Evil Market Omens Seen In The Dow Jones’ Earnings And Dividends

The Dow Jones has seen a nice recovery off its credit crisis lows of March 2009. In the last 4.5 years it’s up about 138%. Don’t you wish you had bought stocks on the 09 March 2009 bottom? It’s easy to say that today, but in March 2009 the only people buying stocks in any significant manner worked for the big Wall Street banking firms who were using inflationary funding flowing from the Federal Reserve. Trading volume exploded during the 2007-09 decline, but that isn’t supposed to happen during historic bear markets. Had the Federal Reserve and US Treasury not supported the debt and stock markets with a massive multi-trillion dollar buy-side intervention (with Congressional approval), the NYSE could have become a no bid market for many of its listed companies, especially insolvent financial companies like the big Wall Street banks. Had the Plunge Protection Team not fully committed itself in March 2009, the decline in the Dow Jones seen in the chart below would not have stopped at 6500!

So what’s my beef with the stock market today? Aren’t earnings for the Dow Jones at historic record highs? They are, but that was also true in November 2007 at the housing-bubble top, as we see in the red box below. In the next nine months, the Dow Jones’ earnings collapsed from $844 to -$109, an almost $1,000 earnings free-fall for the thirty blue chip stocks contained in the Dow Jones. Nothing like that has happened in the Dow Jones earnings since the 1929-32 Great Depression crash.

The S&P 500, a larger and so a better sample for American blue-chip companies trading in the stock market, also saw its earnings collapse during the credit crisis crash (chart below). Like the upswing in the Dow Jones’ post credit crisis earnings, the S&P 500 earnings are also at historic highs just a few years after their historic collapse.

How does something like this violent collapse and recover in corporate earnings happen? I can’t say for sure, but I suspect the big Wall Street banks had been selling derivatives to “hedge risks” to their captured clients in the Dow Jones and the S&P 500. Gambling losses are an excellent way to consume anyone’s income. But then, gambling winnings are also a great way to get back what one has lost, especially when the house is on your side. What else but derivatives can one explain not only the traumatic decline in earnings from 2007-08, but the amazing resurrection in corporate earnings from 2009 to today. After all, for companies selling widgets and services, business has been horrible for the past five years.

Go back to my first chart’s insert charting the Dow Jones earnings from 1929 to 1972. The 1940s and early 1950s were an excellent period for American business. There had been a world war where all our competition were bombed into the Stone Age; corporate America never had it so good. But after the Dow Jones’ earnings bottomed in 1933, their earnings didn’t return to their 1929 levels for another two decades. Compared to what happened from 1933 to the early 1950s, business conditions today are lousy, yet earnings recovered quickly.

So, how do large blue-chip companies’ earnings increase as they have since 2009? Seeing these large companies recoup their earnings so easily after such a traumatic collapse, and then go on to new record earnings in so little time, gives reasonable people cause to doubt the sincerity of current corporate accounting standards. That and unrealized gambling profits from derivatives posing to be assets on these companies balance sheets are the only answer I can think of for such a rapid recovery. Whether such a strategy would generate much in the way of actual cash flow is doubtful. What is also doubtful is how resilient corporate America’s earnings will prove to be when Mr Bear comes back to stress test the stock market.

Why would the “policy makers” make the effort in recouping earnings so quickly after the 2007-09 collapse? Because the Greenspan Fed and CNBC made earning trends the holy grail of stock analysis in the early 1990s. If you look at the upper part of the chart below, we see the relationship between stock valuations (Blue Plot) and earnings trends (Red Plot) as CNBC would have us believe them to be; where earning trends drive stock valuations. But is this true? Well, this certainly has been the case since Greenspan began inflating his bubble in the stock market in the 1990s. As a result, market watchers today have an earnings fetish where they not only want to buy stocks on earnings increases, but sell them on earning declines. This makes rising earnings very important to anyone who wants to ratchet up market valuations.

But before Greenspan and CNBC began their focus on earning trends; trends in earnings had little to do with valuation trends for stocks from 1929 to 1992. That’s not to say that earnings and valuation trends didn’t sometimes rise and fall together, they could. But more times than not their relationship were more like we see in the bottom of the chart above. This was especially so when trends in the stock market’s valuation made a major reversal, up or down.

Let’s look at some charts, and for your information I didn’t download this data from an internet source. I personally went to college libraries and hand entered the following data from dusty old issues of Barron’s. This data is as seen by readers of Barron’s from long ago. Any Barron’s reader from 1929 to 1944 who used Dow Jones’ earnings trends to time their entry and exit points in the market could not have survived the Great Depression intact.

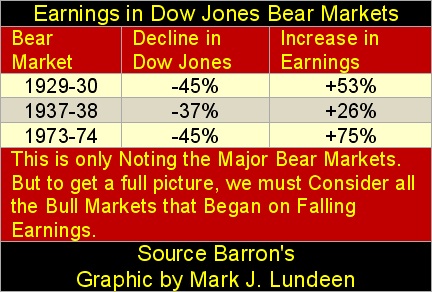

I won’t bore you with the details as a quick look at the chart below tells all. But note that the great crash of October 1929 occurred on rising earnings (table below). In fact, the Dow’s earnings continued to rise to record highs as its valuation declined 50% by October 1930. The best year in the Dow Jones history occurred from July 1932-33, as the Dow Jones’ earnings actually went negative. When the Dow Jones once again saw its earnings become positive in 1933, the bull’s party was over. Did following trends in the Dow Jones earnings help investors avoid the pitfalls in the market from 1929 to 1944? No!

As we see below, from 1929-42, using earnings trends (Red Plot) to market time entry and exit points for the Dow Jones’ (Blue Plot) kept investors in the market during three massive bear markets and kept them out of the market when significant capital gains were to be had.

With few exceptions, this was true from 1929 to 1990. Here’s my favorite chart for the Dow Jones and its earnings (1968-79). From January 1973 to December 1974 the Dow Jones saw its first 40% market decline since April 1942, on robust earnings growth. During this ten year period, earnings trends proved to be total disaster in timing entry and exit points in the market. Today’s “market experts” may focus on earnings to predict future price trends in the market. But before the 1990s, that wasn’t the case at all for the obvious reasons seen in these two charts.

Below is a link for a Gold Eagle article I wrote a few years ago on this subject which contains more charts on the Dow Jones and its earnings from 1929 to 2011. After studying this history, you may agree with me that the current coupling of earnings with price trends is no small point in determining whether or not the financial markets’ valuations have been managed since Alan Greenspan became Chairman of the Federal Reserve.

Here is a historical fact most people are unaware of today; Charles Dow invented his Dow Jones’ Average in the 1880s to predict future business conditions, not as a tool for speculation in the stock market. In other words, he believed price trends in the stock market, as measured by his averages, predicted future earnings trends, or “business conditions” as Mr. Dow would have said it. So originally, the Dow Jones Average was created to assist businessmen in anticipating recessions during the good times and business recoveries during recessions.

This was no small thing; no businessman wants to assume debt to expand their production lines when an economic contraction is approaching. When looking at these charts from this stand point, where the blue price plot predicts what the red earnings plot is going to do, this actually works as Charles Dow would have it, or did until Alan Greenspan became Fed Chairman. The current market rigging has clouded the judgment of business executives and investors.

- Central banks are now so heavily influencing asset prices that investors are unable to ascertain market values. This influence is especially evident, with the Fed's purchase of government bonds, which has made it impossible for investors to use bond prices to learn anything about markets.

- Kevin M. Warsh: Former Federal Reserve Governor. Comments made to the Stanford University Institute for Economic Policy Research, 25 Jan 2012.

Wall Street has seen huge changes since 1885 when Charles Dow first computed his Dow Jones Average. Back then people bought stocks not so much for capital gains as for dividend income; income that was higher than what bonds provided. But as everyone knew back then, if not now, with higher rates of return comes higher risks of income disappointments or even default. Dividend income had risks bonds did not, as dividend payouts could be reduced or completely eliminated at the whim of the company with no legal recourse for stock holders. This wasn’t true for bonds. If a company could not make a coupon payment on its bonds, it risked liquidation for the benefit of its bond holders. Or did until President Obama “liquidated” GM’s and Chrysler’s bond holders in 2009 for the benefit of his union political supporters during the auto manufactures’ recent bankruptcy.

In the chart below plotting the Dow Jones dividend yield (Blue Plot) and Barron’s Best Grade Corporate Bond Yield (Red Plot), we see how the market priced income risk; stocks yielded more than bonds from the 1930s to the late 1950s. Dividend yields were much higher than corporate bond yields. What happened in 1958 that made bond yields soar far above dividend yields? “Monetary policy” became inflationary, resulting in a run on the US gold reserves. Fixed income financial instruments such as bonds were devastated by the resulting rising consumer prices.

As a result of inflation concerns, bond buyers have demanded an inflation premium far above the Dow Jones’ dividend yield since 1958. But even so, investing in bonds has been a sucker’s game for decades because their principle and fixed interest payments are totally exposed to the ravages of monetary inflation.

Since Paul Volcker “slayed the inflationary dragon” in the early 1980s, we all know that consumer inflation has been under control. But looking at bond yields in the chart above, it’s fair saying that the bond market isn’t totally convinced that this is actually the case.

However, stock dividend payouts are not fixed. Not only can a company decrease or completely discontinue its dividend payouts, they can also increase them. In the chart below we see what the Dow Jones Industrials companies have done with their dividend payouts since 1925. Here is why dividend yields have fallen below bond yields since 1958; stocks with their increasing dividend payouts and rising share prices have proven to be a superior vehicle for investment income during our inflationary era.

So does this fact make today’s dividend paying blue-chip stocks a suitable investment for income seekers? I would say no, and for the same reason that bonds are not; today’s “monetary policy” is highly inflationary. Currently, I don’t believe there is a safe income investment.

Long ago, dividend yields for the Dow Jones provided an effective rule of thumb for investors when to time their entry and exit points into the stock market. When the Dow Jones dividend yield increased above 6%, the worst part of a bear market was over and it was time to buy. When the Dow Jones’ dividend yield fell to 3%, the best part of a bull market was over and it was time to get out, and stay out of the market until once again the Dow Jones was again yielding 6%. As with other old market rules, things changed when Alan Greenspan became Chairman of the Federal Reserve. How thoroughly the old Dow Jones dividend rule of thumb has been brushed aside by “policy” can be seen in the chart below.

Look at the Dow Jones 3% yield line. From 1925 to 1987 (62 years) it was the kiss of death for every bull markets that touch it. Now understand that seeing the Dow Jones dividend fall to 3% doesn't produce an instantaneous bear market crash. But for someone who entered the market when the Dow Jones was yielding over 6%, a 3% Dow Jones dividend signaled that the lion’s share of capital gains the bull market would produce were then priced into the market, and it was time to go. It’s interesting noting that the last time the Dow Jones signaled a 3% dividend sell signal was for the market crash of October 1987. Before the October 1987’s market crash the Dow Jones dividend yield first fell below 3% in March of 1987.

Obviously, anyone who sold in March 1987 on the Dow Jones’ 3% dividend rule of thumb, and has been waiting for the Dow Jones to once again yield 6% has had a long wait. Today it’s mostly forgotten, but in December 1996 Alan Greenspan from out of nowhere, gave a speech that shocked the investment world on of all things “irrational exuberance”.

"But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade?"

- Alan Greenspan, from his Irrational Exuberance speech, 5 December 1996

http://www.irrationalexuberance.com/definition.htm

Note how Greenspan blamed investors’ “irrational exuberance” rather than his inflationary “monetary policy” for rising asset prices. Well it’s like Alan Blinder told viewers of PBS’s Nightly Business Report when he became the Federal Reserve’s Vice Chairman:

“The last duty of a central banker is to tell the public the truth.”

- Alan Blinder, Vice Chairman of the Federal Reserve

Returning to Greenspan, what was it that caused Alan Greenspan to give such an unexpected speech to the market’s bulls in December 1996? Unlike Doctor Bernanke who is totally insensitive to market nuance, I suspect that Alan Greenspan was very aware of the Dow Jones’ sell on a 3% yield rule of thumb. On 05 December 1996 when he gave this speech, the Dow Jones was yielding a historic 2.03%, and Greenspan knew what that meant; that the Dow Jones then at 6437.10 was grossly overvalued. I suspect that Alan Greenspan was more than a little concerned when a month later the Dow Jones saw its dividend yield decline below 2% for the first time in history. At its high-tech market top in January 2000 (11,722.98), the Dow Jones yielded an “irrationally exuberant” 1.30% as seen in the chart above.

Now on matters of market mathematics, stock market bulls are dumb as dirt when it comes to computing dividend yields. The only thing bulls care to calculate is the percentage returns on their capital gains. There was even an academic who at the turn of the century wrote a best-selling book predicting a 36,000 Dow Jones. Like other bulls, did he take the sub 2% yield on the Dow Jones into consideration? Not likely!

But this is not true for Mr Bear who has a Ph.D. in dividend studies. The last time the Dow Jones yielded 6% was on 05 September 1982. Except during the credit crisis bottom of 2009, it has been below 3% since 07 May 1993. For over two decades Greenspan’s “irrational exuberance” (with massive assistance from the Federal Reserve) has pushed stock-market valuations deep into bubble territory, and they still are today. Currently the Dow Jones is now near its all-time high as it yields only 2.16%. But when the Dow Jones bottomed on 09 March 2009 at 6,547, its dividend yield had increased to only 4.74% on a dividend payout of $310. This less than 6% Dow Jones’ yield resulted in the second deepest bear market since 1885, so even then the stock market was still overpriced by historical bear market dividend standards.

We can use the table below to see what would have happened to the Dow Jones’ valuation had Mr Bear been allowed to force the Dow Jones to raise its dividend yield up to its old-bear market terminating dividend yield of 6%. A 6% yield with a $300 dollar dividend payout = 5,000 on the Dow Jones; a bear market decline of 64.4% from the Dow Jones’ October 2007 top of 14,043 - ouch! Had dividend payouts declined 30% to $200, which could have easily happened had the stock market been left to its own resources, a 6% yield would have dropped the Dow Jones down to 3,333, or a 73.26% bear market bottom. This relationship between dividend yields, payouts and valuations are mathematical. Bulls choose ignore them, but Mr Bear lives by them.

But big bear markets don’t just see an increase in their dividend yields, but also suffer from declines in their dividend cash payouts too. Go back to Dow Jones dividend payout chart. In September 2008, just weeks before the crash, the Dow Jones paid out $328.39 in cash. But by February 2010 (a year after the bottom), the Dow Jones dividend payout had declined 17%, to $271.79.

But this was nothing to what happened to investors during the 1929-32 market crash, where Dow Jones dividend yield increased from 2.88% to 10.37% as its dividend payout declined 80%. The result was a historic 89% decline in the Dow Jones that’s remembered to this day. The chart below displays the grizzly dividend graphics of the Great Depression’s crash.

Now I say again that stock market bulls don’t give a damn about any of this, and they won’t until their capital gains are only distant memories. But as I see our current market situation, Alan Greenspan committed an act of moral turpitude when he allowed the Dow Jones’ dividend yield to decline to 1.30% in January 2000 – and he knows it too. How this will impact future market valuations will depend on how far Mr Bear can drive the Dow Jones’ dividend yield up toward 6% and maybe much higher, and the decline in dividend payouts in the years to come.

From a historical dividend perspective, this bear market started in January 2000 when the Dow Jones Dividend yield bottomed at 1.30% and will not end until the Dow Jones once again yields something over 6%. If the Dow Jones’ valuation has since twice gone on to new all-time highs in 2007 and now, it’s only because college professors from Ivy League Universities have substituted the market’s realities with their academic fantasies via the Federal Reserve’s Open Market activities. But if you believe in the return to the mean in the financial markets’ parameters, you must then believe that one day we will again see the Dow Jones’ yielding over 6% before this bear market is over.

Today, nothing in the market is real, except maybe for dividend cash payments to shareholders. I say maybe as payouts are supposed to come from a company’s profits, not from the proceeds from issuing new bonds in the market, which I read is happening today, as is using debt to finance stock buyback programs to keep share prices high. The potential for future reductions in dividend payouts to fund these bonds’ coupon payments is huge! The impact this would have on the valuation of the Dow Jones can be seen in the dividend table above.

Giving credit where credit is due, I want to say thank you to Alan Greenspan and Doctor Bernanke, as well to the host of politicians, government regulators and Wall Street bankers, for creating the necessary conditions for us to experience another Great Depression crash. When or not this happens, we will just have to wait to see; but everything is in place for it to happen.

Mark J. Lundeen