The Bottom In 10-Year Treasury Yield Signals A Change Of Era

Summary

-

The bear market for benchmark 10-year Treasury yield is at its end - disruption is coming

-

Numerous indicators corroborate: we are in the midst of an economic transition

-

Will the Powell Fed quickly evolve into a strong counter-balance to the powerful economic transition?

-

On an intraday basis, we explore these overarching themes overlaid on price behavior in my private investing community at MPtrader.com.

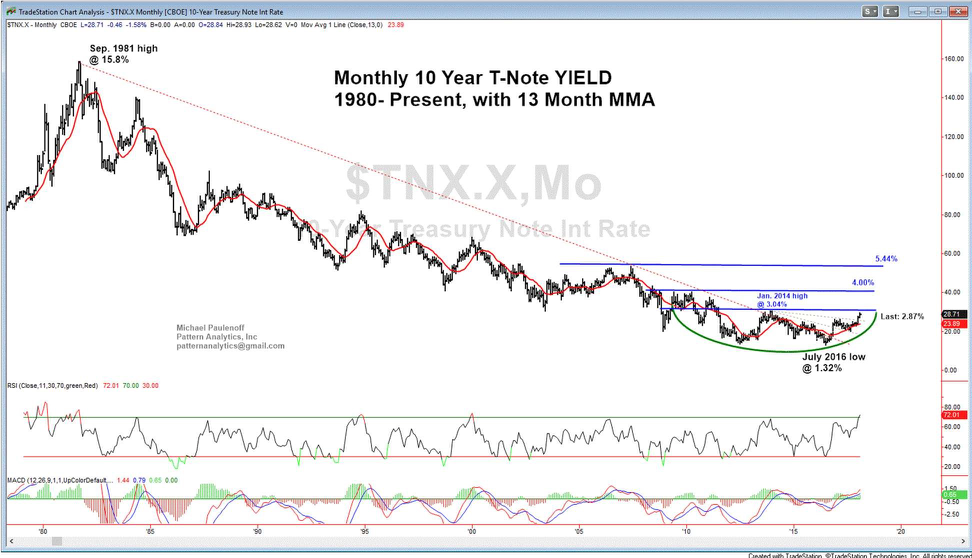

Take a close look at the monthly chart of benchmark 10-year US Treasury yield (Fig. 1) for the period 1981-2018, a 37year period. The dominant bear market for yield may still be alive but is not necessarily all that well.

A Powerful and Highly Disruptive Bull Market for Yield is Brewing

Consider this for a moment: all of the action in yield from around 2009 to present, a period of 9 years, exhibits the behavior and rounded base formation consistent with a technical bottom. The chart of the most recent years of the generational yield bear market should stop market-watchers, Fed-Watchers, investors, and traders in their tracks (see Fig. 1). A 9-year base in any market is potentially consequential. In the case of benchmark 10-year yield, it figures to be highly disruptive across all the major asset classes - equities, bonds, real estate, commodities, and forex.

The idea that 10-year yield could be in the midst of a maturing 2009-to-2018 base formation should raise eyebrows. The 2009 and 2018 years bookend a time of economic resuscitation during the Financial Crisis to a potentially highly stimulative fiscal "shock" layered on top of a well-healed, if not yet vibrant, recovered U.S. economy.

If particular economic trends and underlying conditions perpetuated the multi-decade bear phase in yield, then in theory, the bottoming phase is incubating the opposite-economic conditions and underlying trends that will have the potential to perpetuate a powerful yield bull market. That market is something that anyone under the age of 50 may not recognize or have experience navigating.

From my perspective, the economic conditions breeding within the maturing multi-year technical base formation in yield can be viewed as three distinct market currents: the "Bright Side" economic indicators, the "Dark Side" indicators, and the Efficacy of the Federal Reserve.

The Bright Side Indicators

First, the Bright Side Indicators. They are characterized by stronger economic growth and sharply climbing business sentiment:

-

Three percent GDP growth, and expectations of possibly 3.5% to 4.0% growth

-

Simulative impact, and the prolonged multiplier effect of corporate, personal tax cuts, and foreign capital repatriation (TCJA)

-

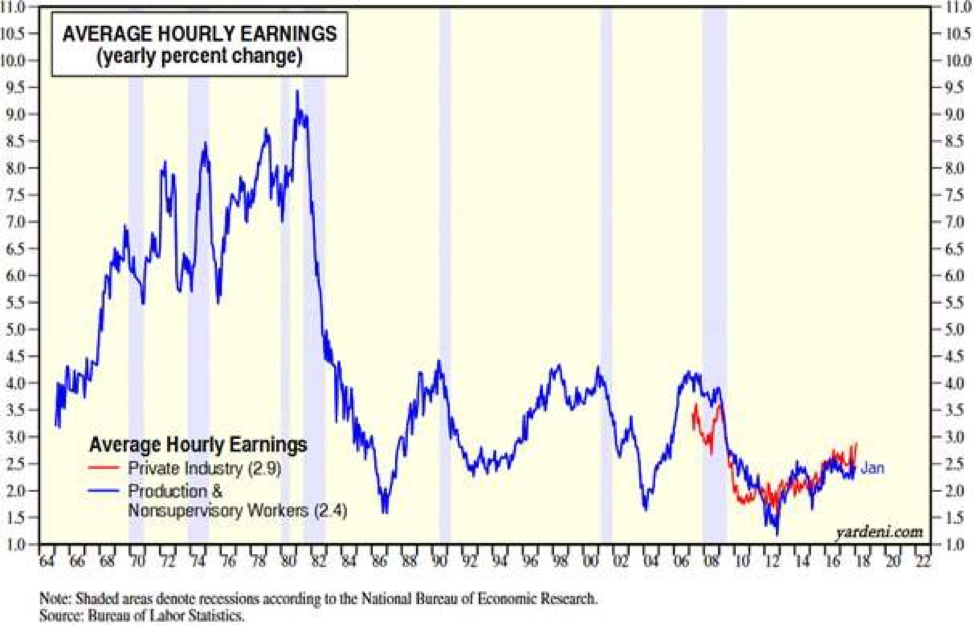

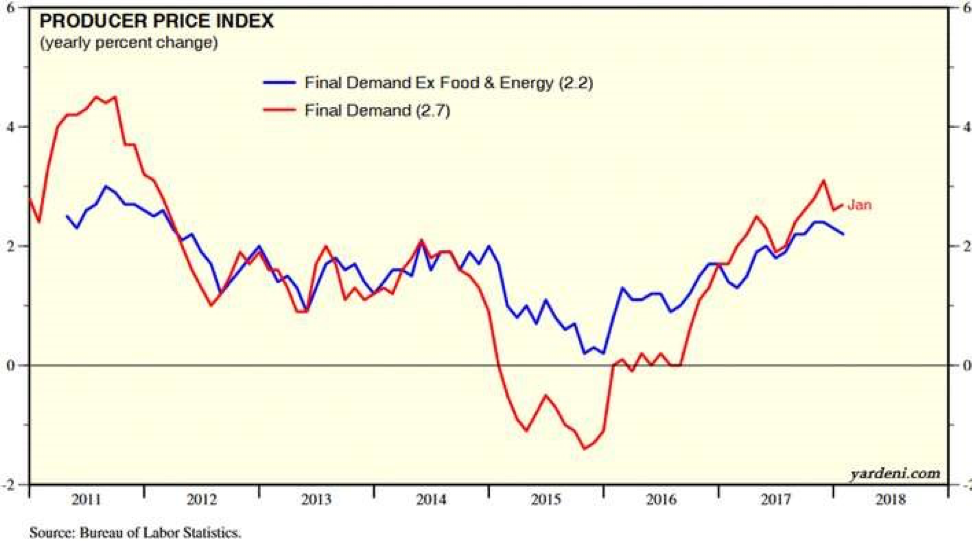

Upward price pressure from average hourly earnings and from some year-over-year price index measures such as CPI and PPI that are elevating expectations of inflation after a multi-decade absence (Fig. 2, Fig. 3)

-

Historically low Unemployment and Jobless Claims, starting to stabilize and lift wages (Fig. 4)

-

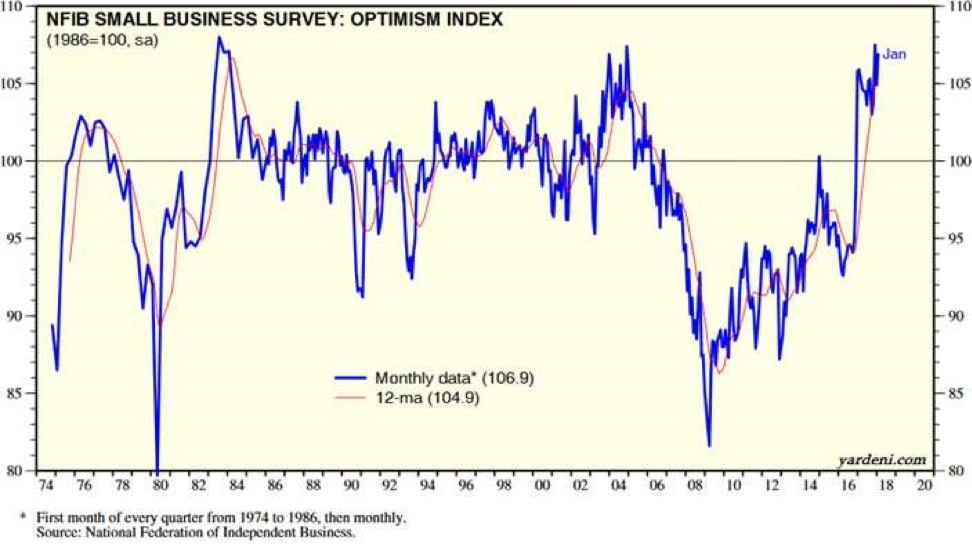

Soaring small business confidence (Fig. 5)

-

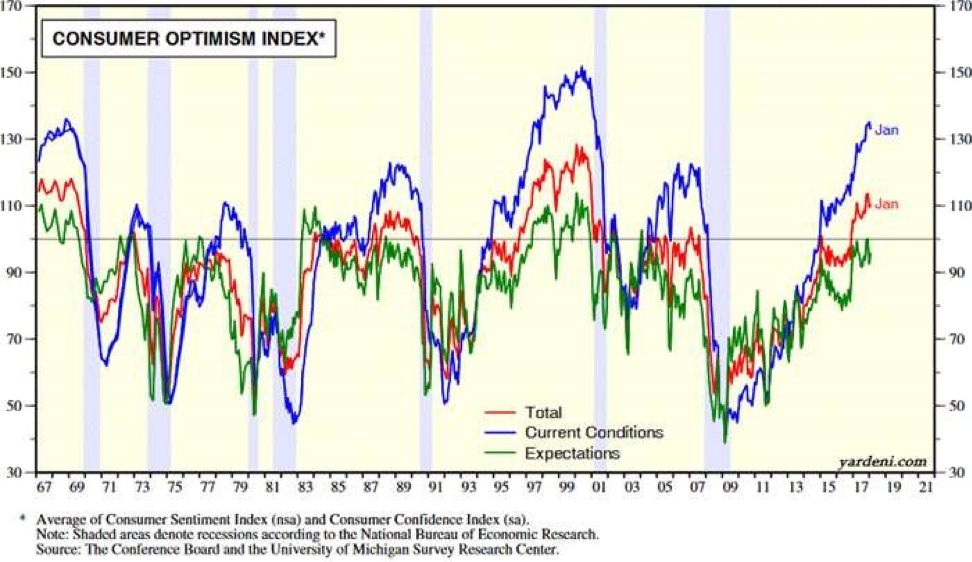

Historic levels of consumer confidence (Fig. 6)

-

Historically strong corporate earnings and a surging equity bull market (Fig. 7, Fig. 8)

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

The list above is not exhaustive, but it provides the sense of improvement and upward momentum in some high-profile data and indicators. These were MIA during the post-crisis years of healing, years characterized by mediocre, economic performance. During the past several months, however, these "Bright Side" Indicators are increasing concern among bond holders and buyers.

The Dark Side Indicators

By contrast, there are other indicators that I label the Dark Side Indicators. They are characterized by their perceived negative bond market "karma" - their potential to undermine, destroy, and erode bond market psychology. Again, this is hardly an exhaustive list:

-

Government (deficit) spending (budget and infrastructure)

-

Huge cumulative, ballooning Federal Debt (Fig. 9)

-

Federal Reserve efforts to reduce its $4 trillion balance sheet by $300 billion in FY 2018 and by $600 billion in FY 2019 that will require larger Treasury auctions (greater supply), and will put increasing downward pressure on bond prices (upward pressure on rates) (Fig. 10)

-

A weakening US Dollar that could be putting in a huge, multi-decade top, consistent with reduction of returns on foreign purchases of US Treasury paper, and which could diminish confidence in the efficacy of the US monetary policy (Fig. 11)

-

Curtailment of foreign buying of US Treasuries

Figure 9

Figure 10

Figure 11

Both the Bright Side and Dark Side Indicators support intensifying upward interest rate pressures, and both sets of indicators are gaining momentum now, which creates conditions that can only be described as a "a Double Whammy" heading in the direction of the Federal Reserve, the keeper of a still historically and abnormally low Fed funds rate at 1.50%.

The Efficacy of the Federal Reserve

Until relatively recently, Nov. 9, 2016 to be precise-the day after the presidential election-Federal Reserve monetary policy represented the only economic "growth engine" from 2009 through 2017. During the immediate post-crisis years, novel and very aggressive Bernanke-Fed (Feb. 2006 to Jan. 2014) experimental monetary policy prescriptions (Quantitative Easing) put the brakes on the acute contraction in business activity and consumer confidence, which enabled the US economy to begin to heal. Thereafter, the extension of super-easy, crisis-level monetary policies supported (stimulated?) only 1% to 2% economic growth, with the lion's share of capital flows seeking the perceived relative safety offered by US equities (Fig. 12), rather than riskier avenues of business expansion and CAPEX. Fiscal policy was nowhere to be found. Political discord and bipartisan dysfunction on Capitol Hill precluded any serious discussion of fiscal remedies, much less actual bipartisan policy prescriptions for a stagnant economy.

Figure 12

Although the Yellen Fed (Feb. 2014 to Jan. 2018) officially ended QE in October 2017, earlier she had begun the process of "normalizing" Fed funds from its crisis-era ZIRP (Zero Interest Rate Policy) or NIRP (Near Zero Interest Rate Policy) with five 25 bps rate hikes between December 2015 and December 2017, elevating Fed funds to 1.50%, where it currently resides (Fig. 13).

Figure 13

But, all that was about to change dramatically.

During 2017, the status quo in Washington, D.C., on the fiscal side of the equation, was in the early stages of undergoing an earth-shaking change in perception that ultimately will present challenges for the incoming new Fed Chair, Jerome Powell.

Yellen's final Fed funds rate hike occurred on December 13, 2017. It was the third 25 bps hike of 2017, during a 12-month timeframe after the election of a new, pro-growth president, Republican Donald Trump, along with a Republican majority in both houses of Congress. On December 20, 2017, one week after Yellen's final rate hike (1.25% to 1.50%), and four weeks prior to the confirmation of a new Fed Chairman, Jerome Powell, the Republican Congress passed historic, and potentially very stimulative, tax reform legislation (the Tax Cut and Jobs Act, TCJA). It was an accomplishment for the new government that matched its pro-growth talk with actual legislative action.

Indeed, from the time Trump took office in Jan. 2017 through February 2018, the Trump Administration has overtly and consistently enacted pro-business policy-the likes of which have not been seen since before 2007 certainly and arguably since the early 1980's.

With the above observations in mind, let's take a quick look at some coincident recent events, and overlay them onto my weekly chart of 10-year yield (Fig. 14):

-

Jan. 21, 2017-present - Trump rolls back hundreds of Obama-era anti-business regulations Nov. 2, 2017 - Trump nominates Jerome Powell as new Fed Chairman

-

Dec. 13, 2017 - Yellen hikes rates 25 bps to 1.50% from 1.25%

-

Dec. 20, 2017 - Congress passes new corporate and personal tax reform law (TCJA)

-

Jan. 23, 2018 - Jerome Powell confirmed as new Fed Chairman

-

Feb. 5, 2018 - Jerome Powell's first day as new Fed Chairman

-

Feb. 9, 2018 - Congress passes new budget-busting spending bill

-

Feb. 27, 2018 - Jerome Powell provides House testimony in the Fed's semiannual Monetary Policy Report

Figure 14

Within a very brief period, underlying economic conditions and expectations have changed dramatically for the incoming Fed Chairman. Fiscal Policy is back with a vengeance and the bond market appears to be quite aware of the change.

From the time Powell was nominated in early November 2017, into his first day at the helm of the Fed on Feb. 5, 2018, and through the passage of the new budget and spending bill on Feb. 9th, yield on the benchmark 10-year Treasury bond climbed from 2.38% to 2.80%, or +18%. From the time Donald Trump was elected president, 10-year yield has climbed from 1.86% to 2.94%, or +58% (Fig. 13), while 2-year Treasury yield (Fig. 15) has climbed to 2.25% from 1.00% since November 2016.

Ten-year yield has not been this high since August 2008-perhaps in anticipation of forthcoming market "reprioritization" of the potential impact of fiscal policy from years of monetary policy dominance?

Figure 15

As the new Fed Chair heads to Capitol Hill on February 27th for his first Humphrey-Hawkins testimony, 10-year yield is 2.87%. That is slightly off of its recent high at 2.94%, but perched atop a major upside breakout. It is accompanied by the introduction of powerful fiscal policy prescriptions, stimulating the heretofore dormant animal spirits of a decade-long stagnant economy.

Unlike his predecessors, who did not have to worry about the influence of intense fiscal stimulus on Fed monetary policy, Chair Powell has the unenviable task of attempting to forecast the economic and inflationary impact of lower personal and corporate taxes, in addition to trillions of dollars of repatriated capital, ballooning federal deficits, and rapidly rising, unwieldy federal and personal debt, all in an economy that appears to be entering a condition of escape velocity, metaphorically speaking. Accurate forecasting and modeling have never been the strongest suit of the academic overseers of our economic wellbeing.

From my perspective, the hyper-stimulative fiscal policies of the singularly, business-fixated Trump Administration are a paramount challenge to our post-financial crisis, gradualist, status quo Federal Reserve. The behavior of Treasury yields, especially since Q4, 2017, is telling us just that. Is a 1.5% Fed funds rate restrictive enough to thwart potentially powerfully rising economic and business inertia unleashed during the past year?

All that needs to happen now is for one economic indicator to blow up for holders of US Treasury paper to yell "fire" in a crowded theater, and to demand considerably more risk premium going forward. How will the Powell Fed handle such a challenge? Will he wait and see, or aggressively micro-manage the situation? My instincts tell me that he was nominated precisely because he is even-keeled and deliberate, usually wonderful qualities to have as a Fed Chairman.

However, the multi-year base patterns that have developed after a multi-decade yield bear market, exhibited across various maturities along the yield curve, suggest that the new Fed Chairman will need to be more like Ben Bernanke's 180 degrees mirror image. He will have to be spontaneously adept at handling "sudden acute growth or inflation syndrome," rather than depression-prevention crisis management.

Let's fasten our seatbelts for an eventful, rollercoaster ride in the financial markets during the upcoming months.

To be continued…

*** Charts labeled Fig. 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12 reprinted with permission from Ed Yardeni, Yardeni Research Inc., yardeni.com

*********

Mike Paulenoff is a veteran technical strategist and financial author, and host of MPTrader.com, a live trading room of his market analysis and stock trading alerts. Sign Up for a Free 15-Day Trial to Mike's Live Trading Room!