On Doomsday Warnings!

Early signs are that the current mega-intervention in the PM markets, a repeat of April 2013 and March this year, has started to taper off despite probably not (yet?) having delivered the hoped for results. There was no large and sustained closing of long positions that would have enabled the shorts to reduce their exposure to any significant degree. The numbers make it look more as if some members of the Big Bank Cartel have started to buy while the others were selling, as mentioned later.

During August there was a distinct decline in the number of new US cases and also in the number of daily deaths, yet the numbers are still on the high side.

I was taken to task for commentating on the COVID-19 pandemic as a major crisis when it should be considered as “. . . normal seasonal flu with the usual 1 in 1,000 death rate”. To put what I wrote in perspective.

My focus on the new virus was triggered fairly early when it became known that infected people were infectious well before they developed symptoms. This is different from the normal flu where infected people first feel sick and are then inclined to take precautions not to spread the flu. It meant that the spread could be more rapid and infect a greater proportion of the population. I also hazarded the opinion that the measures to save lives could have worse consequences than a high mortality among vulnerable people, but that governments will be inclined to play safe and enforce counter-measures to limit the spread.

This is what happened. On COVID mortality the following brief comment should suffice. According to the Washington Post, based on estimates from the Centers for Disease Control and Prevention, influenza — the common flu — has infected about 45 million Americans since October 2019 and killed as many as 46,000.

That is a mortality of 0.10%, which appears to be the annual norm. Comparing apples to apples, calculating mortality as the number of deaths divided by the number of cases, has the US COVID mortality at the moment as 185 901 deaths from 6 096 235 cases. For a mortality of 3.05%, this is 30 times higher than for the usual flu and it is not over yet. If nothing was done and the COVID pandemic spread a little worse than the usual flu to infect say 60 million people to result in nearly 2 million deaths, how much blame would ba cast on the powers that be?

One should keep in mind that the last similar virus outbreak, SARS, also a corona virus, in 2003 had a mortality just short of 10%, when 774 people of 8098 that were infected died. Given the draconian regulations with which China reacted to the new virus, this surely predisposed the world to a virus that could be as deadly as the 2003 outbreak. And Bill Gates keep telling us there is worse to come.

Interesting timing! As I was writing this, I received notice of Jim Rickards – for what it is worth, said to be based on information from the Pentagon – warning us that worse is yet to come. With reference to COVID he has the following quotes. This things not going to stop until it infects 60 to 70% of people.” - Michael Osterholm, Director of CIDRAP (Centers for Infectious Disease research and Policy) . “The worst is yet ahead of us.” -- World Health Organization Director and “Bottom line, it’s going to get worse.” -- Anthony Fauci.

I lack sufficient knowledge to judge whether Rickards and his sources are scaremongering in pursuit of their own agendas or whether there are new studies that support their statements. As shown in US Markets last week, the number of daily new infections are in decline even while daily deaths developed a second wave. There was, however, a recent report of a new apparently more scary virus in China, of which I now cannot find the source. So perhaps Bill Gates is correct in what he is still saying after a long time – also in pursuit of an own agenda – “There is worse to come”.

Meanwhile, Sweden, the poster child of countries whose government did not issue any severe regulations to limit the spread of the virus has suffered 5821 deaths of 83 958 COVID cases for a mortality of 6.9%. They also have 576 deaths per million of their population as opposed to the US’s 561 and Taiwan’s 0.3, with their mortality at 1.5% with 7 deaths from 481 COVID cases. Taiwan’s population is 23.8, 2.2 times that that of Sweden yet with vastly different COVID experience. Taiwan also did not institute a lockdown, but had been fully prepared for COVID-19 after the SARS 2003 epidemic. That made a big difference.

Perhaps the world needed a proper wake-up call to be better prepared for whatever happens next. Clearly, most of the western world had not been as well prepared for COVID as many countries in Asia, including populous countries like Japan and South Korea. There are many possible reasons for the next doomsday event or events populating the media. Many of these are being laughed off as mere doomsday manias that will never happen – or will never be as bad as been predicted by their promoters.

On a local scale there is a channel on YouTube that reports on earthquakes and promotes preparedness for Americans in areas that could be subject to quakes to have the necessary ready for survival should their location experience a large one. I often wonder how many US households in these areas are properly prepared. Just as I listen to the lip-service being paid in most countries to the risk of the effects of global warming or, to keep life interesting, for a new ice age should the trend to lower solar activity extend as deep and as long as similar times in the past. In both cases, if events happen to surprise us by being greater than anticipated, one important effect will by lower food production. That could result in the kind of population reset that Bill Gates and others are known to have championed for a long time and often discussed in the US corridors of power.

Turning back to the PM metals, Kitco had an interesting article last week. It was a report of an interview with Doug Casey and Rick Rule, both I believe with vested interest in the bull markets in gold and silver continuing for quite some time. The article was titled. “The Greater Depression and fate of the global economy”. Sounds much like another reason for a doom laden future not mentioned earlier. Two quotes from it are:

“All of the economic problems that we have are basically caused by government interference in the economy and in people’s lives, and COVID has given them an ideal opportunity to interfere as much as humanly imaginable. So, the greater depression, is going to be, as a result, worse than even I thought it was going to be,” Casey said.

“The consequences and example of extraordinarily low interest rates are that people are being forced to spend and speculate rather than save. Is that a good thing, probably not, but we’re going to continue to see these inconsistencies in the economy as long as we have popular political responses from government,” he [Rule] said.

Casey’s words reflect a knee-jerk reflex opinion that governments mess up matters further when they try to fix a problem. Reflexes develop when the same reaction is needed to avoid suffering a similar problem repeatedly, so there has to be a lot of truth in his words. The second quote points to the problem of low interest rates and their effect on savers, in particular the elderly who have to live off what they have saved.

At the moment many people, investors and workers, are hoping for a V-shaped recovery from COVID. Casey and also Rule are not as optimistic and neither are the commentators who perceive hyperinflation of the US dollar as a new situation with which Americans and the world will have to contend in the not too distant future. Interesting years ahead, irrespective which doomsayers prove to be right.

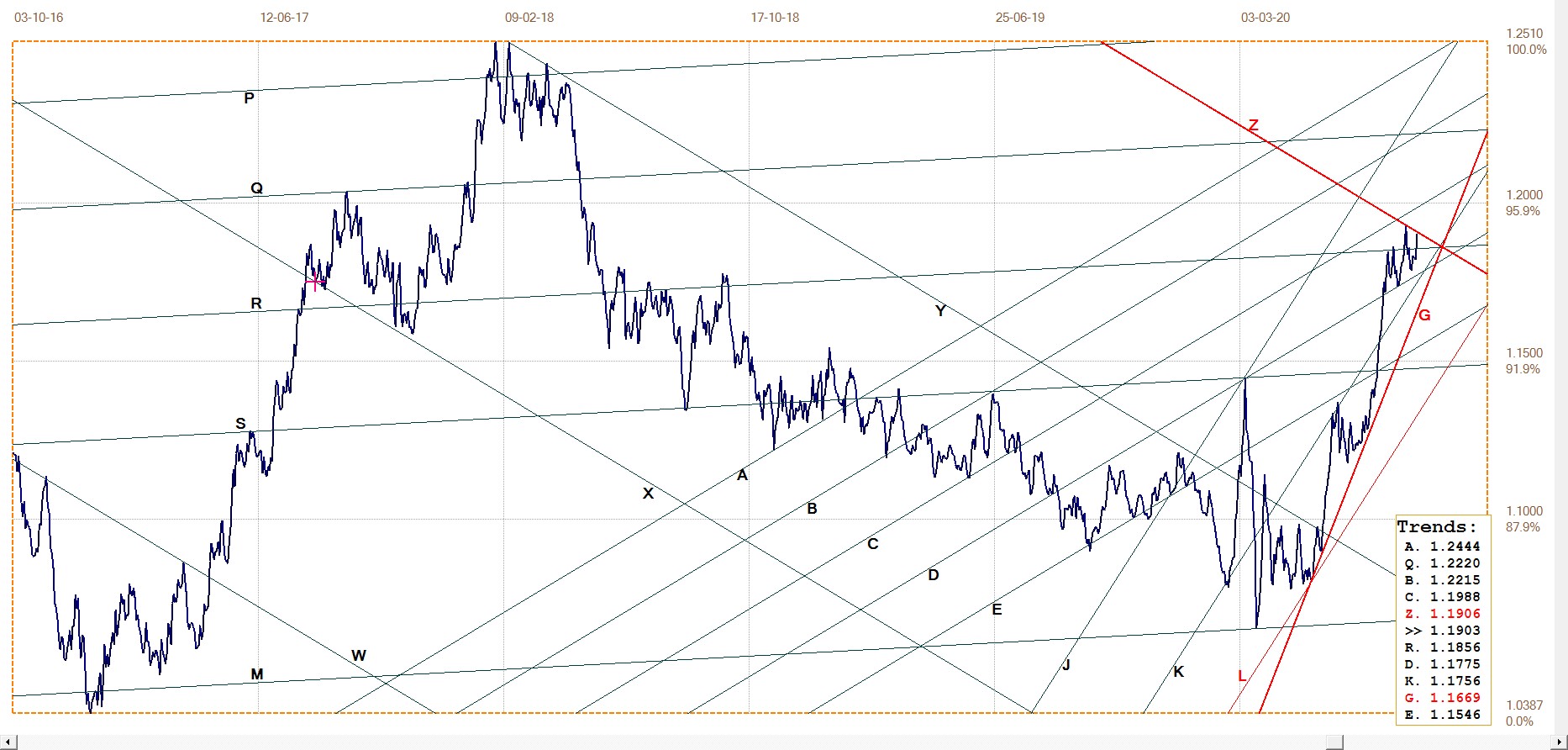

Euro–Dollar

The euro improved from the recent low of a week ago to again reach resistance at line Z ($1.1906). It is still holding in bull channel JK ($1.1756), the upper half of the broad channel JKL. The euro first reversed off line Z on 18 August to hit a low on the 24th, before rebounding for a second close right at line Z.

This trend line is the last of the set WXYZ, which spans four years of price history, with al four trend lines acting as significant resistance or support. They happen to be equally spaced to an accurate degree, with the ratios of its two channel pairs WXY at 502:498 and XYZ at 500:500 close to and at the 500:500 of a channel that is evenly divided.

This implies that line Z should act as important resistance. Therefore the euro will have a spend quite some time challenging the resistance before it could manage to break higher and resumes the rising trend. Alternatively, it might soon break higher and then rapidly extend the ruling bull trend much higher.

Euro–dollar, last = $1.1903 (www.investing.com)

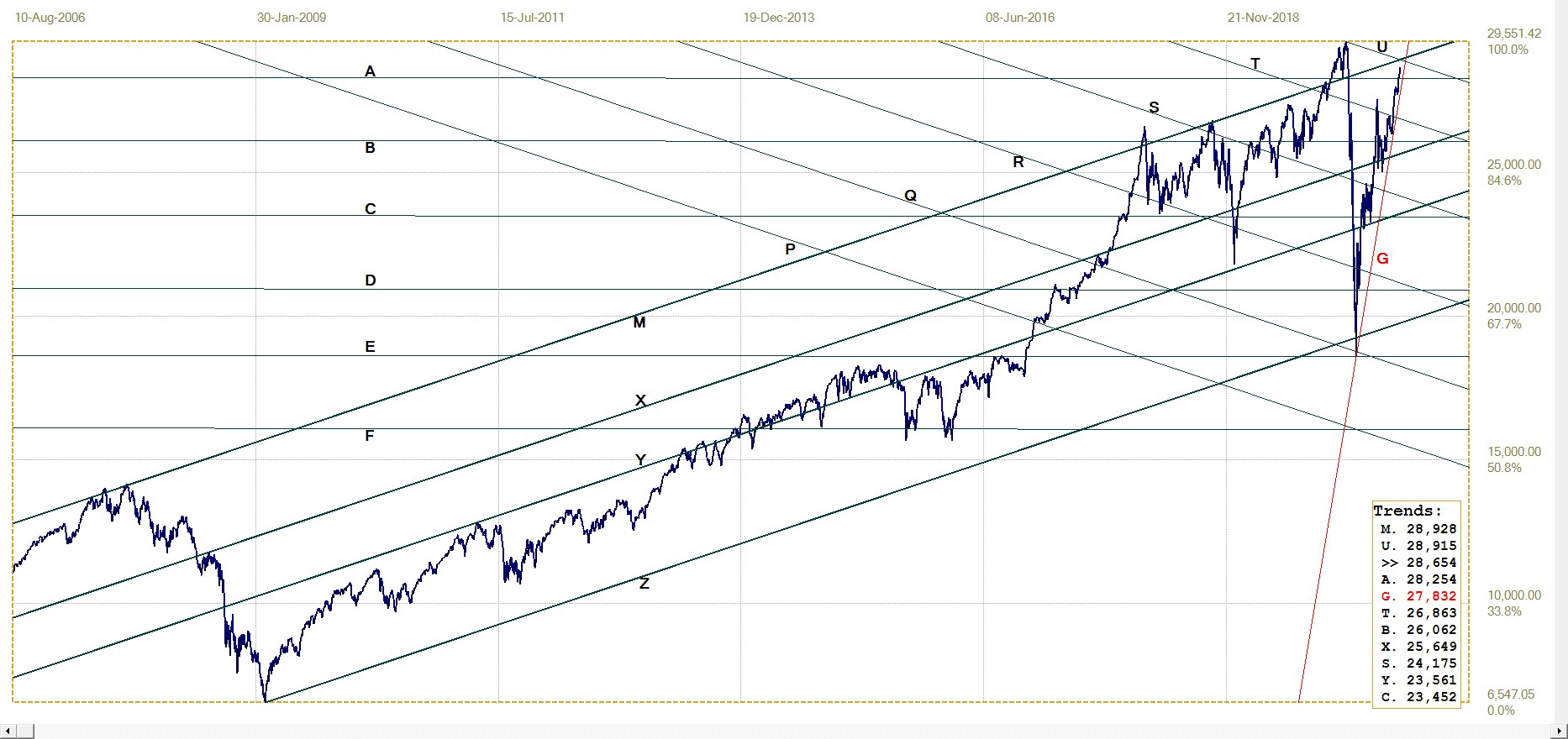

DJIA Daily close

On Friday, the DJIA ended at a new high for the move higher since the recent sell-off. It has been following the steep gradient of line G (17 832) higher since the it made a spike low at 18 593 on 23 March. The initial acceleration was steeper than line G, it has now been holding tight to the trend line. The DJIA is the only laggard, with the S&P500 and the Nasdaq already setting new all time highs – the Nasdaq doing so in serial fashion.

Line U (28 915) and the top of the main bull channel at line M (2 8928) are the two obstacles that have to be overcome before a similar achievement is possible for the DJIA. The sustained rally on Wall Street is posing an interesting dilemma for all analysts who try to explain the illogic of new all time highs at this time when the economy is in trouble. Two key possible reasons for the stock market’s strength are that the COVID-related increase in liquidity is finding a home in equities, secondly, that investors expect inflation and a decrease in the value of the dollar, that will be very bullish for Wall Street once the economy does get into gear again.

Both reasons result from the actions of the Fed and Congress to combat the effects of the pandemic. The knee-jerk reaction of too much money chasing the stocks is more acceptable for many people; as money gets tighter again and the situation returns to normal, prices will adjust lower to reflect financial reality. On the other hand, the Fed’s talk of goosing the inflation rate – in effect to ease the repayment of the COVID emergency spending at a later time – raises the spectre of a repeat of the 1970’s in the US and more recently in a few other countries where inflation, once it picks up speed, creates long lasting problems for the economy. Not that the president is complaining about the confirmation by the stock market of his claims that the economy is in great form with better to come.

DJIA, last = 28653.87 (money.cnn.com)

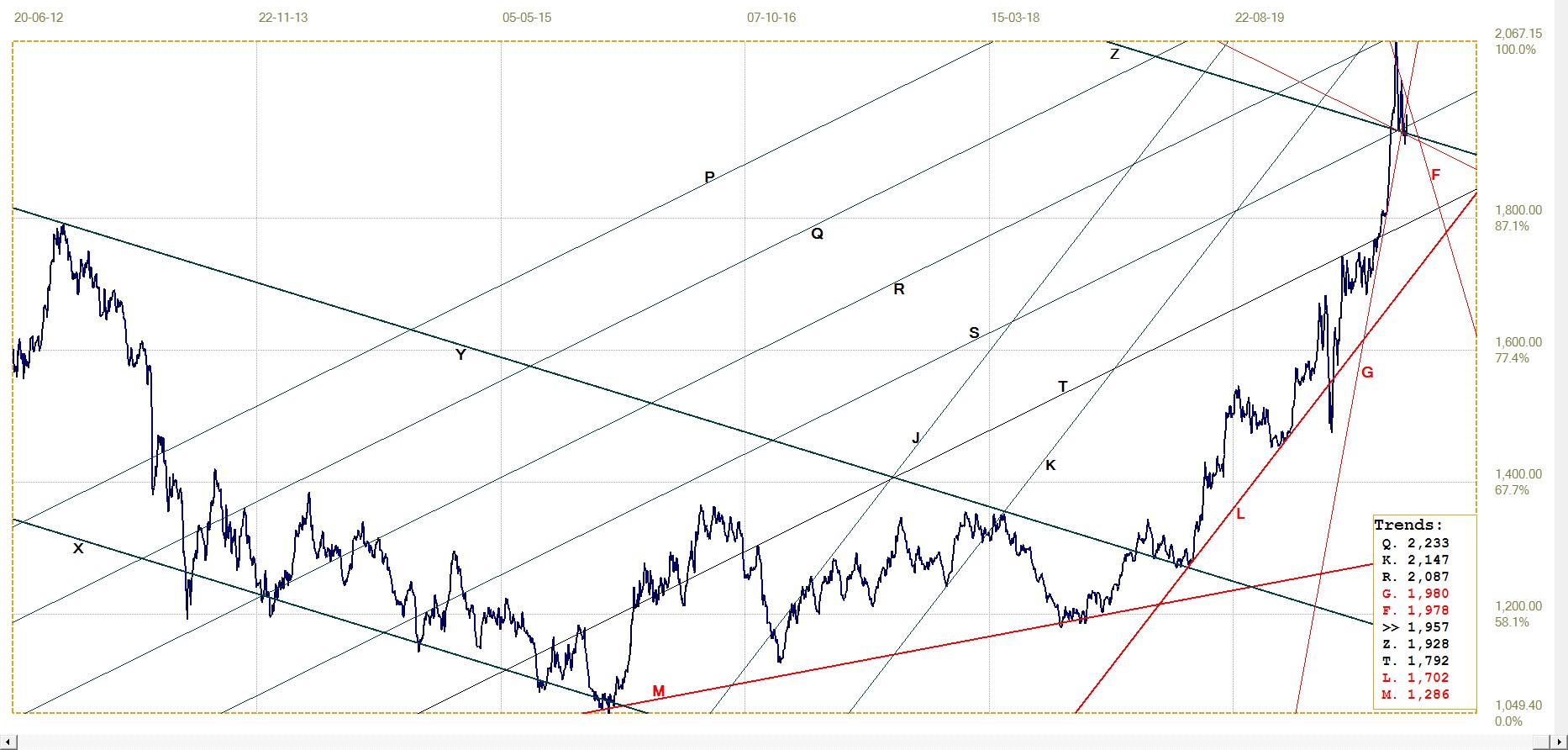

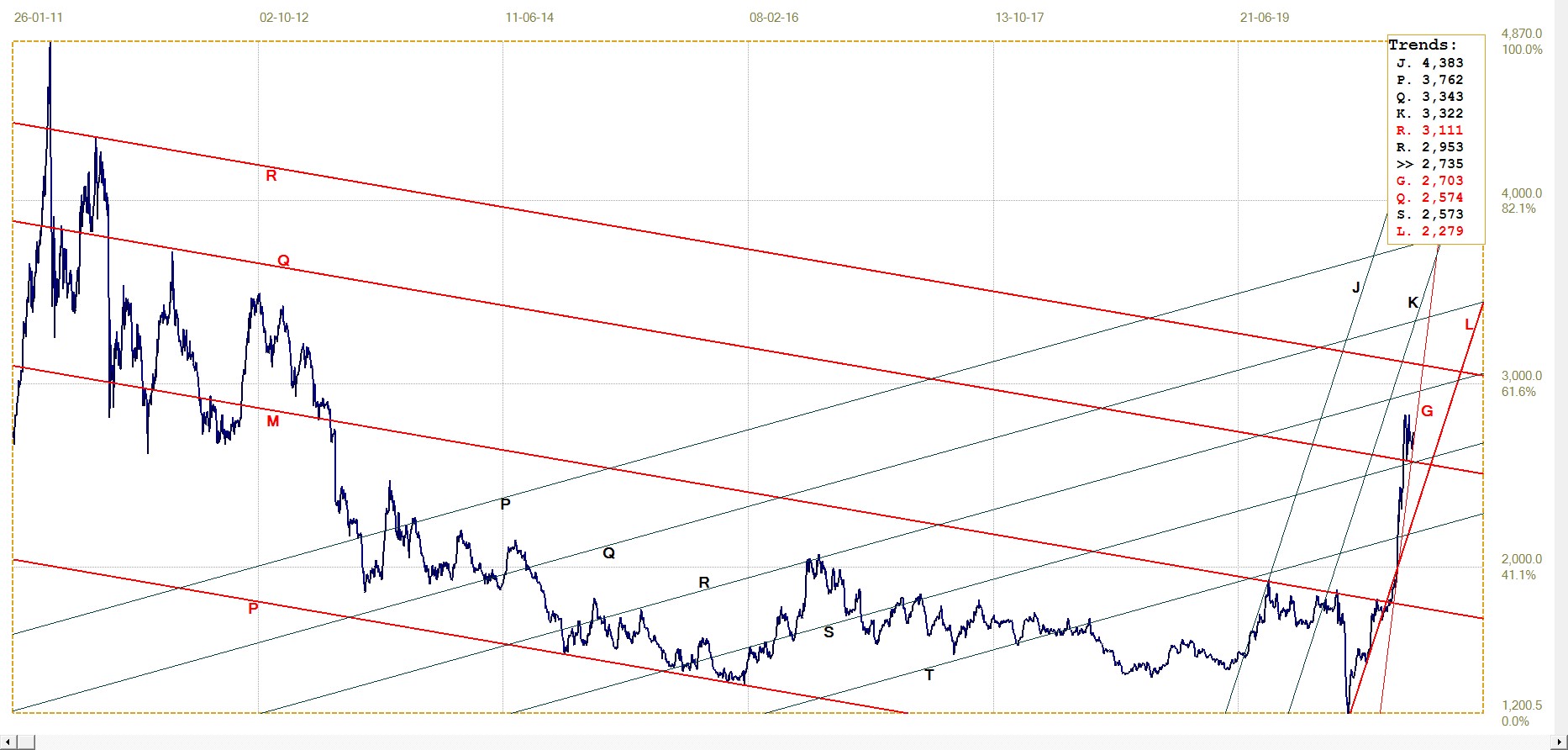

Gold London PM fix – Dollars

The sideways break to below the steep gradient line G extended last week to hit a low London PM fix at $1911.15 that was also a clean break below line Z (1928) – the top of channel XYZ with a ratio of 383:617, one point away from the Fibonacci ratio at 382:618. Last week in US Markets it was also mentioned that a recovery to above line Z and ideally also back above line G ($1980), will put the price of gold back on track to reach the target of $2200 early in October. To do so would also require a break above line F ($1978).

The break back above line Z did materialise last week, but at $1957 for the PM fix on Friday the price is still a little below line G (1980) and also line F. The gold OI on Comex hardly changed during the last week and this could mean that the cartel is not achieving its desired objective of closing their short positions – unless there was also many new long positions opened by opportunistic buyers. This means either the Cartel is still in trouble or the black boxes of the large Specs have decided that the gold rally is over for the moment and it is time to go short.

According to the CoT report, the large Specs did increase their short positions by Tuesday, but the 1670 new short s are too little to change anything substantially.

Gold price – London PM fix, last = $1957,35 (www.kitco.com)

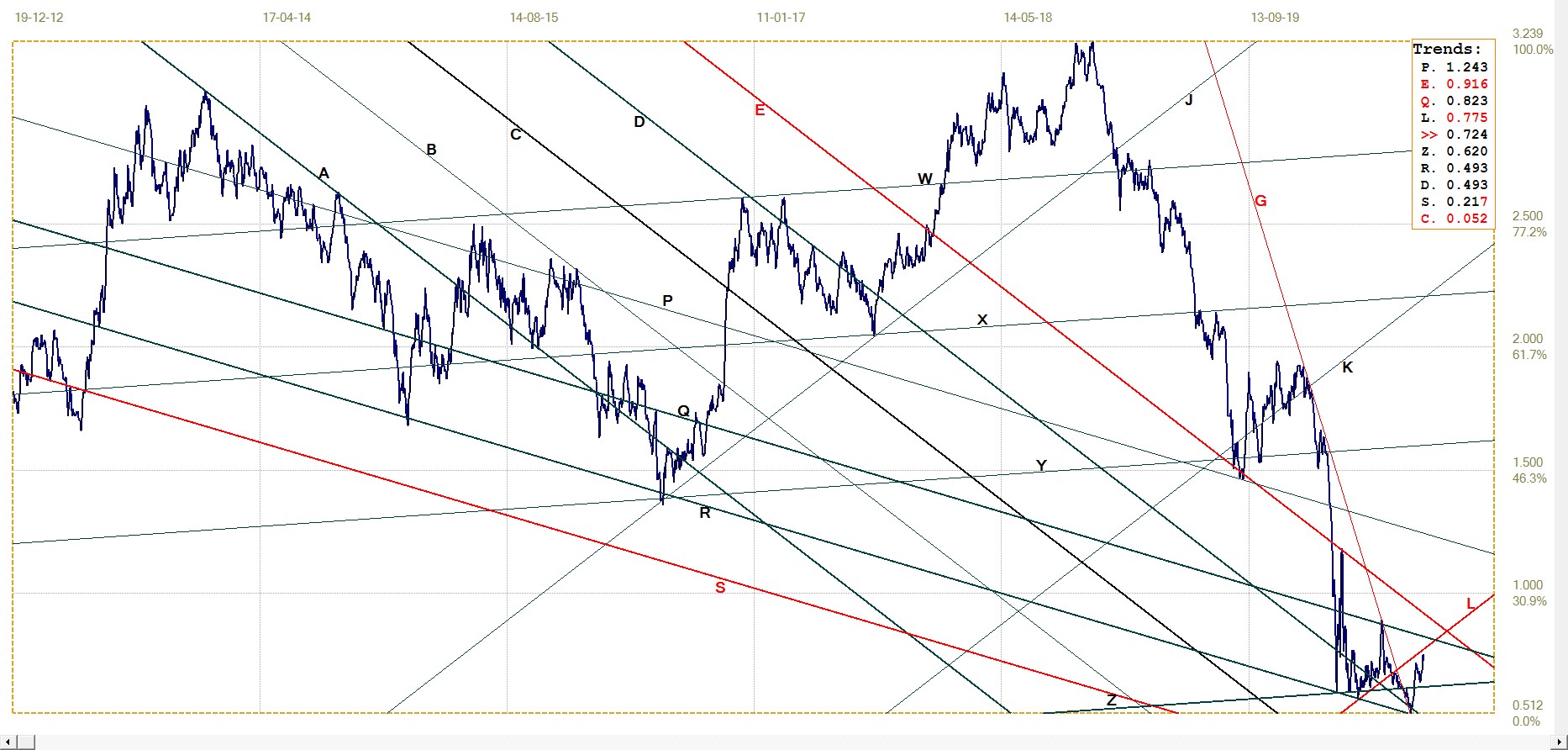

Euro–gold PM fix

The combination of a strong euro last week and the price of gold under some more pressure brought the euro price of gold below the support of line R (€1646) as well as channel KL (€1656). The late improving price of gold and some dollar softness recovered the euro price above line R, but on Friday it was still located below line L.

Despite a less than exciting move higher off the low at €1616.26 on Tuesday, the jump in the euro price at least informs us that the price of gold later last week did improve on its own strength and not merely because the dollar was softer. This may bode well for this week, should the price of gold continue and extends the trend of the recent few days. Only next Friday’s NFP remains as a hurdle that has to be overcome before the bull roars ahead!

Euro gold price – PM fix in Euro, last = €1647.3 (www.kitco.com)

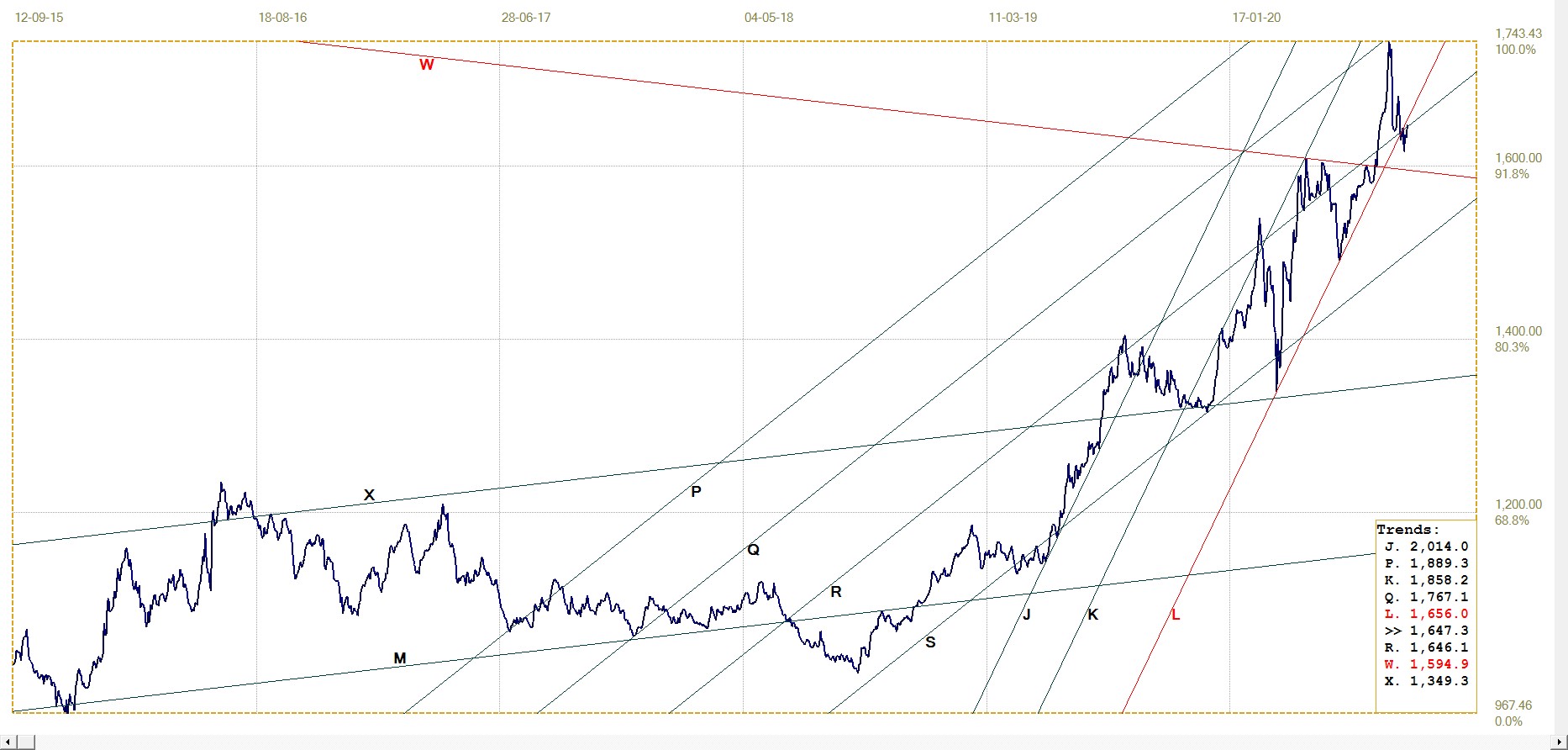

Silver Daily London Fix

Silver daily London fix, last = $27.35 (www.kitco.com)

Last week during the sustained sell-off that only changed late the week, silver held up better than gold. The price per the London fix, which happens still early during the US trading day, remained above line G ($17.03). The low fix last week for silver was on Wednesday, when the fix at $26.395 was only 13c above line G that had a value of $26.26 on that day. Two days later line G was at $26.68 and the $17.03 in the trends table is where the line will be on Monday.

The silver OI on Comex dropped from the 191k ten days ago to 168.6k on Friday as per the preliminary report. That is a substantial decline of more than 22k contracts ad it will be interesting to see the CoT report next week. The September contract fell by about 50k contracts as the month end expiration took its toll. The December contract only increased by a little more than 20k to show the September decline was not due to longs rolling over to the next month. This implies that shorts were covering last week to reduce their silver exposure, which is good news; some members of the cartel were buying while others were selling!

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 0.724% (www.investing.com )

It now looks as if the possibility of lower yields that could even turn negative is not on the cards for the near future. Som reports have mentioned that the yields could drop below zero during 2021, probably based on projections of how much damage of a long-lasting nature COVID-19 could do to the economy. For the time being, a further decline in yields is not a concern. It seems a sideways trend between lines L (0.775%) and Z (0.620%) can be expected.

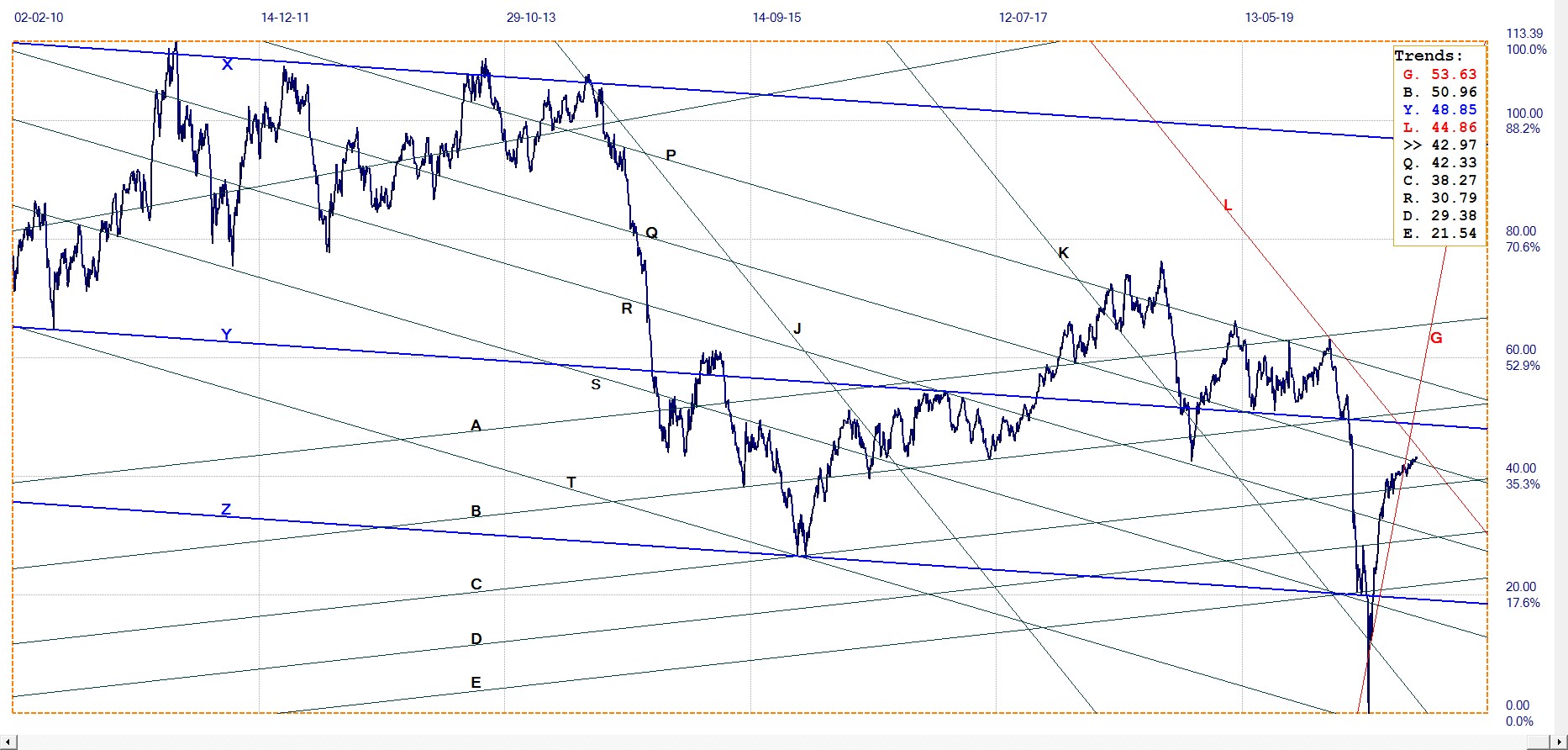

West Texas Intermediate crude. Daily close

The standard comment of the past few weeks still holds: the price of crude inches higher at worm-like speed and has broken below the steep trend line G ($53.63) and then marginally above the resistance at line Q ($42.33). A break above bear channel KL ($44.86) is needed to see the price break free, but if the snail’s pace of the price continues to hold, it could take some weeks to do so.

WTI crude – Daily close, last = $42.97 (www.investing.com )

© 2020 daan joubert

*********