Don’t Dismiss Gold And Silver

There is worrying evidence that 2021 will see the end of fiat currencies, led by the US dollar. US dollar money supply has accelerated at an extraordinary rate, a process that will continue.

Signals from the markets that a monetary collapse is increasingly likely include a weakening dollar on the foreign exchanges, bitcoin’s price reflecting an growing disparity between the rate of its issue and that of fiat, rapidly rising commodity prices, and a bubble in non-fixed interest financial assets.

Current thinking is yet to link these events with a developing collapse in fiat currencies, but it is only a matter of a relatively short period of time, perhaps spurred on by a banking crisis, before a realisation that a John Law-style financial asset and currency collapse is on the cards.

While gold rose in dollar terms by 25% last year, it has yet to reflect an increasingly likely collapse in fiat currencies, which this article concludes is likely to happen in this new year.

Introduction

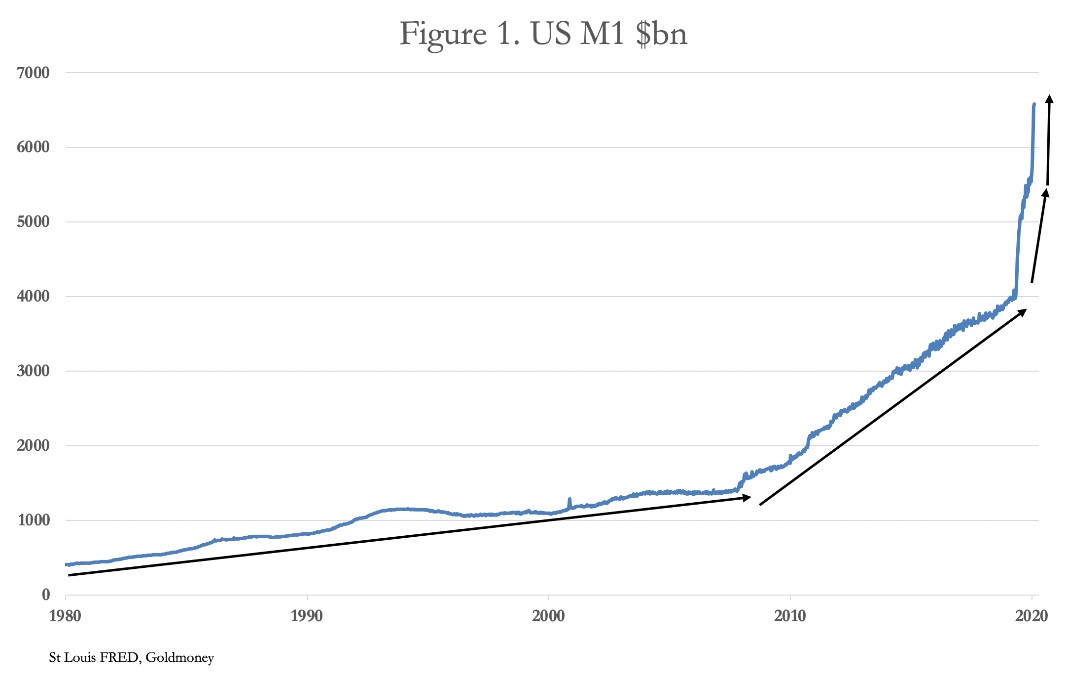

We enter the new year with a growing realisation that fiat currency debasement is accelerating. It is hardly surprising that bitcoin bulls, who have learned about relative rates of currency issuance, are in the vanguard of those hedging increasing currency debasement. They are being encouraged by statistics in charts such as that shown in Figure 1.

Institutional investors in increasing numbers are now clamouring on board what appears to them to be the only asset which offers a hedge for ever-increasing quantitative easing and government budget deficits. They continue to eschew the traditional hedges, precious metals, because they are only seeing one side of the story. The reason that bitcoin is on a tear is because of its heavily restricted rate of issuance relative to fiat. But investment managers still think in terms of profits measured in their own government’s fiat. For them, bitcoin is an investment or speculation, and despite monetary inflation they still believe money is dollars, euros, or whatever to be eventually sold for fiat. Managing money is their mandate, always to be accounted for in fiat, and they are tasked to deliver investment performance measured accordingly.

With respect to fiat, they see the expansion of the money quantity, but in their muddled assessment of the future they still think that at some stage, central banks will succeed in rescuing their economies from disaster through monetary policies. While the short-term outlook is unclear, they read into rising commodity prices an expectation of increased future production. And the stunning performance of equity markets, assumed to be forward looking, is sending the same message. When covid is over, perhaps in the late spring, the common opinion appears to be that business activity will resume, and the economy will continue to grow.

While the establishment’s portfolio managers are dreaming their dreams, gold closed up only 25% on the year, outperformed by most commodities by a country mile — a respectable performance as an investment asset, but barely noticed by the equity and crypto bulls.

The underlying condition is the accelerating debasement of fiat. The chart in Figure 1 is not just a covid response. The rate of M1 monetary inflation has been increasing over the years, but only now has the rate of increase become hyperinflationary — there is no other word for it. So far, the Fed’s inflationary response has been just to the first round in the covid battle; round two is not yet reflected in the rate of hyperinflation, having been delayed by squabbling politicians. And the Fed’s flexible friend is yet to be fully deployed to prevent the US economy from being destabilised by the pre-covid crisis of September 2019 in the US repo market, and the trade and financial wars between America and China, which commenced in earnest in late 2018.

The global banking system is now withdrawing credit from industrial borrowers, because bankers’ greed for loan business is now replaced by fear of non-performing loans. The commercial banks must rapidly contract their balance sheets in the face of collapsing businesses and supply chain disruption or face their own crisis.

This is not a lending environment for the support from bank credit expansion that the Fed or any other central bank would wish for. Even without an overt banking crisis, the Fed and the US Treasury will have to work together in their attempts to rescue the US economy from an inevitable slump. They cannot succeed, but they must try, sacrificing the dollar as a deliberate act of economic policy.

Therefore, the dollar and all the fiat currencies tied to it will become valueless, because there is a firm mandate in all welfare-driven nations to continually deploy monetary inflation at a rate that is now accelerating rapidly.

Currency values are eventually determined by markets

We know from the theories of exchange and from historical examples that fiat money is only money if it is accepted as such by the population, and that irrespective of the quantity in circulation the public can reject it utterly. Rejection of the medium of exchange is not something done lightly. It only happens when the state expands the quantity so recklessly that the public, being initially slow to understand that their money’s purchasing power is being debauched, collectively understands what their government is doing with money, and that there is no hope left for it.

For today’s dollar, that this process can happen quickly is explained by the peculiar circumstance of the current situation compared with past hyperinflations for the following reasons:

- The rapid rise in the price of bitcoin and other leading cryptocurrencies has forewarned a significant and growing minority of people about the consequences of an inflation of the quantity of state-issued fiat money. Alerted by bitcoin, whose price is rising rapidly, increasing numbers of the wider population are getting the message. It is only a small step for bitcoin bulls to realise that bitcoin’s price rising is a forewarning of a monetary collapse and not just the relative supply argument central to reporting today.

- When it is more widely realised that the failing economy is not just a covid problem but that a 1930s slump already beckoned beforehand, investment managers will realise that hyperinflation of the money supply has not only arrived but will continue and end up destroying the currency.

- Foreign holders of dollars and dollar assets are beginning to discard their $27 trillion stockpile, throwing all financing of the US Government’s exploding deficit onto the Fed’s shoulders. The Fed’s financing of the budget deficit and agency debt by QE will run into the headwinds of rising interest rates, reflecting an increasing time preference factor forced upon it through the foreign exchanges.

- When it becomes clear that the Fed has lost control of US Treasury bond prices and therefore of equity market valuations, the dollar will collapse in tandem with asset prices — the closest precedent being John Law’s failed Mississippi bubble in 1720 France. This process of wealth destruction can be expected to be more sudden than the European hyperinflations of the early 1920s.

- When a sounder form of circulating money is available a degree of economic activity can continue, and in doing so prolong the final collapse of the fiat currency. In Germany, between 1920—23 gold-backed US dollars circulated, and increasingly business contracts were struck either in dollars or adjusted by the rate of exchange. There is no offsetting form of circulating sound money to prolong the life of fiat currencies today.

Monetary collapse is the fate that America and the other nations who look to the dollar as their reserve currency are increasingly certain to face. Furthermore, with modern economies highly financialised, the message that a currency breakdown is due will spread considerably more rapidly than in examples from the past. It is therefore possible fiat currencies will not survive to see 2021 out; they may not even survive to mid-year if, as seems highly likely, a global banking crisis occurs in the near future.

The collapse of fiat wipes out financial services

Our analysis is firmly pointing to a combined collapse of financial assets and currencies, likely to be unexpectedly sudden and would certainly be devastating. If, for a moment, we assume a total fiat currency collapse occurs, then all existing financial contracts, being denominated in fiat currencies, will become worthless. The accumulation of OTC derivatives, totalling some $606 trillion nominal, will become redundant, along with a further $30 trillion of exchange traded derivatives, because one side is always a fiat currency or a fiat currency’s interest rate. Global bond markets at a further $128 trillion would also be wiped out. Equities would lose most or all of their value until they can be priced in the successor to fiat money. And being a financial asset designated in fiat, we can kiss goodbye to bank credit in its fiat form. Goodbye to pensions and insurance funds as well.

Part of the elimination of derivatives involves the London forward settlement OTC market for gold and listed gold contracts on Comex. Notional values of these OTC contracts were $867bn according to the Bank for International Settlement at end-June 2020. Today, the main gold futures contract on Comex is capitalised at $111bn, which with other exchanges’ gold contracts gives an all-in total of about one trillion dollars. Those who believe they have exposure to gold in these markets will find they do not, and that the process of this discovery is bound to lead to a rush to obtain physical gold.

In current dollars we are looking at the destruction of roughly one quadrillion dollars of financial and banking contracts. But as described later in this article, there is a solution, and that is to deploy central bank and government owned gold to stop the slide. Where governments are bold enough to do so, their currencies can become gold substitutes. Insofar as financial markets evolve from pure fiat to being based on these gold substitutes, then they have a future. But to the extent that they currently depend on the fuel of monetary inflation, that future will be severely restricted of eliminated. And after some normality returns under gold standards for different currencies, the relatively low and stable originary rate of interest for gold is likely to restrict future demand for derivatives even more.

Bitcoin is not suited to replace fiat

To the dismay of the crypto crowd, bitcoin is both unlikely and unsuited to succeed fiat as the common medium of exchange, for two important reasons. The first is central banks don’t own any and have no interest in adopting any form of crypto other than ones whose ledgers they control. We know they are racing to get central bank digital currencies up and running, partly to head off private sector alternatives. But these proposed CBDCs are just another form of fiat and will fail as surely as revolutionary France’s mandats territoriaux did following public rejection of the inflated and hated assignats.

However, central banks and government treasury departments do own gold — almost certainly less than the 35,171.3 tonnes reported by the World Gold Council, when leases, loans and double-counting are allowed for. But the majority at least own some gold. Even though it is likely to be a last resort, turning their fiat currencies into gold substitutes is a central bank’s only option to avoid a complete currency collapse, and with it the collapse of all state spending.

The second reason bitcoin and similar alternatives are unsuitable is one identified by Ludwig von Mises in a different context — the socialist calculation debate. Mises pointed out that for an economy to function it required unfettered market prices in order for entrepreneurs and businesses to be able to calculate returns on business investment. The other side of prices is their measurement in money terms. When state-issued currencies were functioning as gold substitutes — which was the situation for capitalistic economies at the time of the debate — their purchasing power was broadly stable over a typical investment cycle, allowing businesses and entrepreneurs to anticipate returns on a proposed investment. If an inflexible, limited-issue cryptocurrency like bitcoin became the circulation medium to replace fiat, no investment for a multi-year project could possibly be contemplated because of the effect on future prices. Measured in scarce bitcoin and with a firm cap on its total issue, prices for finished products at the end of the investment would end up being significantly lower than their production costs, thereby ruling out the project itself.

That won’t stop cryptocurrencies like bitcoin continuing to soar while increasing numbers of the investing public see them as must-have wealth protection at a time of rapidly increasing fiat debasement. But that is a different function from operating as a practical means of exchange.

The return to sound money

Gold qualifies as sound money because of its inherent flexibility. If the market demands it, it can draw on above-ground gold stocks currently assigned to other uses, notably as jewellery which probably accounts for about half of all gold ever mined. And annual mine supply throughout history has added to above-ground stocks at a similar pace to global population growth. These are the necessary conditions for a suitable form of money chosen by free markets, which is why whenever government money imposed on its population fails, for millennia the money to which everyone returns has always been metallic.

We know that ever-increasing inflation of the dollar has turned, or is now turning into hyperinflation, by which is meant that it is now virtually impossible for the Fed to resist demands for a continual exponential acceleration of the money supply, ending with the dollar’s destruction. That being the case, the only thing that will stop a rapid and final collapse of the dollar’s purchasing power will be to turn it into a credible gold substitute, accepted by the general public staring into the abyss of a total monetary and economic collapse.

Assuming the US Treasury’s 8,133.5 tonnes of gold still exists and has not been sold, leased or loaned, it is a relatively simple matter to turn fiat dollars into fully exchangeable gold substitutes and to reintroduce gold coinage into circulation. That is not to be disputed; though, admittedly, the sharp reductions in government spending that must accompany sound money are a more difficult topic which must be addressed at the same time.

The most significant problems to be surmounted are both intellectual and political. Intellectual, because the monetary and economic establishment has spent the last fifty years denying gold has a monetary role, and political in that through imposing the dollar and with the assistance of the military complex, the American state sees itself as the world’s protector from Chinese and Russian ambitions — a hegemony it will be reluctant to lose.

America’s current geostrategy is made even more difficult to abandon by the fact that by default Russia has already prepared itself for a gold standard by weaning itself off the dollar. Together with its citizens and as a deliberate act of policy since 1983, China has progressively cornered the market in physical gold. There can be no doubt that since that time China has accumulated a substantial tonnage of bullion not declared as monetary reserves, with which she can back the yuan. Arguably, the economic benefits of putting the yuan on a gold standard and for the Chinese government to abandon inflationary financing would incur less pain from the adjustment process than would be faced by any other nation. Unlike the Russians, private citizens in China owning some 17,000 tonnes will gain a wealth dividend from the introduction of a gold standard. Consequently, the re-establishment of a US gold standard would be seen by America’s permanent establishment as handing unacceptable levels of wealth and economic power to her enemies.

The longer that America dithers about pinning a collapsing dollar to gold, the worse it will be for it. And assuming she actually has 8,133.5 tonnes of unencumbered monetary gold, not only is it the lowest ratio of national gold ownership to above ground stocks in over a hundred years, but it is also the lowest ratio of its gold to total monetary gold held by all the central banks.

This side of a dollar crisis it is hard to assess how quickly the Fed and the US Government will correctly assess and adopt their only option. A significant drawback will be the necessity to return to balanced budgets, which entails massive spending cuts in not only public welfare but in the bloated defence budget. Get it wrong, and 8,000 tonnes of monetary gold could disappear remarkably quickly.

Purely as a working assumption, at this early stage we should assume that a rapid collapse in the dollar’s purchasing power will eliminate between 95%—100% of it; the retention of any residual value being the consequence of changing fiat dollars into becoming credible gold substitutes.

Confidence in this outcome is drawn from the psychological forces at play evidenced in previous fiat money collapses, both on the government side and on that of the general public. In particular, the lessons from the collapse John Law’s Mississippi scheme have worrying parallels with the current situation. Law used inflation of his unbacked livre to ramp the share prices of his Mississippi venture and his Banque Royale, ending up with the destruction of the livre, and therefore of the residual asset values in the combined venture when the bubble burst. Similarly, today’s central banks with their quantitative easing are feeding monetary inflation into the investment management industry, which ends up inflating investable assets on the central banks’ behalf.

If this is the model we need to watch out for, then the collapse of fiat currencies’ purchasing power will not be on the lines of Germany’s 1919—1923 inflation, especially the final phase between May and November 1923. It will be governed by the speed of the collapse of financial assets, particularly bonds, whose prices are remarkably elevated, and their yields suppressed. The flight out of collapsing fiat currencies will continue to be measured against commodities and raw materials. At the consumer level, the destruction of the value of savings and monetary liquidity could become too rapid for a textbook crack-up boom. The time to dump collapsing currencies would be dramatically foreshortened, and naturally, some of the flight out from failing currencies will be into the limited supply of gold coins and bullion.

The prospects for gold’s purchasing power

The introduction to this article describes the backdrop to a shift in purchasing power away from failing fiat currencies. It also concludes that at some point, central banks will have no option other than to turn fiat currencies into gold substitutes. It has pointed out that attempts at a monetary reset without the backing of monetary gold will not only fail, but if the decline in existing fiat currencies is as rapid as this analysis suggests there will be insufficient time to implement fiat alternatives such as central bank digital currencies, and they would rapidly fail anyway.

While the collapse of a fiat currency’s purchasing power will become increasingly obvious, demand for physical gold will increase its purchasing power, measured by the goods and assets it will buy. The desire to hoard relatively limited quantities of gold will increase at the same time as there is a desire to dump fiat money.

Many people who think they have protected themselves with paper gold will find it evaporating due to it not being backed by readily available physical bullion. They are likely to add to the general demand to possess physical gold.

It is therefore not just a matter of the dollar’s purchasing power losing, say, 98% from today. To this an assessment must be made due to the scarcity of gold arising from increasingly determined hoarding of the metal. It is the combination of these factors which drives prices in paper money up, while they fall catastrophically measured in gold. Examples of this effect were commonplace in Germany and Austria in 1922-23, when country estates and residential properties could be acquired for very small amounts of gold — $100 bought a six-bedroom house in a fashionable street in Berlin, when US dollars were trusted gold substitutes at $20.67 to the ounce.

It follows from documented history and from reasoned theory that hyperinflation impoverishes the professional middle classes and bringing hardship and starvation to the wider population. On the threshold of the new year, this appears to be the outlook for anyone who does not take the precaution of hoarding gold. In the light of these factors, there is little point in discussing less important issues, such as the functioning of paper gold markets, let alone following the specious practice of making price forecasts.

Silver

The outlook for silver appears to be less cut and dried than for gold, if only because it is not held by central banks in their monetary reserves. Having been demonetised in the 1870s when Germany moved onto a gold standard, silver’s price measured in gold began a long decline from roughly 15:1 to a record 125:1 last March. Since then, silver has recovered to 71:1 currently.

There is surely little doubt that as the relative moneyness of gold to fiat currencies increases as a result of the hyperinflationary policies of central banks, silver will return towards a relationship with gold that existed when there were metallic metal standards. In those times, coinage was of gold, silver and copper. Even though the abandonment of silver monetary standards in Europe led to a decline in the silver price relative to gold, silver still circulated as money. In fact, by ensuring that a silver to gold ratio in the coinage exceeds Isaac Newton’s 15 ½ to one by a reasonable margin, the problems inherent in maintaining a bimetallic standard do not arise. But in the order of events, a gold exchange standard with otherwise worthless fiat must be established first.

It appears therefore that a return to credible gold substitutes will eventually lead to a lower silver to gold ratio; but it is, at this stage of its evolution hard to imagine it falling much below 20:1. This implies that during the fiat money collapse silver’s purchasing power will significantly outstrip that of gold, more than doubling on a relative basis.

HEAD OF RESEARCH• GOLDMONEY

Twitter: @MacleodFinance

MOBILE: +44 7790 419403

Goldmoney

The Most Trusted Name in Precious Metals tm

NEW YORK | ST. HELIER | TORONTO

Publicly Traded Symbols: CA: XAU | US: XAUMF

© 2020 GOLDMONEY INC. ALL RIGHTS RESERVED. THIS MESSAGE MAY CONTAIN CONFIDENTIAL OR PRIVILEGED INFORMATION. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE ADVISE US IMMEDIATELY. THIS MESSAGE IS FOR GENERAL INFORMATION ONLY AND SHOULD NOT BE CONSTRUED AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY SECURITIES OR ANY OTHER FINANCIAL INSTRUMENTS. WE DO NOT PROVIDE TAX, ACCOUNTING, OR LEGAL ADVICE, AND RECOMMEND THAT YOU SEEK INDEPENDENT PROFESSIONAL ADVICE IF NECESSARY. WE CONSIDER INFORMATION IN THIS MESSAGE RELIABLE BUT WE DO NOT REPRESENT THAT IT IS ACCURATE, COMPLETE, AND/OR UP TO DATE AND IT SHOULD NOT BE RELIED ON AS SUCH. OPINIONS EXPRESSED ARE OUR CURRENT OPINIONS AS OF THE DATE APPEARING ON THIS MESSAGE ONLY AND ONLY REPRESENT THE VIEWS OF THE AUTHOR AND NOT THOSE OF GOLDMONEY INC OR ITS SUBSIDIARIES UNLESS OTHERWISE EXPRESSLY NOTED.

********