The Case For Gold…Gold History In Point Form

There are readers here who might be too young to be aware of the history of gold and what that means for the future of the price of gold, and of course, of silver. The story of gold is however much more convoluted than that of silver. The latter has the effort of the Hunt brothers to corner the silver market as its main point of interest and not too much else, even though silver could have become the primary focus of the current price suppression of the precious metals. This is all about gold, the monetary metal.

There are readers here who might be too young to be aware of the history of gold and what that means for the future of the price of gold, and of course, of silver. The story of gold is however much more convoluted than that of silver. The latter has the effort of the Hunt brothers to corner the silver market as its main point of interest and not too much else, even though silver could have become the primary focus of the current price suppression of the precious metals. This is all about gold, the monetary metal.

In February 1996 the price of gold broke a major chart pattern in the wrong direction: after the break higher and also above $400/oz, it reversed direction and started off on a bear market. In terms of fundamentals at that time, it was the wrong direction and therefore not anticipated. This paradox triggered an extended study of the operation of the gold market that soon brought realisation that the market was being influenced by external forces, probably to support the US dollar. I have been a long-term bull for gold ever since then.

Rather than an extended write up of the history, point format is used for most of the content to keep the document to a reasonable size.

The Early Years

- Prior to WWII, currencies as a rule were linked directly to the price of gold. The notes (paper money) of that time typically contained text similar to this: “I (the president of the local reserve bank) promise to pay the bearer xx amount of gold on presentation of this note at (the central bank)”. Gold was the only real money and paper notes were just that – a promise to pay

- During WWII a meeting was held at Bretton Woods in the US during which it was decided that after the war the dollar would be the only currency directly linked to gold, at a price of $35/oz. All other currencies would be pegged to the US dollar and only indirectly linked to gold. However, the change still meant all currencies effectively remained on a gold standard, even if only indirectly through their peg against the US dollar. When a country’s trade balances fluctuated badly enough, its currency had to be revalued, or more often, devalued, against the dollar and, therefore, against all other currencies as well

- After the war the US owned the majority of all official gold; other countries that over time had a trade surplus with the US could exchange their excess dollars for gold at the official $35/oz price. When European countries were rebuilt after the war and traded with the US they, France in particular under Gen. de Gaulle, used this opportunity to its full effect to obtain an own gold reserve

- In the mid 1960s the cost of the Vietnam War and President Johnson’s effort to eliminate poverty in the US, his ‘Great Society’ plan, caused the money presses to work over-time. Even though inflation was low, a dollar peg at the fixed price of $35/oz meant that by that time gold was becoming cheap and more and more US gold was leaving the US for Europe, much of it to France, not to return

- Much needed support for the dollar to reduce the outflow of US gold was then arranged by the Bank of England; a syndicate known as the ‘London Gold Pool’, was formed with the purpose of buying gold in large quantities to keep the dollar peg intact. By the late 1960s it was clear their effort could not succeed and by 1971 President Nixon took the dollar off the gold standard. Currencies started to float against the dollar and each other, while the official price of gold was raised to about $42/oz. The free price of gold had started to move steeply higher, as it responded to the normally market forces of supply and demand

- Rampant inflation in the US during the 1970s sent the price of gold much higher. After hitting a peak of $850 in 1981, President Reagan’s major remake of the US economy had inflation falling steeply and therefore also the price of gold, which later settled for some years in a sideways band below $400/oz

- After his election in 1992, President Clinton introduced various plans to boost the economy out of the recession which had kept the GWH Bush presidency to just one term. These plans included a loose monetary policy and increased printing of money; as a result, by early 1996 the price of gold had broken higher, clear of the $400 barrier. This break higher came out of a large triangular pattern that traditionally signaled the start of a strong bull market. When the price suddenly reversed direction to fall clear below $400 and also the triangle, this unexpected behaviour grabbed my interest to begin a study of the gold market

The Gold Carry

A ‘carry’ in the trading sense is when one commodity is borrowed and sold so that the money can be invested in something else that provides a higher return than the cost of the borrowing. The new suppression of the gold price commenced in the mid-1990s as the Bullion Banks – those big New York banks active in the gold market – borrowed gold from central banks at near 0.5% interest (because of the very low risk that the gold would not be returned) and sold it to invest in US long bonds that at the time paid above 7%. Where the old ‘Gold Pool’ was common knowledge, this new effort was kept quiet and covert.

- This was such an easy trade to do that banks practically queued up to take part in the ‘gold carry’. The result was too much supply coming into the market, and the price fell steeply and consistently. This was the real objective of the central banks in their eagerness to lease out gold as a covert plan to support the dollar against the price of gold – the true barometer of what a currency is worth

- One potential problem with the gold carry that apparently was not of concern at the time, was that when the banks were due to return the leased gold, they may not be able to do so. It was perhaps assumed that the leased gold would remain in vaults somewhere and could be purchased by the banks again at a lower price than at which they had borrowed, to make a capital profit as well. After all, they had borrowed close to $400/oz and their selling was causing the price to fall; if they could buy back gold at say $350, or lower, they would make massive profit over and above the profit from the carry

- As it happened, too much of the gold sold in this way ended up around the necks and arms of women all over the world, especially in India – where gold jewelry is wealth and is not traded or sold except in emergency. In addition to the problem of possible lack of supply, during this orchestrated bear market in gold various global events triggered a sudden rush to the traditional safe haven – gold – and the gold price jumped. When this happened, central banks acted in panic, first to an Asian financial crisis and shortly thereafter to the default on foreign loans by Russia. They employed two desperate means to keep the lid on gold when it turned so bullish in response to these events:

- The central bank of Switzerland, out of the blue, announced they would sell half of their 3600 tonne stash of gold ‘for humanitarian’ reasons. The announcement consisted of only two sentences; when asked, the Bank said the details were not as yet finalised and would be announced later! Strange behaviour from the normally so conservative and precise Swiss?

- The Bank of England (their central bank) announced they would sell half of their store of gold by a series of auctions. The way these auctions were conducted is most weird. The lowest bid price that would clear the gold on auction was to be applied to every bidder that had bid at a higher price – almost as if it was the full intent of the auction to keep the market price of gold as low as possible!!

- All of this brought the gold price to $250 by about 2000, when a new problem arose; mines started to reduce production, or even close, because the gold price was below the cost of production – as has just recently happened again. This imminent reduction of supply into the market – at the same time as increased safe haven buying ahead of, firstly, the 2000 century change and then also after the 9/11 event – caused the gold price to begin a recovery.

The Comex Years

- Because rates were so low that the gold carry was no longer profitable enough for the degree of risk and the price now clearly had more bullish potential than bearish, the banks were careful of borrowing and selling gold to keep the price low. This meant another means to do so had to be found. This method worked well in the rising trend of the price and has been in use for the past 15-16 years

- For more than a hundred years now, the price of gold is set in London by some member banks of the ‘London Bullion Market Association (LBMA)’. These banks have a close link with the NY bullion banks and some are even the same. While the London Gold Pool had to fail because the supply of gold they could get to sell was limited, the Comex metals futures market has no supply problem – they are a market for trading in ‘paper gold’ and the supply is almost unlimited by design

- As gold started what became its longer term bull market in 2002, the Bullion Banks (BBs) would sell futures contracts in volume, going short of the market. At a suitable point and with good timing in terms of outside events, they would suddenly sell a very large number of contracts in a few days, forcing down the price. Buyers, still remembering the previous 5-year steep bear market, would panic and run away and holders of long positions would close their positions as soon as possible, even if it meant a loss. At a suitably low price, the BBs would begin to buy and close their short positions at a very good profit

- For many years, these regular bear raids by the BBs were major affairs, typically many months apart. The gold price often would fall more than $150-200 and it would take some months before buyers returned to the market. The resulting interruption of the bull trend suited the central banks, while the opportunity for almost risk-free profit was all the BBs wanted. This method of keeping the price of gold under some control would work as long as there was physical gold to sell for buyers who really wanted the metal

- However, by September/October 2011, with the gold price nearing $2000, the gold bulls were winning the long drawn out battle. At that time the BBs struck; a major and sustained period of selling many contracts almost daily, had the gold price trending steeply lower – to be followed by two years of volatile swings and, again, the development of a large sideways triangle. As the price completed leg 4 of the triangle, ready to begin leg 5 and then break higher above the triangle, another bout of heavy selling of paper contracts in April 2013 caused the price to collapse below the triangle in a déjà vu event! It is reported that the equivalent of well over 200 tons of actual gold was sold over a weekend in April when the markets were almost deserted and the selling then continued into Monday as the shell-shocked gold bulls threw their long positions away at any price. Of course, this sell-off helped the BBs to coin money hand over fist

- During the next two months, the gold price fell in staggered fashion from $1577 down to $1192, dragging in new bulls whenever they saw the selling was halted in the hope a bottom had been reached; only to be knocked out when the heavy selling started again to add even more to BB profits

- The past three years since the steep fall have seen a slowly descending but still quite volatile bear trend. Any bulls that tried to get back into the market, were soon stomped out again by what has now become known as ‘waterfall attacks’. Rather than one long lasting attack on the price, as used to be the norm prior to the 2011 high, it seems that the BBs decided more efficient use of ever declining gold reserves could be made by intense selling of paper contracts over a span of only a few minutes, resulting in what is also known as a ‘flash crash’

- The war on gold in the paper market could only work as long as enough gold was on hand to satisfy a relatively small physical demand mainly from investors and jewelers. During 2015 gold bulls were becoming more confident that with China and India buying gold that on some occasions exceeded annual production, the paper war soon would not have enough of the actual metal to support it. Once a demand for gold cannot be satisfied at the artificially low paper price, buyers will raise their bids to obtain gold. As this happens more and more, the gold price soon will be set in a physical market, not by the Comex paper market, as has been happening for decades and that would mean the end of the war

- In April of this year, China opened a gold and silver exchange in Shanghai where the trade happens in the metal itself, not as a paper contract. When a contract expires, there has to be actual delivery of the metal. A seller of a contract has to have the actual metal in the vaults of the exchange in Shanghai. On the Comex, a similar rule should in principle apply, but the Comex rules for gold and silver differ from all other commodities, offering much greater freedom for the BBs

- From the beginning of 2016 the market seems to have changed; for the first time since the steep bear market in 2011 the gold and silver prices are making headway even when under severe selling pressure, such as has been happening recently as gold tries to break above $1300/oz and silver has a ceiling at $18. As soon as prices near these levels, the number of mini flash crashes that typically occur a number of times each day, increases substantially to force prices lower

The charts above are intra-day prices as these appear on www.kitco.com ; the chart on the left is gold, with the silver chart on the right.

Currently

The new bull markets in silver and in gold – which according to long term charts should run for a number of years – are now more than 4 months old. The rising trends have not been smooth; some days prices increase quite smartly and then – often near a ‘round number’ for the price – there would be 4-5 ‘waterfall’ attacks at short intervals, each of them pushing the price down by a relatively small amount, but building on the previous fall in the price to have a significant overall effect.

A big change from the past is what happens at the end of a waterfall; previously, a raid or attack would have a lasting effect on the price; it would drift sideways for some time before buying gradually takes it higher. Nervous buyers would wait before returning to the market. During the rising trend in 2016 – and even to some extent late in 2015 – this pattern of behaviour changed; as the silver chart above shows (it was copied later in the day than the gold chart) buyers rush in to get bargains after a waterfall attack.

The consequences of this greater optimism and determination of gold bulls are of great importance for the market and for the suppression scheme in use. It is to be expected that fewer longs would panic and close positions in reaction to the waterfall attacks, in part because so many contracts are well into profit, but also because of fear that a long position that is closed cannot be opened again later at a lower price. This change in the sentiment also brings bargain hunters into the market whenever the price reacts to the depletion of the bid stack by the waterfall attack.

This means the BBs cannot close their short positions as easily as before and is a sign that the buyers know they are getting the upper hand; while the possibility of a major and sustained attack is not zero, but is now small enough that they hold onto their long positions, even if the price falls. No more stop loss for most of them.

The result is that the BBS are no longer able to close enough of their short positions to reduce their overall short position to a safe level. They are compelled by the way bulls now behave to increase their short positions every time they decide to attack the rising trend in the market. This has brought total open interest in gold futures on Comex – and silver as well – to all time record levels, making the BBs very vulnerable to a squeeze.

At the same time, gold is becoming more scarce. Each long contract on Comex has the potential to ask for delivery of 100 ozz of gold from the seller of the contract. The rule is that a seller must have ‘own’ gold to the extent of the number of contracts that are being sold. At least part of this gold has to be kept in one of the Comex’s regulated vaults, known as the ‘registered’ gold in the vault to distinguish it from other gold that is stored on behalf of its owners for safekeeping only.

Most people active in the gold futures market are trading and do not ask for delivery, so that it is not a crisis when a BB sells more contracts than the gold it keeps in vaults at Comex. Previously, with gold plentiful and BBs easily able to cover short positions whenever they spooked the market causing longs ran for cover, the ratio of total open contracts to the amount of available gold remained low for many years. This meant there never was any fear of default, i.e. a failure to meet a request for delivery.

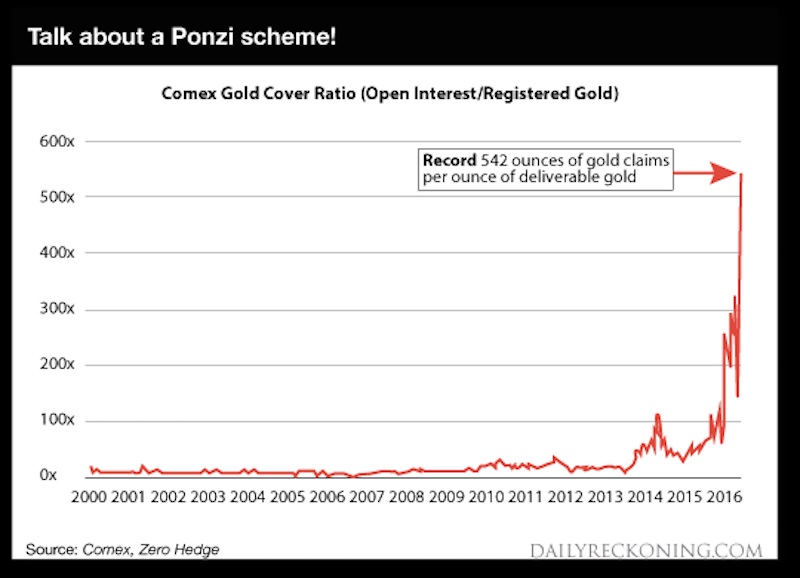

Since late 2015 the situation has been changing for the reasons noted above. As the BBs experienced greater difficulty to close their short positions after a hit on the price, the open interest of the gold contracts grew rapidly to reach all time record highs. By far the greater proportion of short positions are on the books of the BBs. They not only have to carry an increasing amount of margin, but also face the risk of default as more buyers decide to take ownership of the metal as a longer term investment rather than to try and trade futures in a consistently rising market. The chart below illustrates how much recent buyer behaviour has changed this aspect of the market.

Historically, the number of open interest contracts for an ounce of gold in the vaults – also a good indication of the total short position of the BBs – since 2000 remained in the lower digits until about 2010. That was when China joined India at the top as a major purchaser of gold and the slight rise in the ratio after 2010 might be explained by gold becoming less freely available! From 2013 the gold cover of total open interest worsened rapidly, only to explode in 2016, when the gold bull market kicked off.

Given the changed situation with respect to gold futures and the role of the BBs, there seems to be only a low probability of the gold bulls allowing the BBs to reduce their short positions to any significant degree, as they had been able to do previously. It means that a large and sustained inflow of gold into the vaults is needed to ensure that the situation does not get completely out of hand. Also, given the way China and India are buying gold, that prospect too seems to have only a low probability. This means the situation can be expected to get worse, not better.

Yet something specific needs to be done urgently to avoid a catastrophe for the BBs and for Comex – one that would propel gold and silver into totally new high ground. And it has to be done quite soon, in weeks to months, not years. The situation at Comex, as the chart clearly shows, could disrupt one of the biggest financial markets in the world, with wide ranging effects on many other markets.

Just about everything said here about gold also applies to silver. Its manipulation may not have started as early as for gold, in part because at one time the US government had a massive strategic stockpile of silver that could be sold as demand increased – which happened; the stockpile has been history for a decade or longer. The industrial demand for silver is much higher than for gold and with silver mines closing production as the price fell too low, silver in time seems to have become a greater threat to the financial stability of the BBs than gold.

The Future

If the above discussion holds true, the BBs find themselves between a rock and a hard place. The simply have to keep on with waterfall attacks to restrict the gold bull market as much as possible; should the price break free, the margin calls on them will escalate into the financial stratosphere. Secondly, a steep bull market in gold will cause many longs to consider having their hands on the metal itself will be much better than having a long futures position; their requests for delivery will risk default.

On the other hand, should they discontinue the waterfall attacks, the gold price soon will accelerate higher, with rapidly increasing margin calls on their already large short open interest and still with the risk of default should requests for delivery increase, as is then to be expected.

A third possibility is that, somehow, enough gold can be procured to launch a really major offensive on the price and push it down low enough to trigger large scale closing of long positions to enable BB short positions to be closed. If that option does prove to be feasible, the price of gold could be depressed back to where it was in 2015 to defuse the current risk. However at that time it has to be decided whether suppression of the gold price is to continue – resulting in the same critical situation as now exists – or whether the gold price will be left alone to make its own way into a new bull market.

In terms of Comex rules there is also the possibility that when default on delivery is a fact, a condition known as ‘force majeure’ can be invoked; it is in the Comex rules to make provision for when a natural unforeseen event prevents delivery of a commodity against a request, in which case the contract can be settled in cash.

In the gold and silver futures market a need for force majeure will not be because of a natural and unforeseen event, but because of the illegal suppression of the prices, and because Comex did not properly supervise the market. Comex then inevitably will lose all credibility – something Comex would like to prevent at all costs.

Even without any other factors that could come into play, a bullish future for gold and silver over the longer term seems certain. The move higher will not be without hiccups, but it should be steady and sustained when viewed over a longer time scale. These two metals therefore present opportunity for safe haven investments with prospects of very significant capital gains over time. In this respect, many analysts consider that silver is the better opportunity, because it has been suppressed more than gold.

Investing in gold and silver can be done by buying mining shares, through an ETF on a stock exchange or by buying coins or silver bars. Mines offer high gearing and should be part of any portfolio. ETFs offer easy trading opportunities, but carry some risk over the longer term. Owning the metal itself carries no counter party risk, but has a safety risk unless these are stored in secure vaults or other suitable places.

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com