The End Of The Beginning

Last week provided confirmation that the tide of battle in the 2011 war on gold and silver has turned, as anticipated last week. However, winning a major battle is not the end of the war. When the Allies stopped Rommel’s advance eastward along the North African coastline at El Alamein, not many kilometres from the Nile there was great excitement in England that the war could be almost over. Churchill however commented that the victory in the desert was only the end of the beginning; there still was a war to be won. The $1300 mark, where a resurgent gold price closed on Friday, and the $18 level that briefly yielded to silver – and soon should do so again – are major milestones on the road to final victory, which might be left behind as early as this week.

Not too many weeks ago, a majority of comments about the precious metals was in a near panic state because of the extreme net short position of the Commercials; a sure sign of a major retreat in prices that would allow the Commercials opportunity to close many of there short positions at a good profit. Yes, many longs did close a good number of June contracts, but rather than sit on the sidelines, a majority of them switched to a later month, so that the reduction of the net short position most likely fell short of their expectations.

With gold on the march again, being led out of Shanghai, the Commercials are again fighting a rear guard action. With no time to consolidate, they are taking on a new lot of shorts, soon to be back at an extreme net short position. All this raid has accomplished is to make those longs who had closed their positions when the prices fell and now are trying to catch up to the market determined they would not fall for the same trap again.

They yield on the US 10-year Treasury note reached a low below 1.59% last week, a sign than when the DJIA failed to hold 18 000 there was a knee jerk shift to the traditional safe haven when equities looked to full of risk. The other side of the coin has it that if there is such panic buying of bonds, there are not many natural buyers of equities left. It remains to be seen whether the directed buying of equity futures by the mystery players that so often manage to turn a bear into a bull during the final hour of trading can resurrect Wall Street again as they have done so often in the past whenever there was a sell off. Early signs warn that the herd is heading for the narrow exit and it will not be as easy as in the past to steady them and to turn them around.

Rapidly changing conditions on a global front is causing the dollar to become more volatile, even with strong intra-day swings to and fro. Technically, the odds favour a bear market for the currency once the uncertainties get sorted out and the forex market develops its own herd instinct. When that sets in, the widespread selling of dollars will feed the fears of the herd and this one too will be difficult to turn.

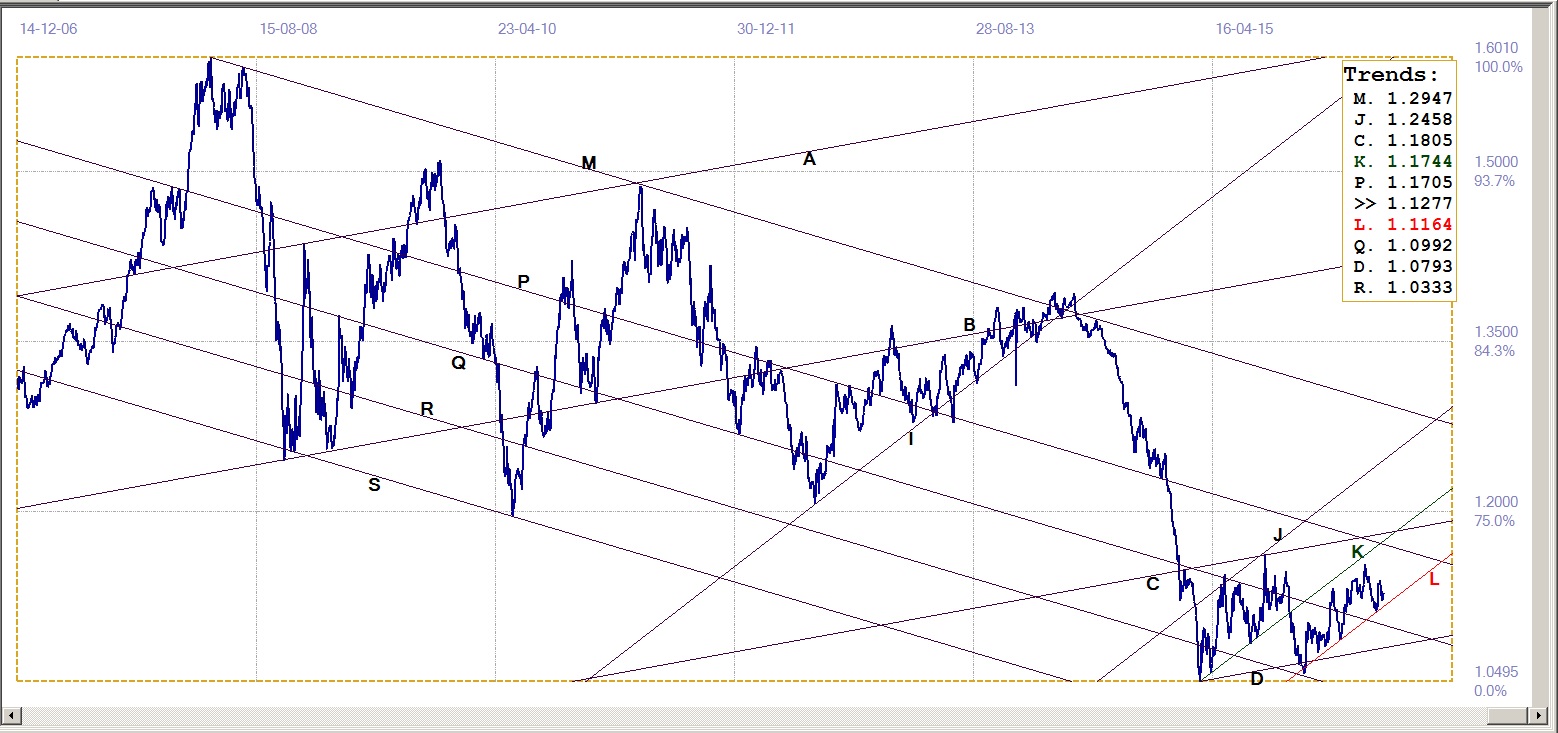

Euro-Dollar

When determined rear guard action had the dollar in a brand new rally, the euro came right to testing support at line L ($1.1164), bottom of new bull channel, KL. When the poor NFP figure provided a springboard, the euro jumped higher, but last week the dollar resumed the offensive and the euro moved mainly sideways at best. The euro is however still bullish, while the channel remains intact. The first resistance for the euro is now at line P, at $1.705, with line K, top of bull channel KL at $1.1744. The resistance is still far out of reach at this time, which means the real test for the euro is how well it can manage to keep away from the bottom of its current bull channel while moving higher to perhaps take on the resistance at lines P and K in due course

Euro-dollar, last = $1.1277 (www.investing.com)

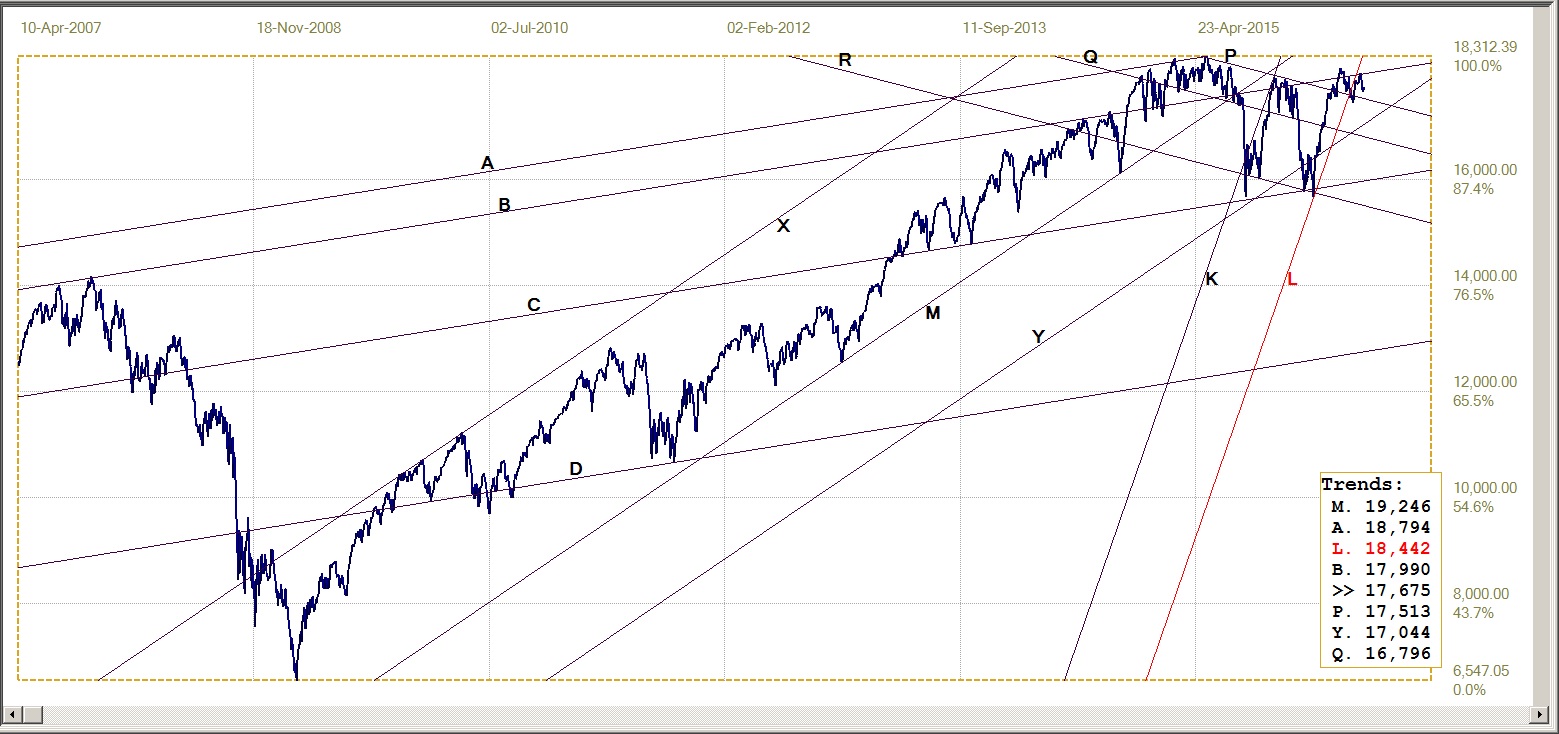

Dow Jones Industrial Average (DJIA)

The failed break above 18 000 late in 2015 soon slipped below steep bull channel KL (with line L by now well out of reach at 18442) and then had another stubborn rally that again and briefly broke above 18 000. This move higher also broke above the resistance at line B (17990) but could not hold. It was anticipated reversal to below line B would be the start of a new bear trend and this has now happened.

Weakness last week ended clear below line B and seemingly ready to test support at line P (17513). A break lower there will confirm a new bear move under way.

Dow Jones Industrial Index, last = 17675 (money.cnn.com)

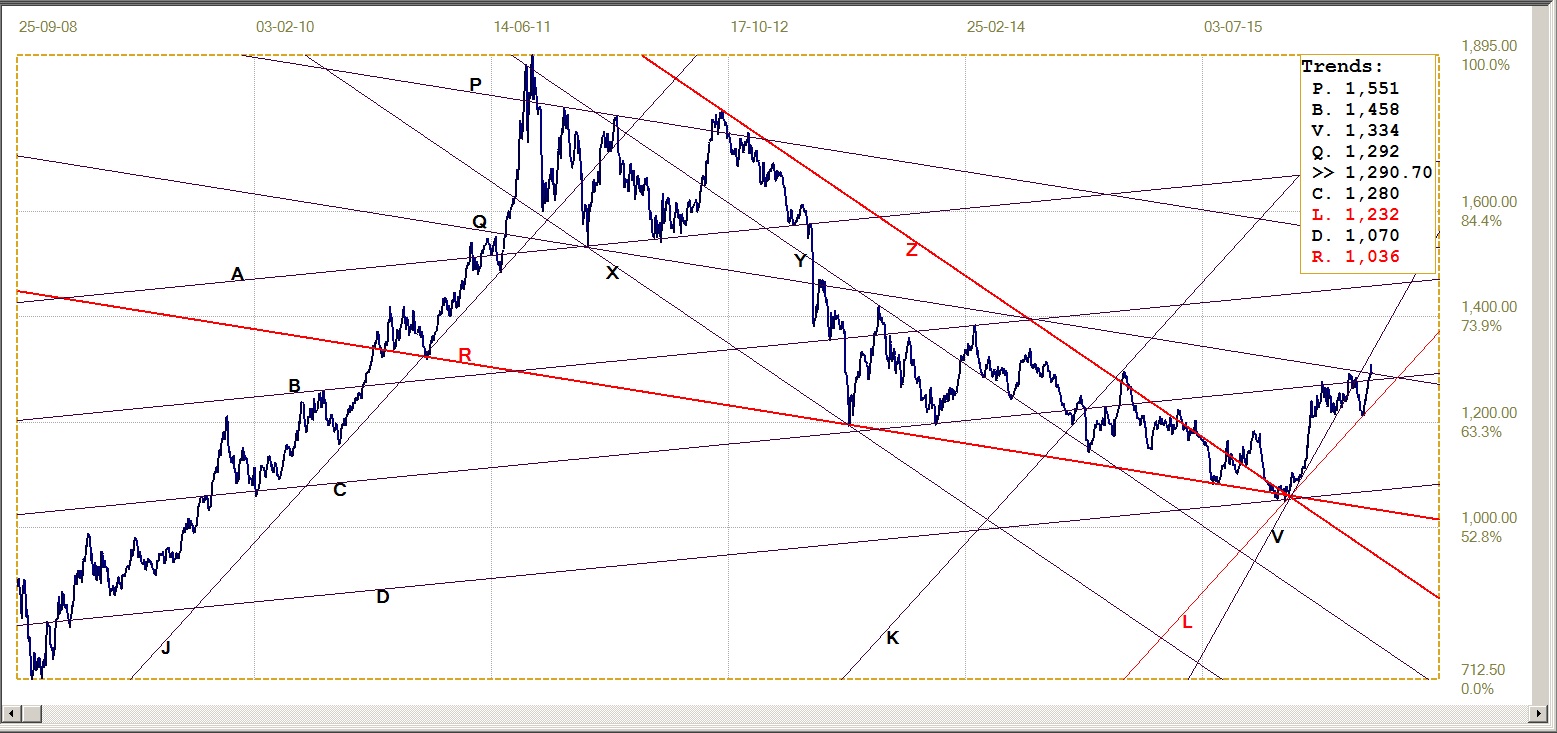

Gold PM Fix - Dollars

Gold price – London PM fix, last = $1290.70 (www.kitco.com)

After holding to the initial steep bull channel during the new 2016 rally, of which line V was the lower boundary, the May sustained rear guard action forced a break lower. As so often happens, the price simply adjusted itself to a new shallower bull channel, KL ($1232), holding at line L before resuming the bull trend. The new bull channel is as usual also derived from the old master gradient, M, which is no longer in view in this analysis.

Observation of how the Comex prices and those in Shanghai change during active trading in Asia clearly showed that prices there have been dragging Comex higher much of the time. $1300 was broken during a surge in Shanghai, but failed to hold under determined selling on Comex and presumably in Shanghai as well. If true, it must be a drain on the available metal reserves in the west.

This week the gold price kicks off above the earlier resistance at line C ($1280). A minor break above line Q ($1292) failed to hold, with Friday’s PM fix marginally back below that trend line, which technically is new resistance – but which may also be a goodbye kiss on line Q before resuming the rising trend. This week should tell.

Gold PM Fix - Euro

Euro gold price – PM fix in Euro, last = €1145.2 (www.kitco.com)

The euro price of gold gained from the stronger price of gold while the euro held mostly sideways. It ended the week close to resistance at line (€1180), with line R (€ 1196) coming into play a little higher, just before the €1200 level. The key to the rising trend is of course that the gold price should continue to improve at faster rate against the dollar than the currency can do. This seems a reasonable expectation as Shanghai (gradually) could be taking over the price setting role from Comex, while Europe is still in turmoil, financially with banking concerns and by the migrants.

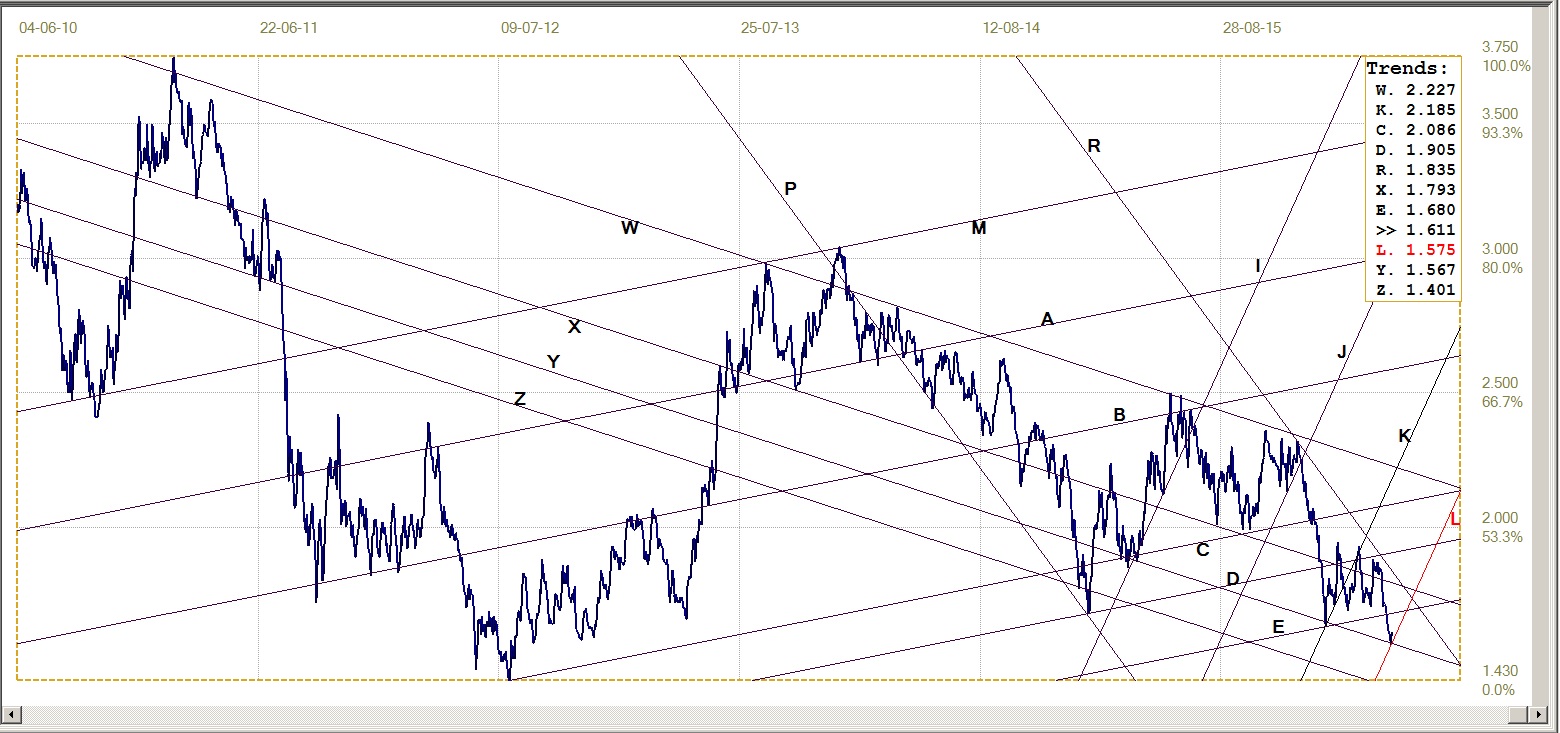

Silver Daily Fix Chart

Silver daily fix, last = $17.37 (www.kitco.com)

The recent adjustment when the new silver bull channel – with a shallower gradient than the original bull channel – proved to perfectly accommodate recent weakness and act as a springboard for the new rally. The move higher off line L ($16.22) has led gold higher, setting the example by breaking above nearby resistance already a week ago, which gold has now followed. Bullish still while support at line R ($16.69) and line D ($16.91) holds.

US 10-year Treasury Note

Last week, the recent bull market in the 10-year US Treasury note carried the yield to a new low value at 1.594% on Wednesday. It is said that fear of Brexit is behind the weak performance of Wall Street that is fuelling a flight to the traditional bond safe haven. Fed indecision and uncertainty about rates also contribute to the rising demand for Treasuries. However, there are voices being heard warning of a bond bubble, and if Brexit does not happen, that bubble could pop, at least a little.

U.S. 10-year Treasury note, last = 1.611% (www.investing.com)

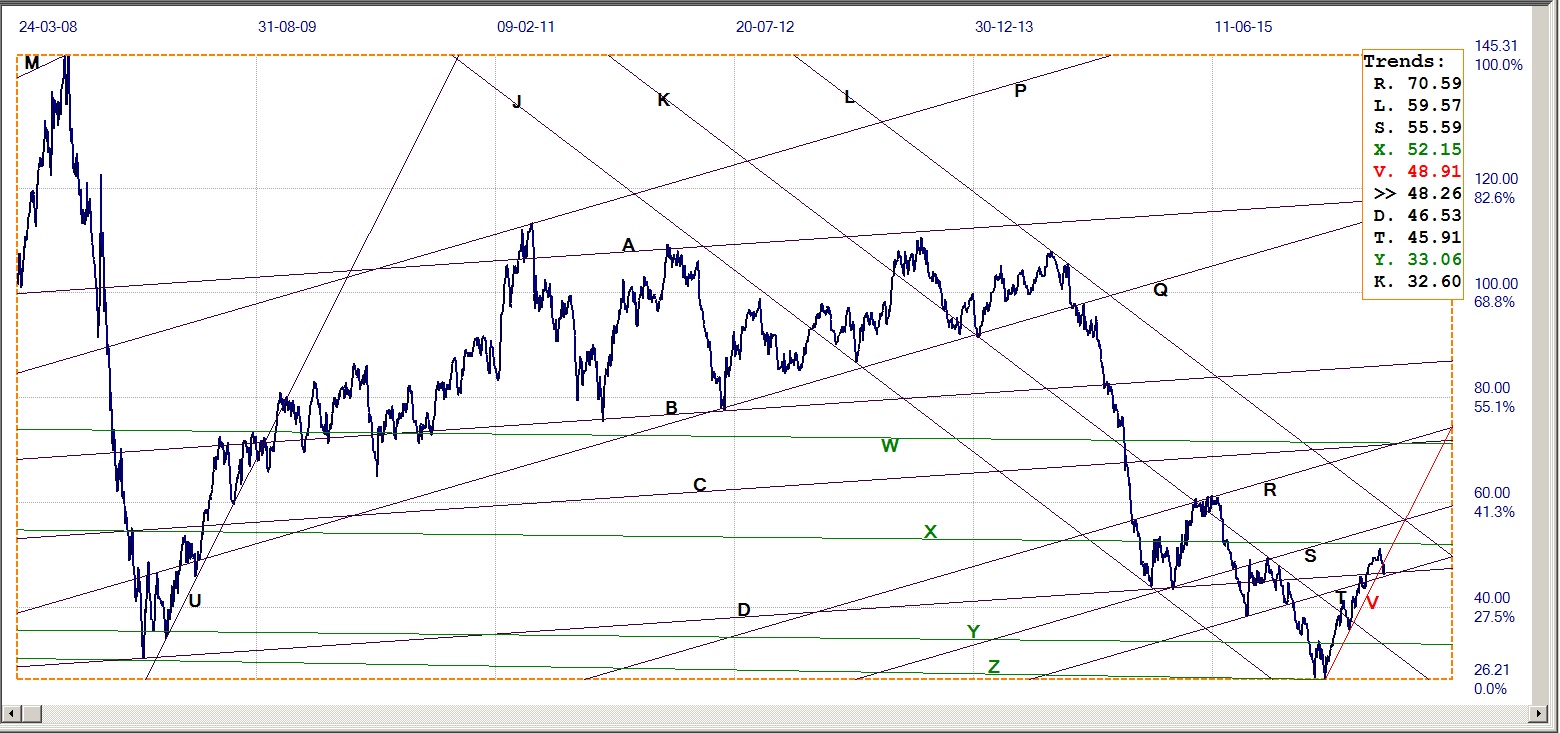

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $48.26 (Investing.com)

Failure to permanently extend the recent rally above the $50 level and signs that demand is still less than the supply, has brought the price of crude back to below $50/bbl and in the process broke below the steep support of channel UV ($48.91). The break lower is still small and it would not take much to recover back into the channel, at least while the support at lines D ($46.53) and T($45.91) holds.

A break lower would be bearish for the near term and perhaps longer, as there is no nearby support. Such an event would imply that global demand is not enough to take on the supply and be a storm warning for the global economy and in particular that of the west.

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com

More from Gold-Eagle