Commodity Super-Cycle

A new Commodity Super-Cycle is likely, finally.

I have poked fun at the Commodity Super Cyclers over the years. Churning out analysis telling of a great economic reset toward real things, fundamental to the global economy, and away from unreal things, like paper “assets” drenched in debt.

I have poked fun at the Commodity Super Cyclers over the years. Churning out analysis telling of a great economic reset toward real things, fundamental to the global economy, and away from unreal things, like paper “assets” drenched in debt.

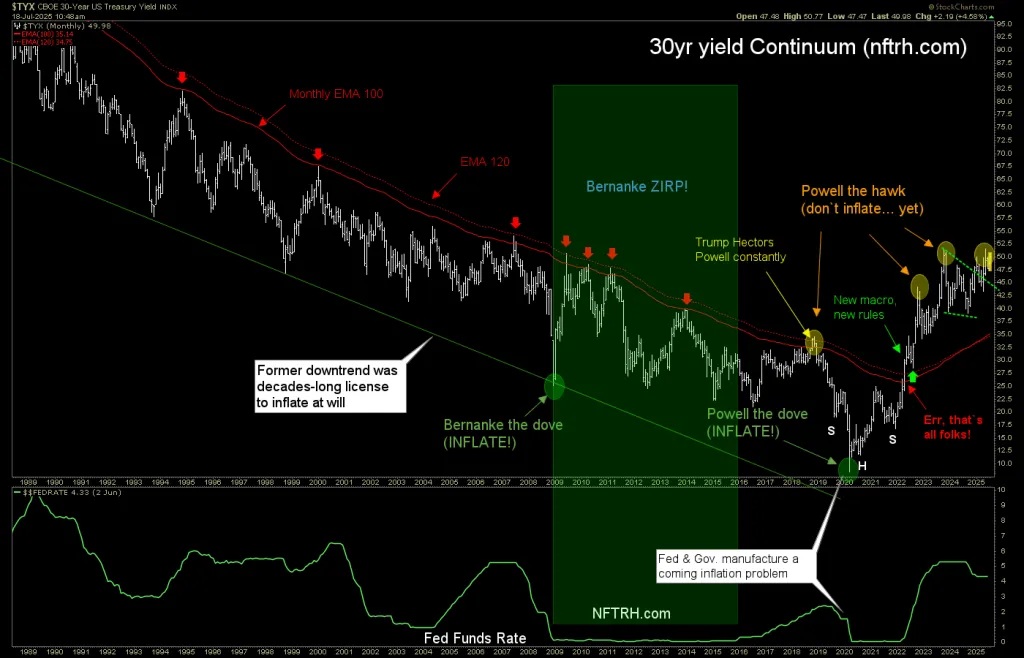

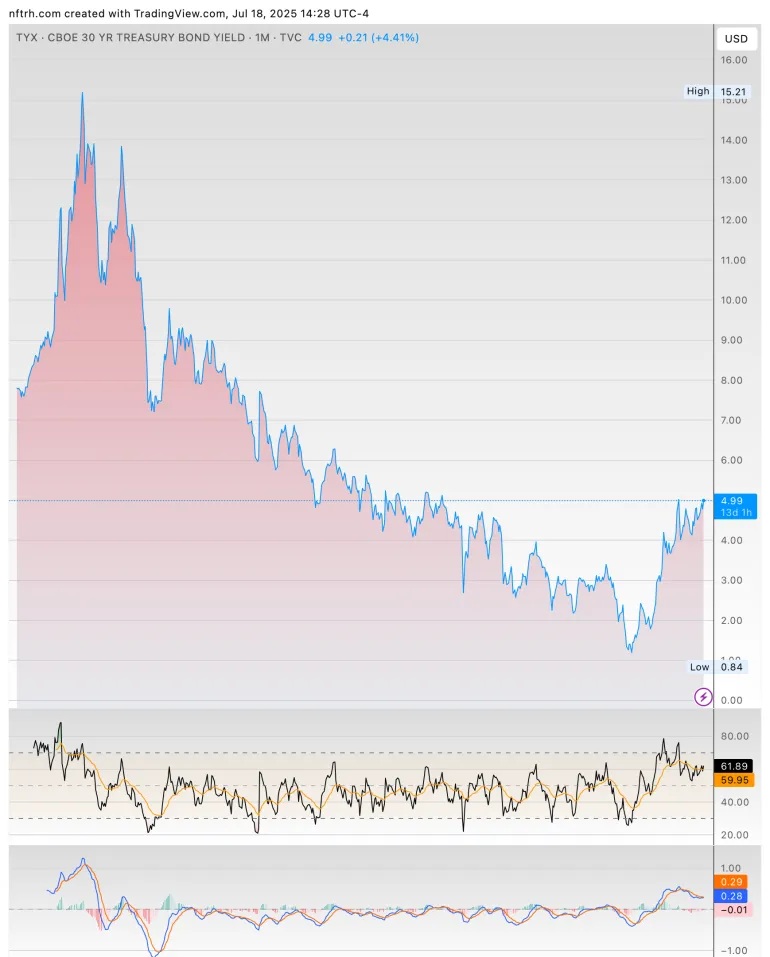

The “Commodity Super-Cycle” theme was promoted with a tone-deaf ear toward the mostly unfavorable macro in place from 2011 to 2020. But when the yield on the ultimate paper asset drenched in debt broke its “Continuum” trend in 2022 (see below) a new macro ensued that would be nothing like that of the previous four decades.

Makes sense to wait for a green light from the “top-down” macro,* don’t you think? In that regard, there could be an interim pullback in late Q3, or Q4 before the festivities in the commodity trades really get going. But the new macro map says it’s very likely on its way. The elusive “commodity super-cycle”. As we are already starting to see, critical commodities will run first and best due to global geopolitical complications.

* Which is exactly what I do at all times in my work. Going macro “top-down” puts you in the right areas so that stock selection becomes orders of magnitude more successful.

New trend in the “Continuum” paves way for a Commodity Super-Cycle

So the Continuum (multi-decade 30yr Treasury yield), about which I’ve spilled oceans of virtual ink in NFTRH and in public over the years, clearly illustrates the new macro from the bond market’s perspective (in markets, the most important perspective), which terminated the old macro in 2022.

The new macro is expected to coincide with a new boom in commodities, especially critical or economically strategic commodities like Rare Earth Elements, Palladium & Platinum, Copper, Uranium and more. Gold would be the “money” anchor of this new macro along with to a lesser degree, silver, which makes up for its less “moneyness” with much more widely used industrial utility than gold.

The old macro (RIP 2022) saw the Federal Reserve inflating the system at will every time a liquidation came along to resolve a previous economic phase that had been inflated by the Fed. The Fed was given license to chronically inflate by extreme fears of deflation that would crop up during post-boom liquidations, when the 30yr Treasury yield spiked hard down. Profound recent examples were Ben “the Hero” Bernanke in 2008 and Powell in 2020.

Powell’s 2020 inflationary operation finally blew the macro gasket that shot us right out of that decades-long trend of disinflationary bond market signaling to today’s inflationary signaling, which is very likely to mean three things (possibly subject to interim deflation scares)…

- More severe inflationary effects as new inflationary policy is layered on top of already inflationary macro signaling (saturation), as opposed to previous decades’ disinflationary signaling in bonds…

- The Fed will be less relevant in this new macro because it is a product of the banking system, and the banking system is intimately tied to the bond market, and the bond market’s signaling is now adversarial for those who wish to inflate using interest rates and bond manipulation. So that leaves…

- Government, which can do whatever the hell it wants where creating new money supply is concerned. As long as said government is in power and is supported by a large enough segment of the population, it can (and just did to the tune of $Trillions) appropriate new credit/debt for the Treasury in order to spend as it sees fit.

As the old Billy Preston song went,

“Nothin’ from nothin’ leaves… nothin’.

You gotta have somethin’ if ya wanna be with me…”

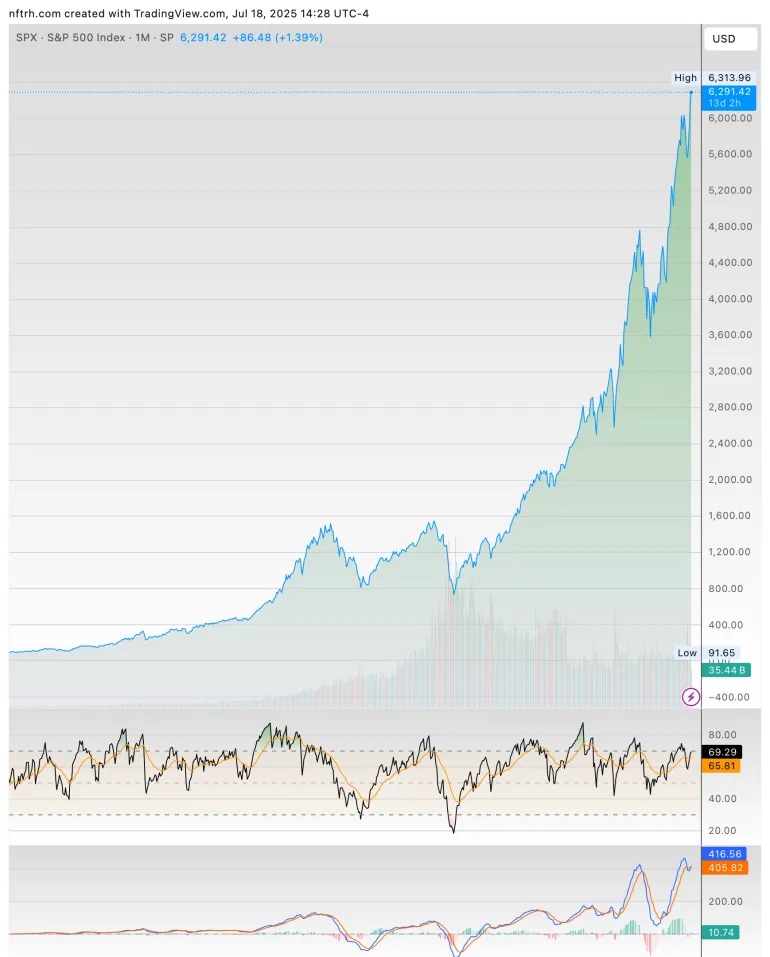

Well, policy in the old macro had been creating somethin’ from nothin’ for decades. Monetary policy from the Fed and Fiscal policy from government. Ever expanding credit and the debt pile that came with it gave us the wonderful illusion of prosperity. Why, just look at the stock market (SPX, first chart below) over the time that the Continuum held sway.

Notable phases were 2001 when Greenspan kicked off the Age of Inflation onDemand, and 2008 when Bernanke kicked us off of any vestige of normalcy as 7 years of Zero Interest Rate Policy and whatever other ingenious manipulation he could get his hands on blighted the system, further enriching the rich, impairing the middle and poor and laying the groundwork for a fed up public’s vote for a strong man, saying all the right things, to assume the White House (twice).

Here is another view of the 30yr yield “Continuum” above, showing what long-term yields were doing as part of the great funding mechanism for the chart directly above. The trend in the funding mechanism is broken and now it’s up to government to do the heavy fiscal, and corrosively inflationary, lifting.

Stocks are at best projected to follow a path similar to the 1970s, perhaps not appearing to be in a bear market but when measured in terms of gold, and soon silver and commodities, very much in a bear market.

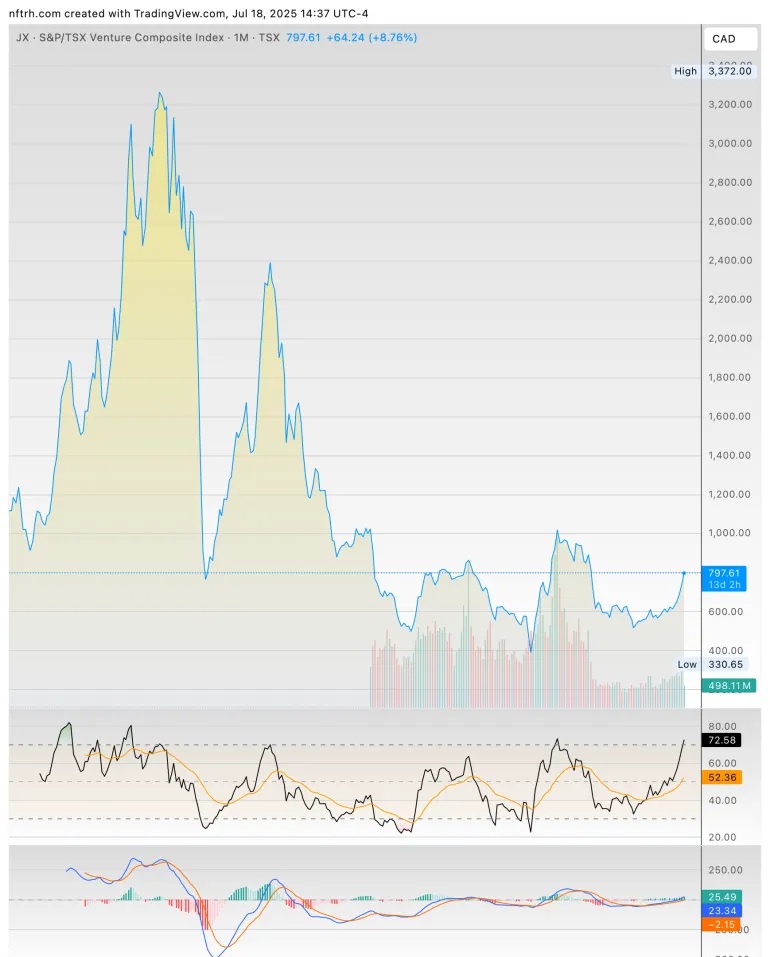

18 Year Bear Market Ending?

On a related note, what do you think that will mean for Canada’s TSX-V index, making its low in the 2020 crash and now on a rally, potentially into a new bull market after topping out in 2007? If it does bull, it will have been earned by years of ignominy. Thus far we have the 2020 low, a higher high and a higher low in the books. I’d say that a higher high above 1000 sets ‘er free.

This index holds many speculative commodity stocks, especially in exploration.

Da ‘V’ is getting overbought lately and is nearing our next upside target in the 800 to 850 range. But dialing up a bigger, inflationary macro picture, the backdrop could be just what the hole drillers in this index ordered. But the index includes excellent prospects and scammy cow pastures alike.

On that note, the October time frame is going to see a new addition to NFTRH’s public presence. It will be an audio Podcast (most likely at our Substack) that will feature discussion of the financial macro in general, but also semi-regularly at least two and possibly three highly experienced geologists,* intimately involved with and knowledgeable about exploration mining. I look forward to learning personally (I got an earful of learning on the phone today with one of the gentlemen) and extending the opportunity to listeners.

While a lot of garbage will probably rise in a bull market, why not try to select the quality? For that, I personally require education and guidance about the real “boots on the ground” aspects of the mineral exploration industry. Not a newsletter. Certainly not a broker. Boots. On. The. Ground. And experience.

Given my current macro view, I cannot wait to get going on the Podcast. I think you’ll like it if you are at all interested in this sector. Listeners can submit questions to these gentlemen, and also we’re going to talk and let ‘er rip on discussion of the entire exploration mining space. I can’t wait. If you haven’t already, subscribe to the Substack. It’s free and that way you’ll be aboard when the Pod starts. Oh, and there will be a lot of good content coming in the meantime. ;-)

* I just found out this week that I am lucky enough to have at least three Geos in the subscriber base.

For “best of breed” top-down macro analysis and market strategy covering Precious Metals, Commodities, Stocks and much more, subscribe to NFTRH Premium, which includes a comprehensive weekly market report, detailed NFTRH+ updates and chart/trade setup ideas, and Daily Market Notes. Receive actionable (free) public content at NFTRH.com and subscribe to our free Substack. Follow via X @NFTRHgt and BlueSky @nftrh.bsky.social, and subscribe to our YouTube Video Channel. Finally, check out Hammer’s trade (long and/or short) setups.

Courtesy of NFTRH.com

********

More from Gold-Eagle