The Changing Role Of Gold

In our post on August 11 titled End of an ERA: The Bretton Woods System and Gold Standard Exchange, we discussed the significance of then-President Nixon’s action of closing the gold window thereby ending the Bretton Woods Monetary system.

Under the Bretton Woods monetary system, central banks could exchange their US dollar reserves for gold. This also ended the gold fixed price of US$35 per ounce.

This week we explore the two questions that concluded last week’s article: What role can gold serve in the international financial system in the future? And why do central banks continue to increase their gold reserves?

Starting with the latter question of why central banks continue to increase their gold reserves?

This is an important factor in the gold market and therefore a topic we have discussed before – see our post from July 8: Central Banks Plan to Increase their Gold Reserves in 2021 – Here’s Why, for example.

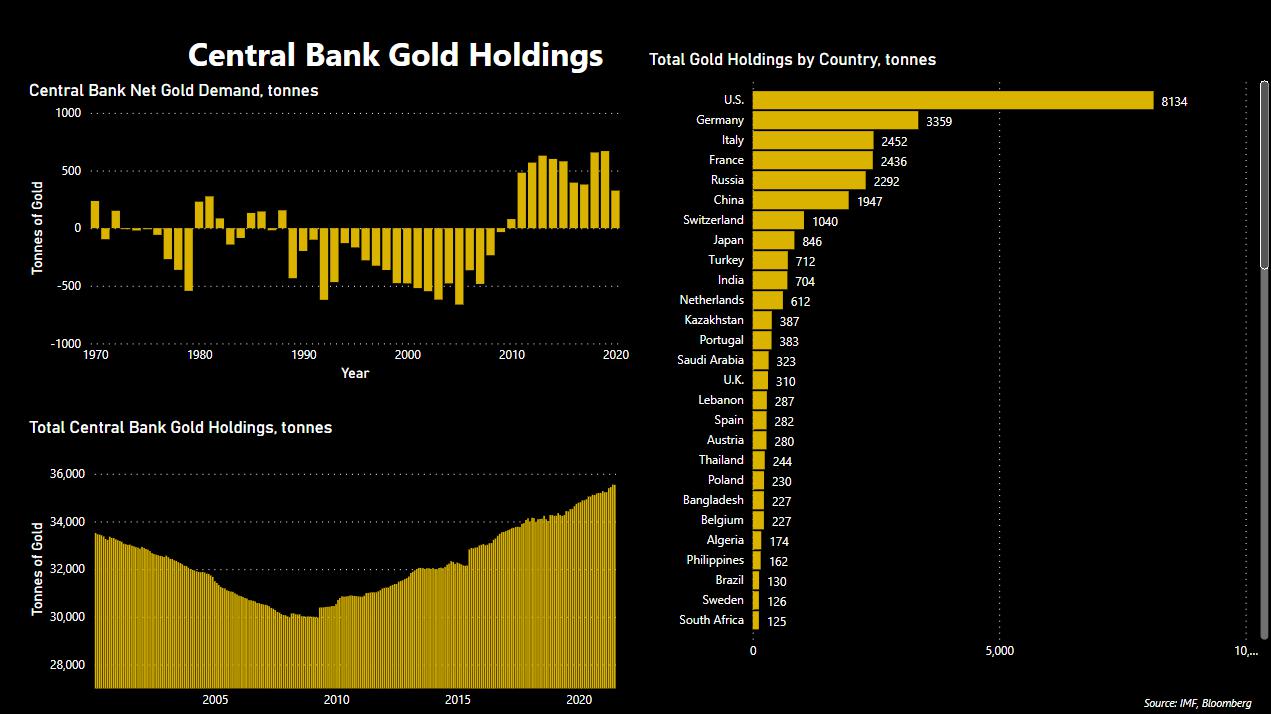

The net demand from central banks has been positive since 2010 and collectively central banks hold over 35,000 metric tonnes of gold. This accounts for approximately a fifth of all gold ever mined.

Gold and its Primary Role

An article posted on Reuters by World Gold Council sums it up as: One of gold’s primary roles for central banks is to diversify their reserves. The banks are responsible for their nations’ currencies. However, these can be subject to swings in value depending on the perceived strength or weakness of the underlying economy.

At times of need, banks may be forced to print more money, Since interest rates, the traditional lever of monetary control, have been stuck near zero for over a decade. This increase in the money supply may be necessary to stave off economic turmoil. However, at the cost of devaluing the currency.

Gold, by contrast, is a finite physical commodity whose supply can’t easily be added to. As such, it is a natural hedge against inflation.

As gold carries no credit or counterparty risks, it serves as a source of trust in a country, and in all economic environments. Making it one of the most crucial reserve assets worldwide, alongside government bonds.

For more on central banks gold holdings see the dashboard below:

Therefore, the bottom line is that central banks are buying gold for many of the same reasons you and I are buying gold. Gold cannot be ‘printed’ by the Fed, the ECB, or any other central bank. In other words, this means gold is not subject to debasement.

And gold has attractive portfolio characteristics. In a central bank portfolio consisting of only a few currencies that might qualify as reserve currencies (i.e., the dollar, the euro and the yen), gold provides excellent diversification characteristics. For example, gold is very inversely correlated to the US dollar, meaning that in general if the US dollar goes down that the price of gold increases.)

Gold and the International Financial System

Turning to the first question of what role can gold serve in the international financial system in the future?

Also, the fact that many central banks are again interested in gold for reserve purposes suggests that a new, semi-official, role for gold could emerge in the future.

One example of a role for gold is future inclusion in the basket of currencies that make up the International Monetary Fund’s (IMF) Special Drawing Rights (SDR) currency basket.

The SDR is an IMF-sponsored currency basket. Presently includes the dollar, yen, pound, euro, and renminbi (the basket weights of each are determined by the size of GDP, trade, etc.).

When first introduced in 1968 the SDR was meant to supplant the role of both the dollar and gold in central bank reserves. The SDR was initially referred to as ‘paper gold’, and its initial value was set equal to one US dollar.

Suffice it to say the SDR failed to supplant the dollar; the dollar is much more useful to central banks. As it can be widely invested and used in foreign exchange market intervention.

Indeed, today the SDR is still a largely irrelevant currency for everything other than specific, narrow transactions with the IMF

Why might the IMF include gold in the SDR at some future point? Simply because gold is again regarded as a financial asset by an increasing number of central banks! Ben Bernanke may have answered Ron Paul on July 13 (2011) with “gold is not money”, but he did allow that gold is a financial asset, like a Treasury bill.

Given that financial assets are commonly pledged as collateral. One implication is that gold’s role as financial collateral will almost certainly expand again, regardless of IMF policy.

Gold is not a currency, at least not in the sense that there is a national central bank that creates it and sets its interest rate. But to many investors, including central banks, gold is a “currency” of sorts: it is the original currency (the original store of value, unit of account, medium of exchange) in which other, fiat, currencies were later defined.

Gold would enhance the acceptability of the SDR. That means such large-reserve countries as China, India and Russia might well hold more SDRs in their reserves.

There are potentially lesser, non-official roles for gold in the monetary system. These too rest on gold’s acceptability as a financial asset and collateral.

Gold could be a key component of a new commodity basket that central banks will use as a monetary policy price target. Moreover, gold could be used as collateral for publicly-floated government bonds.

In addition, gold could serve as an unofficial fix for a currency in which markets have suddenly lost confidence; this would be a temporary function for gold, but a currency backed by gold. Or where the central bank holds significant gold reserves, provides confidence.

In addition, to reiterate the above points about reasons central banks hold gold. Hungary’s central bank increased its gold reserves to 94.5 tonnes (from 31.5 tonnes) earlier this year and cited the reasons for increasing its reserves as: 1.) long-term national and economic policy strategy objectives.

And went on to say the appearance of global spikes in government debts or inflation concerns further increase the importance of gold in national strategy as a safe-haven asset and as a store of value and 2.) The central bank stated that gold is one of the most crucial reserve assets worldwide [that has] no credit or counterparty risks.

Buy Gold Coins

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

18-08-2021 1788.10 1783.45 1300.13 1295.32 1525.61 1522.00

17-08-2021 1794.05 1789.45 1299.61 1300.57 1524.22 1524.61

16-08-2021 1775.75 1786.35 1281.91 1291.53 1507.61 1517.15

13-08-2021 1757.65 1773.85 1273.59 1281.07 1496.64 1506.35

12-08-2021 1755.50 1747.40 1266.24 1262.85 1494.81 1489.66

11-08-2021 1734.05 1743.60 1255.45 1258.88 1480.53 1486.42

10-08-2021 1729.55 1723.35 1248.22 1244.60 1475.13 1471.05

09-08-2021 1741.50 1738.85 1253.88 1254.06 1481.32 1479.24

06-08-2021 1799.45 1762.90 1292.90 1269.64 1523.59 1497.58

05-08-2021 1811.20 1800.75 1302.07 1294.92 1529.74 1521.63

Buy gold coins and bars and store them in the safest vaults in Switzerland, London or Singapore with GoldCore.

Learn why Switzerland remains a safe-haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

*********