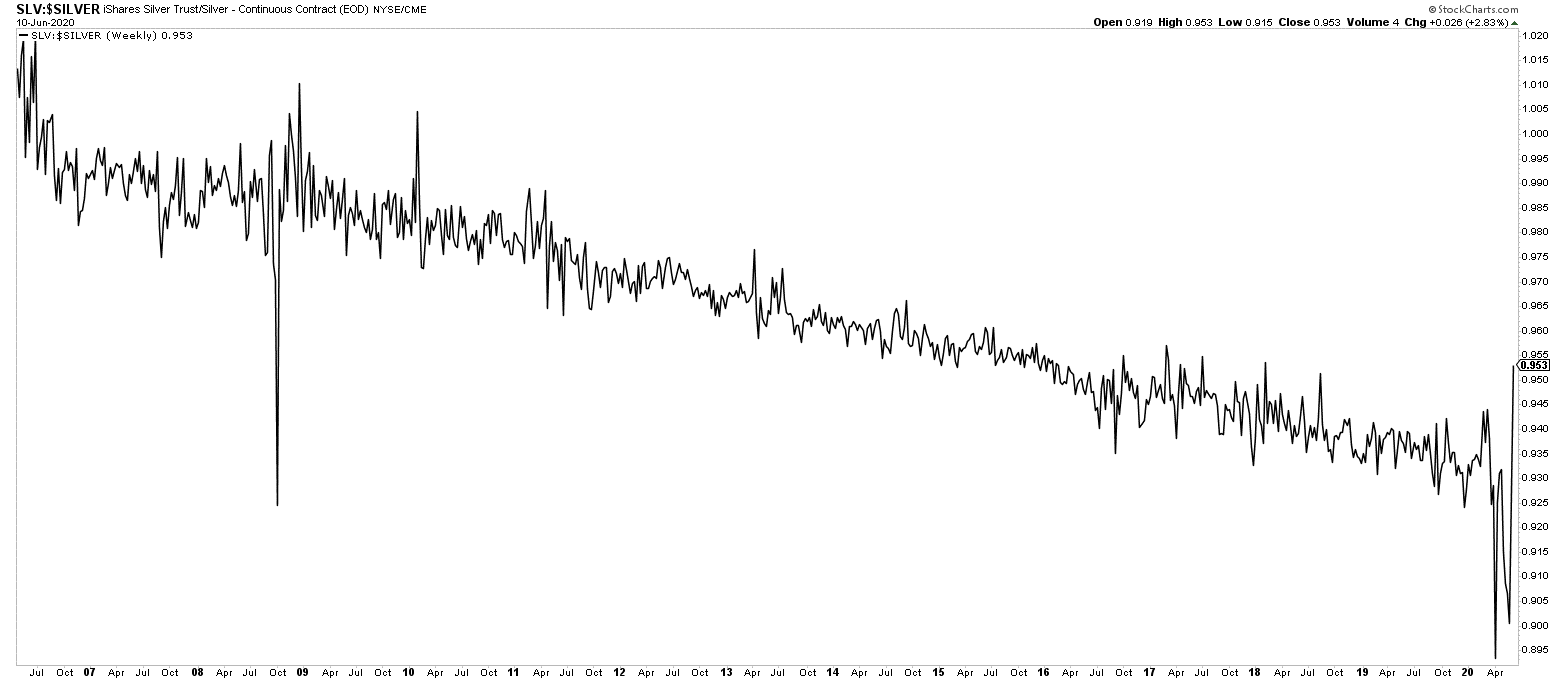

Next we look at the iSHARES Silver Trust (SLV) compared with silver’s performance.

We can see the same degradation of returns in SLV to silver, as we did in GLD to gold. These occur for the very same reasons as noted above for GLD, so no need to repeat those again.

Gold and Silver Stock ETFs

The second gold derivative I want to review are some of the more popular gold miners indexes. The main point to remember here are that while gold mining stocks may offer leveraged gains to the underlying metals price, the index funds are mixing in the best and some of the worst options in that space.

You are spreading your risk among several companies that you may not choose to invest in individually, after doing your research. Therefore, I encourage gold stock investors to do their due diligence in the space first, and pick companies that tend to outperform the space on a consistent basis. The starting factors that I recommend basing these decisions on are:

- Company Management

- Deposit Type and Quality

- Jurisdiction

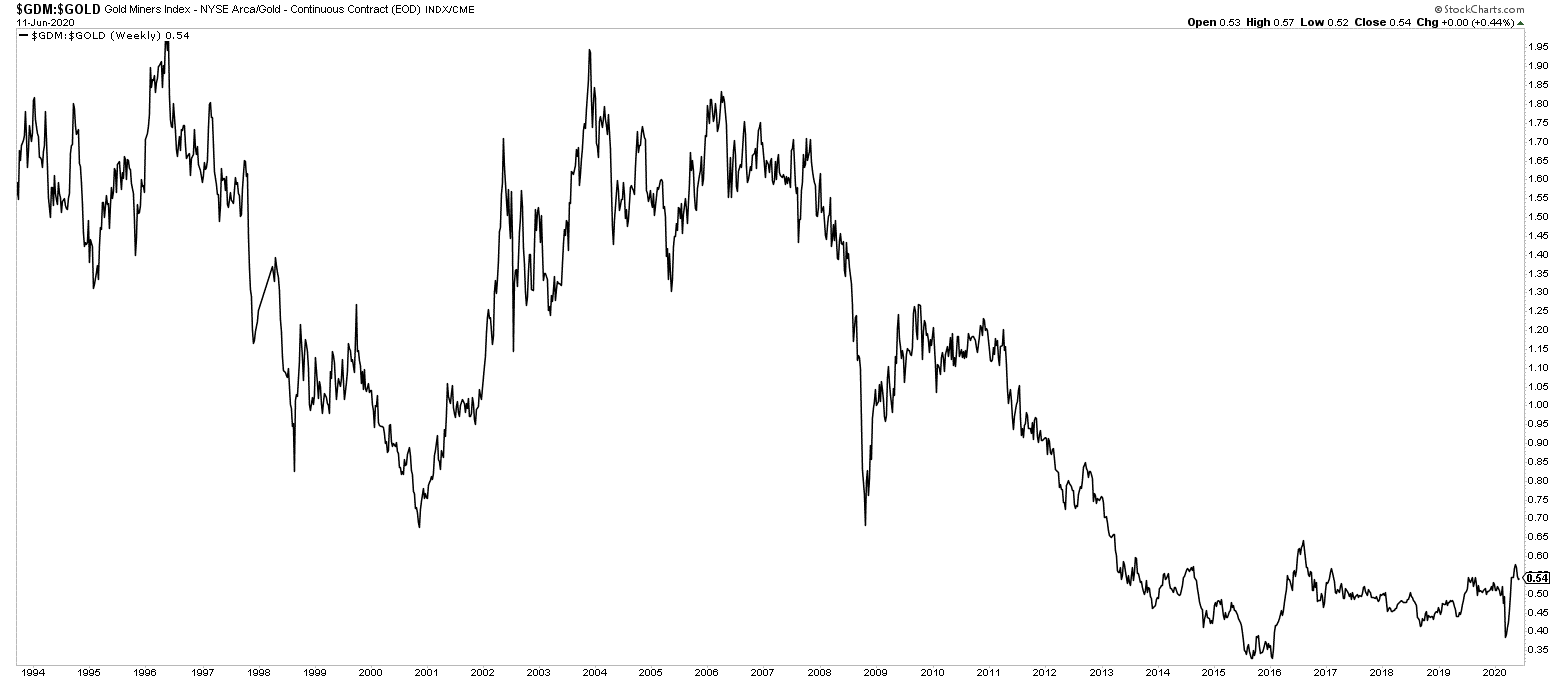

We start by looking at the NYSE Arca Gold Gold Minders Index (GDM).

What is interesting here is that the GDM started off promising originally, but generally followed the recessions downward in 2000 and again in 2008. However, this index has been downhill since 2011 when gold reached its peak of over $1900, and has not recovered at all compared with gold which is rebounding into the mid $1700 price range. This is a trend we will see with several of the stock indexes.

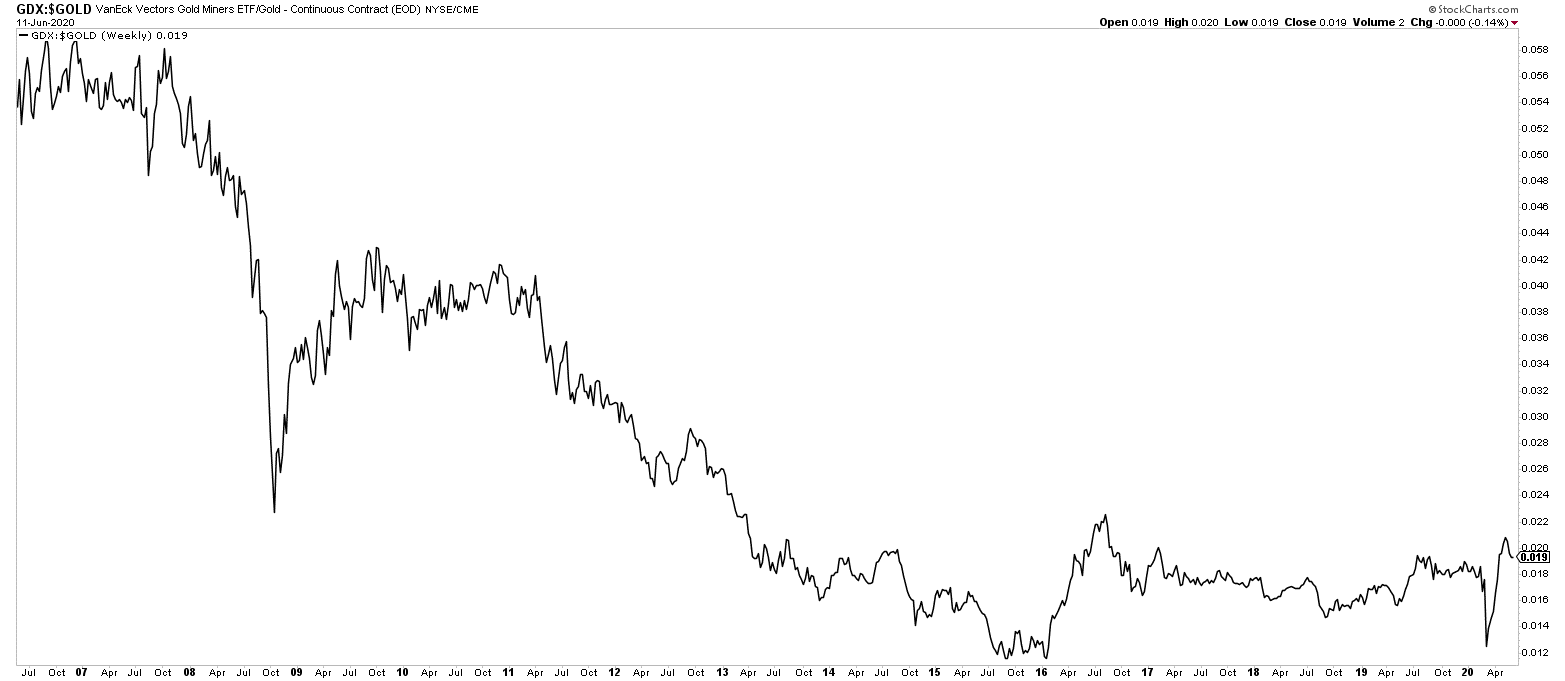

Next we examine the VanEck Vectors Gold Miners ETF (GDX) and notice that it has never recovered from gold’s fall in 2011 either, even though the gold price has rallied strongly from $1190 in late 2018 to its current price over $1700. Again, the index is not doing well.

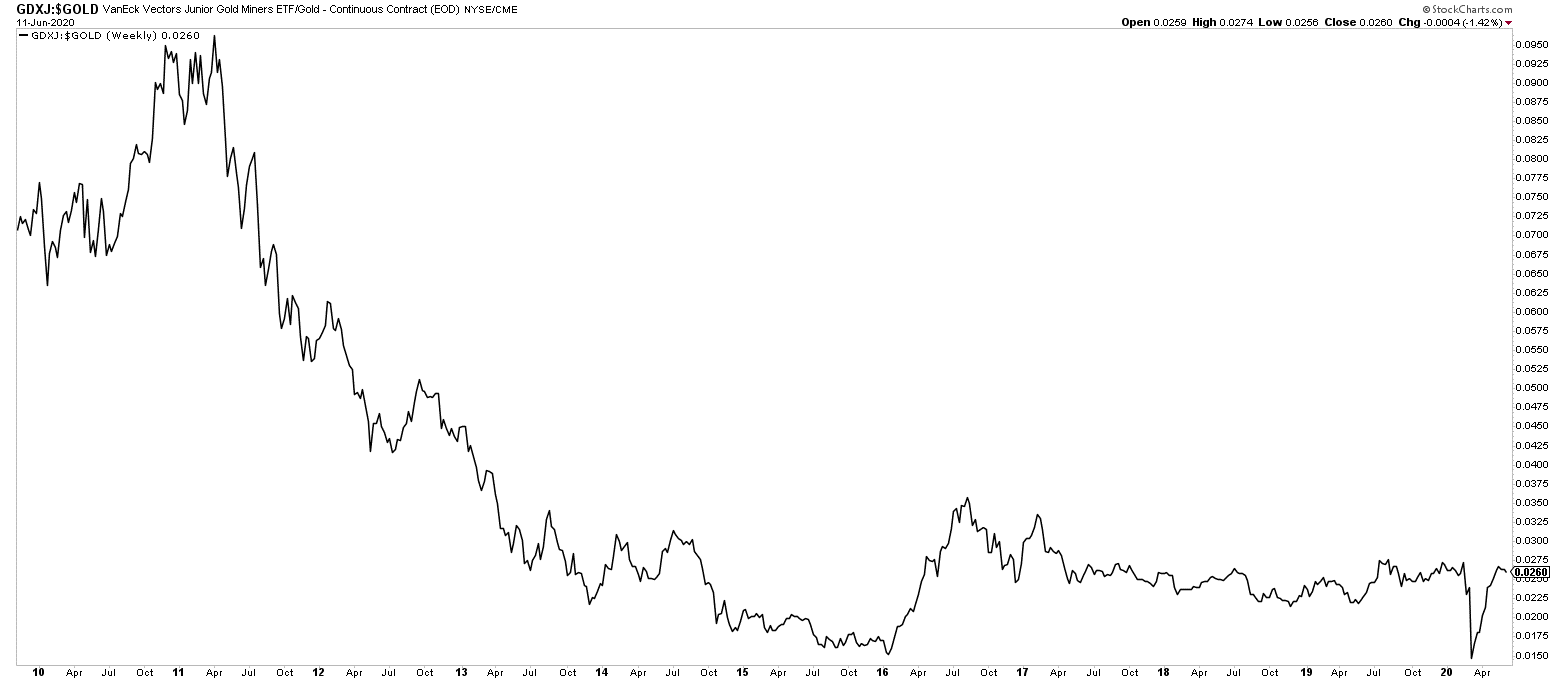

Looking at the VanEck Vectors Junior Gold Miners ETF (GDXJ), we see a bleaker picture than the gold majors.

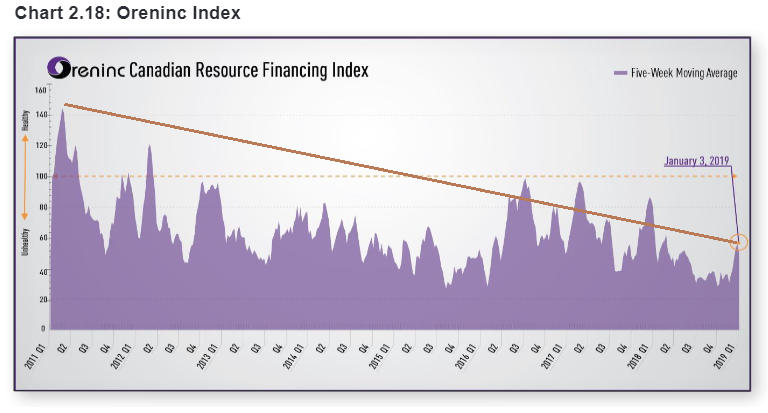

The performance of gold juniors has nearly fallen off the chart. This is also consistent with research that my friend Kai Hoffman of oreninc.com has done with respect to the junior minor financing space.

Notice the steady decline in junior mining resource financings in Canada closely mirrors the performance of the gold mine junior stocks since 2011. As money has not flowed back into the junior mining space, the junior gold minors have not had the money to finance exploration and development efforts, and as a result, their share prices have not recovered as a whole.

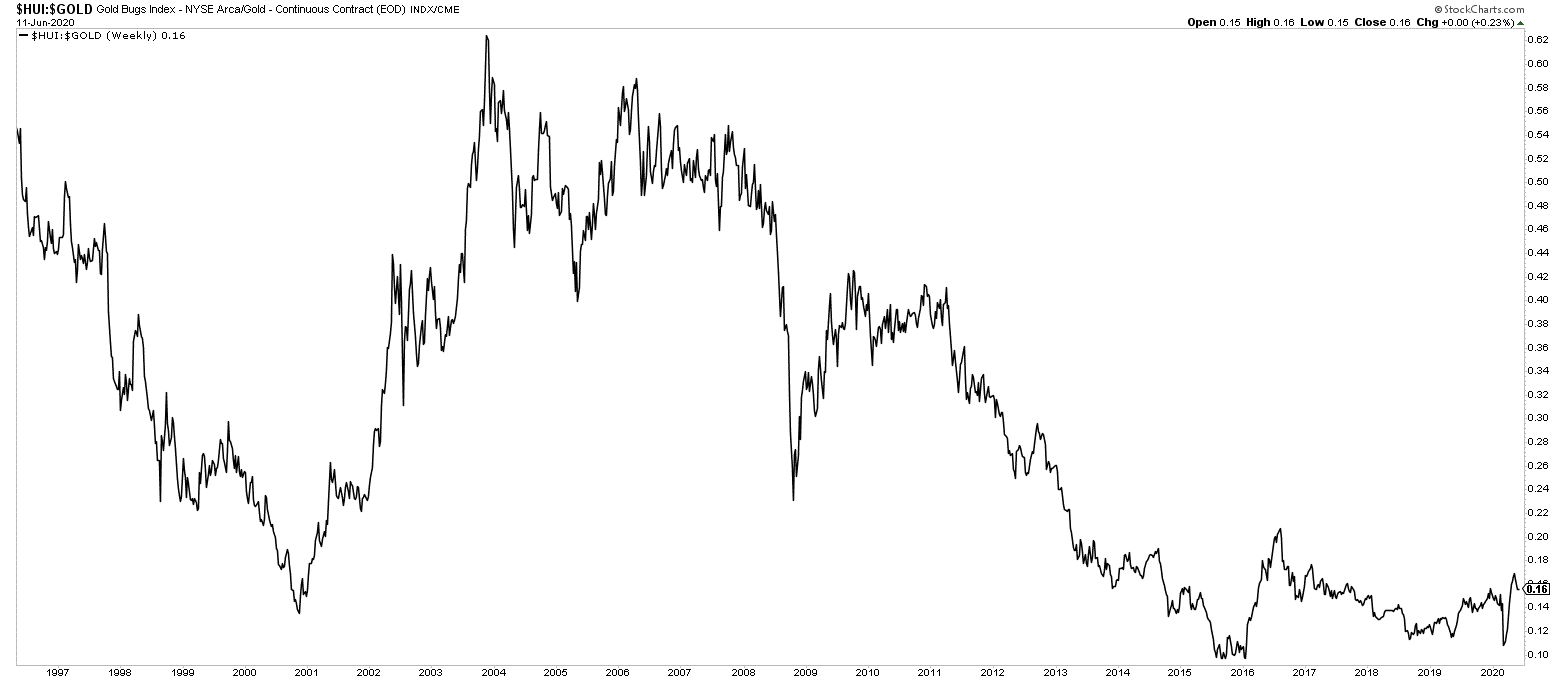

Next we look at the NYSE Arca Gold Bugs Index (HUI) and find a similar picture to the other major gold miner indexes.

The HUI dipped upon both of the last recessions, and since 2011, has not recovered. The index would be undervalued, many would argue. But the fact that this has gone on for nearly 10 years tells me that physical gold is considered more precious by the market than the gold miners, at least for the last decade.

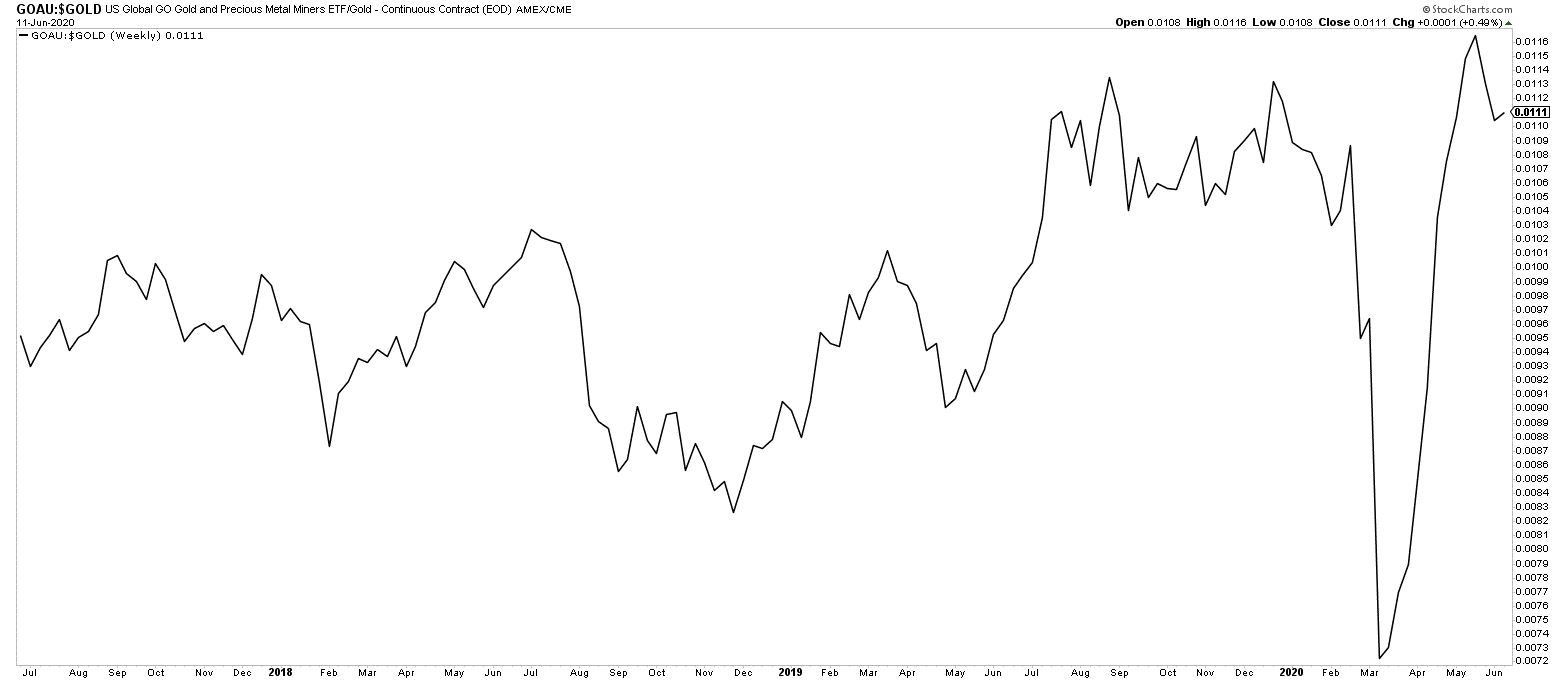

A relatively new entrant into the gold miner index is the US Global GO Gold and Precious Metals Minders ETF (GOAU). Its recent performance is respectable to gold; however, there is much less time data available to analyze on this one. Therefore, I cannot recommend it as a hedge against recession like I can physical gold until we see how it performs during the next economic pullback. Pay particular attention to the sharp drop in March of 2020, likely due to the COVID crisis. Likely, the drop can be attributed to fund managers and large retail investors selling shares to hedge risk elsewhere in their portfolio. That is not a particularly good sign with respect to the recession resistance of this fund.

One thing to note about the GOAU – it invests a lot of its money in gold streaming and royalty companies, so it could be more resilient to economic downturns. Getting its returns on production of the metals, regardless of cost pressures, means the fund is somewhat insulated from drastic changes in the cost structure of gold or the general short-term direction of the gold price. However, when gold companies cannot produce gold profitably, the returns on these companies tends to wane as they have less income.

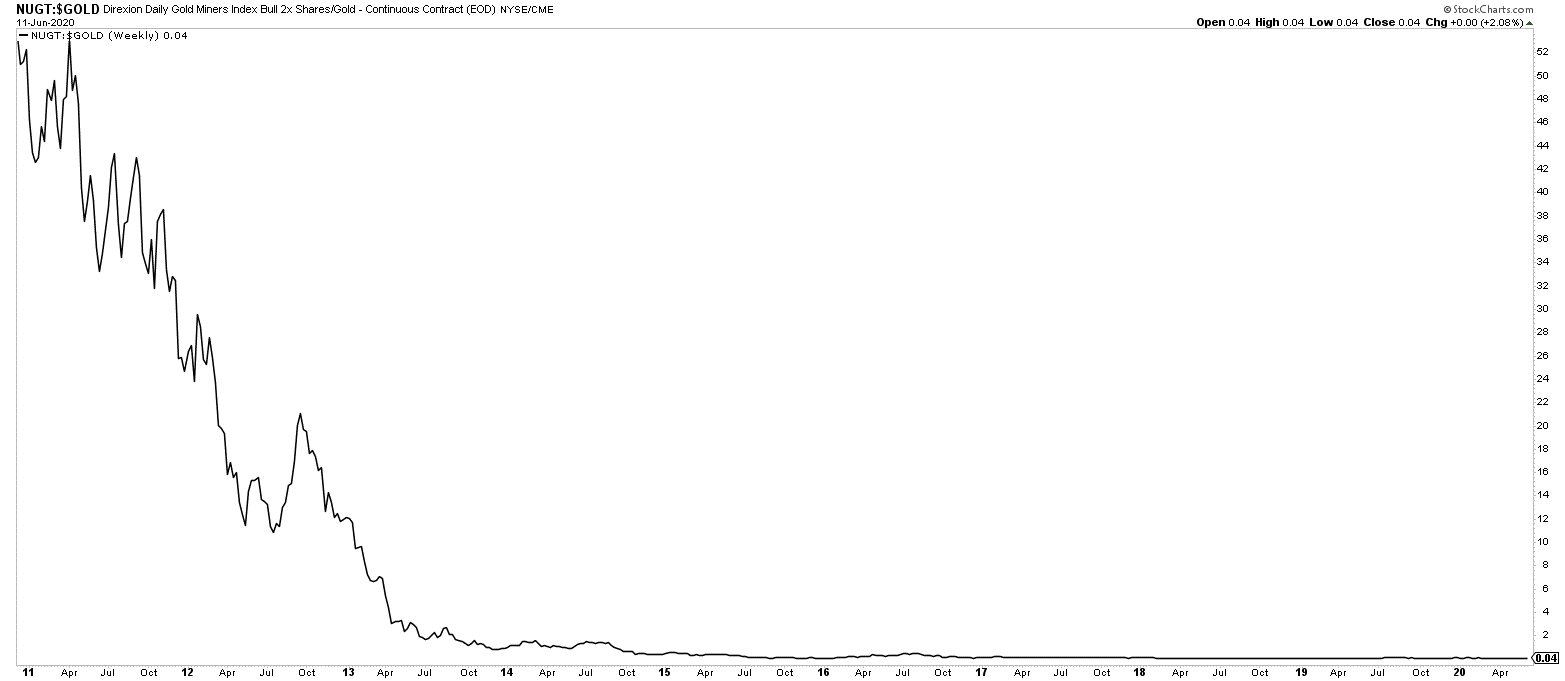

Let us take a look at a leveraged fund, the Direxion Daily Gold Minders Index 2X Shares (NUGT), which is 200% leveraged to the gold price movement.

Any takers on the NUGT when compared with physical gold? Note how after 2011, this fund never recovered even though gold’s price is well on its way. Translated, this means that leveraged indexes to gold prices don’t do any better. This is mainly because a 50% loss in value requires a 100% recovery to break even, and when you multiply that by 2x the effect, it gets ugly pretty fast. No thanks, I think I will pass!

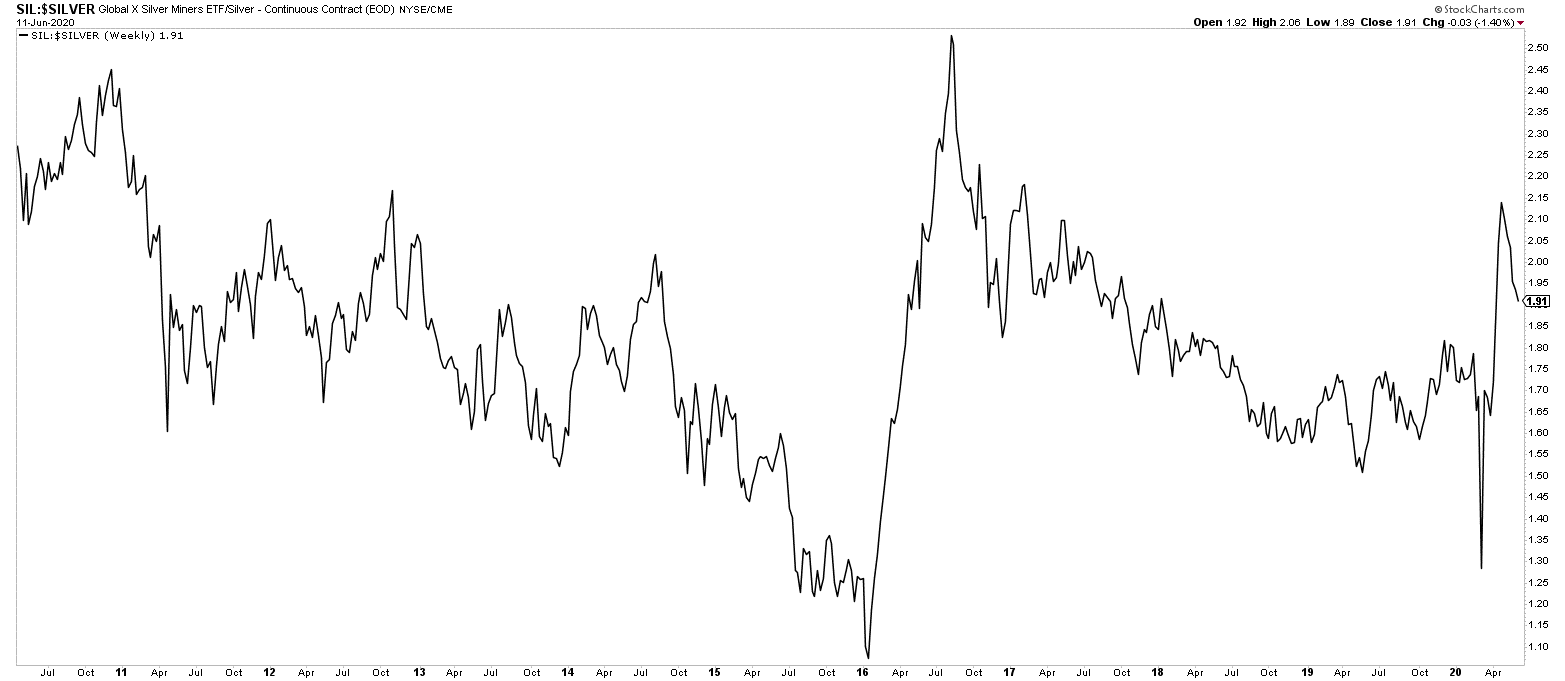

For the silver miner funds, lets first examine the Global X Silver Miners ETF (SIL).

In this case, we see somewhat decent performance in the ETF, though not as good as the silver price. Consider that there are some pretty good primary silver miners in a very small market of participants. This is why this particular ETF is not absolutely horrible.

But, also consider that primary silver miners have a hard time making a lot of profit because the market price of silver has been below its mining cost for the majority of the last ten years. Wake me when silver hits, and stays, above $20 an ounce. I think this chart gets much more interesting then.

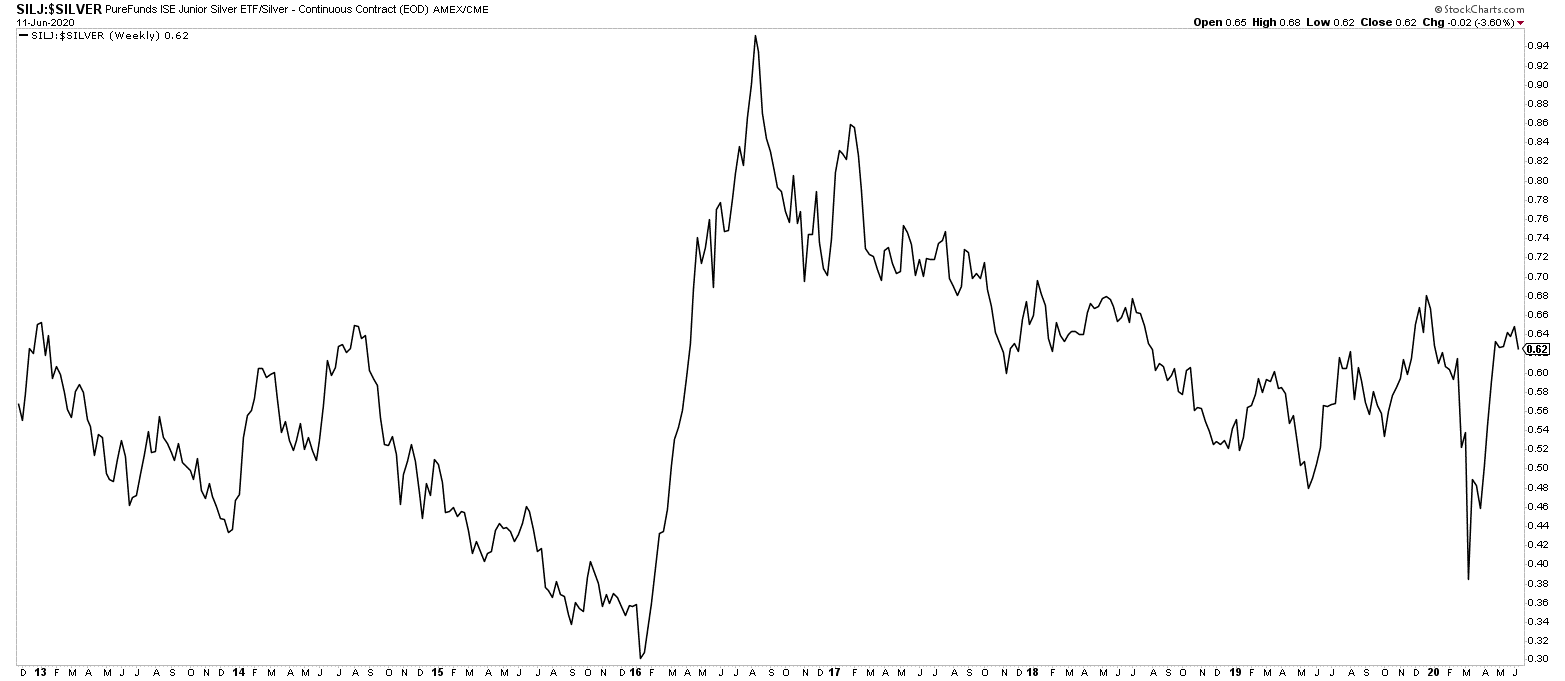

Lastly (but not leastly), we examine the Pure Funds ISE Junior Silver ETF (SILJ).

The $20 price of spot silver in 2016 caused an impressive bull run in this index. But it has been a slow drain from that point to now. I think this basically mimics the price of silver over that same time period. The silver juniors might also get very interesting over $20 an ounce silver, just like the majors. This is worth at least paying attention to, if for nothing other than leverage to a bull market in silver’s price.

Concluding Thoughts

Generally speaking, the physical precious metals tend to have better performance than the various derivative investments, whether stocks or the GLD and SLV. There are a few sort-of exceptions that involve short time frames or very specific niche areas of the precious metals derivative markets. However, over any length of time, owning the physical precious metals provides better returns, and therefore, security within your portfolio.

The risks of owning physical precious metals are reduced when storing them in a legitimate third party storage facility that has the following characteristics:

a) allocated storage (clear title to the owner)

b) regular audits

c) safe jurisdiction

d) insurance

e) low fees (common) compared with those charged by brokers to trade stocks and funds

*********

Robert has been analyzing the precious metals markets for over 10 years, and has built relationships with many experts in the field which include miners, geologists, and analysts. His is the founder/owner of Goldsilverpros.com which is dedicated to providing investors with professional research on the precious metals market. He is also the author of DropShadow: The Truth About the Economy. Robert has a Masters degree in Information Assurance & Security, a Bachelors in Business with an MIS concentration, and an Associates in Applied Sciences in Unix Administration and Cisco Networking.

More from Gold-Eagle